Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Africa AI Servers and GPU Hardware market is valued at approximately USD ~ billion based on a recent historical assessment, supported by infrastructure spending on hyperscale data centers, AI training clusters, and enterprise GPU deployments. Expansion of colocation facilities, sovereign cloud programs, and public sector digital transformation initiatives are increasing demand for high-performance AI servers and accelerator hardware across financial services, telecom, and research institutions.

Johannesburg and Cape Town dominate the South Africa AI Servers and GPU Hardware market due to concentration of hyperscale data centers, fiber connectivity hubs, and enterprise IT headquarters. Johannesburg benefits from financial sector compute demand and carrier-neutral colocation clusters, while Cape Town hosts cloud availability zones and research computing centers. Pretoria contributes through government HPC procurement and national research network infrastructure, reinforcing regional hardware deployment density.

Market Segmentation

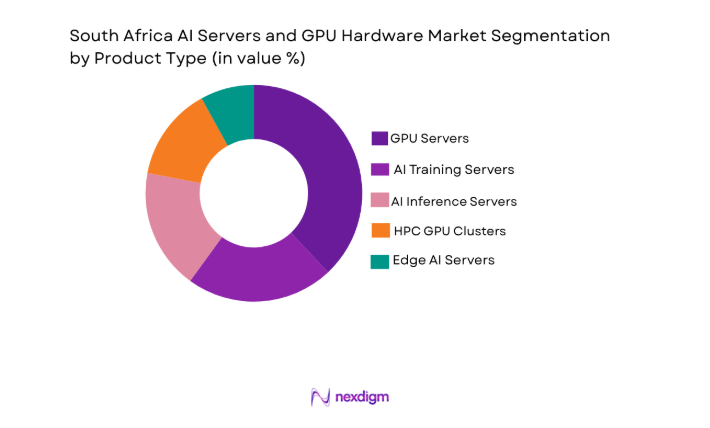

By Product Type

South Africa AI Servers and GPU Hardware market is segmented by product type into GPU servers, AI training servers, AI inference servers, HPC GPU clusters, and edge AI servers. Recently, GPU servers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Enterprise AI workloads in banking, telecom analytics, and cloud platforms prioritize standardized GPU server architectures that integrate accelerator cards with scalable rack systems. Global vendor availability through distributors in Johannesburg and Cape Town improves procurement cycles and support services, strengthening adoption. Data center operators prefer modular GPU servers compatible with existing power and cooling configurations, lowering deployment complexity. Growth of AI model training services and sovereign cloud offerings further increases bulk procurement of GPU-dense servers by hyperscale and colocation providers across the country.

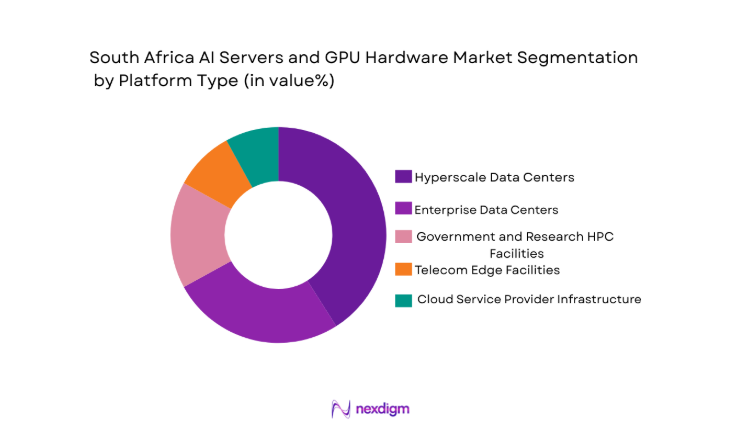

By Platform Type

South Africa AI Servers and GPU Hardware market is segmented by platform type into hyperscale data centers, enterprise data centers, government and research HPC facilities, telecom edge facilities, and cloud service provider infrastructure. Recently, hyperscale data centers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. International cloud providers and large colocation operators are expanding hyperscale campuses in Johannesburg and Cape Town, driving concentrated procurement of AI servers and GPU accelerators. Hyperscale platforms require dense GPU compute for AI training, analytics services, and cloud AI offerings delivered to regional customers. Power and cooling investments in hyperscale campuses enable deployment of high-TDP accelerators compared to enterprise sites. Long-term capacity planning by hyperscale operators leads to multi-rack GPU cluster deployments, surpassing other platform categories in hardware volume.

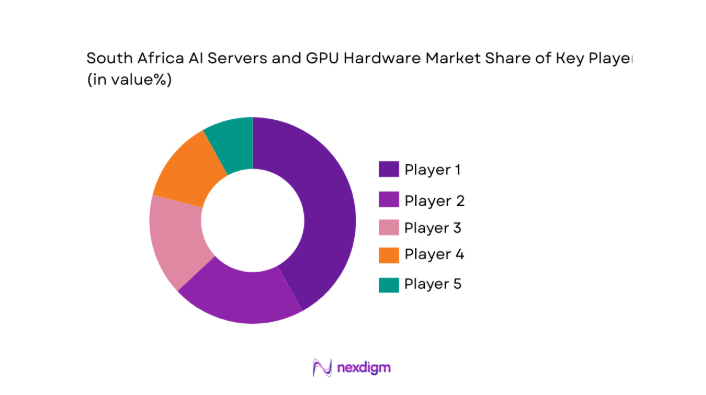

Competitive Landscape

The South Africa AI Servers and GPU Hardware market shows moderate consolidation, with global server OEMs and GPU manufacturers controlling technology supply while regional integrators and distributors influence deployment and procurement. Partnerships between hyperscale operators and international hardware vendors shape market concentration, and enterprise buyers rely on established OEM ecosystems for AI-ready server platforms and accelerator compatibility.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AI Accelerator Integration Capability |

| NVIDIA Corporation | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 2015 | USA | ~ | ~ | ~ | ~ | ~ |

| Lenovo | 1984 | China | ~ | ~ | ~ | ~ | ~ |

| Supermicro | 1993 | USA | ~ | ~ | ~ | ~ |

South Africa AI Servers and GPU Hardware Market Analysis

Growth Drivers

Expansion of Hyperscale and Colocation Data Center Capacity

The South Africa AI Servers and GPU Hardware market is strongly driven by sustained investment in hyperscale and colocation data center infrastructure across Johannesburg and Cape Town, where international cloud providers and regional operators are scaling facilities to support AI and high-performance computing workloads. Hyperscale campuses require dense GPU clusters for AI model training, data analytics, and cloud AI services, resulting in bulk procurement of accelerator-rich servers. Colocation providers are expanding power and cooling capabilities to support high-density AI racks, enabling enterprises to deploy GPU servers without building dedicated facilities. Financial services, telecom, and retail analytics applications are increasing compute intensity, accelerating enterprise migration toward AI-optimized hardware hosted in colocation environments. Government digital transformation programs and sovereign cloud initiatives are also procuring AI servers for national data platforms and secure analytics environments. The presence of subsea cable landings and regional fiber networks improves connectivity, encouraging multinational cloud operators to expand AI compute infrastructure locally rather than abroad. Hardware vendors are establishing regional supply chains and integration partnerships, improving availability of GPU-accelerated systems and shortening deployment cycles. This ecosystem expansion creates recurring demand for AI servers, storage, and networking components aligned with hyperscale capacity growth across South Africa.

Adoption of AI Workloads Across Enterprise and Public Sector Domains

The South Africa AI Servers and GPU Hardware market is expanding due to rapid adoption of artificial intelligence workloads across banking, telecom, healthcare, mining, and government sectors that require on-premise or sovereign compute infrastructure. Financial institutions are deploying GPU servers for fraud detection, risk modeling, and customer analytics, while telecom operators use AI inference and training clusters for network optimization and predictive maintenance. Public sector agencies and research institutions are investing in high-performance GPU systems for climate modeling, genomics, and language processing aligned with national innovation agendas. Enterprises increasingly prefer localized AI infrastructure to address data sovereignty requirements and latency-sensitive analytics applications. Growth of generative AI experimentation within corporate environments is further driving procurement of AI training servers and inference accelerators. System integrators and managed service providers are offering AI infrastructure as managed platforms, lowering adoption barriers for mid-sized organizations. Educational and research collaborations are expanding national HPC capabilities, increasing GPU cluster deployments in academic and scientific facilities. Collectively, widespread AI workload adoption across sectors is creating sustained and diversified demand for AI servers and GPU hardware in South Africa.

Market Challenges

Power and Cooling Constraints in High-Density AI Deployments

The South Africa AI Servers and GPU Hardware market faces structural challenges related to power availability, grid reliability, and cooling capacity required for high-density GPU clusters deployed in data centers. AI accelerators consume significantly higher power than conventional servers, necessitating advanced cooling solutions and stable electrical supply, which can be constrained in regional infrastructure environments. Load shedding and electricity supply variability increase operational risk for hyperscale and enterprise facilities attempting to host AI training workloads locally. Data center operators must invest heavily in backup power, liquid cooling, and energy management systems, increasing total cost of ownership for AI hardware deployments. Smaller enterprises and research facilities may struggle to support high-TDP GPU servers due to facility limitations. Expansion of hyperscale campuses is also affected by grid connection approvals and infrastructure upgrades, delaying AI hardware scaling plans. Environmental regulations and energy efficiency targets further complicate deployment of large GPU clusters requiring substantial electricity consumption. These constraints collectively limit rapid expansion of AI compute density and slow broader diffusion of GPU-accelerated infrastructure across the country.

High Capital Costs and Import Dependence for AI Hardware

The South Africa AI Servers and GPU Hardware market is constrained by high capital expenditure requirements and reliance on imported AI accelerators and server systems sourced from global vendors. Advanced GPUs and AI servers carry premium pricing due to specialized silicon, high-speed memory, and interconnect technologies, increasing procurement barriers for enterprises and public institutions. Currency volatility and import duties further elevate acquisition costs for hardware purchased from international suppliers. Limited domestic manufacturing or assembly capacity reduces local price competitiveness and supply resilience. Smaller enterprises and startups may defer AI infrastructure adoption due to budget limitations, relying instead on cloud services hosted abroad. Public sector procurement cycles for high-value AI hardware are lengthy and complex, slowing deployment in research and government environments. Vendor lock-in risks associated with proprietary accelerator ecosystems also raise long-term investment concerns for buyers. Dependence on imported components exposes the market to global semiconductor supply fluctuations, affecting availability and pricing stability. These economic and structural factors collectively moderate adoption pace of AI servers and GPU hardware in South Africa.

Opportunities

Development of Sovereign AI Cloud and National HPC Infrastructure

The South Africa AI Servers and GPU Hardware market has significant opportunity in development of sovereign AI cloud platforms and national high-performance computing infrastructure aligned with data sovereignty and digital economy objectives. Governments and strategic industries increasingly require local AI compute environments to process sensitive data within national jurisdiction, driving procurement of GPU clusters and AI servers in sovereign facilities. National research networks and supercomputing centers are expanding capabilities to support scientific computing, climate research, and language technologies relevant to regional priorities. Public-private partnerships for sovereign cloud initiatives are creating demand for domestically hosted AI training and inference platforms. Localization policies encourage deployment of national AI infrastructure rather than reliance on foreign cloud regions. Telecommunications operators and defense sectors also require secure AI compute nodes, expanding specialized hardware procurement. Regional leadership ambitions in African digital innovation position South Africa as a hub for AI infrastructure serving neighboring markets. Expansion of sovereign HPC and AI cloud ecosystems will stimulate sustained investment in GPU hardware, networking, and storage technologies across the country.

Edge AI Infrastructure for Telecom, Mining, and Industrial Automation

The South Africa AI Servers and GPU Hardware market can expand through deployment of edge AI infrastructure supporting telecom networks, mining operations, smart cities, and industrial automation across geographically distributed environments. Telecom operators require GPU-accelerated edge servers for real-time analytics, video processing, and 5G network optimization at distributed sites. Mining and energy sectors are adopting AI-enabled predictive maintenance, autonomous equipment control, and safety monitoring systems deployed near operational locations. Smart city programs in metropolitan regions require localized AI inference for surveillance analytics, traffic management, and public safety platforms. Industrial facilities are integrating AI vision and robotics systems that rely on ruggedized edge GPU servers for low-latency processing. Growth of edge AI workloads reduces dependence on centralized data centers and expands hardware deployment footprint nationwide. Vendors offering compact, energy-efficient GPU systems optimized for edge environments can capture emerging demand segments. Infrastructure rollout across remote and industrial regions creates new procurement channels beyond traditional data center markets, supporting diversification of AI hardware adoption in South Africa.

Future Outlook

South Africa AI Servers and GPU Hardware market is expected to expand steadily as hyperscale capacity, sovereign cloud programs, and enterprise AI adoption increase across industries. Advancements in accelerator efficiency and liquid cooling will enable higher density deployments. Regulatory emphasis on data sovereignty will favor localized AI infrastructure investments. Telecom and industrial edge AI deployments will broaden hardware demand beyond core data centers.

Major Players

- NVIDIA Corporation

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Supermicro

- Cisco Systems

- IBM

- Inspur

- Fujitsu

- Huawei

- Quanta Cloud Technology

- ASUS

- Gigabyte Technology

- Atos

- NEC Corporation

Key Target Audience

- Hyperscale data center operators

- Cloud service providers

- Telecom network operators

- Banking and financial institutions

- Government and regulatory bodies

- Investments and venture capitalist firms

- Mining and energy companies

- Large enterprise IT infrastructure buyers

Research Methodology

Step 1: Identification of Key Variables

Supply-side variables such as GPU shipments, server deployments, and data center capacity were mapped alongside demand-side indicators including AI workload adoption and sectoral IT spending. Macroeconomic and infrastructure indicators were incorporated to contextualize hardware demand patterns.

Step 2: Market Analysis and Construction

Bottom-up assessment of AI server and GPU deployments across hyperscale, enterprise, telecom, and government segments was conducted using vendor shipment data and data center capacity metrics. Revenue modeling aligned hardware volumes with regional pricing benchmarks.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with data center operators, system integrators, and enterprise IT architects to confirm deployment trends and procurement drivers. Cross-verification with infrastructure expansion announcements ensured accuracy of market sizing assumptions.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into market segmentation, competitive mapping, and growth analysis frameworks. Consistency checks ensured alignment across infrastructure, demand, and vendor ecosystem perspectives before finalization.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of AI Enabled Cloud Infrastructure in South Africa

Rising Demand for Localized AI Model Training Capacity

Government Digital Transformation and HPC Investments

Growth of Fintech and AI Driven Financial Analytics

Telecom Edge AI Deployment for 5G Services - Market Challenges

High Capital Cost of Advanced GPU Hardware Imports

Power and Cooling Constraints in Data Centers

Dependence on Foreign Semiconductor Supply Chains

Limited Local AI Hardware Integration Expertise

Rapid Obsolescence of GPU Architectures - Market Opportunities

Development of Sovereign AI Computing Infrastructure

Adoption of AI Servers in Public Sector Digital Programs

Regional AI Hosting and Colocation Services Expansion - Trends

Shift Toward Liquid Cooled High Density GPU Racks

Adoption of AI Inference Edge Servers in Telecom Networks

Growth of AI Supercomputing in Academic Institutions

Hybrid CPU GPU Architectures for Enterprise AI Workloads

Deployment of Energy Efficient AI Accelerators - Government Regulations & Defense Policy

National Data Sovereignty and Localization Policies

Public-Sector High-Performance Computing Initiatives

AI Research Funding and Digital Infrastructure Programs - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Training GPU Servers

AI Inference Edge Servers

High Performance Computing GPU Clusters

Hybrid CPU GPU Accelerated Servers

Dense Multi GPU Rack Systems - By Platform Type (In Value%)

Hyperscale Data Centers

Enterprise On Premise Data Centers

Cloud Service Provider Infrastructure

Telecom Edge Infrastructure

Research and Academic Supercomputing Facilities - By Fitment Type (In Value%)

Rack Mounted GPU Servers

Blade GPU Servers

Tower AI Workstations

Modular GPU Expansion Units

Integrated AI Appliance Systems - By End User Segment (In Value%)

Cloud and Colocation Providers

Financial Services Institutions

Telecommunications Operators

Government and Defense Agencies

Universities and Research Institutes - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrator Contracts

Cloud Marketplace Procurement

Government Tender Procurement

Value Added Reseller Channels - By Material / Technology (in Value %)

NVIDIA CUDA GPU Architecture Systems

AMD ROCm GPU Platforms

ARM Based AI Server Architectures

Liquid Cooled GPU Server Systems

PCIe Gen5 GPU Accelerated Platforms

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (GPU Performance Density, Energy Efficiency, Cooling Technology, AI Framework Compatibility, Scalability Architecture, Procurement Cost Structure, Local Support Capability, Deployment Flexibility, Supply Chain Reliability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

Advanced Micro Devices

Intel

Dell Technologies

Hewlett Packard Enterprise

Lenovo

Supermicro

Cisco Systems

Huawei

Inspur

Fujitsu

Atos

IBM

NEC

Gigabyte Technology

- Cloud providers expanding AI compute zones in domestic data centers

- Financial institutions deploying GPU clusters for risk and fraud analytics

- Telecom operators integrating edge AI servers into 5G infrastructure

- Universities investing in GPU supercomputing for AI research

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now