Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Singapore tennis equipment market’s current economic footprint can be approximated through related racket sports equipment data, which includes tennis rackets, balls, and accessories. In the broader Singapore racket sports equipment market, revenues are projected at USD ~ million, reflecting the combined impact of racket sports such as tennis and badminton and indicating robust consumer spend on racket sports gear. This revenue base is driven by rising demand for quality performance equipment among both recreational players and competitive enthusiasts as national participation in racket sports continues to expand alongside premium product import growth.

Demand is concentrated in Singapore’s urban centres, supported by high disposable income levels and strong public and private sports infrastructure. Cities such as Singapore’s Central and East regions dominate the market due to dense populations, a higher presence of tennis clubs and facilities, and accelerated participation driven by youth and adult recreational programs. Additionally, Singapore’s strategic role as a regional retail and distribution hub attracts global sports brands, reinforcing its position as a leading centre for tennis equipment availability in Southeast Asia.

Market Segmentation

By Product Type

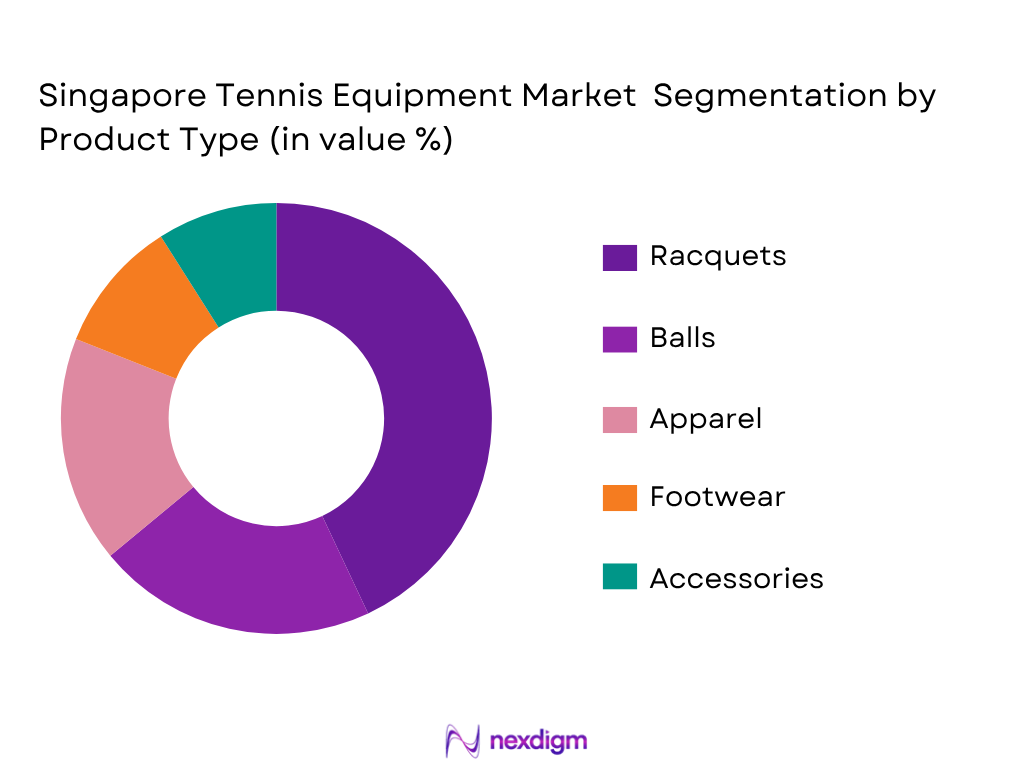

In Singapore, rackets account for the largest share of tennis equipment revenue due to high unit prices and strong consumer preference for premium performance frames among recreational and competitive players. Global and regional brands such as Wilson, Babolat, and Head dominate retail inventories in specialist stores and e‑commerce platforms, reinforcing this sub‑segment’s prominence. Tennis balls follow as the next largest revenue contributor, driven by regular replacement cycles among both club players and casual users. Apparel and footwear also hold meaningful share, supported by urban consumers who align sportswear with lifestyle and fitness preferences. Accessories (grips, bags, stringing kits) round out the portfolio but contribute a smaller share due to lower unit prices.

By Distribution Channel

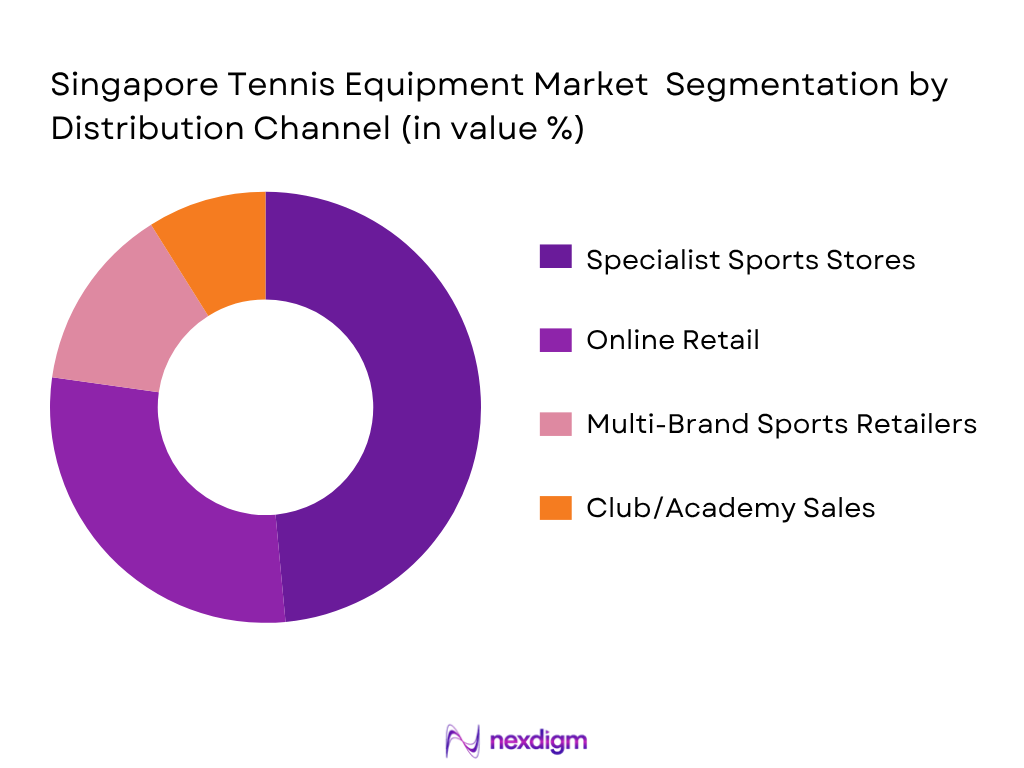

Specialist sports stores represent the dominant distribution channel for tennis equipment in Singapore. These outlets provide product expertise, brand variety, and services such as racket demo options and stringing, which appeal to serious players and first‑time buyers alike. Moreover, physical retail stores located near major shopping and sports precincts consolidate traffic from both locals and expatriates, reinforcing their leading role. Online retail is the second most significant channel, driven by convenience, broader model availability, and competitive pricing, particularly among younger and more tech‑savvy consumers. Multi‑brand sports retailers and club/academy procurement play smaller roles but support niche demand from institutional buyers and coaching programmes.

Competitive Landscape

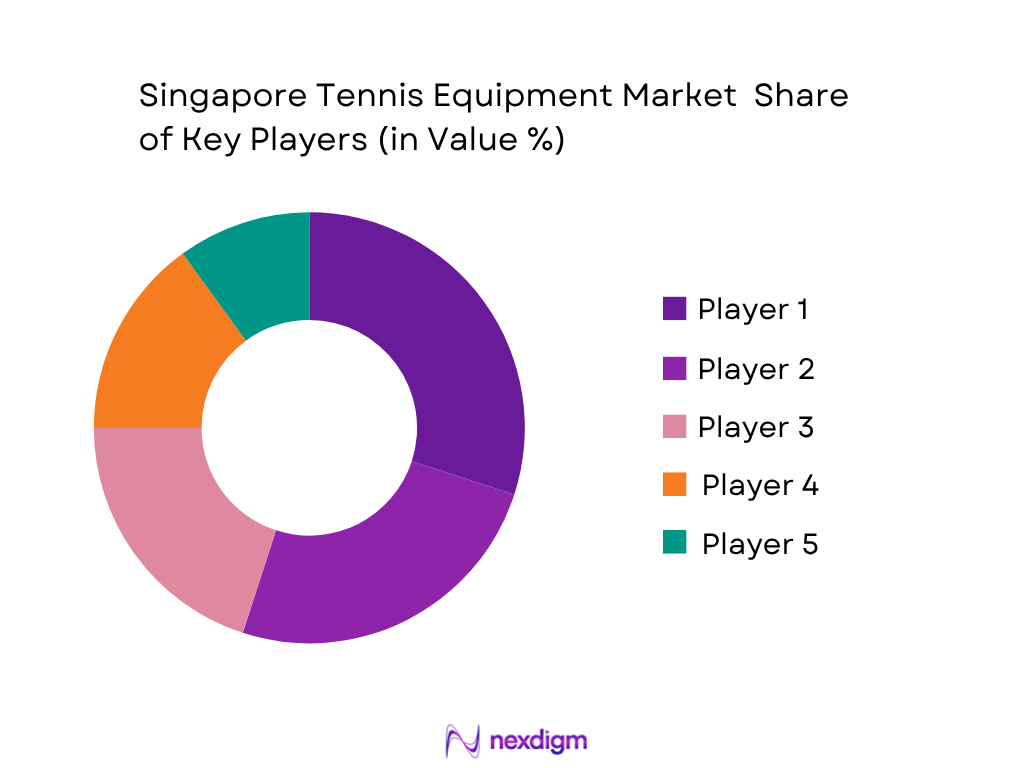

Tennis equipment retail in Singapore features a mix of international brands with strong global recognition and local specialist retailers addressing niche customer needs. The Singapore tennis equipment market is characterised by competition among leading global brands distributed through specialist retailers and online channels. International manufacturers maintain influence through brand loyalty, product innovation, and high visibility in specialty stores. Retail consolidation is limited, with multiple mid‑size and boutique players co‑existing, reflecting the fragmented nature of consumer demand.

| Company | Year Established | Headquarters | Brand Portfolio Depth | Retail Footprint | Online Presence | Customization/ Services | Import Partnerships |

| Wilson Sporting Goods | 1914 | USA | ~ | ~ | ~ | ~ | ~ |

| Babolat | 1875 | France | ~ | ~ | ~ | ~ | ~ |

| Head N.V. | 1950 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| Yonex Co., Ltd. | 1946 | Japan | ~ | ~ | ~ | ~ | ~ |

| Decathlon Singapore | 2001 | France | ~ | ~ | ~ | ~ | ~ |

Singapore Tennis Equipment Market Analysis

Growth Drivers

Tennis Participation Rate and Growth Index (Clubs, Courts Usage)

Singapore’s national annual Sport & Exercise Participation Survey (NSPS) provides the most credible insight into resident involvement in sporting activities that include tennis as part of racket sports and physical exercise. The NSPS, conducted by Sport Singapore with a minimum annual sample of 4,500 respondents, tracks weekly participation across sports, indicating structured growth in overall physical activity engagement. Although the NSPS does not break out tennis specifically, it reflects sport participation behaviour where Singapore residents aged 13 and above increasingly engage in weekly physical activity. The availability and usage of sports facilities managed by Sport Singapore show consistent activity: annual facility usage data through 2025 indicates sustained engagement with public courts and sports facilities across Singapore. With a population of 6 million people as of 2024, according to the World Bank, this urban market has a dense base of potential players accessing courts and club programmes foundational for rising tennis participation and subsequent increased demand for tennis equipment. Population growth of 2.0% supports the continued expansion of active lifestyles. Frequent participation in broader sports translated into ancillary demand for sport‑specific gear such as rackets, balls, and apparel, feeding the tennis equipment ecosystem in dedicated clubs and recreational settings.

Disposable Income & Sports Spend Elasticity

Singapore is characterised by significant consumer purchasing power, a key driver of discretionary sports equipment spending. According to the World Bank, Singapore’s GDP per capita reached USD 90,674.1 in 2024, reflecting a high‑income economy with residents possessing robust spending capacity on leisure and performance products. This level of per‑capita income places Singapore among the world’s most affluent nations, making sports equipment such as tennis rackets, premium balls, and performance apparel an accessible purchase for a large proportion of the population. Moreover, Singapore’s GDP growth of 4.4% in 2024 and a low unemployment rate of 2.8% in 2025 contribute to economic stability and rising consumer confidence in discretionary purchases. These macroeconomic conditions allow households to allocate a portion of spending toward non-essential goods, including sport and fitness categories. With inflation at 2.4% in 2024, consumer price levels remained moderate relative to income growth, helping to preserve real disposable income for retail expenditure. High internet penetration (94% of the population) also underpins diverse retail choices and price competition that fuel sports equipment purchase behaviour as part of broader lifestyle consumption preferences.

Market Challenges

Competition from Other Sports

Singapore’s sports ecosystem is diverse, with multiple popular activities competing for participant time, club memberships, and retail spending. Government and public data indicate that sports such as football, swimming, basketball, badminton, table tennis and cycling dominate recreational participation patterns, often drawing significant user engagement and facility usage. While tennis participation is embedded within broader sports activity frameworks, it remains less prominent compared with these mainstream sports—a factor that limits the share of users prioritising tennis equipment purchases. The Sport in Singapore overview shows that outdoor and community sports infrastructure emphasises highly ranked sports with broad appeal, creating a competitive landscape where tennis must vie for attention against both low‑cost participation options (like community basketball or public swimming) and emerging trends in racket sports such as padel and pickleball. These alternatives absorb spend that might otherwise have been allocated to tennis gear, reducing the marginal growth potential for tennis‑specific equipment. Compounding this, competitive discounting and expansive retail positioning by large sports chains in general sport categories push tennis equipment into a lower priority retail segment, weakening its competitive positioning in physical stores and omnichannel platforms where multiple sports gear categories compete for shelf space.

Import Cost Structure & Tariff Influence on ASP

Singapore’s status as a free‑trade economy reduces traditional tariff barriers for imported goods, yet import cost structures still materially influence consumer pricing for tennis equipment. While Singapore’s World Bank data show the applied weighted mean tariff rate on all products at approximately 0.05%, effectively zero for most goods, importers typically face a 9% Goods and Services Tax (GST) on imported goods at CIF (Cost, Insurance & Freight) value plus any duties or charges. This GST applies broadly to imported tennis rackets, balls, apparel, and accessories unless exempted, adding to landed cost before retail pricing. Even with near‑zero tariffs, the tax regime increases upfront import costs, which is passed through to average selling prices (ASP) for consumers. Moreover, firms must absorb non‑tariff costs such as freight, insurance, and distribution logistics in Singapore’s global supply chain context. These cost inputs have a direct bearing on retail price points for imported high‑end equipment, making premium tennis products relatively expensive compared with locally available substitutes or mass‑market alternatives from other sports categories. This cost structure challenge can deter price‑sensitive buyers and compress margin potential for retailers in specialist tennis equipment segments.

Market Opportunities

Product Technology Adoption

In the Singapore tennis equipment market, the adoption of product innovations such as advanced racket materials, optimized string technology, sensor integration and ergonomic grip systems presents a clear opportunity to drive demand among performance‑oriented players. Singapore’s affluent consumer base, indicated by a GDP per capita of USD 90,674.1 in 2024, supports the willingness to spend on premium and technologically differentiated sporting goods. The high level of internet penetration (94% of the population) facilitates educated and connected consumer behaviour that often follows technical specifications, peer reviews, and advanced performance features in sport equipment. Furthermore, national economic growth supports a competitive market where retailers can stock and promote cutting‑edge products that cater to discerning recreational and competitive players. Technology adoption in products such as rackets with vibration dampening systems and digital analytics tools near consumer gaming and fitness segments increases the perceived value of advanced tennis gear. As global manufacturers continue incorporating performance‑enhancing materials and digital compatibility, Singapore’s status as a premium retail destination ensures early availability and adoption, enabling the market to capture incremental spend from tech‑savvy consumers seeking differentiated equipment experiences that heighten play and training outcomes.

E‑Commerce and Omnichannel Fulfillment

E‑commerce growth in Singapore underscores a material opportunity for tennis equipment distribution, driven both by cross‑border and domestic online retail. Singaporeans demonstrate strong online shopping behaviour, evidenced by the tripling of e‑commerce volumes in recent years as consumers increasingly embrace digital retail channels for a variety of categories including sports goods. Convenience, broader product selection, and the ability to compare prices contribute to a robust online retail environment where tennis equipment can reach customers beyond physical store limitations. Cross‑border e‑commerce trends reflect broader consumer inclination to access specialized products not easily found locally, opening avenues for niche tennis brands to access the Singapore market through online channels. The high internet penetration (94%) and preference for quality and functionality in online purchases reinforce the potential for omnichannel strategies where consumers research online and convert either via click‑and‑collect at specialist stores or direct home delivery. As omni‑fulfillment models mature, integrating digital platforms with personalized service offerings such as stringing and demo bookings can further enhance customer acquisition and retention, ultimately expanding the market footprint beyond traditional retail.

Future Outlook

The outlook for the Singapore tennis equipment market over the coming decade is positive. Growth will be underpinned by increasing recreational participation, ongoing investments in tennis infrastructure, and continued consumer preference for high‑performance playing gear. Urban wellness trends, coupled with academy expansion and junior programme uptake, will sustain demand for both premium and entry‑level products. Digital commerce channels will continue to expand reach and convenience, particularly among younger cohorts. Finally, strategic import partnerships and brand innovations will support product differentiation and long‑term market expansion.

Major Players

- Wilson Sporting Goods

- Babolat

- Head N.V.

- Yonex Co., Ltd.

- Decathlon Singapore

- Adidas AG (Tennis Apparel/Footwear)

- Nike, Inc. (Tennis Apparel/Footwear)

- Tecnifibre

- Dunlop Sport

- Prince Tennis

- TennisHub (Singapore Retail)

- RacketHaus (Singapore Retail)

- Leisure Sports Singapore

- Specialist Sports SG

- Sports shop SG

Key Target Audience

- Regional Sporting Goods Retailers

- National Tennis Federations & Associations

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Tennis Clubs & Coaching Academies

- E‑Commerce Marketplace Operators

- Import/Distribution Partners & Logistics Firms

- Brand License Holders & Franchise Operators

Research Methodology

Step 1: Data Collection and Definitions

Primary and secondary data were gathered from industry databases, trade reports, and verified online sources. Market definitions and product categories were standardised to ensure consistency in segmentation and reporting.

Step 2: Market Analysis and Benchmarking

Historical and current revenue figures were analysed alongside import trends and consumer participation data. Competitive benchmarking included retail footprints, brand portfolios, and distribution strategies.

Step 3: Expert Validation

Hypotheses were validated through consultations with market practitioners within Singapore’s sports retail ecosystem, including store managers, distributors, and coaches to refine assumptions and product insights.

Step 4: Forecasting and Synthesis

A bottom‑up approach informed revenue and CAGR forecasts, with import and consumer demand trends factored into longer‑term projections. Findings were triangulated across multiple data sources to enhance reliability.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Segmentation Logic and Nomenclature, Data Sources and Validation Protocols, In‑Depth Primary Research Framework (Retailers, Clubs, Coaches, Players), Forecasting Models, Limitations and Market Scope Boundaries)

- Market Genesis & Evolution

- Demand Landscape and Participation base

- Distribution & Supply Dynamics

- Sports Infrastructure Overview

- Product Life Cycle Intensity by Type

- Growth Drivers(Tennis Participation Rate and Growth Index, Disposable Income & Sports Spend Elasticity, Health & Fitness Trends Affecting Tennis Engagement, Brand Endorsement Impact Score)

- Market Challenges (Competition from Other Sports and Leisure Activities, Import Cost Structure & Tariff Influence on ASP, Retail Footprint Limitations, Store Density Constraints, Seasonal Demand Variability)

- Market Opportunities (Product Technology Adoption, E‑Commerce and Omnichannel Fulfillment Trends, Sustainability and Eco‑Material Integration)

- Trends (Social Tennis Events & Community-Led Engagement, Sustainability Initiatives in Apparel & Accessories, Digital Coaching Integration, Youth-Oriented Performance Gear)

- Retail Integration, Social Play & Community‑Led Marketing)

- Regulatory Environment (Product Safety and Certification Requirements, Import Duties & Trade Tariff Impacts, Advertising and Endorsement Guidelines)

- SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats of the Singapore tennis equipment market)

- Stakeholder Ecosystem (Relationships among manufacturers, distributors, retail chains, sports federations, tennis clubs and coaches)

- Porter’s Five Forces (Competitive rivalry, supplier power (e.g. material suppliers), buyer power, threat of new entrants (niche sports tech startups), threat of substitutes)

- By Value (2020-2025)

- By Units and Volume Distribution (2020-2025)

- By Average Selling Price Trends (2020-2025)

- By Import vs Domestic Supply Mix (2020-2025)

- By Product Type (In Value %)

Rackets

Tennis Balls

Apparel & Footwear

Accessories

Court Equipment & Training Tools - By Consumer Application (In Value %)

Recreational Play

Competitive Training & Tournament

Coaching & Academia

Corporate & Fitness Programs - By Sales Channel (In Value %)

Specialty Pro Shops

Multi‑brand Sports Retailers

E‑Commerce Platforms

Club & Academy Procurement - By Consumer Cohort (In Value %)

Junior/Youth

Adult Beginner

Intermediate

Advanced/Competitive Players

Coaches & Institutions - By Price Tier (In Value %)

Entry

Mid

Premium & Professional

- Market Share (Value & Volume) by Major Entities

- Cross Comparison Parameters (Brand Portfolio Depth, Retail & E‑Commerce Presence Score, Pricing Tier Coverage, Exclusive Distribution Agreements, Revenue by Product Segment, Stringing/Customization Services Offered, Store Density and Foot Traffic Metrics, Digital Engagement & Loyalty Program Impact)

- Competitive Intensity Mapping (Concentration, Fragmentation)

- Channel and Tier‑Level Competition Dynamics

- SWOT of Major Players (Strengths, Weaknesses, Opportunities, Threats for key companies)

- Pricing & Promotional Benchmarking (Average selling prices and SKU-level pricing for major brands, premium vs standard product lines)

- Detailed Profiles of Major Players

Leisure Sports

RacketHaus

TennisHub

Transworld Sports

C & E Sports

MY Tennis Court SG PTE. LTD.

Wilson Sporting Goods

Yonex Co., Ltd.

Babolat VS S.A.

Head N.V.

Dunlop Sports

Prince Tennis

Adidas AG

Nike, Inc.

Tecnifibre

- Demand and Utilization (Sales breakdown by end-user type: recreational players vs professional athletes, club/academy purchases)

- Consumer Demographics and Purchasing Behavior (Age, income, gender distribution, purchasing frequency, channel preferences)

- Budget and Price Sensitivity (Pricing tiers: premium vs mid-range vs value segment, consumer spending patterns on equipment and apparel)

- Needs, Desires and Pain Points (Comfort, performance, and durability requirements, desire for brand/image, issues like gear availability or fitting)

- Decision-Making Process (Influencers in purchase decisions: coaches’ recommendations, peer reviews, online research, role of professional endorsements and demo clinics)

- By Value (2026-2035)

- By Units and Volume Distribution (2026-2035)

- By Average Selling Price Trends (2026-2035)

- By Import vs Domestic Supply Mix (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now