Download PDF

Download PDF Download PDF

Download PDF- UBS

- Credit Suisse

- DBS Private Bank

- HSBC Global Private Banking

- Julius Baer

- Standard Chartered Private Bank

- Citi Private Bank

- Bank of Singapore

- OCBC Private Bank

- BNP Paribas Wealth Management

- Morgan Stanley Private Wealth

- Goldman Sachs Private Wealth

- Lombard Odier

- Pictet Wealth Management

- UOB Private Bank

Market Overview

Singapore’s wealth management market administers approximately USD ~ trillion in assets under management within its financial system, supported by private banking inflows, institutional mandates, and regional capital allocation activities reported by the Monetary Authority of Singapore and global asset managers. Market expansion is driven by high-net-worth population growth, cross-border portfolio diversification demand, and strong inflows from family offices and global investors establishing regional investment hubs within Singapore’s regulated financial environment.

Within Singapore, the central financial district dominates wealth management activity due to concentration of private banks, asset managers, and advisory platforms integrated with global custody and investment infrastructure. The country leads Asia’s offshore wealth management flows because of political stability, strong investor protection, and advanced capital market connectivity enabling seamless access to global equities, alternatives, and structured products, attracting affluent investors from Southeast Asia, China, and Middle Eastern markets.

Market Segmentation

By Product Type

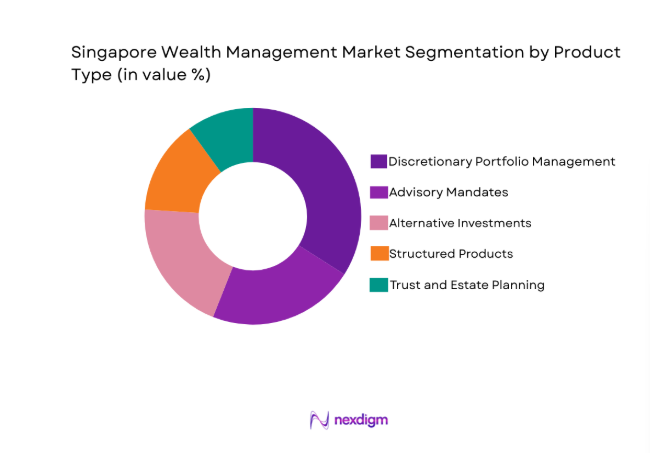

Singapore Wealth Management market is segmented by product type into discretionary portfolio management, advisory mandates, alternative investments, structured products, and trust and estate planning. Recently, discretionary portfolio management has a dominant market share due to factors such as institutionalized investment frameworks, global asset allocation capabilities, and strong client preference for professionally managed diversified portfolios aligned with cross-border wealth preservation objectives and regulatory reporting requirements.

By Platform Type

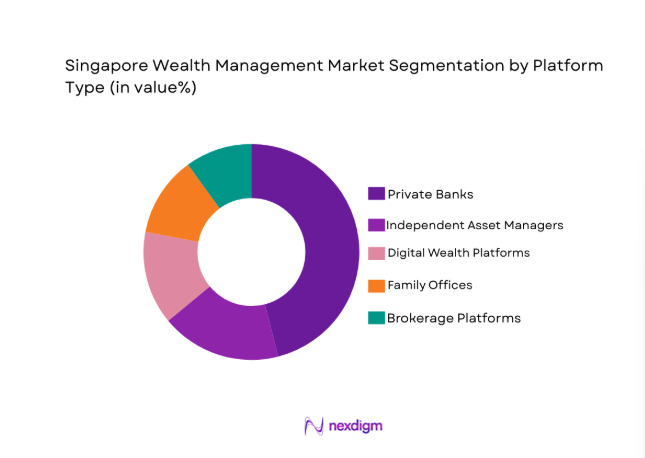

Singapore Wealth Management market is segmented by platform type into private banks, independent asset managers, digital wealth platforms, family offices, and brokerage platforms. Recently, private banks have a dominant market share due to factors such as global custody infrastructure, integrated lending and investment services, strong brand trust among high-net-worth clients, and ability to structure complex cross-jurisdiction portfolios within Singapore’s regulated financial ecosystem.

Competitive Landscape

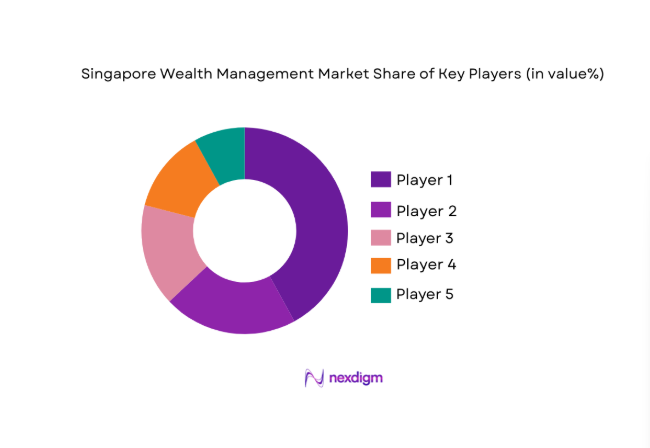

Singapore’s wealth management market is highly consolidated around global private banks and large asset managers operating regional hubs in the country, supported by regulatory licensing frameworks that encourage international firms to book Asian client assets locally. Competition centers on portfolio advisory sophistication, alternative investment access, and cross-border structuring expertise, with major players leveraging global investment platforms and family office services to attract ultra-high-net-worth clients.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AUM Focus |

| UBS | 1862 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Credit Suisse | 1856 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| DBS Private Bank | 1968 | Singapore | ~ | ~ | ~ | ~ | ~ |

| HSBC Global Private Banking | 1865 | UK | ~ | ~ | ~ | ~ | |

| Julius Baer | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

Singapore Wealth Management Market Analysis

Growth Drivers

Expansion of Ultra-High-Net-Worth Population and Family Office Inflows

Singapore’s wealth management market growth is structurally anchored in the rapid expansion of ultra-high-net-worth individuals and the migration of family office capital into Singapore’s regulated financial ecosystem, which has transformed the country into Asia’s primary booking center for offshore wealth preservation and intergenerational asset planning across emerging market investors. The city-state’s regulatory clarity, tax neutrality on investment gains, and strong investor protection frameworks have encouraged affluent families from Southeast Asia, China, and the Middle East to establish single and multi-family offices locally, transferring substantial global portfolios into Singapore-domiciled structures administered by private banks and independent asset managers. Family office establishment requirements tied to local investment and employment commitments have further embedded wealth assets within domestic financial institutions, increasing discretionary portfolio mandates and long-term custody relationships managed in Singapore. Global private banks and asset managers have responded by expanding regional investment teams, alternative asset distribution capabilities, and succession planning advisory services to capture these inflows, reinforcing market scale and sophistication. The presence of deep capital markets connectivity allows Singapore-based wealth managers to allocate client portfolios across global equities, private equity, hedge funds, and real assets efficiently, strengthening the country’s position as an international wealth allocation hub rather than merely a regional banking center. Wealth creators in technology, commodities, manufacturing, and trade sectors across Asia increasingly seek jurisdictional diversification of assets due to geopolitical and regulatory uncertainties in home markets, driving relocation of financial holdings into Singapore’s stable environment. This inflow is amplified by professionalization of family governance and generational transition planning, where heirs require institutional investment oversight, consolidated reporting, and fiduciary controls provided by Singapore-based wealth managers. As a result, wealth management institutions continue to experience sustained growth in assets under management, discretionary mandates, and advisory revenues anchored in structural demographic and capital migration trends favoring Singapore.

Institutionalization of Cross-Border Portfolio Diversification and Alternative Investment Access

Singapore’s wealth management market expansion is strongly propelled by rising demand among affluent investors for globally diversified portfolios and institutional-grade access to alternative investments that extend beyond domestic public markets and traditional asset classes available in their home jurisdictions. High-net-worth and ultra-high-net-worth clients increasingly allocate significant portions of their wealth to private equity, venture capital, private credit, hedge funds, and real assets such as infrastructure and real estate, seeking enhanced returns, inflation hedging, and portfolio resilience against global economic volatility. Singapore-based private banks and asset managers have developed extensive feeder fund structures, co-investment platforms, and curated alternative investment programs that allow clients to participate in global institutional opportunities previously restricted to large pension and sovereign funds. The regulatory framework supporting accredited investor regimes and cross-border fund distribution enables seamless marketing and execution of global alternative products to Singapore-booked clients, making the country a preferred access point for international asset managers distributing private market strategies across Asia. Wealth managers have also integrated sophisticated asset allocation models, risk analytics, and portfolio construction technologies that enable multi-asset diversification across regions and asset classes, reinforcing the value proposition of discretionary mandates managed in Singapore. Investors from emerging Asian economies increasingly rely on Singapore advisers to construct globally diversified portfolios insulated from domestic currency risk, political uncertainty, and capital market concentration, driving sustained demand for offshore wealth management services. The city’s position as a financial gateway connecting Asian capital with Western investment markets strengthens its attractiveness for cross-border portfolio deployment and custody. As alternative investment participation expands and global diversification becomes a structural necessity for wealth preservation, Singapore’s wealth management institutions benefit from higher fee pools, deeper client engagement, and long-duration portfolio relationships anchored in sophisticated cross-border investment capabilities.

Market Challenges

Rising Regulatory Compliance Complexity and Cost Burden for Cross-Border Wealth Structures

Singapore’s wealth management market faces significant structural pressure from the increasing complexity and cost of regulatory compliance associated with cross-border wealth structuring, tax transparency requirements, anti-money laundering controls, and evolving international reporting standards that govern offshore financial assets and investment flows. Wealth managers operating in Singapore must comply simultaneously with domestic financial regulations, international tax reporting frameworks, and multiple client-jurisdiction disclosure regimes, requiring extensive documentation, due diligence, and monitoring systems to ensure compliance across diverse client bases originating from numerous countries. Global initiatives on tax transparency and beneficial ownership disclosure have increased reporting obligations for trusts, holding companies, and family office vehicles administered through Singapore, raising administrative costs and operational complexity for private banks and independent asset managers. Compliance requirements related to source-of-wealth verification, transaction monitoring, and sanctions screening have expanded significantly, necessitating investment in advanced compliance technologies, specialized personnel, and ongoing regulatory engagement to maintain licensing and reputation standards. Smaller wealth managers and independent advisers face disproportionate cost burdens due to limited scale in compliance infrastructure, leading to industry consolidation as institutions merge or partner to share regulatory resources. Clients are also experiencing increased onboarding timelines and documentation demands, potentially affecting acquisition efficiency and client experience in competitive wealth management relationships. Regulatory divergence across jurisdictions adds further complexity when structuring cross-border portfolios and estate planning vehicles for internationally mobile clients. While Singapore maintains strong regulatory credibility that attracts global capital, the associated compliance intensity raises operational expenses and barriers to entry for wealth management firms. Consequently, maintaining regulatory alignment while preserving efficiency and profitability remains a persistent structural challenge for the market.

Intensifying Competition from Emerging Asian Wealth Hubs and Digital Wealth Platforms

Singapore’s wealth management sector encounters growing competitive pressure from other Asian financial centers and technologically enabled wealth platforms that are increasingly capable of attracting regional high-net-worth capital and delivering investment services traditionally dominated by Singapore-based institutions. Competing jurisdictions have strengthened regulatory frameworks, tax incentives, and financial infrastructure to position themselves as alternative booking centers for offshore wealth, encouraging regional investors to diversify wealth management relationships across multiple hubs rather than concentrating assets in Singapore. Concurrently, digital wealth platforms and fintech-enabled advisory models are transforming client expectations toward lower fees, transparent portfolio construction, and on-demand access to investment products, challenging traditional private banking models reliant on relationship-based advisory and premium pricing structures. Younger affluent investors, particularly entrepreneurs and technology professionals, demonstrate openness to digital investment solutions and hybrid advisory models that combine automated portfolio management with selective human advice, reducing dependence on legacy wealth management institutions. Private banks and asset managers in Singapore must therefore invest heavily in digital advisory tools, portfolio analytics platforms, and client experience technologies to maintain competitiveness against both regional hubs and fintech entrants. Fee compression pressures are intensifying as clients compare services across jurisdictions and platforms, demanding institutional investment access at lower cost levels. Talent competition is also increasing, with experienced relationship managers and investment specialists being recruited across Asian wealth centers. The convergence of regional competition and technological disruption is reshaping the competitive landscape, requiring Singapore-based wealth managers to continuously innovate while defending their historical leadership position.

Opportunities

Expansion of Institutional-Grade Alternative Investment Distribution to Mass Affluent Segments

Singapore’s wealth management market holds substantial opportunity in extending access to institutional-quality alternative investments beyond ultra-high-net-worth clients into the rapidly expanding mass affluent investor segment across Asia that seeks diversification and higher return potential traditionally reserved for elite portfolios. Financial innovation in fund structures, minimum investment thresholds, and feeder vehicle design enables wealth managers to package private equity, private credit, infrastructure, and real asset strategies into scalable formats suitable for affluent investors with lower capital bases than traditional institutional mandates. Regulatory support for accredited investor frameworks and cross-border distribution allows Singapore-domiciled funds to be marketed efficiently across regional client bases, positioning Singapore as the principal gateway for alternative investment penetration into emerging wealth segments. Digital subscription platforms and portfolio aggregation technologies further facilitate participation by simplifying onboarding, reporting, and investment monitoring for clients previously excluded from private markets. As wealth accumulation accelerates among professionals, entrepreneurs, and corporate executives across Asia, demand for sophisticated portfolio diversification tools expands beyond traditional high-net-worth tiers. Wealth managers that successfully democratize alternative investments while maintaining institutional standards of due diligence and governance can capture significant new fee pools and client relationships. Asset managers are increasingly partnering with Singapore-based distributors to access this expanding investor base through locally regulated channels. The combination of growing regional wealth, structural diversification demand, and scalable investment vehicles creates a powerful growth pathway for Singapore’s wealth management industry. This opportunity reinforces the city-state’s evolution from elite private banking center to comprehensive regional investment distribution hub.

Integration of Advanced Wealth Technology and Data-Driven Advisory Models

Singapore’s wealth management sector has strong opportunity to enhance productivity, scalability, and client engagement through the integration of advanced wealth technology platforms, artificial intelligence-driven portfolio analytics, and data-enabled advisory models that transform traditional relationship-centric service delivery into digitally augmented investment management ecosystems. Wealth managers are deploying portfolio optimization algorithms, risk modeling engines, and behavioral analytics tools that enable highly personalized asset allocation strategies aligned with client objectives, liquidity needs, and risk tolerance profiles across global investment markets. Digital client interfaces and consolidated reporting dashboards allow real-time portfolio visibility, performance tracking, and scenario analysis, improving transparency and engagement for sophisticated investors managing complex cross-border assets. Automation of compliance monitoring, onboarding workflows, and reporting processes reduces operational costs and enhances regulatory efficiency, enabling firms to scale client acquisition without proportional increases in staffing. Hybrid advisory models combining human expertise with algorithmic insights can serve broader client segments while maintaining quality and consistency of investment advice. Singapore’s strong fintech ecosystem and regulatory openness to financial innovation support experimentation and adoption of advanced wealth technologies within licensed institutions. Technology integration also enables seamless connectivity between private banks, asset managers, and family offices, creating unified wealth ecosystems anchored in Singapore. Firms that effectively leverage data and technology can differentiate through superior investment outcomes, efficiency, and client experience. This digital transformation pathway offers substantial long-term strategic advantage for Singapore-based wealth managers as global wealth management increasingly converges with financial technology innovation.

Future Outlook

Singapore’s wealth management market is expected to sustain strong expansion as regional wealth accumulation, family office inflows, and cross-border portfolio diversification continue to favor Singapore’s regulated financial ecosystem. Technological integration, alternative investment democratization, and institutional advisory models will deepen client engagement and expand addressable segments. Regulatory credibility and global capital connectivity will reinforce Singapore’s leadership among Asian wealth hubs. Demand from emerging affluent populations and international investors will support sustained growth.

Major Players

Key Target Audience

- Private banks

- Asset management firms

- Family offices

- Sovereign wealth funds

- High-net-worth investor groups

- Investment and venture capitalist firms

- Government and regulatory bodies

- Insurance wealth platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables include assets under management flows, client segmentation, platform distribution models, and regulatory factors shaping wealth allocation structures across Singapore’s financial ecosystem. Primary mapping covers institutional, private banking, and family office channels influencing market size.

Step 2: Market Analysis and Construction

Market structure is constructed using financial disclosures, regulatory statistics, and institutional asset data to estimate product and platform segmentation within Singapore’s wealth management industry. Competitive positioning and distribution dynamics are modeled across investor segments.

Step 3: Hypothesis Validation and Expert Consultation

Findings are validated through consultation with private banking executives, asset managers, and regulatory specialists to confirm market drivers, structural trends, and competitive dynamics shaping Singapore’s wealth management sector.

Step 4: Research Synthesis and Final Output

Validated insights are synthesized into structured market segmentation, competitive analysis, and strategic outlook to produce a comprehensive assessment of Singapore’s wealth management market evolution and growth trajectory.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Ultra-High-Net-Worth Population and Family Office Inflows

Institutionalization of Cross-Border Portfolio Diversification

Rising Allocation to Alternative Investments

Regional Wealth Migration into Singapore

Professionalization of Intergenerational Wealth Planning - Market Challenges

Rising Regulatory Compliance Complexity

Intensifying Regional Wealth Hub Competition

Fee Compression from Digital Platforms

Talent Retention in Private Banking

Cross-Border Tax Transparency Pressures - Market Opportunities

Democratization of Alternative Investments

Integration of Advanced Wealth Technology

Expansion into Mass Affluent Segment - Trends

Growth of Single and Multi-Family Offices

Hybrid Digital-Human Advisory Models

Increasing Private Market Allocations

ESG and Sustainable Wealth Portfolios

Cross-Border Custody Consolidation - Government Regulations & Defense Policy

Accredited Investor and Fund Distribution Frameworks

Tax Incentives for Family Office Establishment

Anti-Money Laundering and Transparency Regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory Portfolio Management

Alternative Investment Solutions

Structured Wealth Products

Trust and Estate Planning Services - By Platform Type (In Value%)

Private Banking Platforms

Independent Asset Management Firms

Digital Wealth Management Platforms

Family Office Platforms

Brokerage and Custody Platforms - By Fitment Type (In Value%)

Onshore Booked Wealth Structures

Offshore Booking Structures

Hybrid Cross-Border Structures

Custody-Only Arrangements

Discretionary Mandate Structures - By End User Segment (In Value%)

Ultra-High-Net-Worth Individuals

High-Net-Worth Individuals

Family Offices

Institutional Investors

Affluent Mass Investors

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Assets Under Management Scale, Client Segment Focus, Geographic Reach, Alternative Investment Access, Advisory Model, Digital Platform Capability, Custody Infrastructure, Family Office Services, Regulatory Licensing)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

UBS Global Wealth Management

DBS Private Bank

Bank of Singapore

UOB Private Bank

OCBC Private Bank

HSBC Global Private Banking

Citi Private Bank

Julius Baer

Pictet Wealth Management

Lombard Odier

Morgan Stanley Private Wealth Management

Goldman Sachs Private Wealth Management

BNP Paribas Wealth Management

Standard Chartered Private Bank

Credit Suisse Wealth Management

- Ultra-high-net-worth clients prioritize global diversification and capital preservation

- Family offices demand institutional-grade reporting and governance structures

- High-net-worth investors increasingly adopt discretionary mandates

- Affluent segment adoption driven by digital wealth platforms

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Singapore Wealth Management market administers approximately USD ~ trillion in assets under management within its financial system. The market scale reflects private banking, institutional mandates, and regional offshore wealth inflows booked in Singapore.

Singapore Wealth Management market dominance stems from strong regulatory credibility and global capital connectivity attracting cross-border wealth.

The country hosts over 1,100 asset managers and a rapidly growing number of family offices managing regional portfolios.

Singapore Wealth Management market is led by discretionary portfolio management with about 34% share. Dominance reflects demand for professional global asset allocation and institutional investment access among high-net-worth clients.

Singapore Wealth Management market distribution is led by private banks holding roughly 46% share.

Global custody infrastructure and integrated lending-investment services support their leadership among affluent investors.

Singapore Wealth Management market includes UBS, DBS Private Bank, HSBC, Julius Baer, and Bank of Singapore among major institutions. These firms manage large regional assets and provide cross-border portfolio and advisory services from Singapore.

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now