Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Singapore toys and games market is valued at approximately USD ~ million in 2025, based on comprehensive industry data tracking retail sales across physical and digital product categories. This valuation reflects sustained consumer expenditure on both traditional playthings and interactive gaming products, with demand supported by relatively high household disposable incomes and robust participation in leisure spending. Licensed merchandise, educational toys, and video game-related products have contributed to overall market traction.

Key regional hubs such as Singapore’s Central Business District (CBD), Orchard Road, and major suburban retail precincts dominate market activity due to high footfall in large-format retail outlets, premium toy stores, and integrated entertainment complexes. Singapore’s status as a strategic distribution point in Southeast Asia also attracts international brands, making it a preferred location for flagship launches and experiential retail. Urban affluence and dense population clusters further consolidate demand in these areas.

Market Segmentation

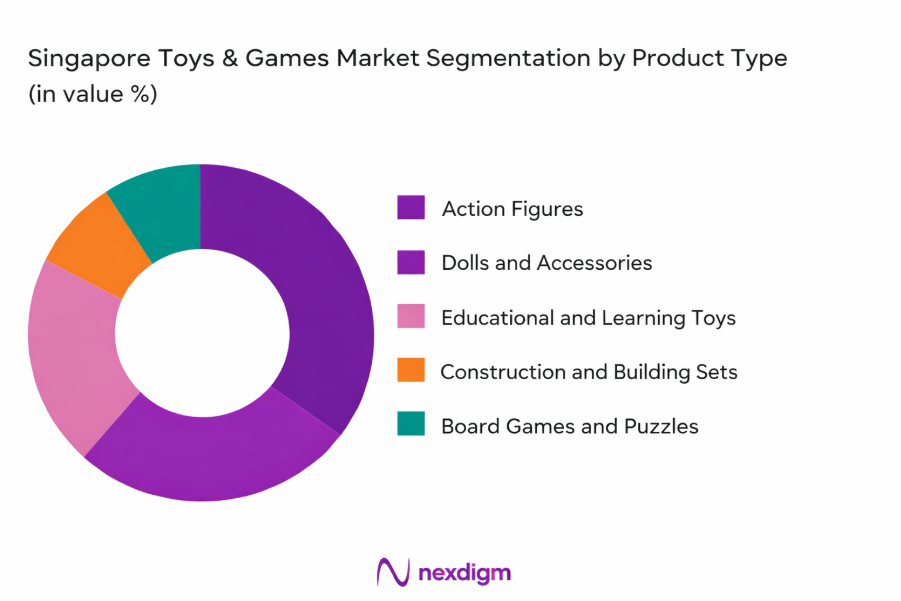

By Product Type

The Singapore toys and games market is segmented by product type into action figures, building sets, games and puzzles, dolls, sports and outdoor toys, and other miscellaneous categories. In recent years, action figures have maintained dominance within this segmentation due to strong brand licensing, franchise popularity (such as superheroes and pop culture characters), and collector demand that extends beyond traditional child consumers to teen and adult segments. International franchises and promotional tie-ins with media content further elevate the appeal of this sub segment.

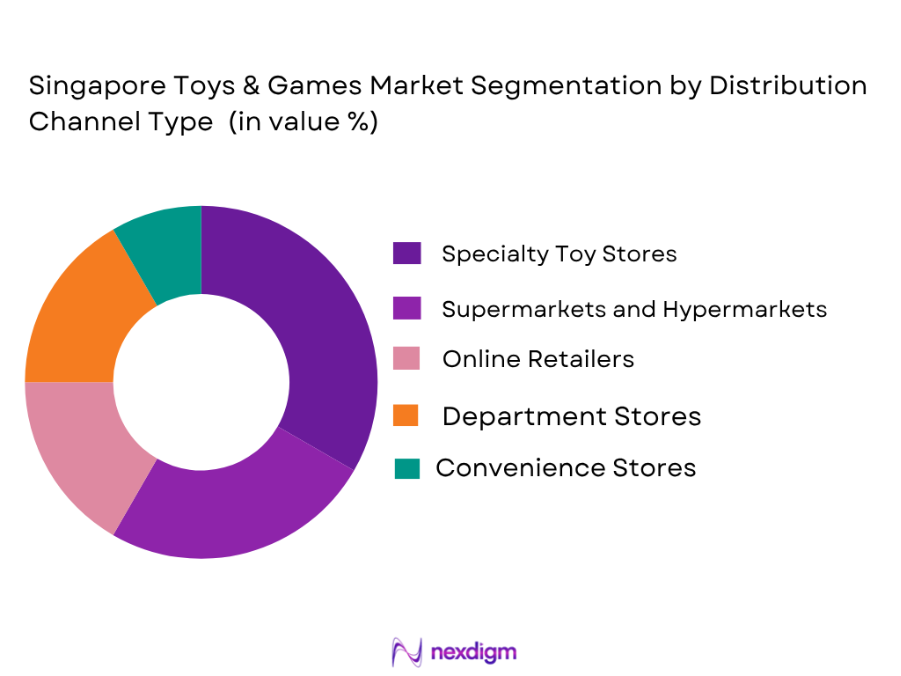

By Distribution Channel Type

Under distribution channels, the Singapore market is categorized into specialty toy stores, supermarkets and hypermarkets, online channels, department stores, and convenience stores. Specialty toy stores hold the largest share, largely because they offer extensive assortments and dedicated retail experiences that appeal to both children and adult hobbyists. These outlets often curate exclusive product lines, host in‑store events, and provide knowledgeable staff, creating a differentiated retail environment compared with mass retail formats.

Competitive Landscape

The Singapore toys and games market features a competitive structure with several global and regional players shaping industry dynamics. Established international brands leverage extensive portfolios and distribution relationships to sustain visibility and consumer loyalty. At the same time, niche importers and local distributors contribute to market diversity by supplying emerging product categories.

| Company | Establishment Year | Headquarters | Product Portfolio Breadth | Regional Presence | Distribution Reach | Retail Footprint | Licensing Partnerships | Marketing Investment |

| LEGO Group | 1932 | Denmark | ~ | ~ | ~ | ~ | ~ | ~ |

| Hasbro, Inc. | 1923 | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Mattel, Inc. | 1945 | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Bandai Namco Holdings | 1950 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Sunshing Marketing Pte Ltd | 1980 | Singapore | ~ | ~ | ~ | ~ | ~ | ~ |

Singapore Toys & Games Market Analysis

Growth Drivers

Increase in Disposable Income and Consumer Spending

The Singapore toys and games market is significantly propelled by the rise in disposable income among households, which directly translates to higher consumer spending on leisure and recreational products. Families are increasingly allocating a portion of their budgets to toys that offer educational value, entertainment, or both. The presence of premium retail outlets, branded toy stores, and experiential play centers encourages discretionary spending, while urban affluence in central and suburban areas ensures consistent demand. Additionally, dual-income households with greater purchasing power are investing in both traditional toys and digital gaming devices. This sustained consumer spending drives overall market expansion, making Singapore one of the most lucrative Southeast Asian markets for toys and games.

Rising Popularity of Educational and STEM Toys

The growing emphasis on early childhood development and skill-based learning has accelerated demand for educational and STEM (Science, Technology, Engineering, Mathematics) toys in Singapore. Parents increasingly prefer products that combine entertainment with cognitive and motor skill enhancement. Schools, enrichment centers, and after-school programs also integrate these toys into learning activities, further expanding market uptake. Brands offering interactive kits, coding-based games, and science experiment sets gain significant traction among both children and teenagers. This segment benefits from continuous innovation, global partnerships, and marketing campaigns highlighting the educational value, positioning STEM-focused toys as a preferred choice for consumers seeking long-term developmental benefits alongside recreational play.

Market Challenges

High Competition and Price Sensitivity

The Singapore toys and games market faces intense competition from both local distributors and global brands, which often leads to price-based rivalry. Consumers have access to a wide variety of domestic and imported products, driving demand for competitive pricing without compromising quality. New entrants and online marketplaces increase pressure on traditional retail outlets, forcing brands to innovate or adjust prices. Price sensitivity among parents, especially for non-essential luxury or branded items, can limit revenue growth. Seasonal sales and promotional campaigns further intensify competition. The combination of diversified consumer options, price-conscious behavior, and aggressive marketing strategies by competitors challenges established players to maintain profitability while sustaining market share.

Regulatory Compliance and Safety Standards

Strict regulatory requirements regarding toy safety, labeling, and material quality present significant challenges for market participants in Singapore. Compliance with Singapore Consumer Protection (Safety Requirements) regulations ensures that products meet safety standards for children, including toxicity limits, small parts restrictions, and electronic safety certifications. Non-compliance can lead to product recalls, fines, or reputational damage, adding operational complexity. Manufacturers and importers must invest in testing, quality assurance, and certification processes, which increases production costs. Additionally, evolving regulations necessitate ongoing monitoring to ensure adherence. These factors create barriers for new entrants and require established companies to maintain rigorous compliance frameworks to sustain consumer trust and market credibility.

Opportunities

Emergence of Eco-friendly and Sustainable Toys

The growing awareness of environmental sustainability presents a notable opportunity in Singapore’s toys and games market. Consumers are increasingly seeking eco-friendly alternatives made from recycled, biodegradable, or non-toxic materials. Companies that incorporate sustainable production methods and environmentally responsible packaging can differentiate themselves in a crowded market. Eco-conscious parents are willing to pay a premium for products that reduce environmental impact, particularly in urban areas with strong environmental advocacy and government initiatives supporting green practices. This trend also aligns with global movements in sustainability, enabling Singapore-based companies to leverage international partnerships and appeal to both local and export markets. The demand for sustainable toys is expected to rise steadily, creating a niche growth segment.

Integration of AR/VR and Smart Technology in Toys

Advancements in augmented reality (AR), virtual reality (VR), and smart technology provide a significant growth avenue for the Singapore toys and games market. Interactive and tech-enabled toys, such as AR-based learning kits, app-connected robots, and VR gaming accessories, attract tech-savvy children and parents seeking immersive experiences. These products bridge physical play and digital engagement, creating added value and educational benefits. The integration of technology allows for personalized experiences, gamification, and extended product lifecycles, increasing consumer retention. Additionally, collaborations with software developers and content creators enhance interactivity, positioning Singapore as a forward-looking market for innovation-driven toys. Market adoption of such products is accelerating due to growing digital literacy and parental willingness to invest in smart play solutions.

Future Outlook

Over the 2025–2035 period, the Singapore toys and games market is expected to grow steadily, supported by continued consumer spending on both traditional play products and digital gaming experiences. Market momentum will be influenced by sustained interest in licensed and branded merchandise, expansion of online retail channels, and innovations that blend physical toys with digital interactivity. Technological integration and experiential retail formats are likely to become more significant drivers of market expansion.

Major Players

- LEGO Group

- Hasbro, Inc.

- Mattel, Inc.

- Bandai Namco Holdings

- TOMY Company, Ltd.

- Dream International Limited

- Sunshing Marketing Pte Ltd

- Spin Master Corp.

- Funko, Inc.

- VTech Holdings Ltd.

- Playmates Toys

- Ravensburger AG

- Jakks Pacific, Inc.

- Mega Brands Inc.

- Schylling Inc.

Key Target Audience

- Retail buyers and toy importers

- Domestic and international toy manufacturers

- Investment and venture capitalist firms

- Government and regulatory bodies

- Specialty retail chains’ procurement teams

- Children’s entertainment and amusement operators

- E‑commerce platform category managers

- Licensing and brand partnership divisions

Research Methodology

Step 1: Market Definition and Scoping

The initial stage involves defining the Singapore toys and games ecosystem, identifying key product categories, distribution channels, and end‑user groups based on secondary research, industry classification standards, and consumer segmentation frameworks.

Step 2: Data Collection and Validation

This phase compiles verified historical market data from reputable industry reports and financial disclosures, supported by expert interviews. It includes sales data, retail trends, and distribution performance, ensuring accuracy through triangulation across multiple sources.

Step 3: Expert Consultation and Input

Market assumptions and preliminary findings are refined through structured interviews with industry professionals, including brand representatives, retail executives, and distribution partners. These expert engagements provide qualitative insights into market drivers and challenges.

Step 4: Forecast Modelling and Analysis

Analytical models are constructed using historical data and validated assumptions to develop forward‑looking forecasts. Scenario analysis evaluates potential growth pathways, accounting for macroeconomic conditions and evolving consumer behavior.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach Understanding Market Potential Through In-Depth Industry Interviews, Primary Research Approach, Limitations and Future Conclusions)

- Definition and Scope

- Market Dynamics Overview

- Market Genesis

- Major Players and Market Timeline

- Business Cycle and Trends

- Supply Chain and Value Chain Analysis

- Growth Drivers

Increase in Disposable Income and Consumer Spending

Rising Popularity of Educational and STEM Toys

Growing Influence of Licensing and Branded Merchandise

Expansion of E-commerce and Online Retail Channels

Rising Interest in Interactive and Digital Toys - Market Challenges

High Competition and Price Sensitivity

Rapid Product Obsolescence

Regulatory Compliance and Safety Standards

Fluctuating Raw Material Costs

Counterfeit and Unlicensed Products - Opportunities

Emergence of Eco-friendly and Sustainable Toys

Integration of AR/VR and Smart Technology in Toys

Expansion of Online and Direct-to-Consumer Channels

Growing Licensing Partnerships and Brand Collaborations

Innovative Product Designs and Customization - Key Trends

Focus on Educational and STEM-oriented Toys

Integration of Technology and Gamification

Popularity of Collectibles and Limited Edition Toys

Demand for Sustainable and Environmentally Friendly Products

Growth of Online Toy Marketplaces - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Value, 2020–2025

- By Volume, 2020–2025

- By Average Price, 2020–2025

- By Product Type (In Value %)

Action Figures

Dolls and Accessories

Educational and Learning Toys

Construction and Building Sets

Board Games and Puzzles - By Material Type (In Value %)

Plastic

Wood

Metal

Fabric/Textile

Others - By Age Group (In Value %)

Infants (0–2 Years)

Toddlers (3–5 Years)

Children (6–12 Years)

Teenagers (13–18 Years)

Adults (18+ Years) - By Distribution Channel (In Value %)

Specialty Toy Stores

Supermarkets and Hypermarkets

Online Channels

Department Stores

Convenience Stores - By Region (In Value %)

Central Singapore

East Singapore

West Singapore

North Singapore

North-East Singapore

- Market Share of Major Players by Value/Volume

- Market Share of Major Players by Product Type

- Cross Comparison Parameters (Company Overview, Business Strategies, Recent Developments, Strength, Weakness, Organizational Structure, Revenues, Revenues by Product Type, Number of Touchpoints, Distribution Channels, Number of Dealers and Distributors, Margins, Production Plant, Capacity, Unique Value Offering and Others)

- SWOT Analysis of Major Players

- Pricing Analysis Based on Product Categories for Major Players

- Detailed Profiles of Major Companies

Hasbro, Inc.

LEGO Group

Mattel, Inc.

Bandai Namco Holdings

Spin Master Corp.

Tomy Company, Ltd.

Funko, Inc.

Playmates Toys

MEGA Brands Inc.

VTech Holdings Ltd.

Fisher-Price, Inc.

Ravensburger AG

Jakks Pacific, Inc.

Gund, Inc.

SMT Toys & Games Pte Ltd.

- Market Demand and Utilization

- Purchasing Power and Budget Allocations

- Regulatory and Compliance Requirements

- Needs, Desires, and Pain Point Analysis

- Decision-Making Process

- By Value, 2026–2035

- By Volume, 2026–2035

- By Average Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now