Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Singapore search and rescue aircraft market was valued at USD ~ million, supported by sustained public-sector investment in aviation safety, maritime surveillance, and national emergency preparedness programs. Demand is driven by fleet modernization initiatives, integration of advanced avionics and sensor payloads, and the requirement for rapid-response capabilities across congested air and sea corridors. Additional momentum comes from lifecycle upgrades, maintenance contracts, and mission system retrofitting aligned with international aviation safety obligations and multi-agency coordination mandates.

Based on a recent historical assessment, Singapore remains the dominant operational hub for the regional search and rescue aircraft market due to its strategic maritime location, high air traffic density, and centralized command-and-control infrastructure. Changi and Paya Lebar anchor mission coordination through proximity to major sea lanes and aerospace maintenance clusters. Regional influence extends through cooperation with neighboring Southeast Asian countries, where Singapore-based platforms support cross-border missions, training exercises, and logistics, reinforced by strong regulatory frameworks and defense-led procurement stability.

Market Segmentation

By Product Type

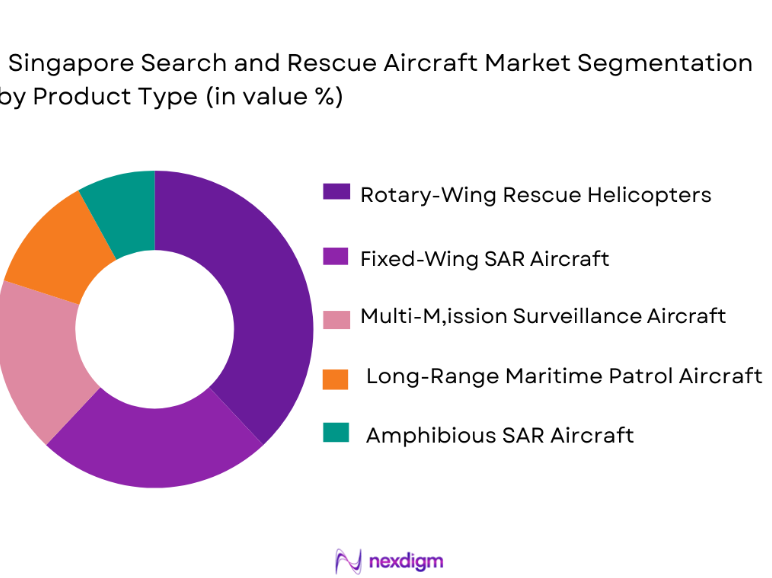

The Singapore Search and Rescue Aircraft Market is segmented by product type into fixed-wing search and rescue aircraft, rotary-wing rescue helicopters, amphibious rescue aircraft, long-range maritime patrol aircraft, and multi-mission surveillance and rescue aircraft. Recently, rotary-wing rescue helicopters have a dominant market share due to their ability to access difficult-to-reach areas and operate efficiently in diverse rescue scenarios. Their flexibility, coupled with high demand for rapid response in offshore and mountainous regions, makes them the preferred choice for search and rescue operations.

By Platform Type

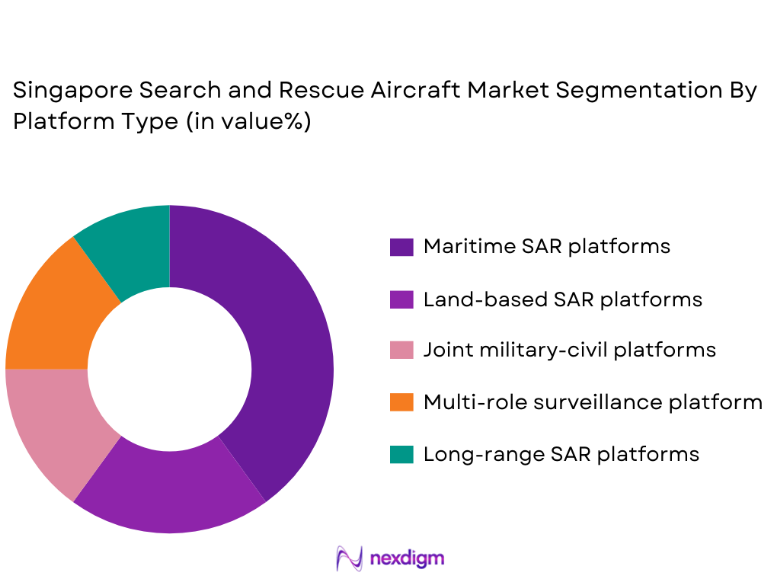

Singapore Search and Rescue Aircraft Market is segmented by platform type into maritime SAR platforms, land-based SAR platforms, joint military-civil platforms, and multi-role surveillance platforms and Long-Range SAR Platforms. Recently, maritime SAR platforms had a dominant market share due to Singapore’s geographic profile, extensive territorial waters, and exposure to high-density commercial shipping routes. The concentration of offshore energy assets, port infrastructure, and international sea lanes necessitates aircraft optimized for long-endurance maritime patrol, over-water navigation, and integrated sensor fusion. These platforms are prioritized for their ability to coordinate with naval vessels, deploy rescue equipment at sea, and conduct extended missions without refueling. Strong interoperability requirements for centralized maritime command structures, and continuous investment in coastal security aviation assets further consolidate the dominance of maritime-focused SAR platforms within national procurement strategies.

Competitive Landscape

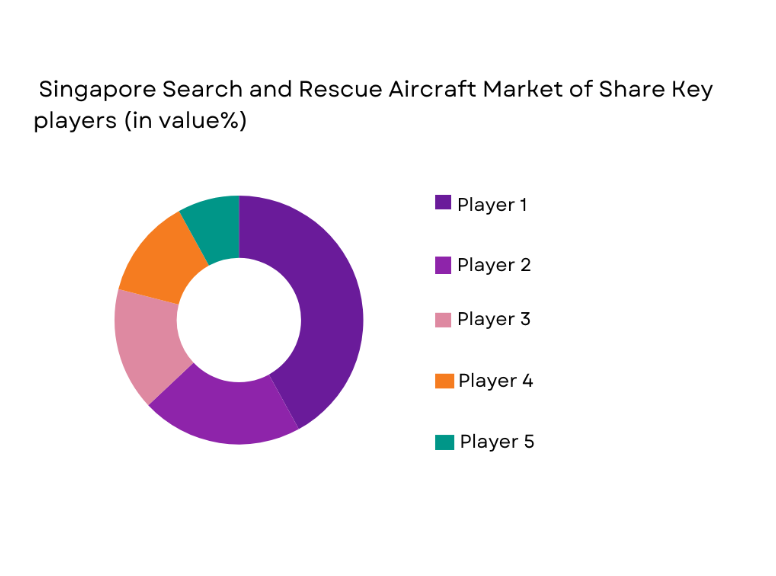

The Singapore search and rescue aircraft market is moderately consolidated, with a limited number of global aerospace manufacturers and system integrators supplying specialized platforms and mission systems. Major players exert strong influence through long-term government contracts, technology partnerships, and regional maintenance hubs, creating high entry barriers for new participants while reinforcing supplier concentration.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Regional MRO Capability |

| Airbus Defence and Space | 1970 | Europe | ~ | ~ | ~ | ~ | ~ |

| Leonardo Helicopters | 1948 | Italy | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1995 | USA | ~ | ~ | ~ | ~ | ~ |

| Boeing Defense | 1916 | USA | ~ | ~ | ~ | ~ | ~ |

| ST Engineering Aerospace | 1990 | Singapore | ~ | ~ | ~ | ~ | ~ |

Singapore Search and Rescue Robots Market Analysis

Growth Driver

Maritime and Aviation Traffic Density Expansion

Maritime and aviation traffic density expansion is a primary growth driver shaping the Singapore search and rescue aircraft market, driven by the country’s position along some of the world’s busiest sea lanes and air routes, which significantly increases the probability of emergency incidents requiring rapid aerial response. The continuous rise in commercial shipping movements, offshore energy logistics, and passenger air traffic places sustained pressure on national authorities to maintain high-readiness SAR aviation assets capable of operating in congested and high-risk environments. This traffic concentration necessitates aircraft with advanced surveillance sensors, long endurance, and rapid deployment capability to minimize response times. As vessel sizes and passenger volumes increase, the potential scale of rescue operations expands, further reinforcing the need for technologically advanced aircraft fleets. The operational complexity associated with dense traffic corridors also drives investment in mission management systems that enhance situational awareness and coordination. Government agencies respond by prioritizing funding for SAR aircraft upgrades and replacements. Regional cooperation frameworks further amplify this driver by assigning Singapore a leadership role in joint SAR operations. These combined factors ensure sustained demand for capable SAR aircraft platforms.

Defense Modernization and Multi-Role Aircraft Integration

Defense modernization and multi-role aircraft integration act as a critical growth driver for the Singapore search and rescue aircraft market, as national defense policy emphasizes flexible platforms capable of performing multiple missions beyond traditional SAR roles. Aircraft procurement increasingly favors systems that can support surveillance, maritime security, and humanitarian assistance alongside rescue operations, maximizing asset utilization. This approach aligns with budget optimization strategies and operational readiness requirements. Advanced avionics, sensor fusion, and communications systems enhance mission adaptability and effectiveness. Modernization programs also prioritize interoperability with allied forces and civilian agencies, driving demand for standardized yet customizable aircraft solutions. The integration of multi-role capabilities reduces fleet fragmentation and simplifies training and maintenance. As older platforms approach obsolescence, replacement cycles accelerate, reinforcing procurement momentum. These modernization imperatives collectively sustain long-term market growth.

Market Challenges

High Acquisition and Lifecycle Cost Constraints

High acquisition and lifecycle cost constraints represent a major challenge for the Singapore search and rescue aircraft market, as specialized SAR platforms require significant upfront capital investment and sustained operational expenditure over their service life. Advanced mission systems, sensors, and avionics substantially increase procurement costs compared to conventional aircraft. In addition, maintenance, training, and certification expenses place ongoing pressure on defense and civil aviation budgets. Lifecycle cost management becomes more complex when fleets are limited in size, reducing economies of scale. Budgetary trade-offs with other national security and infrastructure priorities further constrain procurement flexibility. Currency exposure for imported platforms also introduces financial risk. These cost-related factors can delay replacement cycles and limit fleet expansion. As a result, procurement decisions require extensive evaluation and approval processes.

Operational and Airspace Limitation

Operational and airspace limitations pose another significant challenge for the Singapore search and rescue aircraft market due to the country’s compact geography and heavily regulated airspace. High air traffic density restricts training windows and operational flexibility for SAR missions. Coordinating military, civilian, and commercial air operations requires complex air traffic management protocols. Limited space for dedicated SAR bases further constrains rapid deployment options. Cross-border operations require diplomatic clearances and coordination, potentially affecting response time. Weather conditions and urban proximity add operational complexity. These constraints necessitate highly efficient planning and coordination mechanisms. Managing these limitations increases operational overhead and demands advanced command systems.

Opportunities

Integration of Unmanned and Manned SAR Operations

Integration of unmanned and manned SAR operations presents a major opportunity for the Singapore search and rescue aircraft market, as technological maturity enables drones to complement traditional aircraft in reconnaissance and early response roles. Unmanned systems can extend surveillance coverage and reduce risk to crewed aircraft. Data collected by drones enhances mission planning and targeting accuracy. Combined operations improve response efficiency and resource utilization. Regulatory acceptance of unmanned systems continues to improve. Investment in integrated command systems supports this convergence. This opportunity aligns with Singapore’s broader smart defense and digitalization strategies.

Regional SAR Cooperation and Service Export Potential

Regional SAR cooperation and service export potential offer a significant opportunity for the Singapore search and rescue aircraft market, leveraging the country’s advanced infrastructure and operational expertise. Singapore-based assets increasingly support regional training, joint exercises, and emergency response. This positioning creates opportunities for service-based contracts and technical support for exports. Regional demand for SAR capability continues to rise. Government-to-government agreements facilitate collaboration. Such cooperation enhances fleet utilization and justifies further investment. This opportunity strengthens Singapore’s role as a regional SAR hub.

Future Outlook

Over the next five years, the Singapore search and rescue aircraft market is expected to experience steady growth driven by fleet modernization, technological integration, and sustained government support. Advancements in sensors, communications, and multi-role platforms will enhance operational efficiency. Regulatory alignment with international SAR standards will continue to support procurement. Demand will remain anchored in maritime and aviation safety requirements, reinforcing long-term investment stability.

Major Players

- AirbusDefenceand Space

- Leonardo Helicopters

- Lockheed Martin

- Boeing Defense

- ST Engineering Aerospace

- Sikorsky Aircraft

- Bell Textron

- Embraer Defense

- Saab Aerospace

- Korea Aerospace Industries

- Elbit Systems

- IAI Aviation Group

- RUAG Aerospace

- Pilatus Aircraft

- Textron Aviation Defense

Key Target Audience

- Defense Ministries

- Civil aviation authorities

- Maritime safety agencies

- Disaster management authorities

- Port and shipping authorities

- Offshore energy operators

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Market scope, aircraft categories, end users, and regulatory factors were identified through secondary research and industry databases. Demand drivers and constraints were mapped to operational requirements. Key variables were shortlisted for further analysis.

Step 2: Market Analysis and Construction

Historical procurement data, fleet composition, and budget allocations were analyzed to construct the market framework. Segmentation logic was applied based on operational relevance.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with aviation experts, defense analysts, and industry stakeholders to ensure accuracy and relevance.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into a structured market model, ensuring consistency across sections and alignment with research objectives.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Strategic maritime location with dense air and sea traffic

Rising emphasis on rapid response and aviation safety

Modernization of air force and maritime patrol capabilities

Integration of advanced sensors and surveillance technologies

Regional cooperation requirements for cross-border rescue missions - Market Challenges

High acquisition and lifecycle costs of specialized aircraft

Limited airspace and operational constraints

Complex certification and regulatory compliance requirements

Dependence on imported platforms and subsystems

Skilled workforce requirements for advanced mission systems - Market Opportunities

Fleet upgrades with multi-role and modular aircraft

Integration of unmanned systems with manned rescue operations

Expansion of regional search and rescue cooperation frameworks - Trends

Adoption of multi-mission aircraft with SAR capability

Increased use of real-time data sharing and networking

Integration of long-endurance surveillance platforms

Focus on rapid deployment and interoperability

Emphasis on sustainability and fuel-efficient aircraft - Government Regulations & Defense Policy

Alignment with international aviation safety and SAR standards

Defense capability development under national security frameworks

Strengthening of maritime and aviation safety regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Fixed-wing search and rescue aircraft

Rotary-wing rescue helicopters

Amphibious rescue aircraft

Long-range maritime patrol aircraft

multi-mission surveillance and rescue aircraft - By Platform Type (In Value%)

Manned aircraft platforms

Unmanned aerial support platforms

Joint manned-unmanned platforms

Naval aviation-based platforms

Air force-operated platforms - By Fitment Type (In Value%)

New-build dedicated rescue aircraft

Missionized transport aircraft

Retrofit and upgrade installations

Leased and chartered rescue aircraft

Modular mission kit integrations - By End User Segment (In Value%)

Air force and defense forces

Maritime and port authorities

Civil aviation and airport authorities

National disaster management agencies

Offshore energy and industrial operators - By Procurement Channel (In Value%)

Government direct acquisition programs

Defense procurement contracts

OEM-led system integration programs

International government-to-government agreements

Leasing and service-based procurement - By Material / Technology (in Value %)

Advanced avionics and mission systems

Electro-optical and infrared sensors

Satellite communication and data links

Lightweight composite airframes

AI-enabled mission management software

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Aircraft range, Payload capacity, Sensor integration level, Mission endurance, Lifecycle cost efficiency, Interoperability, Certification compliance, After-sales support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Airbus Defence and Space

Leonardo Helicopters

Boeing Defense

Lockheed Martin

Textron Aviation Defense

Sikorsky Aircraft

Bell Textron

Embraer Defense and Security

Saab Aerospace

Korea Aerospace Industries

RUAG Aerospace

ST Engineering Aerospace

Elbit Systems Aerospace

IAI Aviation Group

Pilatus Aircraft

- Defense users prioritize long-range endurance and mission reliability

- Maritime agencies focus on rapid deployment and all-weather capability

- Civil authorities emphasize compliance and interoperability

- Industrial operators require flexible and contracted rescue solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now