Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Singapore Robotics Market reached approximately USD ~ billion in total market value according to industry statistics compiled from the International Federation of Robotics and Singapore Economic Development Board automation investment reports. The market is driven by widespread industrial automation across electronics manufacturing, semiconductor fabrication, logistics warehousing, and healthcare robotics deployment. Government robotics grants, advanced manufacturing initiatives, and rising labor costs continue accelerating adoption of industrial robots, collaborative robots, and autonomous mobile robots across Singapore’s advanced production and service sectors.

Singapore serves as a leading robotics deployment hub in Southeast Asia due to its highly automated manufacturing ecosystem, particularly within advanced semiconductor fabrication facilities located in Jurong and Tampines industrial clusters. The country’s logistics automation sector also expands rapidly across large distribution centers supporting regional e-commerce supply chains operating through Changi logistics zones. Government supported robotics innovation centers, strong foreign technology investment, and high manufacturing productivity standards further reinforce Singapore’s dominance in robotics system integration and deployment across Asia Pacific.

Market Segmentation

By Product Type

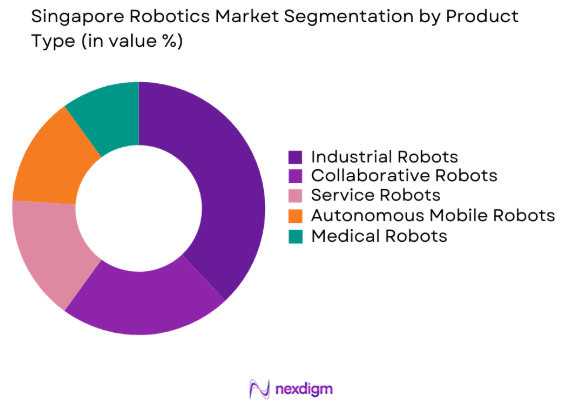

Singapore Robotics Market is segmented by product type into Industrial Robots, Collaborative Robots, Service Robots, Autonomous Mobile Robots, and Medical Robots. Recently, Industrial Robots has a dominant market share due to factors such as strong manufacturing demand, semiconductor fabrication automation, and advanced electronics production lines. Singapore hosts numerous semiconductor manufacturing facilities and precision electronics assembly plants that rely heavily on robotic arms for wafer handling, micro-component assembly, and automated inspection processes. Industrial robots provide consistent operational efficiency, precision, and productivity improvements required for high-volume electronics manufacturing. Government manufacturing modernization programs and strong investments from global semiconductor companies further increase industrial robot installations across the country. Additionally, rising labor costs encourage manufacturers to adopt robotic automation to maintain competitive production efficiency. These factors collectively ensure that industrial robots maintain the largest share of robotics deployment within Singapore’s automation ecosystem.

By End User Industry

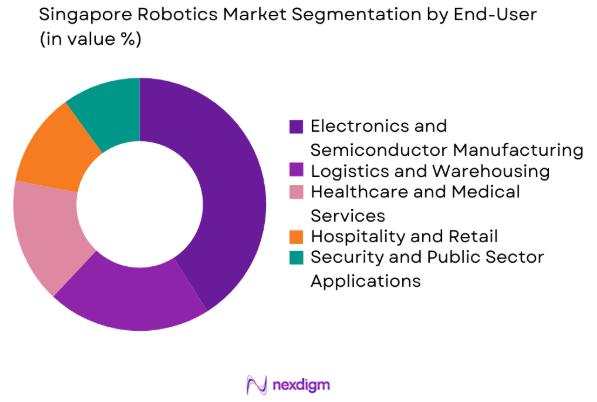

Singapore Robotics Market market is segmented by end user industry into Electronics and Semiconductor Manufacturing, Healthcare and Medical Services, Logistics and Warehousing, Hospitality and Retail, and Security and Public Sector Applications. Recently, Electronics and Semiconductor Manufacturing has a dominant market share due to factors such as the country’s strong semiconductor manufacturing base, advanced electronics production, and the presence of global chip manufacturing facilities. Semiconductor wafer fabrication requires extremely precise robotic systems for material transport, micro-component assembly, and automated inspection within cleanroom environments. Global semiconductor manufacturers operating in Singapore invest heavily in robotics automation to maintain defect free production and extremely high productivity standards. Electronics assembly plants also deploy robotics for printed circuit board manufacturing and microelectronics testing operations. These large-scale automated manufacturing operations generate the highest demand for robotic systems within Singapore’s industrial economy.

Competitive Landscape

The Singapore Robotics Market demonstrates a moderately consolidated competitive structure dominated by large global robotics manufacturers and specialized automation solution providers. International robotics companies maintain strong regional operations in Singapore due to the country’s advanced manufacturing sector and technology friendly regulatory environment. Major players focus heavily on industrial automation robotics, collaborative robots, autonomous logistics robots, and service robotics applications. Competition centers on technology capabilities, robotics integration services, software intelligence platforms, and advanced robotic vision systems supporting Industry 4.0 manufacturing environments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Robotics Deployment Capability |

| ABB Robotics | 1988 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Fanuc Corporation | 1956 | Japan | ~ | ~ | ~ | ~ | ~ |

| Yaskawa Electric | 1915 | Japan | ~ | ~ | ~ | ~ | ~ |

| KUKA AG | 1898 | Germany | ~ | ~ | ~ | ~ | ~ |

| Universal Robots | 2005 | Denmark | ~ | ~ | ~ | ~ | ~ |

Singapore Robotics Market Analysis

Growth Drivers

Rapid Expansion of Semiconductor and Electronics Manufacturing Automation in Singapore

Singapore’s advanced semiconductor and electronics manufacturing ecosystem significantly accelerates robotics adoption because precision microelectronics production requires highly automated environments capable of maintaining strict quality standards and consistent output across complex processes. Semiconductor fabrication facilities use robotics extensively to handle delicate silicon wafers and transport them through fabrication stages such as photolithography, etching, deposition, and packaging. These operations require robotic systems that maintain cleanroom conditions while performing precise repetitive tasks without contamination risk. Electronics assembly plants across Singapore’s industrial clusters also deploy robotic arms for circuit board assembly, inspection, and packaging supporting global exports. Government manufacturing modernization initiatives and automation incentives further encourage companies to invest in robotics technologies and advanced production systems.

Government Automation Programs and National Robotics Innovation Investments

Singapore’s government plays a critical role in accelerating robotics adoption through national automation programs, research funding initiatives, and technology development strategies aimed at strengthening smart manufacturing capabilities. National robotics programs provide financial grants supporting robotics development across manufacturing, logistics, healthcare, and urban service applications. These initiatives promote collaboration between robotics technology firms, industrial manufacturers, and public sector organizations to accelerate commercialization of advanced robotics solutions. Automation support schemes also help businesses adopt robotics through subsidies for system procurement, integration, and workforce training. Singapore’s innovation ecosystem includes robotics laboratories, research centers, and testing facilities that support technology development. Government investment in artificial intelligence and autonomous systems further strengthens robotics innovation and industry adoption.

Market Challenges

High Capital Costs and Long Investment Payback Period for Robotics Deployment

Robotics system deployment often requires significant upfront investment including robotic hardware acquisition, software integration, system installation, and workforce training, creating financial barriers for smaller manufacturing firms and service organizations adopting automation technologies. Industrial robotic systems used in semiconductor manufacturing, logistics automation, and healthcare applications involve complex integration processes requiring engineering design, robotics programming, and production line restructuring. These requirements increase total adoption costs beyond the base price of robotic equipment. Small and medium sized enterprises within Singapore’s manufacturing ecosystem may struggle to justify such investments due to limited production volumes. Ongoing maintenance contracts, software upgrades, and system support also create recurring operational expenses that influence automation investment decisions.

Limited Availability of Advanced Robotics Engineering Talent and Integration Specialists

Robotics deployment requires specialized engineering expertise including robotics programming, artificial intelligence integration, machine vision systems, and advanced automation design capabilities that remain limited across global technology labor markets. Singapore’s robotics industry therefore faces workforce constraints because companies require highly skilled engineers capable of designing, deploying, and maintaining complex robotic systems across manufacturing, healthcare, and logistics automation environments. Robotics engineers must possess multidisciplinary knowledge covering mechanical engineering, electrical systems, software development, artificial intelligence, and automation architecture, which restricts the available talent pool. As robotics technologies become more sophisticated, companies increasingly require experts in machine learning algorithms, sensor integration, and robotics navigation software. Strong competition for skilled robotics engineers further intensifies talent shortages within the industry.

Opportunities

Expansion of Autonomous Logistics and Warehouse Robotics Systems

Singapore’s expanding logistics and e commerce distribution ecosystem creates strong opportunities for robotics technologies designed to automate warehouse operations inventory management and parcel handling within large fulfillment centers. Logistics operators managing regional distribution hubs increasingly deploy autonomous mobile robots to transport goods across warehouse floors using coordinated fleet management systems. These robots improve operational efficiency by reducing manual labor and accelerating order processing for online retail shipments. Advanced sensors artificial intelligence navigation software and warehouse management platforms allow robots to operate efficiently within complex warehouse environments alongside human workers. Growing digital commerce across Southeast Asia continues increasing demand for high capacity logistics infrastructure. As a regional logistics hub Singapore encourages greater adoption of robotics driven warehouse automation technologies.

Development of Healthcare Robotics and Medical Automation Technologies

Healthcare robotics represents a rapidly expanding opportunity within Singapore due to the country’s advanced healthcare infrastructure, strong medical technology sector, and growing demand for precision surgical procedures and hospital automation systems. Robotic surgical platforms enable minimally invasive procedures with high precision, improving patient outcomes and shortening recovery periods. Hospitals increasingly deploy robotic systems for urological, orthopedic, cardiac, and neurological procedures that require accuracy and stability. Service robots are also used in hospitals for medical supply transport, patient assistance, and facility sanitation. Singapore’s biomedical innovation ecosystem encourages robotics development through collaboration between medical technology firms, healthcare providers, and research institutions. Government healthcare innovation programs further support robotics research and clinical testing, accelerating adoption of advanced healthcare automation technologies.

Future Outlook

The Singapore Robotics Market is expected to experience sustained expansion driven by increasing automation across manufacturing, logistics, and healthcare sectors. Advancements in artificial intelligence, machine vision, and autonomous robotics systems will significantly enhance robotic capabilities across industrial and service environments. Government innovation programs and automation incentives will continue encouraging robotics adoption among enterprises. Expanding semiconductor production, logistics automation, and smart city initiatives will further accelerate robotics deployment across Singapore’s technology driven economy.

Major Players

- ABB Robotics

- Fanuc Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Universal Robots

- Omron Robotics and Safety Technologies

- Denso Robotics

- Kawasaki Robotics

- Mitsubishi Electric Automation

- TechmanRobot

- StaubliRobotics

- GreyOrange

- OTSAW Digital

- Aethon

- Mobile Industrial Robots

Key Target Audience

- Robotics Manufacturing Companies

- Semiconductor Manufacturing Firms

- Logistics and Warehouse Automation Companies

- Healthcare Technology Providers

- Electronics Manufacturing Companies

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Industrial Automation Equipment Distributors

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying critical variables influencing the Singapore Robotics Market including automation adoption rates, robotics installation levels, manufacturing activity, and logistics automation trends. These variables form the base framework for market analysis and segmentation.

Step 2: Market Analysis and Construction

Data collected from industry reports, robotics deployment statistics, government technology programs, and manufacturing sector performance indicators are analyzed to construct the overall market structure and segmentation patterns within the robotics ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including robotics engineers, automation solution providers, and manufacturing technology specialists validate research assumptions. Their insights help confirm adoption trends and identify emerging technological developments influencing robotics demand.

Step 4: Research Synthesis and Final Output

All validated research findings are consolidated into a structured market model, ensuring consistency between qualitative insights and quantitative data points. The final output delivers a comprehensive analysis of the Singapore Robotics Market ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Smart Manufacturing and Industry 4.0 Adoption

Government Robotics Funding and National Automation Initiatives

Rising Labor Costs and Workforce Automation Demand - Market Challenges

High Capital Investment Requirements for Robotics Deployment

Integration Complexity with Legacy Industrial Systems

Shortage of Advanced Robotics Engineering Talent - Market Opportunities

Growth of Autonomous Logistics and Warehouse Robotics

Expansion of Healthcare and Surgical Robotics Applications

Development of Robotics as a Service Business Models - Trends

Increasing Deployment of Collaborative Robots in Manufacturing

Integration of Artificial Intelligence and Machine Vision in Robotics

Growth of Autonomous Mobile Robots for Logistics Automation - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Industrial Robots

Collaborative Robots

Service Robots

Mobile Autonomous Robots

Humanoid Robots - By Platform Type (In Value%)

Manufacturing Platforms

Healthcare Platforms

Logistics and Warehousing Platforms

Hospitality and Service Platforms

Security and Surveillance Platforms - By Fitment Type (In Value%)

New Installations

Retrofit Integrations

Modular Robotic Systems

Embedded Robotics Solutions

Hybrid Automation Systems - By End User Segment (In Value%)

Electronics and Semiconductor Manufacturing

Healthcare and Medical Facilities

Logistics and E Commerce Operators

Hospitality and Retail Services

Public Sector and Security Agencies - By Procurement Channel (In Value%)

Direct Enterprise Procurement

Government Technology Procurement Programs

System Integrator Contracts

Robotics Leasing and Robotics as a Service Providers

Technology Distributor Networks

- Market Share Analysis

- Cross Comparison Parameters (Robot Type Portfolio, Industrial Application Coverage, AI Integration Capability, Service Network Strength, Regional Deployment Scale)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

ABB Robotics

Fanuc Corporation

Yaskawa Electric Corporation

KUKA AG

Universal Robots

Omron Robotics and Safety Technologies

Denso Robotics

Kawasaki Robotics

Mitsubishi Electric Automation

Techman Robot

Staubli Robotics

GreyOrange

OTSAW Digital

Aethon

Mobile Industrial Robots

- Electronics manufacturers increasingly deploy robotics for precision semiconductor assembly

- Healthcare institutions adopt robotic surgical and hospital service robots

- Logistics companies implement warehouse automation robots for high throughput fulfillment

- Government agencies utilize robotics for urban services security and infrastructure maintenance

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now