Download PDF

Download PDFMarket Overview

Singapore RegTech compliance solutions market stands at US$ ~ million, after rising from US$ ~ million in the prior year. Growth is being supported by a stricter compliance environment, continued MAS backing for RegTech adoption, and rising digital-finance complexity. MAS has maintained a dedicated RegTech support track and earlier committed S$42 million to accelerate technology adoption in risk management and compliance. Public ecosystem mapping also shows Singapore has an estimated 900 fintech firms, with RegTech representing 15% of the landscape.

Within Singapore, the heaviest concentration of RegTech demand sits around the CBD, Marina Bay, and Raffles Place because these districts house the largest concentration of banks, insurers, capital-markets firms, and regional compliance teams. Singapore also dominates as an ASEAN compliance hub because MAS provides regulatory clarity, the ecosystem is dense, and the city-state attracts international decision-makers: the Singapore FinTech Festival drew 65,000 participants from 134 countries and regions, including 3,400 government and regulatory attendees from 665 institutions.

Market Segmentation

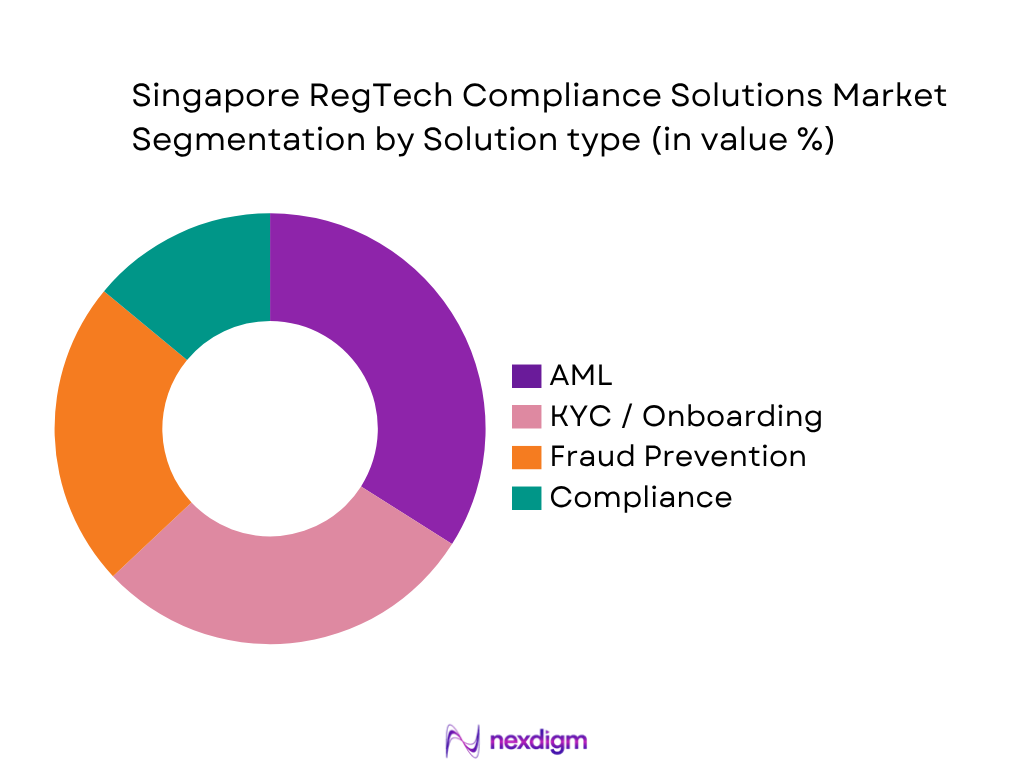

By Solution Type

AML is the leading solution-type segment in Singapore RegTech. That dominance makes structural sense: Singapore’s role as an international financial center means firms face persistent pressure around transaction monitoring, sanctions screening, suspicious-activity escalation, and beneficial-ownership checks. The public risk environment also supports this mix. Singapore’s Commercial Affairs Department reported 85,988 suspicious transaction reports in 2024, showing how fast reporting volumes are scaling and why institutions continue prioritizing AML automation, alert triage, and case management. KYC/onboarding is also substantial because banks and payment firms need faster client activation without weakening screening controls, but AML remains the anchor workload because it touches ongoing monitoring, regulatory reporting, and financial-crime investigations across the full customer lifecycle.

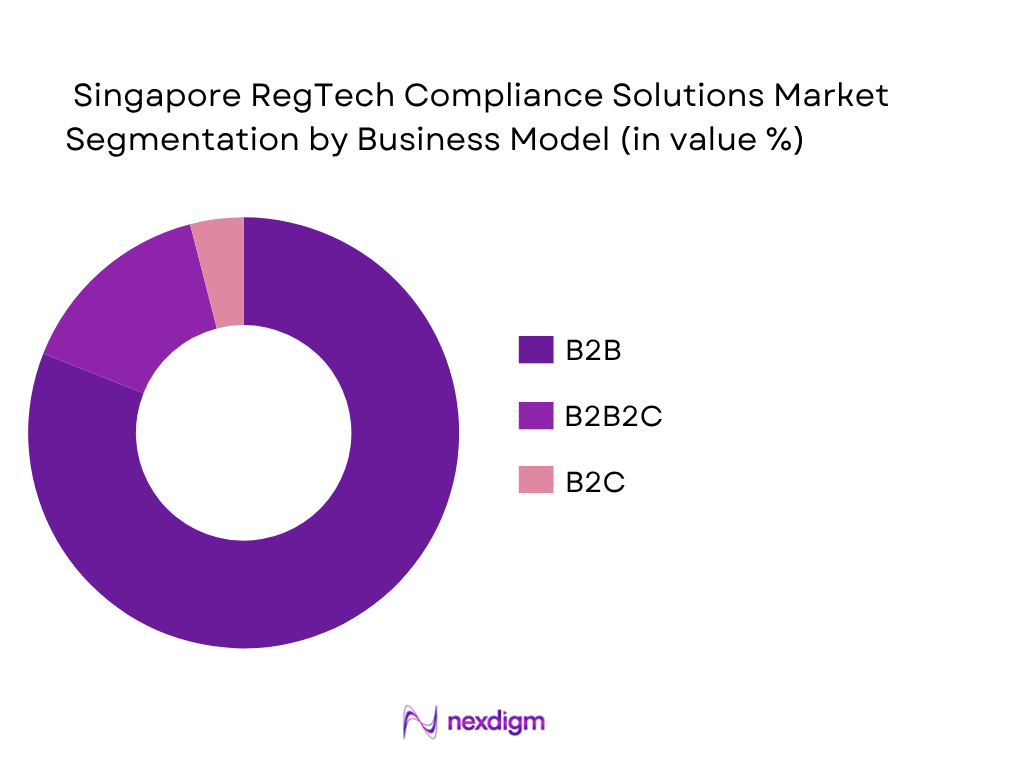

By Business Model

B2B clearly dominates the Singapore RegTech compliance solutions market. That is expected because the main buyers are regulated institutions rather than retail users: banks, insurers, digital banks, payment institutions, brokerages, and enterprise treasury or compliance teams. These buyers need configurable workflows, audit trails, API-based screening, ongoing monitoring, entity resolution, policy-rule engines, and integration into core banking or case-management systems. Singapore’s market structure reinforces this enterprise bias because MAS-regulated firms typically procure tools through formal vendor selection, proof-of-concept, and compliance sign-off cycles. B2B2C remains relevant in identity verification and onboarding-linked workflows where end-customer interaction matters, but the budget holder is still usually the institution. Pure B2C remains niche because end users rarely purchase standalone RegTech products directly in this market.

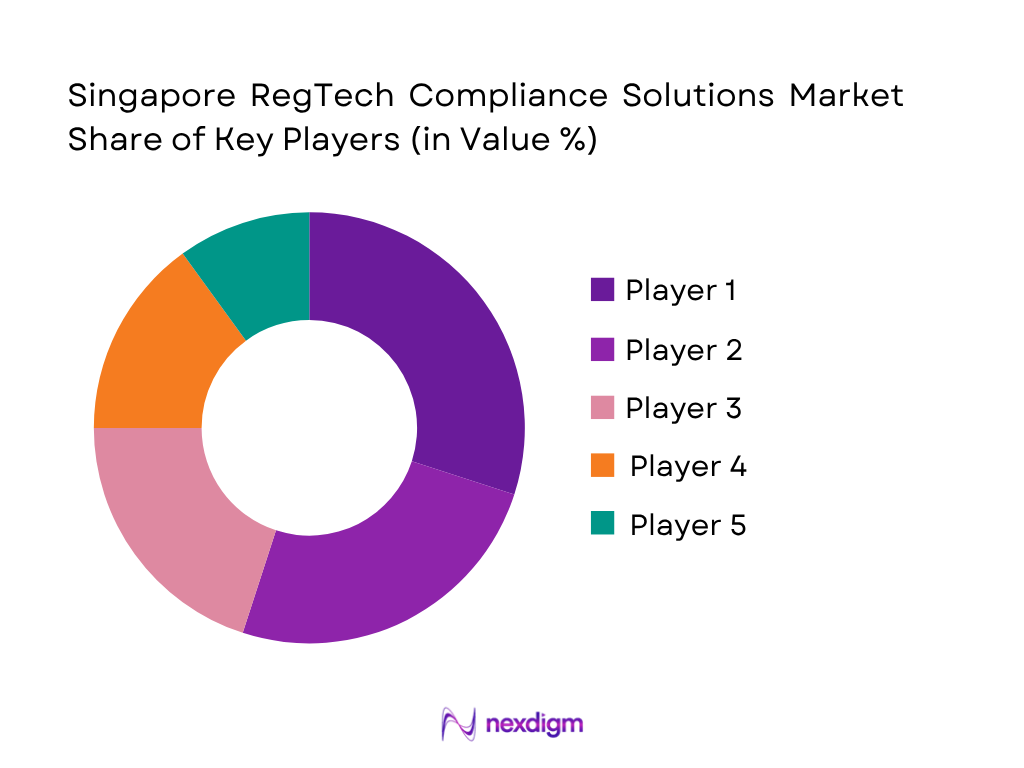

Competitive Landscape

The Singapore RegTech compliance solutions market is shaped by a mix of Singapore-based specialists and international financial-crime-compliance platforms. Local vendors such as Tookitaki benefit from MAS-linked use cases and ASEAN proximity, while global players such as Fenergo, NICE Actimize, LexisNexis Risk Solutions, and ComplyAdvantage compete on data breadth, AI-driven monitoring, client lifecycle management, and enterprise integration depth. The market is relatively concentrated at the upper end because large banks and payment institutions prefer vendors that can support onboarding, screening, transaction monitoring, auditability, and regional regulatory scale from a single platform.

| Company | Establishment Year | Headquarters | Core Market Focus | Key Modules | Primary Buyer Group | Delivery Model | Singapore / ASEAN Relevance | Public Pricing Visibility |

| Fenergo | 2009 | Dublin, Ireland | – | – | – | – | – | – |

| ComplyAdvantage | 2014 | London, UK | – | – | – | – | – | – |

| Tookitaki | 2015 | Singapore | – | – | – | – | – | – |

| NICE Actimize | 1999 | Hoboken, New Jersey, US | – | – | – | – | – | – |

| LexisNexis Risk Solutions | 1997* | Atlanta, Georgia, US | – | – | – | – | – | – |

Competitive Benchmarking Analysis

Singapore RegTech compliance solutions market demonstrates a highly capability-driven competitive structure, where differentiation is not limited to pricing but extends to AI accuracy, regulatory alignment, and operational efficiency gains. Vendors are benchmarked across pricing models, AML/KYC efficiency, regulatory adaptability, and integration capabilities, as financial institutions increasingly prioritize ROI on compliance spend and automation of manual processes. The benchmarking landscape highlights that Singapore-based vendors compete strongly on regional compliance alignment, while global vendors lead in data coverage, scalability, and cross-border compliance capabilities.

Pricing Benchmarking (API Cost, Subscription, Licensing Models)

Pricing across Singapore RegTech vendors is largely non-standardized and enterprise-driven, with most providers adopting hybrid models combining subscription and usage-based pricing. KYC verification costs typically vary depending on jurisdiction coverage and identity data sources, while AML screening pricing depends on transaction volume and alert generation. Vendors such as ComplyAdvantage and Trulioo emphasize API-based pricing for scalability, whereas enterprise platforms like Fenergo follow licensing-heavy models due to full lifecycle integration.

Capability Benchmarking (AML Accuracy, False Positives, AI Models)

Capability benchmarking shows that AI-led platforms outperform traditional rule-based systems in reducing false positives and improving investigation efficiency. Vendors such as Feedzai and Silent Eight are positioned strongly due to machine learning-based detection and automated decisioning. Singapore-specific players like Tookitaki leverage federated learning and consortium-based data sharing, improving detection of regional financial crime patterns.

Regulatory Benchmarking (MAS, FATF, Multi-Jurisdiction Coverage)

Regulatory compliance benchmarking is a key differentiator in Singapore. Vendors are assessed based on their alignment with MAS AML/CFT frameworks, FATF standards, and cross-border compliance capabilities. Global vendors such as LexisNexis Risk Solutions and Dow Jones Risk & Compliance lead due to extensive global watchlists and sanctions data. However, Singapore-focused firms maintain an edge in localized compliance workflows and faster adaptation to MAS regulatory updates.

Technology & Integration Benchmarking (API, Cloud, Integration Time)

Singapore’s market strongly favors API-first, cloud-native RegTech solutions, driven by digital banking growth and fintech integration requirements. Vendors such as Onfido and Jumio are highly competitive due to fast deployment and seamless onboarding integration. In contrast, enterprise vendors like NICE Actimize focus on deep integration with legacy banking systems, which offers robustness but increases deployment timelines.

Operational Efficiency Benchmarking (Cost-to-Compliance, Automation Rate)

Operational benchmarking reveals that RegTech adoption significantly reduces compliance workload. Institutions adopting automated AML and KYC platforms report improved case resolution speed, reduced manual reviews, and lower compliance operational costs. Vendors offering end-to-end compliance orchestration (onboarding, monitoring, reporting) provide higher value compared to point solutions, as they reduce fragmentation and improve audit readiness.

Scalability & Performance Benchmarking (Transaction Processing, Latency)

Scalability benchmarking is critical in Singapore due to high cross-border transaction volumes. Vendors are evaluated based on their ability to handle real-time transaction monitoring, high-frequency alerts, and low-latency processing. API-driven platforms outperform traditional systems in handling peak transaction loads, especially for payment institutions and digital banks.

Vendor Positioning Benchmark Matrix

| Benchmark Dimension | Global Vendors | Singapore / Regional Vendors |

| Pricing Flexibility | Medium (Enterprise Contracts) | High (API & Modular Pricing) |

| AML Detection Accuracy | High (Global Data Sets) | Medium-High (Regional Focus) |

| Regulatory Coverage | Very High (Multi-Jurisdiction) | High (MAS-Focused) |

| Integration Speed | Medium | High |

| AI/ML Capability | High | High |

| Customization | Medium | High |

| ASEAN Market Fit | Medium | Very High |

| Innovation Speed | Medium | High |

Singapore RegTech Compliance Solutions Market Analysis

Growth Drivers

Digital Banking Licenses Issued

Singapore’s RegTech demand is being structurally supported by the presence of four MAS-issued digital bank licences, with MAS stating that no new digital bank licences are currently being granted. That matters because each licensed digital bank adds a long-duration need for onboarding controls, sanctions screening, transaction monitoring, fraud detection, and reporting infrastructure rather than a short-term licensing event. The broader operating environment also supports this demand: Singapore’s nominal GDP reached US$547.5 billion and GDP per capita reached US$90,689 in 2024, while the national digital economy expanded to S$128.1 billion, equal to 18.6% of GDP. Within that digital base, the Finance & Insurance sector remained the largest contributor to value added from digitalisation, and its digital adoption intensity reached 3.13 out of six measured digital areas. For RegTech vendors, this means licence issuance is no longer just a market-entry story; it is a trigger for sustained spend on automated compliance, model governance, API integrations, and AML controls across a tightly supervised digital-banking cohort.

Cross-Border Transaction Volume

Cross-border transaction intensity is one of the clearest demand drivers for Singapore RegTech compliance solutions because Singapore sits at the center of regional goods, services, FX, and treasury flows. In 2024, Singapore’s total merchandise trade reached S$1.3 trillion, with exports and imports both rising, while its overall services trade reached S$1,021.4 billion, including S$533.7 billion in services exports and S$487.6 billion in services imports. The same year, Singapore’s average daily FX traded volumes exceeded S$1.5 trillion, underlining the scale of international financial flows that need sanctions controls, customer due diligence, source-of-funds checks, and real-time monitoring. The partner mix also increases compliance complexity: services trade links were strongest with the United States, the European Union, Mainland China, Japan, Australia, and ASEAN, meaning institutions operating from Singapore must manage multiple jurisdictions, payment corridors, and reporting standards. This scale of cross-border activity directly raises demand for RegTech platforms that can automate screening, policy checks, exception management, and audit trails at speed.

Market Challenges

False Positive Rates

False positive pressure is a core operating challenge in Singapore because institutions are screening within a very high-volume, high-vigilance environment. MAS has explicitly stated in its transaction-monitoring guidance that financial institutions should use statistical analysis to tune rules and reduce false positives and false negatives, which shows the issue is material at the supervisory level. The problem is magnified by the size of reporting activity: the STRO received 85,988 STRs in 2024, while the banking sector alone contributed 59,945 of them. CAD also reported that STRO’s domestic disseminations increased by 70% in 2024, meaning more intelligence was moving into investigations and enforcement workflows. In parallel, Singapore saw 55,810 scam and cybercrime cases in 2024, with 51,501 being scam cases, increasing pressure on banks and payment institutions to detect bad actors without overwhelming analysts with noise. In practice, this means false positives are not just an accuracy issue; they are a throughput problem that affects analyst capacity, customer onboarding speed, alert-aging, and the ability to identify genuinely suspicious behavior on time.

Integration Costs

Integration remains a major challenge because Singapore’s compliance stack now sits inside a much larger digital and data-intensive financial operating environment. In 2024, Singapore’s digital economy reached S$128.1 billion, while value added from digitalisation in the rest of the economy reached S$86.8 billion. Within this, Finance & Insurance remained the largest contributor to digitalisation value added, and the sector’s digital adoption intensity climbed to 3.13, the highest among all sectors measured by IMDA. That level of digitisation is positive for RegTech demand, but it also raises implementation complexity because new AML, KYC, screening, and monitoring systems must connect with core banking platforms, onboarding systems, payment rails, reporting tools, and third-party data sources. MAS has effectively acknowledged the investment load by committing an additional S$100 million in 2024 under FSTI 3.0 to strengthen AI and quantum capabilities in financial services. Even operational reporting systems are being upgraded for scale: from 26 March 2025, SONAR users could file up to five times more reports in a single entry. The challenge is therefore not just buying software, but integrating RegTech into a rapidly deepening digital finance architecture.

Opportunities

AI Adoption Rate

AI adoption is creating one of the strongest current opportunities for the Singapore RegTech market because the financial sector is already digitised enough to operationalise model-based compliance tools. IMDA reported that among all enterprises, 95.1% had adopted at least one digital area in 2024, while the Finance & Insurance sector recorded the highest digital adoption intensity at 3.13. AI uptake accelerated sharply in the same period: adoption among non-SMEs rose from 44.0 to 62.5, and among SMEs rose from 4.2 to 14.5. At the sector level, Finance & Insurance recorded an AI adoption rate of 22.6, placing it behind only Information & Communications and Professional Services. MAS reinforced this direction by committing an additional S$100 million in 2024 to support quantum and AI capability building in financial services. For RegTech suppliers, that combination matters because it shifts buyer appetite from rule-only compliance tooling toward AI-assisted alert triage, risk scoring, name screening, investigation prioritisation, and fraud pattern detection. The opportunity is immediate because the financial system already has the digital maturity, regulatory pressure, and compute-oriented investment environment needed to absorb AI-led compliance tools.

API Economy Growth

API-led infrastructure is expanding the addressable opportunity for Singapore RegTech because compliance is increasingly being embedded into digital workflows rather than executed as a detached back-office process. IMDA reported that Singapore’s digital economy reached S$128.1 billion in 2024 and that enterprise digital adoption continued to deepen across cloud, analytics, AI, and e-payments. On the financial-data side, SGFinDex had reached 150,000 users, connected 290,000 bank accounts, and facilitated 620,000 data retrievals. MAS also continues to maintain the Financial Industry API Register, while its developer portal frames APIs as a way to simplify access to real-time financial and regulatory data for innovation and automation. The need for API-based compliance is further supported by services-trade structure: Singapore’s services exports reached S$533.7 billion in 2024, and key export categories to major partners included telecommunications, computer and information services and financial services. This creates strong demand for RegTech tools that can be plugged into onboarding journeys, payment orchestration, partner due diligence, transaction monitoring, and real-time reporting through APIs rather than standalone interfaces.

Future Outlook

Singapore RegTech compliance solutions market is positioned for sustained expansion as compliance workloads become more real time, more cross-border, and more data intensive. Demand should remain strongest in AML, onboarding orchestration, sanctions screening, and fraud-compliance convergence. The next phase is likely to be shaped by AI-assisted investigations, cloud-native compliance stacks, stronger policy automation, and embedded controls for digital banks and payment firms. MAS support for AI and advanced financial-sector capabilities, including an additional S$100 million under FSTI 3.0, should further reinforce vendor investment and buyer readiness.

Major Players

- Fenergo

- ComplyAdvantage

- NICE Actimize

- LexisNexis Risk Solutions

- Tookitaki

- Trulioo

- Jumio

- Onfido

- Chainalysis

- Dow Jones Risk & Compliance

- Feedzai

- Silent Eight

- Cynopsis Solutions

- Oracle Financial Services

- Wolters Kluwer

Key Target Audience

- Banks and digital banks

- Payment institutions, remittance firms, and e-wallet operators

- Insurance companies and reinsurance groups

- Asset managers, private banks, brokerages, and wealth platforms

- FinTech, embedded-finance, and neobank platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

- RegTech vendors, compliance-platform integrators, and financial infrastructure providers

Research Methodology

Step 1: Identification of Key Variables

The study begins by mapping the Singapore RegTech ecosystem across regulators, banks, digital banks, payment institutions, insurers, compliance teams, and solution vendors. Secondary research is used to identify the variables that matter most in this market: AML workload, KYC complexity, transaction-monitoring volume, cloud readiness, vendor deployment model, pricing architecture, and MAS-driven compliance requirements. This stage also establishes the market boundary between broader compliance software and narrower RegTech spending.

Step 2: Market Analysis and Construction

Historical market construction is built using country-level Singapore RegTech spending data, public Singapore fintech ecosystem mapping, and open-source vendor intelligence. The analysis then aligns the market with solution categories such as AML, KYC/onboarding, fraud prevention, and compliance automation. Pricing and benchmarking lenses are layered in by comparing delivery models, sales posture, enterprise focus, and module breadth across leading vendors active in the Singapore market.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings are tested against public regulator guidance, vendor case material, and industry survey evidence from Singapore-focused fintech and compliance sources. In a full commercial engagement, this phase would be strengthened through CATI interviews with compliance heads, chief risk officers, procurement leaders, digital-bank operators, and regional financial-crime specialists. The purpose is to validate demand drivers, buying criteria, deployment barriers, and vendor shortlisting logic.

Step 4: Research Synthesis and Final Output

The final stage triangulates market size, ecosystem structure, vendor profiles, and adoption signals into a single strategic view of the Singapore RegTech compliance solutions market. Bottom-up vendor mapping is reconciled with top-down country spending indicators and regulator-led demand drivers. The result is a business-ready output designed for market entry decisions, pricing analysis, competitor benchmarking, partnership screening, and opportunity identification in Singapore and the wider ASEAN corridor.

- Executive Summary

- Research Methodology (Market Definitions and Scope of RegTech Compliance Solutions, Regulatory Coverage Scope (MAS, AML/CFT, FATCA, CRS, PDPA), Pricing Benchmarking Framework (Subscription, Usage-Based, API-Based), Vendor Benchmarking Approach, Primary Interviews with Banks/FinTechs/Compliance Officers, Secondary Research (MAS Guidelines, Annual Reports, Vendor Disclosures), Data Triangulation Model, Limitations and Assumptions)

- Definition and Scope

- Evolution of RegTech in Singapore Financial Ecosystem

- MAS Regulatory Landscape (AML/CFT, KYC, Transaction Monitoring, Risk Management)

- Compliance Lifecycle Mapping (Onboarding to Reporting)

- Value Chain Analysis (Data Providers, API Integrators, RegTech Vendors, Financial Institutions)

- Business Model Evolution (SaaS, API-Driven, Platform-Based Compliance)

- Integration with Banking Core Systems & FinTech Stack

- Growth Drivers (Digital Banking Licenses Issued, Cross-Border Transaction Volume, Compliance Cost Burden, AML Case Volumes)

- Market Challenges (False Positive Rates, Integration Costs, Data Privacy Constraints, Talent Availability in Compliance Tech)

- Opportunities (AI Adoption Rate, API Economy Growth, Embedded Compliance Adoption, RegTech Partnerships)

- Market Trends (AI Model Accuracy, Automation Rate, API Integrations, Cloud Adoption Rate)

- Government Regulations (MAS Guidelines, AML/CFT Directives, PDPA Compliance, FATF Alignment)

- SWOT Analysis (Vendor Capabilities, Compliance Complexity, Market Fragmentation, Pricing Competitiveness)

- Stakeholder Ecosystem (Banks, FinTechs, RegTech Vendors, Regulators, Data Providers)

- Porter’s Five Forces (Supplier Power, Buyer Power, Threat of Substitutes, Entry Barriers, Competitive Rivalry)

- Competition Ecosystem (Global Vendors vs Local RegTech Firms, API-Based vs Platform-Based Vendors)

- By Revenue (Platform Fees, Subscription Revenue, Licensing Fees), 2020-2026

- By Deployment Spend (Cloud vs On-Premise Compliance Solutions), 2020-2026

- By Average Contract Value (ACV), 2020-2026

- By Compliance Cost Allocation per Financial Institution, 2020-2026

- By Solution Type (In Value %)

AML Screening Volume

KYC Turnaround Time

Fraud Detection Accuracy Rate

Risk Scoring Models - By Deployment Model (In Value %)

Cloud Adoption Rate

Data Residency Compliance

API Latency

Integration Complexity - By Pricing Model (In Value %)

Subscription Fees

Cost per API Call

Tiered Pricing

Licensing Fees

Implementation Costs - By End User (In Value %)

Compliance Budget Allocation

Transaction Volume

Customer Onboarding Volume

Regulatory Reporting Frequency - By Compliance Function (In Value %)

Screening Frequency

Alert False Positive Rate

Regulatory Reporting Turnaround Time - By Geography (In Value %)

Financial Hub Density

Cross-Border Transaction Volume

Digital Banking Penetration

- Vendor Positioning Matrix (Global vs Singapore-Focused Vendors, BFSI Penetration, Tier-1 vs Tier-2 Client Base)

- Pricing Benchmarking Analysis (Cost per API Call, Cost per KYC Verification, Annual Subscription Pricing, Enterprise Licensing Cost, Implementation & Integration Fees)

- Solution Capability Benchmarking (AML Detection Accuracy, False Positive Reduction Rate, Real-Time Monitoring Capability, AI/ML Model Sophistication)

- Regulatory Coverage Benchmarking (MAS Compliance Readiness, FATF Alignment, Multi-Jurisdiction Coverage, Regulatory Update Frequency)

- Technology & Integration Benchmarking (API Availability, SDK Support, Integration Time with Core Banking Systems, Cloud Compatibility, Data Processing Speed)

- Customer Experience Benchmarking (Onboarding Time Reduction, User Interface Efficiency, Client Support SLAs, Customization Flexibility)

- Scalability & Performance Benchmarking (Transactions Processed per Second, High-Volume Processing Capability, System Downtime, Latency Metrics)

- Vendor Differentiation Analysis (AI-Driven vs Rule-Based Systems, Embedded Compliance Offerings, Ecosystem Partnerships, Proprietary Data Sources)

- Cost-to-Value Benchmarking (ROI on Compliance Spend, Cost per Compliance Case Resolved, Efficiency Gains in Compliance Teams)

- Use Case Benchmarking (Retail Banking, Corporate Banking, Digital Banks, Cross-Border Payments, Crypto Compliance Use Cases)

- Innovation & Product Roadmap Benchmarking (AI Advancements, Automation Features, Regulatory Sandbox Participation, Product Expansion Strategy)

- Market Share Analysis (Revenue Share, Client Base, API Volume Processed)

- Cross Comparison Parameters (API Pricing per Call, KYC Verification Cost per Customer, False Positive Rate, Integration Time, Regulatory Coverage (MAS/FATF), AI/ML Capability Score, Cloud Deployment Flexibility, Client Base in BFSI Sector)

- SWOT Analysis of Major Players

- Pricing Analysis Basis SKUs / Modules (AML Module Pricing, KYC Pricing, Transaction Monitoring Cost, Reporting Module Cost)

- Detailed Profiles of Major Companies

Refinitiv

LexisNexis Risk Solutions

Fenergo

ComplyAdvantage

Trulioo

Jumio

Onfido

Chainalysis

Feedzai

Actimize (NICE Actimize)

Dow Jones Risk & Compliance

Tookitaki

Silent Eight

Cynopsis Solutions

Ascent RegTech

- Compliance Spend Allocation per Institution

- Vendor Selection Criteria (Pricing, Accuracy, Integration Ease, Regulatory Coverage)

- Pain Point Analysis (False Positives, Manual Processes, Reporting Delays)

- Decision-Making Framework (CFO, CRO, Compliance Officers)

- Adoption Lifecycle (Pilot to Full-Scale Deployment)

- By Revenue (Platform Fees, Subscription Revenue, Licensing Fees), 2026-2035

- By Deployment Spend (Cloud vs On-Premise Compliance Solutions), 2026-2035

- By Average Contract Value (ACV), 2026-2035

- By Compliance Cost Allocation per Financial Institution, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now