Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Africa’s third-party logistics sector represents a significant component of the national transport and supply chain industry, with the broader logistics sector generating approximately USD ~ Billion in economic activity based on recent assessments published by the South African Department of Transport and Statistics South Africa. Growth is driven by expanding retail distribution networks, mining exports, manufacturing supply chains, and increasing demand for outsourced warehousing and freight management services. Logistics providers play a critical role in managing transportation networks, cargo consolidation, warehousing operations, and distribution services across complex national and regional supply chains.

Johannesburg and Gauteng province dominate logistics activity because the region functions as the primary industrial and commercial hub supporting national distribution networks. Durban also holds strategic importance due to the Port of Durban, one of Africa’s largest container ports facilitating international trade flows and freight forwarding operations. Cape Town supports logistics demand through port operations and consumer distribution networks. These cities benefit from established transportation corridors, advanced warehousing infrastructure, and proximity to major manufacturing, mining, and retail markets.

Market Segmentation

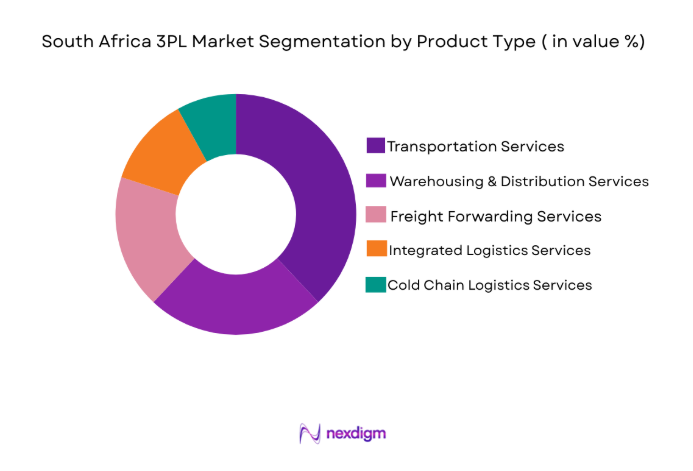

By Product Type

South Africa 3PL market is segmented by product type into transportation services, warehousing and distribution services, freight forwarding services, cold chain logistics services, and integrated logistics solutions. Recently, transportation services has a dominant market share due to factors such as extensive road freight dependency, growing retail distribution networks, and strong demand from mining and manufacturing industries that rely heavily on road transportation for domestic cargo movement across long distances.

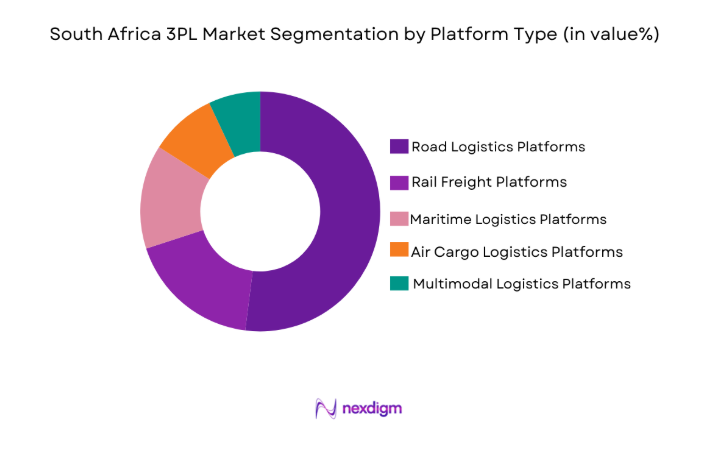

By Platform Type

South Africa 3PL market is segmented by platform type into road logistics platforms, rail freight platforms, air cargo logistics platforms, maritime logistics platforms, and multimodal logistics platforms. Recently, road logistics platforms has a dominant market share due to South Africa’s extensive highway network connecting industrial regions with ports and urban markets, combined with the flexibility road transport provides for nationwide distribution and last mile freight delivery operations.

Competitive Landscape

The South Africa 3PL market shows moderate consolidation with several global logistics corporations operating alongside regional supply chain providers. Large multinational logistics companies dominate integrated freight forwarding, contract logistics, and warehousing operations, while domestic operators maintain strong positions in road transportation and distribution services. Strategic partnerships with manufacturing, retail, and mining companies significantly influence market competition.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Size |

| Imperial Logistics | 1946 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| Bidvest Panalpina Logistics | 1985 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Bonn | ~ | ~ | ~ | ~ | ~ |

| DSV | 1976 | Hedehusene | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Schindellegi | ~ | ~ | ~ | ~ | ~ |

South Africa 3PL Market Analysis

Growth Drivers

Expansion of Retail and E Commerce Distribution Networks

Rapid growth of digital retail platforms and modern supermarket chains across South Africa significantly increases demand for professional logistics providers capable of managing large distribution networks connecting manufacturers, warehouses, and retail outlets. Online retail transactions continue expanding across major urban markets, creating rising shipment volumes that require advanced warehousing facilities and efficient transportation networks. Third party logistics providers support this demand by offering integrated services including inventory storage, order fulfillment, packaging, and last mile distribution. Retail companies increasingly outsource logistics operations to improve operational efficiency and reduce infrastructure investments associated with maintaining their own transportation fleets and warehouses. Urban consumers also demand faster delivery timelines, encouraging logistics firms to establish regional fulfillment hubs located near major population centers. These facilities allow faster order processing and delivery to cities such as Johannesburg, Cape Town, and Durban where retail demand remains highly concentrated. Logistics companies invest in warehouse automation technologies, digital inventory management systems, and route optimization software to handle rising shipment volumes efficiently. As digital commerce continues expanding nationwide, outsourcing logistics services becomes essential for retailers seeking scalable supply chain solutions capable of supporting rapid distribution across national markets.

Growth of Regional Trade Corridors and Export Logistics Networks:

South Africa functions as a strategic logistics gateway connecting Southern African Development Community markets with international shipping routes, significantly strengthening demand for third party logistics services that manage cross border freight transportation and trade logistics. The country’s mining, automotive manufacturing, agriculture, and chemical industries generate substantial export volumes that require coordinated logistics operations linking production centers with ports and international freight networks. Logistics companies therefore provide services such as cargo consolidation, customs clearance, freight forwarding coordination, and multimodal transportation management to ensure efficient movement of goods across borders. Major ports including Durban, Cape Town, and Ngqura handle significant container traffic supporting exports to global markets. Road freight corridors connecting South Africa with neighboring countries including Botswana, Namibia, Zimbabwe, and Mozambique further increase demand for integrated logistics services capable of managing cross border cargo movement. Logistics providers also deploy digital shipment tracking systems that enable exporters to monitor cargo flows across multiple transport modes. Continued growth in regional trade flows across Southern Africa therefore strengthens the role of third party logistics companies supporting industrial export supply chains.

Market Challenges

Infrastructure Constraints Across National Transport Networks:

South Africa’s logistics industry faces significant operational challenges due to infrastructure bottlenecks across rail freight systems, highways, and port operations that limit cargo movement efficiency and increase logistics costs for supply chain operators. Congestion at major ports creates cargo handling delays that disrupt export schedules for industries such as mining and agriculture. Rail freight capacity limitations also force companies to rely heavily on road transportation, which increases transportation expenses and vehicle congestion across key freight corridors. Logistics providers therefore encounter operational inefficiencies that reduce overall supply chain productivity. Aging infrastructure across certain transportation routes further increases maintenance requirements and reduces freight reliability. Government agencies continue investing in transportation modernization programs, but infrastructure upgrades require long development timelines before significant improvements become visible. Logistics companies often compensate by expanding private transportation fleets and warehousing networks to maintain service reliability. Despite these efforts, infrastructure limitations remain one of the most persistent operational challenges affecting logistics efficiency across national distribution and export supply chains.

Rising Fuel Costs and Logistics Operating Expenses:

Transportation operations across South Africa remain heavily dependent on road freight services, making logistics companies highly sensitive to fuel price fluctuations that significantly affect operating costs and freight pricing structures across the supply chain industry. Diesel fuel costs represent a large proportion of transportation expenditure for logistics providers managing long distance cargo movement across national distribution networks. Rising energy costs therefore increase freight charges for manufacturers, retailers, and exporters that depend on logistics companies for cargo transportation. Logistics operators attempt to reduce fuel consumption through route optimization software and fleet efficiency improvements, yet fuel price volatility remains difficult to control. Maintenance costs for heavy transport vehicles also increase operating expenses as logistics companies maintain large vehicle fleets. These cost pressures may reduce profit margins for logistics providers while simultaneously increasing transportation costs for businesses relying on third party logistics services. Managing operational efficiency therefore remains a constant challenge for logistics firms operating in a highly cost sensitive transportation environment.

Opportunities

Expansion of Cold Chain Logistics for Pharmaceutical and Food Distribution:

Demand for temperature controlled logistics services continues expanding across South Africa as pharmaceutical distributors, food producers, and healthcare suppliers require reliable cold chain infrastructure capable of preserving product quality throughout transportation and storage processes. Pharmaceutical companies depend on temperature controlled logistics systems to transport vaccines, medicines, and biological products that require strict temperature conditions to remain effective. Similarly, food producers transporting dairy products, frozen foods, and perishable agricultural goods require specialized cold chain distribution networks connecting farms, processing facilities, warehouses, and retail outlets. Logistics companies increasingly invest in refrigerated trucks, temperature monitored storage facilities, and digital tracking systems capable of monitoring product conditions throughout transportation. Advanced cold storage warehouses located near major distribution hubs further strengthen cold chain infrastructure supporting nationwide distribution networks. As healthcare supply chains expand and food distribution networks become more sophisticated, demand for professional cold chain logistics services continues growing significantly across national logistics markets.

Adoption of Digital Logistics Platforms and Supply Chain Automation:

Rapid adoption of digital supply chain technologies presents significant opportunities for logistics companies seeking to improve operational efficiency, shipment visibility, and service reliability across national distribution networks. Logistics providers increasingly deploy advanced transportation management systems that optimize cargo routing, track vehicle fleets, and coordinate multimodal freight operations. Warehouse automation technologies including robotic storage systems and automated sorting equipment also enhance inventory handling efficiency within distribution centers. Digital shipment tracking platforms provide real time cargo visibility for customers, allowing manufacturers and retailers to monitor inventory movement across transportation networks. These digital systems reduce administrative complexity and improve operational coordination across multiple supply chain partners. Logistics companies adopting advanced data analytics tools can also predict shipment demand patterns and optimize logistics capacity planning. As digital technologies continue transforming supply chain operations worldwide, logistics providers implementing technology driven logistics solutions are positioned to capture significant operational and commercial advantages within competitive logistics markets.

Future Outlook

The South Africa 3PL market is expected to experience steady development as supply chains modernize and digital logistics technologies improve operational efficiency. Increasing e commerce activity, expanding regional trade networks, and infrastructure modernization projects will continue strengthening logistics demand. Investments in warehouse automation, cold chain distribution, and multimodal freight networks will enhance logistics capabilities. Government support for trade corridor development and port modernization is also expected to improve freight connectivity and supply chain integration across the region.

Major Players

- Imperial Logistics

- Bidvest Panalpina Logistics

- DHL Supply Chain

- DSV

- Kuehne + Nagel

- DB Schenker

- CEVA Logistics

- Unitrans Supply Chain Solutions

- Value Logistics

- Bolloré Logistics

- Onelogix Logistics

- Aramex South Africa

- Cargo Compass Logistics

- Transnet Freight Rail

- Hellmann Worldwide Logistics

Key Target Audience

- Logistics and transportation companies

- Retail and e-commerce companies

- Manufacturing and industrial enterprises

- Supply chain technology providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Freight forwarding companies

Research Methodology

Step 1: Identification of Key Variables

This stage focuses on identifying the major industry variables that influence the South Africa 3PL market. These include freight demand patterns, trade volumes, warehousing capacity, transportation infrastructure, and logistics outsourcing trends across retail, manufacturing, and export industries.

Step 2: Market Analysis and Construction

Industry data is analyzed using logistics industry reports, government transportation statistics, and company financial disclosures. Market structures are constructed by evaluating logistics service demand across transportation, warehousing, and freight forwarding segments.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market findings are validated through consultations with logistics industry professionals, supply chain managers, and transportation infrastructure specialists who provide insights into operational realities and emerging logistics trends.

Step 4: Research Synthesis and Final Output

All validated findings are consolidated into a structured market analysis. Quantitative data, industry insights, and competitive assessments are integrated to produce a comprehensive research report describing the South Africa 3PL market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of e commerce and digital retail distribution networks

Rising demand for outsourced logistics among manufacturing industries

Growth of regional trade corridors connecting Southern African markets - Market Challenges

Infrastructure bottlenecks across road and rail transportation networks

High fuel costs and logistics operating expenses

Port congestion and cargo handling inefficiencies - Market Opportunities

Development of integrated multimodal logistics corridors

Increasing demand for cold chain logistics across food and pharmaceutical sectors

Adoption of digital freight management platforms - Trends

Growing investment in warehouse automation and digital logistics platforms

Expansion of regional distribution hubs supporting African trade networks - Government Regulations

Transport and logistics regulations governing freight operations, customs procedures, and cross border cargo movement across Southern African Development Community trade routes - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Transportation Management Services

Warehousing and Distribution Services

Freight Forwarding Services

Integrated Logistics Solutions

Cold Chain Logistics Services - By Platform Type (In Value%)

Road Transportation Networks

Rail Freight Logistics Systems

Air Cargo Logistics Platforms

Maritime and Port Logistics Platforms

Multimodal Logistics Platforms - By Fitment Type (In Value%)

Dedicated Contract Logistics

Shared Warehousing Services

Asset Based Logistics Operations

Non Asset Based Logistics Services - By End User Segment (In Value%)

Retail and E Commerce Companies

Manufacturing and Industrial Firms

FMCG and Consumer Goods Companies

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio Breadth, Warehousing Capacity, Transportation Fleet Size, Technology Integration Level, Geographic Distribution Network, Cold Chain Capability, Multimodal Logistics Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Imperial Logistics

Bidvest Panalpina Logistics

DHL Supply Chain South Africa

DSV South Africa

Unitrans Supply Chain Solutions

Value Logistics

Transnet Freight Rail Logistics

Bolloré Logistics South Africa

Kuehne + Nagel South Africa

DB Schenker South Africa

CEVA Logistics South Africa

Aramex South Africa

UTi South Africa

Cargo Compass Logistics

Onelogix Logistics

- Retail companies increasingly outsource warehousing and last mile distribution services to improve supply chain efficiency

- Manufacturing firms depend on contract logistics providers to manage inbound raw material transportation and finished goods distribution

- FMCG producers rely on advanced distribution networks capable of handling high frequency inventory replenishment

- Pharmaceutical distributors require temperature controlled logistics infrastructure to support nationwide medicine supply chains

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now