Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Singapore Industrial Automation Market generated approximately USD ~ billion in economic activity based on a recent historical assessment, supported by extensive deployment of robotics, programmable logic controllers, distributed control systems, and industrial software across manufacturing facilities and logistics infrastructure. Data published by the Singapore Economic Development Board and the International Federation of Robotics highlights strong industrial investment in semiconductor fabrication plants, electronics manufacturing lines, and precision engineering facilities, which collectively drive demand for advanced automation technologies that improve manufacturing efficiency, operational accuracy, and process control.

Singapore’s industrial automation ecosystem is concentrated within advanced manufacturing districts where semiconductor fabrication plants, electronics assembly facilities, and high precision engineering manufacturers operate integrated production lines requiring robotics and digital control technologies. Jurong Industrial Estate, Tuas Industrial Zone, and Changi Business Park host major clusters of electronics manufacturers, semiconductor fabrication facilities, and biomedical production plants that deploy automation technologies to manage complex production processes. Government industrial transformation programs also encourage companies to adopt robotics, industrial analytics platforms, and smart manufacturing technologies to strengthen national manufacturing productivity and technological competitiveness.

Market Segmentation

By Product Type

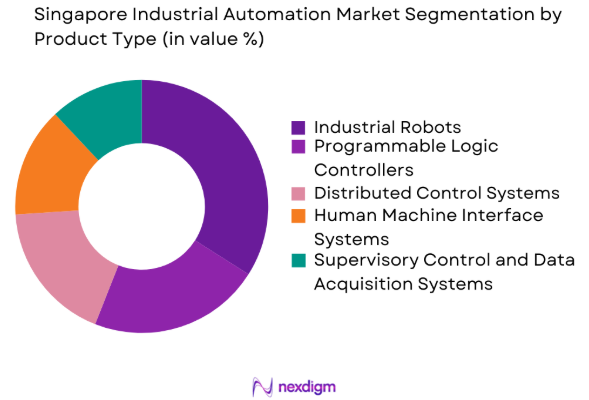

Singapore Industrial Automation market is segmented by product type into industrial robots, programmable logic controllers, distributed control systems, human machine interface systems, and supervisory control and data acquisition systems. Recently, industrial robots has a dominant market share due to strong adoption across semiconductor fabrication plants, electronics manufacturing facilities, and high precision engineering production environments operating within Singapore’s advanced manufacturing sector. Robotics systems allow manufacturers to maintain extremely high precision required for semiconductor wafer fabrication and microelectronics assembly operations. Industrial robots also reduce dependence on manual labor in complex electronics manufacturing lines while maintaining consistent product quality. Global automation suppliers support robotics integration through collaborative robots, machine vision inspection systems, and automated material handling technologies designed for semiconductor and electronics manufacturing clusters.

By End-User Industry

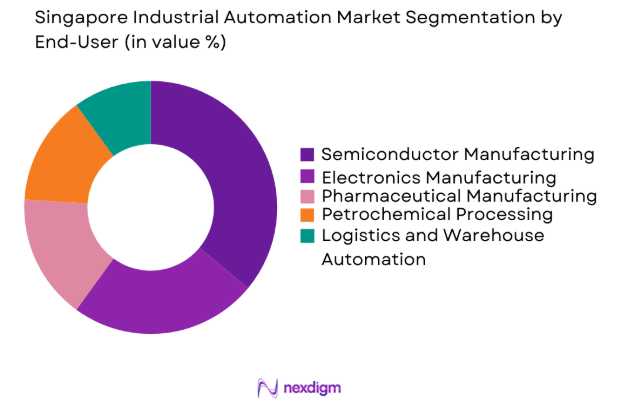

Singapore Industrial Automation market is segmented by end user industry into semiconductor manufacturing, electronics manufacturing, pharmaceutical manufacturing, petrochemical processing, and logistics and warehouse automation. Recently, semiconductor manufacturing has a dominant market share because Singapore operates as a global semiconductor manufacturing hub hosting multiple wafer fabrication facilities operated by international semiconductor companies. Semiconductor production requires extremely precise automation systems capable of managing wafer processing, photolithography equipment, chemical deposition processes, and automated wafer transport systems. These facilities deploy robotics, programmable controllers, automated inspection systems, and digital process monitoring platforms designed to maintain extremely precise manufacturing environments. Global demand for semiconductor chips used in artificial intelligence systems, consumer electronics, automotive electronics, and data center infrastructure continues driving automation investments within semiconductor fabrication facilities across Singapore’s industrial manufacturing zones.

Competitive Landscape

Singapore Industrial Automation market demonstrates moderate consolidation where global automation technology companies compete through robotics systems, industrial control platforms, and smart manufacturing solutions. Leading automation providers maintain regional headquarters, engineering centers, and integration facilities within Singapore, enabling them to supply advanced automation technologies to semiconductor fabrication plants, electronics manufacturing facilities, and precision engineering companies across Southeast Asia. Competition largely focuses on robotics innovation, digital factory platforms, industrial analytics capabilities, and turnkey smart manufacturing automation systems.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Industrial Automation Capability |

| Siemens | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

| ABB | 1883 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Schneider Electric | 1836 | France | ~ | ~ | ~ | ~ | ~ |

| Rockwell Automation | 1903 | United States | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Electric | 1921 | Japan | ~ | ~ | ~ | ~ | ~ |

Singapore Industrial Automation Market Analysis

Growth Drivers

Expansion of Semiconductor Fabrication and Electronics Manufacturing Infrastructure

Singapore’s advanced manufacturing sector strongly drives demand for industrial automation technologies because semiconductor fabrication plants and electronics assembly facilities rely on robotics systems, programmable controllers, automated inspection platforms, and digital manufacturing software capable of maintaining highly precise production environments. Semiconductor wafer fabrication involves complex processes including photolithography, ion implantation, chemical vapor deposition, and wafer etching that require automation systems capable of continuously monitoring production conditions. Global semiconductor companies operating fabrication facilities in Singapore deploy robotic wafer transport systems, distributed process control platforms, and automated quality inspection technologies to maintain defect free manufacturing. Electronics manufacturers also deploy robotics assembly lines, automated testing equipment, and digital production monitoring systems to support global semiconductor and electronics supply chains.

Adoption of Smart Manufacturing and Industrial Digitalization Programs

Singapore’s national industrial transformation strategy encourages widespread adoption of digital manufacturing technologies including robotics systems, artificial intelligence enabled automation, industrial analytics platforms, and industrial internet of things infrastructure across manufacturing sectors. Government supported initiatives promote smart factory deployment where industrial sensors, robotics platforms, cloud computing infrastructure, and analytics solutions optimize manufacturing operations through real time monitoring and predictive maintenance. Automation vendors collaborate with manufacturers to build integrated production environments where machines communicate through industrial networks that enable automated process control and data driven decision making. Digital manufacturing improves production throughput while reducing downtime, operational errors, and energy consumption. Companies also deploy collaborative robotics and industrial analytics platforms to enhance operational efficiency and predictive maintenance across modern manufacturing facilities.

Market Challenges

High Capital Investment Requirements for Advanced Industrial Automation Systems

Industrial automation deployment within advanced manufacturing facilities requires substantial financial investment because robotics systems, programmable controllers, industrial networking equipment, and digital manufacturing software platforms involve high procurement, installation, and system integration costs. Semiconductor fabrication plants and electronics manufacturing facilities deploy extensive automation equipment including robotic arms, motion control systems, programmable logic controllers, automated inspection machines, and industrial sensors connected through advanced industrial communication networks. These systems must operate with exceptional precision and reliability because equipment downtime can cause significant production losses. Automation deployment also requires specialized engineering expertise to integrate robotics platforms with existing machinery, manufacturing execution systems, and process control platforms. Continuous maintenance, software upgrades, and system monitoring further increase operational costs for manufacturers.

Integration Complexity with Legacy Manufacturing Infrastructure and Workforce Adaptation

Many manufacturing facilities still operate legacy production equipment designed before widespread digital automation adoption, creating integration challenges when companies attempt to deploy modern automation systems. Older machines often use outdated control systems and communication protocols that cannot easily connect with robotics platforms or digital manufacturing software. Automation engineers therefore develop customized integration solutions that link new automation technologies with existing machinery while avoiding production disruptions. Each facility contains unique combinations of equipment and software that require careful configuration within integrated automation architectures. Workforce adaptation also becomes challenging because employees must learn new skills related to robotics operation, industrial networking, and digital analytics platforms. Companies therefore invest in training programs that help employees transition toward managing automated manufacturing environments effectively.

Opportunities

Expansion of Collaborative Robotics Deployment Across Advanced Manufacturing Facilities

Collaborative robotics technology creates strong opportunities within Singapore Industrial Automation market because collaborative robots are designed to work safely alongside human workers in manufacturing environments that require flexible automation. Unlike traditional industrial robots operating inside safety cages, collaborative robots use sensors, machine vision, and safety software to detect human presence and adjust movements to prevent accidents. Manufacturing companies increasingly adopt collaborative robots for repetitive assembly tasks while human operators supervise complex production processes. Electronics manufacturing facilities benefit particularly from collaborative robots because they ensure precise placement of microelectronic components during assembly operations. These robots also require fewer infrastructure changes compared with traditional robotic systems, reducing deployment costs and simplifying integration within existing manufacturing facilities while expanding automation adoption.

Growth of Automated Logistics and Smart Warehouse Infrastructure Supporting Global Trade

Singapore functions as a major international logistics hub connecting global maritime trade routes and air cargo networks, creating strong demand for warehouse automation technologies capable of handling high shipment volumes across distribution centers and logistics facilities. Automated logistics infrastructure including robotic warehouse systems, automated storage and retrieval equipment, conveyor networks, and digital inventory management platforms enables logistics operators to process shipments efficiently while reducing operational delays in high volume distribution environments. Rapid expansion of electronic commerce across Asia further increases parcel movement through logistics hubs, encouraging companies to deploy automation technologies for faster sorting, storage, and dispatch operations. Autonomous mobile robots transport goods inside warehouses while communicating with centralized inventory management systems that monitor shipment flows and inventory levels.

Future Outlook

Singapore Industrial Automation market is expected to expand steadily as manufacturers continue investing in robotics, artificial intelligence enabled automation platforms, and digital manufacturing technologies designed to improve operational efficiency and global competitiveness. Semiconductor fabrication expansion, smart factory initiatives, and logistics automation projects will continue supporting automation demand. Government digital transformation programs and investments in advanced manufacturing technologies will accelerate automation adoption across industrial sectors. Integration of robotics, industrial analytics, and industrial internet of things platforms will further modernize Singapore’s manufacturing ecosystem.

Major Players

- Siemens

- ABB

- Schneider Electric

- Rockwell Automation

- Mitsubishi Electric

- Omron Corporation

- Honeywell International

- Emerson Electric

- Yokogawa Electric Corporation

- Bosch Rexroth

- Fanuc Corporation

- Yaskawa Electric

- Delta Electronics

- Beckhoff Automation

- Advantech

Key Target Audience

- Semiconductor manufacturing companies

- Electronics manufacturing companies

- Industrial automation equipment manufacturers

- Logistics and warehouse operators

- Pharmaceutical manufacturing companies

- Petrochemical processing companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key industry variables including automation adoption rates, manufacturing investment, robotics deployment levels, and industrial production capacity were identified. Industrial policy initiatives, manufacturing infrastructure expansion, and automation technology supply chains were also analyzed to determine primary market indicators.

Step 2: Market Analysis and Construction

Extensive secondary research using government manufacturing statistics, industrial automation reports, and robotics industry publications was conducted. Market structure, value chain relationships, and automation technology adoption across manufacturing sectors were evaluated.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including automation engineers, semiconductor manufacturing executives, and robotics integration specialists were consulted to validate market assumptions. Their insights refined technology adoption patterns and investment trends across Singapore’s advanced manufacturing ecosystem.

Step 4: Research Synthesis and Final Output

All research findings were consolidated through comparative evaluation of multiple industry data sources. Final market estimates, segmentation structures, and industrial insights were synthesized to produce a comprehensive industrial automation market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Semiconductor Manufacturing and Electronics Production

Government Smart Industry and Digital Manufacturing Initiatives

Rising Adoption of Industrial IoT and Smart Factory Technologies - Market Challenges

High Capital Investment Requirements for Automation Infrastructure

Integration Complexity with Legacy Manufacturing Systems

Workforce Skill Gaps in Advanced Automation Technologies - Market Opportunities

Growth of Smart Factory Deployments Across Advanced Manufacturing

Integration of Artificial Intelligence in Industrial Automation Systems

Expansion of Automated Logistics and Warehouse Operations - Trends

Increasing Deployment of Collaborative Robots in Manufacturing

Integration of Edge Computing with Industrial Automation Platforms

Expansion of Predictive Maintenance Technologies in Industrial Facilities - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Industrial Robots

Distributed Control Systems

Programmable Logic Controllers

Human Machine Interface Systems

Supervisory Control and Data Acquisition Systems - By Platform Type (In Value%)

Manufacturing Automation Platforms

Process Automation Platforms

Robotics Integration Platforms

Industrial IoT Automation Platforms

Smart Factory Automation Platforms - By Fitment Type (In Value%)

New Industrial Installations

Retrofit Automation Systems

Modular Automation Integration

End-to-End Turnkey Automation

Hybrid Automation Deployment - By End User Segment (In Value%)

Semiconductor Manufacturing Facilities

Electronics Assembly Plants

Petrochemical Processing Industries

Pharmaceutical Manufacturing Facilities

Logistics and Warehouse Automation Centers - By Procurement Channel (In Value%)

Direct Industrial Procurement

Engineering Procurement and Construction Contracts

System Integrator Partnerships

Government Industrial Development Projects

Industrial Equipment Distributors

- Market Share Analysis

- Cross Comparison Parameters (Automation Technology Portfolio, Industrial Robotics Capability, System Integration Expertise, Smart Factory Solutions, Regional Manufacturing Presence)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Siemens

ABB

Schneider Electric

Rockwell Automation

Mitsubishi Electric

Omron Corporation

Honeywell International

Emerson Electric

Yokogawa Electric Corporation

Bosch Rexroth

Fanuc Corporation

Yaskawa Electric Corporation

Delta Electronics

Beckhoff Automation

Advantech

- Semiconductor fabrication plants increasing deployment of robotics and automated wafer handling systems

- Electronics manufacturing companies integrating advanced assembly automation and quality inspection systems

- Petrochemical plants implementing distributed control systems and process automation technologies

- Pharmaceutical manufacturers adopting automated packaging and sterile production automation systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now