Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The South Africa Agricultural Equipment market reached approximately USD ~ billion based on a recent historical assessment derived from agricultural machinery sales statistics, import-export data, and mechanization investment reports published by the Department of Agriculture, Land Reform and Rural Development and industry associations such as the South African Agricultural Machinery Association. Demand is driven by commercial farming modernization, replacement of aging machinery fleets, and expansion of mechanized operations in grain, horticulture, and livestock sectors.

Major activity centers are concentrated in Gauteng, Free State, Western Cape, and KwaZulu-Natal due to commercial agriculture intensity, large farm sizes, and established dealer networks. Cities such as Johannesburg, Bloemfontein, Cape Town, and Pietermaritzburg function as distribution and service hubs hosting equipment importers, assembly facilities, and parts logistics centers. These regions benefit from advanced agribusiness infrastructure, export-oriented farming, and strong financing availability supporting agricultural equipment adoption.

Market Segmentation

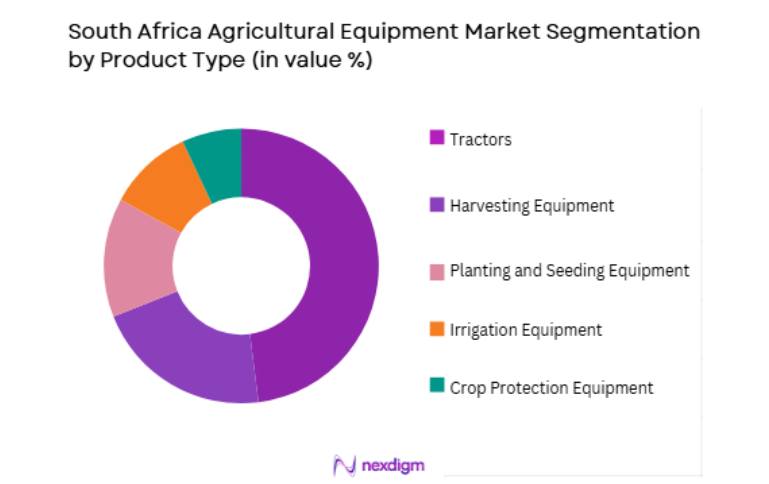

By Product Type

South Africa Agricultural Equipment market is segmented by product type into tractors, harvesting equipment, planting and seeding equipment, irrigation equipment, and crop protection equipment. Recently, tractors has a dominant market share due to factors such as essential role across all farming operations, high capital value per unit, and widespread use in large-scale commercial agriculture. Tractors support tillage, planting, hauling, and mechanized livestock operations across grain and horticulture farms, making them the core mechanization platform in South Africa’s extensive farming systems.

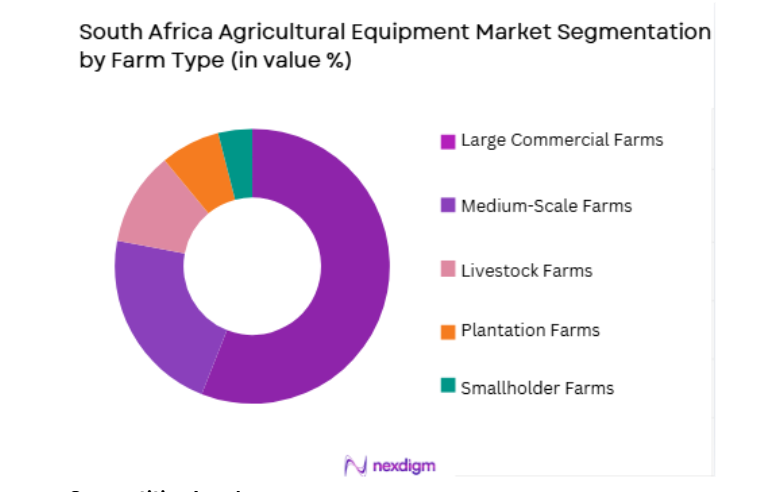

By Farm Type

South Africa Agricultural Equipment market is segmented by farm type into large commercial farms, medium-scale farms, smallholder farms, plantation farms, and livestock farms. Recently, large commercial farms has a dominant market share due to factors such as extensive landholdings, mechanization intensity, and financial capacity for high-value equipment investment. South Africa’s agricultural sector is characterized by relatively large mechanized farms producing grains, fruits, and livestock products for domestic and export markets, sustaining strong demand for tractors, harvesters, and precision agriculture machinery.

Competitive Landscape

The South Africa Agricultural Equipment market is moderately consolidated with strong presence of global OEMs operating through importer-dealer networks and localized assembly operations. Major multinational manufacturers dominate high-value tractor and harvester segments, supported by nationwide dealerships and financing programs. Local distributors and equipment importers complement OEM presence, particularly in specialized implements. Competitive positioning depends on dealer coverage, after-sales service capability, and financing partnerships with agricultural banks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Dealer Network Size |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK | ~ | ~ | ~ | ~ | ~ |

| AGCO | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| Kubota | 1890 | Japan | ~ | ~ | ~ | ~ | ~ |

| CLAAS | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

South Africa Agricultural Equipment Market Analysis

Growth Drivers

Commercial Agriculture Modernization and Mechanization Intensity

The South Africa Agricultural Equipment market is strongly driven by the modernization of commercial agriculture characterized by large mechanized farms adopting advanced machinery to enhance productivity and efficiency. South Africa’s agricultural structure includes extensive grain, fruit, and livestock operations requiring high-capacity tractors, harvesters, and precision implements to manage large land areas effectively. Mechanization enables timely planting and harvesting across climatic zones, supporting yield stability and export competitiveness. Commercial farmers invest in technologically advanced equipment to reduce labor dependence and optimize operational scale. Adoption of precision agriculture technologies including GPS guidance and variable rate application further increases machinery demand. Replacement of aging fleets with higher-capacity and fuel-efficient equipment sustains recurring market growth. Export-oriented agriculture incentivizes modernization to meet quality and productivity standards. Financing availability through agricultural banks and OEM programs supports capital equipment acquisition. Expansion of mechanized horticulture and grain production reinforces demand for advanced agricultural machinery. Commercial agriculture modernization therefore acts as a primary structural driver of equipment market expansion in South Africa.

Government Support Programs and Agricultural Financing Access

The South Africa Agricultural Equipment market benefits from policy frameworks and financing mechanisms that facilitate farm mechanization investment and equipment acquisition across commercial and emerging farming sectors. Government agricultural development programs support mechanization access for black commercial farmers and emerging producers through grants and subsidized equipment schemes. Land reform initiatives and farm consolidation efforts increase demand for tractors and implements among newly established commercial operators. Agricultural financing institutions provide equipment loans aligned with seasonal farm income cycles, improving affordability of capital machinery. OEM financing partnerships offer structured payment solutions encouraging adoption of modern equipment. Mechanization support programs aim to improve national agricultural productivity and rural economic growth. Public investment in irrigation and infrastructure expands mechanized farming potential in multiple regions. Access to finance reduces capital barriers and stimulates equipment purchases among medium-scale farms transitioning toward commercial production. Policy emphasis on agricultural competitiveness and food security encourages machinery modernization. Financing and policy support therefore constitute a significant growth driver sustaining agricultural equipment demand in South Africa.

Market Challenges

High Equipment Cost and Currency Volatility Impacting Imports

The South Africa Agricultural Equipment market faces challenges from high equipment costs driven by reliance on imported machinery and exposure to currency exchange fluctuations. Most tractors, harvesters, and advanced implements are sourced from international manufacturers, making prices sensitive to exchange rate movements and import duties. Depreciation of the local currency increases acquisition cost for farmers, reducing affordability and delaying equipment replacement cycles. Imported machinery also carries higher logistics and distribution expenses that raise retail prices. Financing requirements increase as equipment cost rises, limiting accessibility for medium-scale farmers. Currency volatility creates uncertainty in pricing and procurement planning for dealers and farmers. OEMs and distributors must adjust pricing frequently to reflect exchange rate changes, affecting demand stability. High capital cost also elevates risk perception among lenders, tightening credit availability during economic downturns. These import-linked cost pressures constrain market expansion and adoption of advanced agricultural machinery.

Climate Variability and Agricultural Income Uncertainty

The South Africa Agricultural Equipment market is significantly affected by climate variability including drought cycles, rainfall unpredictability, and extreme weather events that influence agricultural productivity and farmer income. Drought conditions reduce crop output and farm revenue, leading to postponement of machinery investment and replacement. Rainfall variability affects planting schedules and equipment utilization patterns, reducing predictability of mechanization demand. Agricultural income volatility increases financial risk for farmers considering capital equipment purchases. Regions heavily dependent on rain-fed agriculture experience fluctuating equipment demand aligned with climatic conditions. Insurance and risk mitigation mechanisms remain limited in some farming segments, amplifying income uncertainty. Dealers and manufacturers face cyclical sales patterns linked to seasonal climate impacts. Climate stress also affects livestock operations, reducing investment capacity in mechanized feeding and handling equipment. Long-term climate uncertainty therefore acts as a structural constraint on consistent agricultural equipment market growth in South Africa.

Opportunities

Expansion of Precision Agriculture and Smart Farming Technologies

The South Africa Agricultural Equipment market presents significant opportunity through adoption of precision agriculture technologies that enhance productivity and resource efficiency across large commercial farms. GPS-guided tractors, variable rate application systems, and data-driven crop management tools enable optimized input usage and yield improvement. Commercial farmers increasingly invest in smart machinery integrated with sensors and digital farm management platforms. Precision technologies reduce fuel consumption, fertilizer waste, and operational cost, improving return on equipment investment. Export-oriented agriculture encourages adoption of advanced technologies to maintain global competitiveness. OEMs offer integrated precision solutions embedded in tractors and harvesters, creating higher-value equipment segments. Expansion of data analytics and remote monitoring supports predictive maintenance and fleet optimization. Government and industry initiatives promoting digital agriculture adoption reinforce market potential. As large-scale farms prioritize efficiency and sustainability, precision agriculture integration becomes a major growth opportunity in the South Africa Agricultural Equipment market.

Mechanization Growth in Emerging and Medium-Scale Farming Segments

The South Africa Agricultural Equipment market can expand through increasing mechanization adoption among emerging black commercial farmers and medium-scale agricultural enterprises transitioning toward commercial production. Land reform and agricultural development policies aim to expand participation in commercial agriculture, creating new demand for tractors and implements. Medium-scale farms require mechanization to improve productivity and scale operations competitively. Equipment leasing, cooperative ownership, and mechanization service models enable access to machinery without full capital investment. Development finance institutions support equipment acquisition for emerging farmers, expanding mechanization reach beyond established commercial farms. Mechanization improves labor efficiency and production reliability for growing agricultural enterprises. Expansion of irrigation and diversified cropping encourages adoption of specialized equipment. OEMs and dealers are targeting this segment with mid-range machinery suited to evolving farm sizes. Mechanization growth in emerging farming sectors therefore represents a major structural opportunity for agricultural equipment market expansion in South Africa.

Future Outlook

The South Africa Agricultural Equipment market is expected to expand steadily driven by commercial farm modernization, precision agriculture adoption, and mechanization growth in emerging farming segments. Technological integration in tractors and harvesters will enhance productivity and efficiency. Financing access and agricultural development programs will support equipment acquisition. Expansion of irrigated and export-oriented agriculture will sustain machinery demand. Replacement of aging fleets will maintain baseline market growth.

Major Players

- John Deere

- CNH Industrial

- AGCO

- Kubota

- CLAAS

- SAME Deutz-Fahr

- Mahindra Tractors

- Massey Ferguson South Africa

- New Holland Agriculture

- Case IH

- Fendt

- Valtra

- Landini

- McCormick Tractors

- JCB Agriculture

Key Target Audience

- Agricultural equipment manufacturers

- Farm equipment importers and distributors

- Commercial farming enterprises

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural cooperatives

- Agricultural financing institutions

- Precision agriculture technology providers

Research Methodology

Step 1: Identification of Key Variables

Key variables including farm size distribution, mechanization intensity, equipment import volumes, and financing penetration were identified through agricultural statistics and industry datasets. Product category demand drivers and regional farming structures were mapped to define market scope.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using equipment sales data, import statistics, and farm mechanization indicators across regions and farm types. Product type shares and farm segment demand were derived from industry and policy sources.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding mechanization trends, financing influence, and regional demand patterns were validated through consultation with equipment dealers, agricultural economists, and commercial farm operators. Findings were cross-checked against sector studies.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into structured analysis covering market size, segmentation, competitive landscape, and growth dynamics. Consistency checks ensured alignment with agricultural production and mechanization trends in South Africa.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of commercial farming and export-oriented agriculture

Mechanization demand driven by labor cost and availability constraints

Government support for agricultural modernization and productivity - Market Challenges

High equipment acquisition cost and financing limitations

Climate variability and drought affecting farm investment

Dependence on imported agricultural machinery and components - Market Opportunities

Adoption of precision agriculture and smart farming technologies

Growth in mechanization services and equipment rental markets

Localization of equipment assembly and distribution networks - Trends

Shift toward high horsepower tractors for large farms

Increasing use of precision spraying and planting systems

Digital fleet management and telematics adoption - Government regulations

Agricultural mechanization and land reform support programs

Import duties and equipment certification standards

Environmental and emission compliance requirements - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Tractors

Combine Harvesters

Sprayers

Planting and Seeding Equipment

Tillage Equipment - By Platform Type (In Value%)

Wheeled Equipment

Tracked Equipment

Mounted Implements

Trailed Implements

Self-Propelled Equipment - By Fitment Type (In Value%)

Open Station Equipment

Cab Enclosed Equipment

Precision Farming Equipped Systems

Heavy-Duty Commercial Equipment

Specialty Crop Equipment - By End User Segment (In Value%)

Large Commercial Farms

Medium Scale Farms

Smallholder Farms

- Market Share Analysis

- Cross Comparison Parameters (Equipment Type Portfolio, Horsepower Range, Precision Technology Integration, Price Positioning, Dealer Network Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

John Deere South Africa

CNH Industrial South Africa

AGCO South Africa

Kubota South Africa

Claas South Africa

Case IH South Africa

New Holland Agriculture South Africa

Massey Ferguson South Africa

Deutz-Fahr South Africa

Lemken South Africa

Kuhn South Africa

Horsch South Africa

Bell Equipment

Stara South Africa

Jacto South Africa

- Large commercial farms driving demand for high-capacity equipment

- Medium farms upgrading mechanization for productivity gains

- Smallholders adopting shared or rental equipment models

- Contract farming enterprises expanding equipment fleets

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now