Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Africa AI Infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by accelerated enterprise digitalization, hyperscale data center investments, and expanding cloud-AI workloads across banking, telecom, and public services. Strong capital inflows into data center construction and GPU-accelerated computing platforms are enabling large-scale AI training and inference deployments. Government digital economy initiatives and enterprise automation spending are reinforcing sustained demand for high-performance compute, storage, and networking infrastructure nationwide.

Johannesburg and Cape Town dominate AI infrastructure deployment due to concentration of hyperscale data centers, subsea cable landing stations, and enterprise headquarters clusters that support large-scale compute demand. These cities host major colocation campuses, financial institutions, and technology hubs requiring AI processing capacity for analytics, fintech, and digital services. Durban is emerging as a secondary node supported by port logistics digitization and telecom expansion, while regional connectivity corridors linking Southern Africa strengthen cross-border data processing relevance.

Market Segmentation

By Product Type

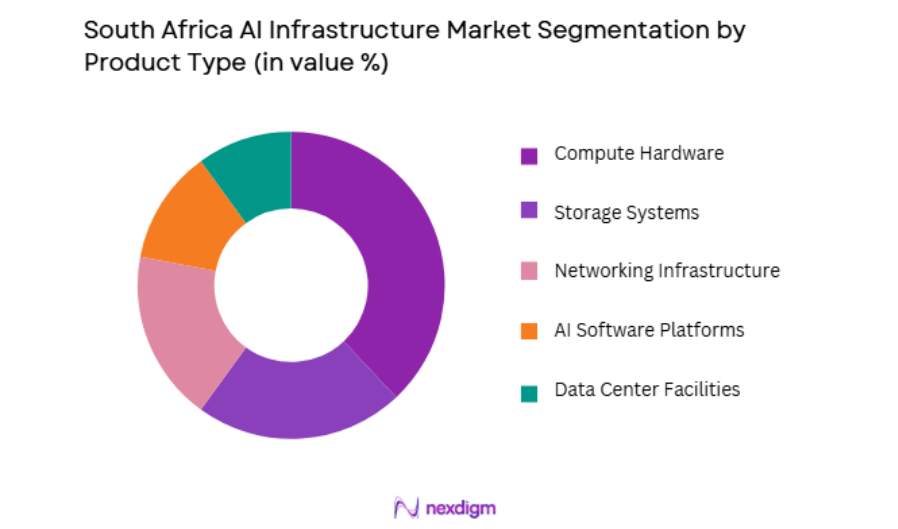

South Africa AI Infrastructure market is segmented by product type into Compute Hardware, Storage Systems, Networking Infrastructure, AI Software Platforms, and Data Center Facilities. Recently, Compute Hardware has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. The rapid scaling of AI training clusters, GPU servers, and accelerated computing nodes for enterprise analytics and machine learning workloads has driven disproportionate investment toward compute hardware. Financial services, telecom operators, and hyperscale cloud providers prioritize high-performance processors and AI accelerators to support real-time decision systems and predictive analytics. Strong vendor ecosystems, supply agreements with global semiconductor firms, and rising enterprise adoption of generative AI applications have reinforced compute spending.

By End-Use Industry

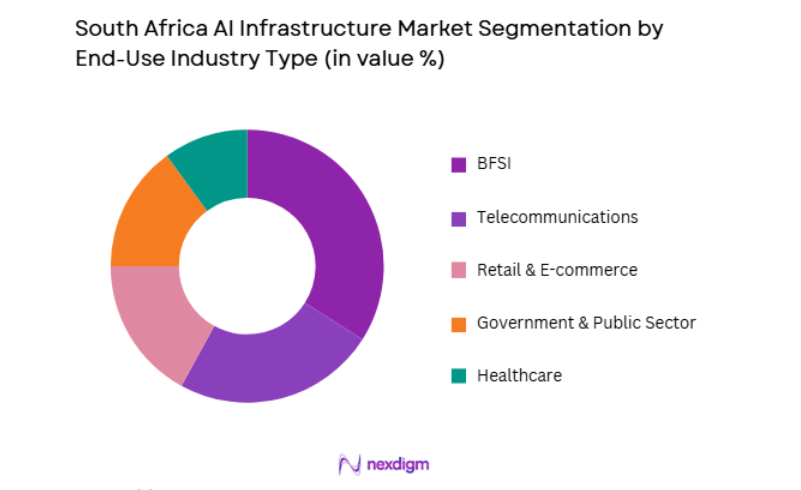

South Africa AI Infrastructure market is segmented by end-use industry into BFSI, Telecommunications, Retail & E-commerce, Healthcare, and Government & Public Sector. Recently, BFSI has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. South Africa’s financial institutions are among the most technologically mature in Africa, deploying AI for fraud detection, risk modeling, customer analytics, and automated trading systems that require substantial compute and storage infrastructure. Regulatory compliance, digital banking expansion, and mobile payment ecosystems generate massive transactional datasets demanding real-time processing. Large banking groups and insurers maintain private data centers and hybrid cloud AI clusters, sustaining continuous infrastructure upgrades.

Competitive Landscape

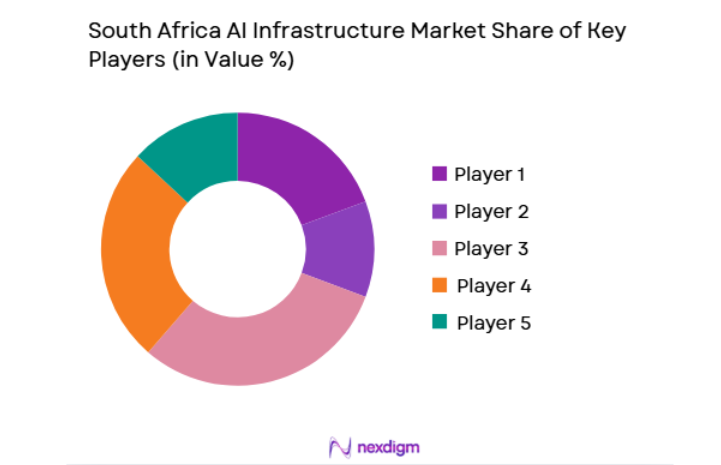

South Africa AI Infrastructure market shows moderate consolidation with global hyperscale technology providers and specialized data center operators controlling high-capacity deployments, while regional system integrators support enterprise adoption. Market leaders influence technology standards through GPU supply agreements, cloud platform ecosystems, and large-scale data center investments. Strategic partnerships with telecom operators and energy providers enable scalable AI infrastructure rollouts, creating entry barriers for smaller vendors lacking capital and semiconductor access.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Data Center Capacity (MW) |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| 1998 | USA | ~ | ~ | ~ | ~ | ~ | |

| Teraco | 2008 | South Africa | ~ | ~ | ~ | ~ | ~ |

| Huawei | 1987 | China | ~ | ~ | ~ | ~ | ~ |

South Africa AI Infrastructure Market Analysis

Growth Drivers

Expansion of Hyperscale and Colocation Data Center Investments

This is accelerating South Africa AI Infrastructure market growth by providing the physical foundation required for large-scale AI compute deployment across industries. Global cloud providers and regional operators are investing heavily in multi-megawatt campuses near subsea cable landing points and urban enterprise clusters to support AI workloads. These facilities enable enterprises to access scalable GPU clusters, high-density storage, and ultra-low-latency networking essential for machine learning training and inference. The presence of neutral interconnection hubs reduces bandwidth costs and improves data exchange speeds between enterprises, cloud platforms, and telecom networks. Renewable energy procurement agreements are allowing operators to power AI infrastructure sustainably while meeting growing compute intensity demands.

Enterprise Adoption of AI-Driven Automation and Analytics Platforms

It is significantly expanding demand for AI infrastructure across South Africa’s financial services, telecom, retail, and public sectors. Organizations are deploying machine learning models for fraud detection, predictive maintenance, supply chain optimization, and customer personalization, which require high-performance computing resources. The rise of generative AI applications in customer service, document processing, and marketing analytics is increasing inference workloads across enterprise data centers and cloud environments. Hybrid cloud strategies combining on-premise GPU clusters with public cloud AI services are driving continuous infrastructure upgrades. Large enterprises are investing in dedicated AI training environments to maintain data sovereignty and regulatory compliance while scaling model development. Telecommunications providers are implementing AI-enabled network optimization and traffic forecasting systems that demand real-time data processing capacity.

Market Challenges

Energy Supply Constraints and High Electricity Costs for AI Data Centers

Energy supply constraints and high electricity costs for AI data centers are a major structural challenge limiting the scalability of South Africa AI Infrastructure market expansion. AI workloads require dense GPU clusters and cooling systems that consume significantly more power than traditional IT infrastructure, intensifying grid demand. Intermittent electricity supply and load-shedding risks force data center operators to invest in backup generation and energy storage systems, increasing operational expenditure. Rising electricity tariffs directly affect colocation pricing, making AI compute services more expensive for enterprises. The need to secure renewable power purchase agreements adds complexity and capital requirements to infrastructure projects. Smaller enterprises may delay AI adoption due to high infrastructure costs linked to energy pricing. International hyperscale providers must carefully assess long-term energy availability before expanding capacity in the country.

Limited Domestic Semiconductor Ecosystem and Dependence on Imported AI Hardware

Limited domestic semiconductor ecosystem and dependence on imported AI hardware present a significant supply chain vulnerability for South Africa AI Infrastructure market growth. The country lacks local fabrication facilities and relies heavily on imported GPUs, AI accelerators, and high-performance processors from global manufacturers. Global semiconductor shortages or export restrictions can delay AI infrastructure deployment and increase equipment costs. Currency volatility amplifies hardware import expenses, raising capital expenditure for data center operators and enterprises. Lead times for advanced AI servers and networking equipment remain long, constraining rapid scaling of compute clusters. Dependence on foreign vendors also reduces domestic innovation and customization capability in AI hardware design. Maintenance and replacement cycles become costlier due to imported component dependency. Local system integrators face challenges competing with global providers possessing direct hardware supply agreements. These factors collectively create structural constraints on infrastructure availability and long-term technological sovereignty.

Opportunities

Regional AI Processing Hub Development for Sub-Saharan Digital Economies

Regional AI processing hub development for Sub-Saharan digital economies represents a major opportunity for South Africa AI Infrastructure market expansion due to the country’s advanced connectivity and data center ecosystem. South Africa hosts multiple subsea cable landing stations linking Africa to Europe and Asia, enabling low-latency data exchange across the continent. Enterprises in neighboring countries increasingly rely on South African facilities for cloud hosting and AI processing due to limited domestic infrastructure. Financial services, telecom, and e-commerce firms across Southern Africa require centralized AI analytics platforms accessible regionally. International cloud providers are positioning South Africa as a gateway node for African AI workloads. Regional demand aggregation improves utilization rates of large-scale GPU clusters and data center capacity. Government initiatives promoting digital trade and cross-border data flows support regional infrastructure integration. Expansion of regional fiber networks further strengthens interconnection with neighboring economies. These factors collectively position South Africa to become the primary AI compute hub for Sub-Saharan Africa.

Adoption of Green AI Infrastructure and Renewable-Powered Data Centers

Adoption of green AI infrastructure and renewable-powered data centers offers substantial growth potential in South Africa AI Infrastructure market as sustainability requirements intensify globally. AI data centers consume large amounts of electricity, creating strong incentives for operators to integrate solar, wind, and energy storage solutions. South Africa’s renewable energy resources enable cost-competitive clean power procurement for data center campuses. Enterprises and hyperscale providers increasingly prioritize low-carbon infrastructure to meet environmental commitments. Green infrastructure reduces long-term operating costs and improves investment attractiveness. Government renewable energy procurement programs support private sector power generation for data centers. Sustainable cooling technologies and energy-efficient hardware designs further enhance infrastructure efficiency. International investors favor environmentally responsible digital infrastructure assets, increasing capital inflows. These dynamics create a strategic pathway for South Africa to expand AI infrastructure while aligning with global sustainability trends.

Future Outlook

South Africa AI Infrastructure market is expected to expand steadily over the next five years as hyperscale data center capacity, enterprise AI adoption, and regional digital demand continue rising. Advancements in GPU computing, edge AI nodes, and high-speed interconnection will enhance processing capability. Renewable energy integration and regulatory digital economy initiatives will support infrastructure expansion. Increasing cross-border data processing demand will further position South Africa as Africa’s primary AI infrastructure hub.

Major Players

- Amazon Web Services

- Microsoft

- Teraco

- Huawei

- IBM

- Oracle

- Dell Technologies

- Nvidia

- Cisco

- Equinix

- Africa Data Centres

- Vodacom

- MTN

- HPE

Key Target Audience

- Cloud service providers

- Data center operators

- Telecommunications companies

- BFSI institutions

- Retail and e-commerce firms

- Investments and venture capitalist firms

- Government and regulatory bodies

- AI software developers

Research Methodology

Step 1: Identification of Key Variables

Key variables such as AI compute capacity, data center investments, enterprise AI spending, and industry adoption intensity were identified through secondary research across public financial reports, infrastructure databases, and technology adoption studies. Market boundaries were defined around hardware, data center, and networking infrastructure components supporting AI workloads.

Step 2: Market Analysis and Construction

Market size was constructed by aggregating infrastructure spending across product categories including servers, storage, networking, and AI-ready data center capacity deployed in South Africa. Industry-wise allocation models and vendor revenue mapping were applied to derive segment distribution and competitive positioning.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultations with data center operators, cloud architects, telecom infrastructure specialists, and enterprise IT leaders to confirm deployment patterns and spending intensity. Expert feedback refined assumptions on infrastructure utilization and regional demand flows.

Step 4: Research Synthesis and Final Output

Validated data was synthesized into market models, segmentation tables, and competitive assessments to produce the final report. Consistency checks ensured alignment between infrastructure capacity, enterprise demand, and vendor presence across all sections.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of hyperscale and colocation data center capacity in South Africa

Rising enterprise adoption of AI and machine learning workloads

Government digital transformation and AI readiness initiatives - Market Challenges

Power supply constraints and energy costs affecting data center operations

Limited domestic semiconductor and advanced hardware supply chain

Skills shortages in AI infrastructure deployment and management - Market Opportunities

Growth of sovereign and localized cloud AI infrastructure demand

Edge AI deployment across mining, energy, and logistics sectors

Publicprivate partnerships for national AI compute infrastructure - Trends

Adoption of GPUdense AI clusters in hyperscale facilities

Integration of edge AI with 5G and IoT infrastructure - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Compute Servers

GPU Accelerated Systems

AI Storage Infrastructure

AI Networking Infrastructure

Edge AI Infrastructure - By Platform Type (In Value%)

Cloud AI Infrastructure

OnPremise Data Center AI Infrastructure

Hybrid AI Infrastructure

Edge AI Platforms

HighPerformance Computing AI Clusters - By Fitment Type (In Value%)

Greenfield AI Data Centers

Brownfield AI Upgrades

Modular AI Infrastructure

Integrated AI Appliances - By End User Segment (In Value%)

Telecommunications Providers

Financial Services Institutions

Government and Public Sector

- Market Share Analysis

- Cross Comparison Parameters (Compute Performance, Energy Efficiency, Scalability, Deployment Model, Industry Focus, AI Accelerator Integration, Data Center Tier Compatibility, Edge Readiness, Total Cost of Ownership, Vendor Support & Services)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Dell Technologies

Hewlett Packard Enterprise

Cisco Systems

Huawei Technologies

IBM Corporation

Microsoft

Amazon Web Services

Google Cloud

Oracle Corporation

NVIDIA Corporation

Intel Corporation

NEC XON

NTT Ltd

Liquid Intelligent Technologies

Dark Fibre Africa

- Telecom operators investing in AI-ready network and edge infrastructure

- Banks deploying AI compute for fraud detection and analytics

- Government building national AI and data platforms

- Healthcare providers adopting AI imaging and diagnostics infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now