Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Singapore Semiconductor Manufacturing market generated approximately USD ~ billion in manufacturing output value according to statistics reported by the Singapore Economic Development Board and the Singapore Department of Statistics. The market is primarily driven by strong demand for advanced logic chips, memory semiconductors, and power devices used in consumer electronics, automotive electronics, and data infrastructure systems. Significant investments by global semiconductor companies, strong fabrication infrastructure, and government supported industrial policies further strengthen production capacity across advanced wafer fabrication and semiconductor packaging facilities operating in the country.

Singapore remains one of the most significant semiconductor manufacturing hubs globally, supported by highly developed industrial clusters located in Woodlands, Tampines, Pasir Ris, and Jurong Innovation District. These areas host multiple wafer fabrication plants, semiconductor equipment facilities, and advanced packaging operations supported by specialized semiconductor suppliers and engineering service providers. Strong logistics connectivity through Changi Airport and Tuas Mega Port enhances supply chain efficiency for semiconductor exports. Government industrial programs, skilled engineering talent, and stable regulatory frameworks further reinforce Singapore’s dominance in semiconductor manufacturing within the Asia Pacific technology ecosystem.

Market Segmentation

By Product Type

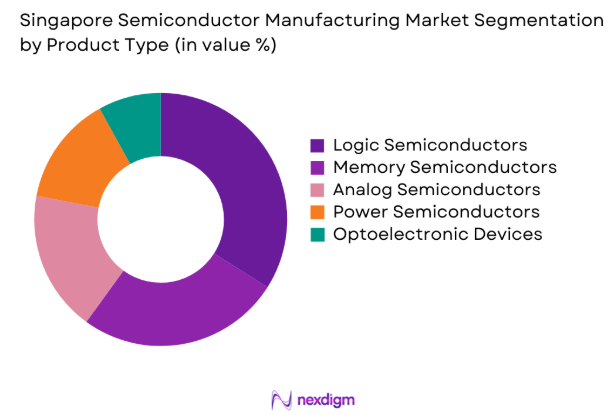

Singapore Semiconductor Manufacturing market is segmented by product type into logic semiconductors, memory semiconductors, analog semiconductors, power semiconductors, and optoelectronic devices. Recently, logic semiconductors have a dominant market share due to rising demand from artificial intelligence processors, data center infrastructure, high performance computing systems, and advanced consumer electronics. Singapore hosts multiple advanced wafer fabrication facilities capable of producing complex integrated circuits required for processors and communication chips. Major global semiconductor firms operate high precision manufacturing plants within Singapore’s semiconductor ecosystem, enabling large scale production of logic devices for global technology companies. Increasing global demand for AI accelerators, networking chips, and automotive control systems strengthens the dominance of logic semiconductor manufacturing within the country. Government incentives supporting semiconductor technology development, strong intellectual property protection frameworks, and availability of highly skilled semiconductor engineers further reinforce Singapore’s leadership in logic semiconductor manufacturing within the broader semiconductor supply chain ecosystem.

By Wafer Size

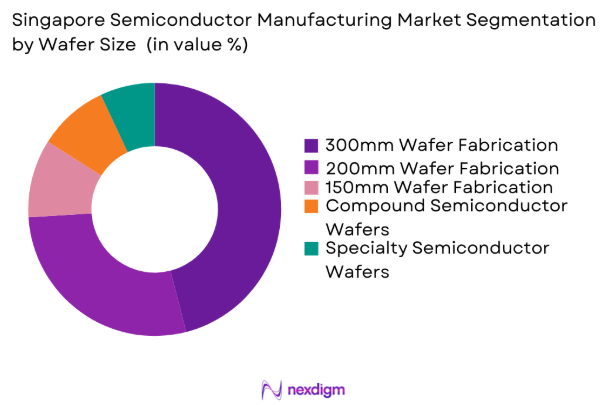

Singapore Semiconductor Manufacturing market is segmented by wafer size into 300mm wafer fabrication, 200mm wafer fabrication, 150mm wafer fabrication, compound semiconductor wafers, and specialty semiconductor wafers. Recently, 300mm wafer fabrication has a dominant market share due to its ability to produce a higher number of semiconductor dies per wafer while significantly improving manufacturing efficiency and cost optimization. Large semiconductor fabrication facilities operating in Singapore increasingly adopt 300mm wafer manufacturing technologies to support advanced chip production required for artificial intelligence processors, networking equipment, and automotive semiconductor applications. Semiconductor manufacturers benefit from higher productivity, lower per chip production costs, and improved process automation capabilities offered by 300mm wafer fabrication systems. Global semiconductor companies continue expanding advanced 300mm fabrication capacity within Singapore to support high volume chip production for international technology markets. Continuous investments in advanced lithography systems, wafer processing equipment, and automated fabrication systems further strengthen the dominance of 300mm wafer manufacturing technologies across Singapore’s semiconductor production infrastructure.

Competitive Landscape

The Singapore Semiconductor Manufacturing market exhibits a highly concentrated competitive landscape dominated by multinational semiconductor manufacturers and advanced semiconductor equipment companies operating large fabrication facilities across the country. These firms maintain strong technological capabilities in wafer fabrication, advanced packaging, semiconductor equipment manufacturing, and chip design integration. Strategic investments in advanced node manufacturing technologies, cleanroom infrastructure, and automation systems enable major players to maintain high production volumes and strong global supply chain positions within the semiconductor industry.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fabrication Capability |

| GlobalFoundries | 2009 | United States | ~ | ~ | ~ | ~ | ~ |

| Micron Technology | 1978 | United States | ~ | ~ | ~ | ~ | ~ |

| Infineon Technologies | 1999 | Germany | ~ | ~ | ~ | ~ | ~ |

| United Microelectronics Corporation | 1980 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ |

Singapore Semiconductor Manufacturing Market Analysis

Growth Drivers

Expansion of Artificial Intelligence and High Performance Computing Semiconductor Demand

The rapid expansion of artificial intelligence technologies significantly increases global demand for advanced semiconductor chips capable of supporting complex computing workloads required for machine learning algorithms data center processing and cloud infrastructure. Semiconductor manufacturers in Singapore experience strong demand for logic processors high bandwidth memory devices and specialized semiconductor accelerators designed for artificial intelligence applications. Advanced semiconductor fabrication plants in Singapore operate high precision wafer manufacturing systems capable of producing complex integrated circuits required for artificial intelligence processors networking chips and high performance computing systems. Global technology companies continue investing heavily in artificial intelligence infrastructure which directly increases semiconductor demand because processors accelerators and networking chips form the hardware foundation supporting modern digital computing systems.

Growth of Automotive Electronics and Electric Vehicle Semiconductor Requirements

The rapid electrification of the global automotive industry significantly increases demand for advanced semiconductor devices used in electric vehicles autonomous driving systems battery management technologies and vehicle power electronics. Electric vehicles rely heavily on semiconductor components including microcontrollers power semiconductors sensors and communication chips that enable intelligent vehicle control systems advanced driver assistance technologies and efficient battery management infrastructure. Semiconductor manufacturing facilities in Singapore increasingly produce power semiconductor devices and automotive grade integrated circuits required for vehicle electrification technologies. Automotive manufacturers depend on semiconductor suppliers capable of delivering reliable semiconductor components that meet strict automotive safety and durability standards. As vehicle electrification accelerates globally semiconductor demand continues rising strengthening Singapore’s role in the global automotive electronics supply chain.

Market Challenges

Extremely High Capital Expenditure Requirements for Advanced Semiconductor Fabrication Facilities

Semiconductor manufacturing requires extremely capital intensive fabrication facilities equipped with advanced lithography systems wafer processing equipment ultra clean production environments and automated manufacturing technologies that require multi billion dollar investments for each fabrication plant. Semiconductor companies operating in Singapore must continuously invest large amounts of capital to upgrade manufacturing equipment adopt advanced technologies and expand wafer fabrication capacity required for next generation semiconductor production. The rising cost of semiconductor manufacturing equipment including extreme ultraviolet lithography systems etching tools and deposition technologies creates financial pressure for manufacturers expanding production capacity. Companies must also invest heavily in specialized cleanroom infrastructure environmental control systems and advanced process monitoring technologies to maintain high manufacturing precision standards.

Global Semiconductor Supply Chain Disruptions and Geopolitical Technology Restrictions

The global semiconductor industry operates within a complex international supply chain involving semiconductor equipment manufacturers materials suppliers chip designers and electronic device producers across multiple regions. Semiconductor manufacturers in Singapore rely heavily on imported semiconductor equipment specialized materials and advanced lithography technologies supplied by global technology companies. Geopolitical tensions among major technology producing countries increasingly influence semiconductor trade policies export controls and technology transfer regulations affecting global semiconductor manufacturing networks. Restrictions on advanced semiconductor equipment may limit access to cutting edge manufacturing tools required for producing advanced semiconductor devices. Semiconductor companies therefore adopt diversified supplier networks and supply chain risk management strategies to maintain stable semiconductor production capabilities.

Opportunities

Expansion of Advanced Semiconductor Packaging and Chiplet Integration Technologies

The rapid evolution of semiconductor design architectures increasingly highlights advanced semiconductor packaging technologies capable of integrating multiple semiconductor dies into high performance computing systems using chiplet based structures. Packaging technologies including three dimensional chip stacking heterogeneous integration and wafer level packaging improve processing performance energy efficiency and system integration within modern electronic devices. Semiconductor companies operating in Singapore are expanding advanced packaging capabilities to support next generation semiconductor products used in artificial intelligence processors high performance computing systems and networking infrastructure. Global semiconductor manufacturers are investing in advanced packaging facilities that integrate multiple semiconductor components into optimized computing modules designed for complex processing workloads across modern digital technologies.

Growth of Compound Semiconductor Manufacturing for Power Electronics and Renewable Energy Systems

The global transition toward renewable energy electric vehicles and advanced power electronics significantly increases demand for compound semiconductor materials such as silicon carbide and gallium nitride used in high efficiency power semiconductor devices. These devices provide higher power efficiency improved thermal stability and faster switching performance compared with conventional silicon semiconductor technologies which makes them suitable for renewable energy systems electric vehicles and industrial power conversion equipment. Semiconductor manufacturers in Singapore are increasingly investing in compound semiconductor manufacturing technologies to support rising demand for high performance power devices. Renewable energy infrastructure energy storage systems and smart grid networks require advanced power semiconductors capable of efficiently managing high voltage electricity flows across modern energy systems.

Future Outlook

The Singapore Semiconductor Manufacturing market is expected to experience continued expansion driven by strong global demand for artificial intelligence processors advanced memory devices automotive semiconductors and power electronics technologies. Semiconductor manufacturers are likely to increase investments in advanced wafer fabrication systems automation technologies and advanced packaging facilities supporting next generation semiconductor products. Government industrial development programs and semiconductor workforce development initiatives will further strengthen national semiconductor capabilities. Increasing semiconductor demand from data centers electric vehicles and renewable energy technologies will also reinforce long term growth.

Major Players

- GlobalFoundries

- Micron Technology

- Infineon Technologies

- United Microelectronics Corporation

- STMicroelectronics

- ASM International

- Applied Materials

- Lam Research

- Tokyo Electron

- ASE Technology Holding

- Broadcom

- Qualcomm

- Texas Instruments

- NXP Semiconductors

- Siliconware Precision Industries

Key Target Audience

- Semiconductor Manufacturing Companies

- Semiconductor Equipment Manufacturers

- Consumer Electronics Manufacturers

- Automotive Electronics Manufacturers

- Data Center Infrastructure Companies

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Semiconductor Materials Suppliers

Research Methodology

Step 1: Identification of Key Variables

Primary variables influencing the Singapore Semiconductor Manufacturing market were identified through semiconductor industry databases government statistics and semiconductor trade association reports. Key indicators included semiconductor fabrication capacity wafer processing volumes semiconductor equipment investments and semiconductor export performance indicators.

Step 2: Market Analysis and Construction

Market structure was constructed using data collected from semiconductor manufacturing companies equipment suppliers government industrial statistics and international semiconductor trade databases. Supply chain relationships fabrication technologies semiconductor product categories and production capacity indicators were analyzed to define market segmentation.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary research findings were validated through consultation with semiconductor industry engineers semiconductor equipment manufacturers semiconductor supply chain specialists and technology analysts. These consultations ensured accuracy of production capacity analysis semiconductor technology adoption trends and global semiconductor demand drivers.

Step 4: Research Synthesis and Final Output

All collected data and validated insights were integrated using structured research frameworks designed to present a comprehensive analysis of the Singapore Semiconductor Manufacturing market. Quantitative semiconductor production data qualitative industry insights and technology trend analysis were synthesized into the final market report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Global Semiconductor Supply Chain Diversification

Government Incentives Supporting Semiconductor Manufacturing Investments

Rising Demand for Advanced Chips in Artificial Intelligence and Automotive Electronics - Market Challenges

High Capital Expenditure Requirements for Semiconductor Fabrication Facilities

Dependence on Imported Semiconductor Manufacturing Equipment and Materials

Intense Global Competition from Major Semiconductor Manufacturing Hubs - Market Opportunities

Expansion of Advanced Packaging and Chiplet Manufacturing Technologies

Growth of Compound Semiconductor Manufacturing for Power Electronics

Strategic Partnerships with Global Foundries and Technology Firms - Trends

Adoption of 300mm Wafer Fabrication Technologies

Integration of AI Driven Process Optimization in Semiconductor Fabs

Increasing Investment in Advanced Semiconductor Packaging Technologies - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Integrated Circuit Fabrication Systems

Wafer Processing Equipment

Semiconductor Assembly and Packaging Systems

Advanced Lithography Systems

Semiconductor Testing and Inspection Systems - By Platform Type (In Value%)

300mm Wafer Fabrication Platforms

200mm Wafer Fabrication Platforms

Compound Semiconductor Platforms

MEMS Manufacturing Platforms

Advanced Packaging Platforms - By Fitment Type (In Value%)

Fully Automated Semiconductor Production Lines

Modular Semiconductor Fabrication Systems

High Precision Cleanroom Installed Systems

Integrated Fab Automation Solutions

Retrofitted Semiconductor Manufacturing Equipment - By End User Segment (In Value%)

Integrated Device Manufacturers

Pure Play Semiconductor Foundries

Outsourced Semiconductor Assembly and Test Providers

Fabless Semiconductor Design Companies

Consumer Electronics Component Manufacturers - By Procurement Channel (In Value%)

Direct Procurement from Equipment Manufacturers

Strategic Technology Partnerships

Government Supported Semiconductor Programs

Industrial Supply Chain Distributors

Long Term Semiconductor Equipment Contracts

- Market Share Analysis

- Cross Comparison Parameters (Technology Node Capability, Wafer Size Support, Packaging Technology, Production Capacity, Automation Level, Lithography Technology, Yield Optimization Systems, Cleanroom Class Infrastructure, Energy Efficiency in Fabrication, Advanced Packaging Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

GlobalFoundries

Micron Technology

Infineon Technologies

United Microelectronics Corporation

Siliconware Precision Industries

STMicroelectronics

Texas Instruments

NXP Semiconductors

ASM International

Applied Materials

Lam Research

Tokyo Electron

ASE Technology Holding

Broadcom

Qualcomm

- Integrated Device Manufacturers Expanding Local Fabrication Capacity

- Foundry Operators Scaling Advanced Node Production Facilities

- Outsourced Assembly and Test Providers Strengthening Packaging Capabilities

- Consumer Electronics Manufacturers Increasing Semiconductor Component Sourcing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now