Download PDF

Download PDF Download PDF

Download PDFMarket Overview

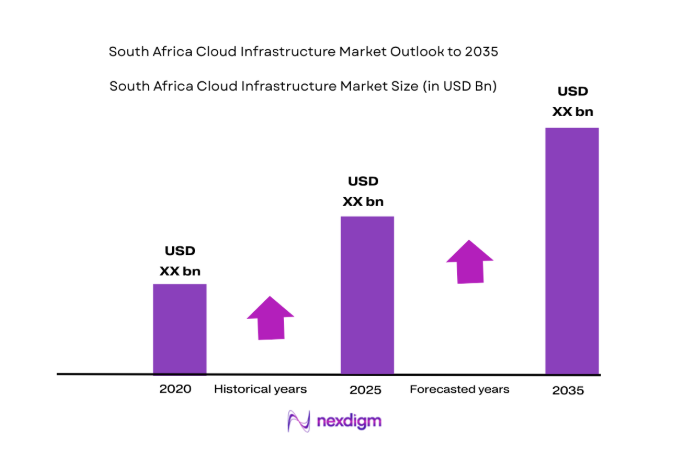

South Africa’s cloud infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by accelerated enterprise migration from legacy IT to scalable cloud environments and expanding hyperscale data center investments. Demand has been reinforced by financial services digitization, telecom network virtualization, and government digital service modernization. Large enterprises and regulated sectors increasingly adopt hybrid and sovereign cloud deployments to address compliance and latency requirements, strengthening infrastructure spending across compute, storage, and networking domains.

Johannesburg and Cape Town dominate South Africa’s cloud infrastructure landscape due to concentrated data center campuses, dense enterprise clusters, and submarine cable connectivity landing points. Johannesburg hosts major financial institutions and telecom headquarters that anchor cloud demand, while Cape Town benefits from international connectivity corridors and disaster recovery deployments. Pretoria contributes through government and public sector cloud programs. These metropolitan hubs attract hyperscale operators and colocation ecosystems, enabling low latency interconnection and regional cloud service distribution across Southern Africa.

Market Segmentation

By Product Type

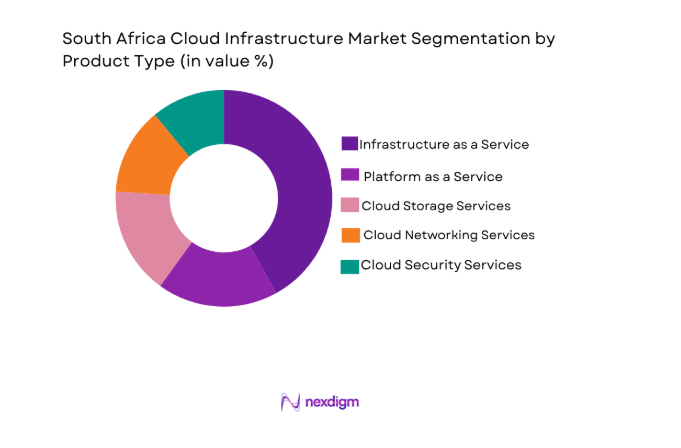

South Africa Cloud Infrastructure market is segmented by product type into Infrastructure as a Service, Platform as a Service, Cloud Storage Services, Cloud Networking Services, and Cloud Security Services. Recently, Infrastructure as a Service has a dominant market share due to factors such as enterprise migration from on premise data centers, strong hyperscaler presence, scalable compute demand from fintech and digital platforms, and availability of local data center capacity enabling compliance aligned deployments. Organizations prioritize flexible compute and storage provisioning over platform abstraction, reinforcing IaaS dominance across regulated and large scale workloads.

By Platform Type

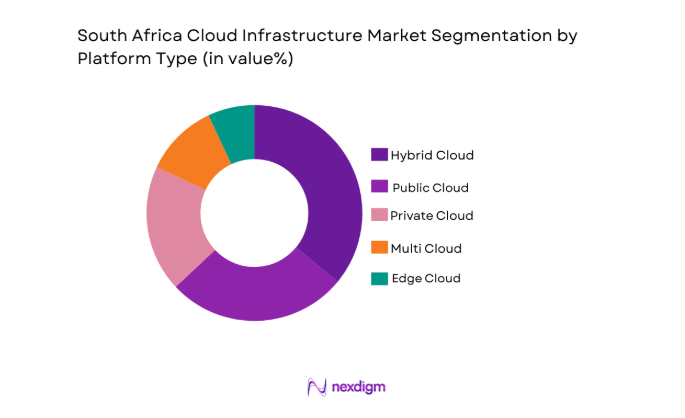

South Africa Cloud Infrastructure market is segmented by platform type into Public Cloud, Private Cloud, Hybrid Cloud, Multi Cloud, and Edge Cloud. Recently, Hybrid Cloud has a dominant market share due to factors such as regulatory data residency requirements, legacy system integration needs, and demand for workload portability across public and private environments. Enterprises maintain sensitive data on private infrastructure while leveraging public cloud scalability, creating sustained demand for hybrid orchestration platforms and interconnection services across finance, telecom, and government sectors.

Competitive Landscape

South Africa’s cloud infrastructure market shows moderate consolidation with global hyperscalers and regional telecom integrated providers dominating large enterprise and government contracts. International cloud vendors leverage local data center partnerships and compliance certifications, while domestic telecom and colocation firms provide connectivity integrated cloud offerings. Competitive positioning depends on data residency capability, interconnection density, and managed services breadth, leading to strategic alliances between hyperscalers, telecom operators, and data center providers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Data Center Footprint |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | USA | ~ | ~ | ~ | ~ | ~ |

| Huawei Cloud | 2017 | China | ~ | ~ | ~ | ~ | ~ |

| MTN Business | 2000 | South Africa | ~ | ~ | ~ | ~ | ~ |

South Africa Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise Digital Transformation and Cloud Migration Acceleration

South Africa’s enterprise sector is undergoing a structural shift from legacy on premise IT environments toward scalable and consumption based cloud infrastructure architectures that enable digital service delivery and operational agility across industries, and this transformation is being driven by competitive pressure to modernize banking platforms, retail commerce systems, and telecom service stacks while reducing capital intensive hardware ownership. Organizations are increasingly adopting cloud native development frameworks and microservices architectures that require elastic compute and container orchestration environments, which in turn stimulates demand for Infrastructure as a Service and platform integrated cloud stacks deployed within domestic data centers to ensure compliance with data residency regulations. Financial institutions, insurance firms, and telecommunications operators are prioritizing hybrid and sovereign cloud models to meet regulatory requirements while enabling digital customer engagement channels such as mobile banking, online marketplaces, and streaming platforms that depend on high availability cloud hosting environments. The expansion of enterprise software as a service ecosystems and data analytics workloads is further reinforcing the need for scalable storage and high performance computing clusters accessible through cloud infrastructure platforms integrated with enterprise identity and security frameworks. Migration programs are also motivated by the need to improve disaster recovery resilience and business continuity following regional power instability and infrastructure risks, leading enterprises to adopt geographically distributed cloud deployments across multiple metropolitan data center zones. Government modernization initiatives promoting digital public services and e governance platforms are compelling state entities to transition workloads from legacy government owned data centers into managed cloud infrastructure hosted within national jurisdiction boundaries. The emergence of artificial intelligence and data driven business models across sectors such as healthcare, logistics, and mining is generating new requirements for GPU accelerated cloud computing environments that enterprises prefer to access through on demand infrastructure provisioning rather than owning specialized hardware. Managed service providers and telecom operators are facilitating migration through packaged cloud transformation services that reduce technical complexity for enterprises lacking in house expertise, thereby accelerating adoption across midmarket organizations. As enterprises increasingly measure IT performance in terms of service agility, uptime, and cost transparency rather than asset ownership, cloud infrastructure migration becomes a core strategic imperative sustaining long term demand expansion across South Africa’s digital economy.

Hyperscale Data Center Expansion and Connectivity Ecosystem Development

South Africa is experiencing sustained investment in hyperscale and carrier neutral data center infrastructure concentrated in major metropolitan corridors, creating foundational capacity that enables cloud service providers to deploy localized regions and deliver low latency cloud services across Southern Africa while complying with national data sovereignty requirements. Global hyperscale operators and regional colocation firms are constructing large scale campuses interconnected with submarine cable landing stations and terrestrial fiber backbones, significantly increasing available compute and storage capacity accessible to enterprises and cloud platforms within domestic borders. The presence of multiple international subsea cables terminating in coastal hubs such as Cape Town enhances international bandwidth availability and reduces latency for cross border data flows, making the country a preferred regional cloud hosting location for multinational enterprises operating across the African continent. Data center ecosystems are also supported by telecom operator investment in metropolitan fiber networks and internet exchange points that facilitate high speed interconnection between enterprises, cloud providers, and content delivery networks, thereby strengthening the performance characteristics of cloud infrastructure services delivered from South African facilities. Hyperscale campus expansion generates economies of scale that reduce unit infrastructure costs and enable cloud providers to offer competitively priced compute and storage services compared to offshore hosting, encouraging enterprises to repatriate workloads into local cloud regions. Government policies promoting digital infrastructure development and incentives for data center investment are attracting international capital and technology partnerships that further accelerate cloud ecosystem maturation. Colocation providers are integrating direct cloud on ramps and cross connect services within facilities, allowing enterprises to securely connect private IT environments to public cloud platforms and implement hybrid architectures with minimal latency and high reliability. Renewable energy integration and energy efficient cooling technologies deployed in modern data centers are improving sustainability credentials and operational efficiency, addressing environmental and power reliability concerns that previously constrained infrastructure expansion. As hyperscale and interconnection capacity continues to scale, South Africa strengthens its position as the primary cloud infrastructure hub for Southern Africa, reinforcing sustained demand growth from domestic and regional enterprises.

Market Challenges

Power Reliability Constraints and Energy Cost Volatility

South Africa’s cloud infrastructure expansion faces structural challenges arising from persistent electricity supply instability and escalating energy costs, which directly affect data center operations that require continuous high density power availability and stable grid conditions to maintain uptime guarantees demanded by enterprise cloud customers. Frequent load shedding events and grid disruptions necessitate substantial investment in backup generation, battery storage, and energy management systems within data center facilities, increasing capital expenditure and operating costs that cloud providers must absorb or pass through to customers in service pricing. Energy intensive cooling systems and high performance computing clusters amplify electricity consumption, making operational efficiency and power sourcing a critical determinant of data center viability within the national context. Cloud infrastructure providers must therefore secure diversified power procurement strategies including renewable energy contracts, onsite solar generation, and independent power producer agreements to mitigate grid dependency, yet these solutions introduce additional regulatory approvals and infrastructure integration complexity. Elevated energy costs reduce the cost competitiveness of locally hosted cloud services compared to offshore regions with stable and lower priced electricity markets, potentially slowing enterprise workload repatriation and limiting hyperscale investment expansion. Power instability also creates operational risk exposure that can affect service level agreements and enterprise trust in domestic cloud hosting reliability, particularly for mission critical financial and telecommunications workloads that require near zero downtime performance standards. Infrastructure redundancy requirements to ensure resilience increase construction complexity and extend deployment timelines for new data center capacity, slowing the pace at which cloud supply can scale to meet rising demand. Telecom and fiber network infrastructure also depend on stable power supply, meaning energy disruptions can cascade into connectivity outages affecting cloud service delivery. Addressing this challenge requires coordinated national energy infrastructure improvement and regulatory support for data center power procurement diversification, without which long term cloud infrastructure growth may remain constrained despite strong demand fundamentals.

Data Sovereignty Compliance and Skills Shortage in Advanced Cloud Architecture

South Africa’s cloud infrastructure market encounters systemic constraints related to evolving data protection regulations and limited availability of advanced cloud engineering talent, both of which complicate enterprise adoption and provider deployment of sophisticated cloud architectures across regulated industries. Data sovereignty requirements under national privacy legislation compel organizations to ensure that sensitive personal and financial data remains within national jurisdiction boundaries and is processed in compliant infrastructure environments, necessitating local cloud regions, certified facilities, and complex governance frameworks that increase deployment costs and compliance burden for both providers and customers. Enterprises in banking, healthcare, and government sectors must implement stringent security, encryption, and access control architectures aligned with regulatory audits, creating technical complexity that slows migration from legacy systems and raises reliance on specialized expertise. However, the domestic workforce skilled in cloud native architecture design, cybersecurity engineering, and multi cloud orchestration remains limited relative to demand, creating talent shortages that inflate labor costs and delay project execution timelines across migration and deployment initiatives. Cloud providers must invest heavily in training programs and partner ecosystems to build local technical capability, yet skill development cycles are lengthy and cannot immediately satisfy the rapid growth in enterprise cloud adoption requirements. Limited expertise in advanced technologies such as container orchestration, serverless computing, and cloud security automation constrains the sophistication of solutions that domestic enterprises can implement, potentially reducing realized value from cloud investments and slowing innovation. Skills scarcity also affects public sector digital transformation projects that depend on local system integrators and managed service providers to implement secure government cloud environments. Compliance requirements combined with talent limitations increase total cost of ownership for cloud deployments and create risk perception among enterprises evaluating migration decisions. Overcoming this challenge requires sustained workforce development, certification programs, and collaboration between industry, academia, and government to expand cloud engineering capacity and ensure regulatory alignment does not impede technological advancement.

Opportunities

Expansion of Sovereign Cloud and Regulated Industry Cloud Platforms

South Africa presents substantial opportunity for the development of sovereign cloud and sector specific regulated cloud platforms tailored to industries such as finance, healthcare, and government that require strict data residency, security, and compliance assurance within national jurisdiction boundaries. Enterprises in regulated sectors increasingly demand cloud environments that combine the scalability and elasticity of public cloud with localized control, certified infrastructure, and governance frameworks aligned with national privacy legislation and sector regulations, creating demand for specialized sovereign cloud architectures hosted within domestic data centers. Cloud providers can differentiate through compliance certifications, secure identity frameworks, and isolated tenancy models that enable sensitive workload hosting without cross border data exposure risks. Financial institutions migrating core banking and payment processing systems require high assurance infrastructure with advanced encryption, auditability, and operational transparency, which sovereign cloud platforms can provide while maintaining digital service agility. Government agencies adopting digital citizen services and e governance platforms similarly require nationally controlled cloud environments to ensure public data sovereignty and national security compliance. Healthcare organizations digitizing patient records and telemedicine platforms must store and process medical data locally under privacy mandates, further expanding sovereign cloud demand. Telecom operators and defense related entities also prefer domestically governed infrastructure for mission critical communications and analytics workloads. Hyperscalers and regional providers that establish sovereign cloud offerings through partnerships with local data center operators and regulatory authorities can capture high value enterprise and public sector contracts. The ability to deliver compliant cloud platforms domestically also positions South Africa as a regional hosting hub for neighboring countries with similar regulatory requirements but limited infrastructure capacity. As regulatory scrutiny intensifies globally, sovereign cloud capability becomes a strategic differentiator and long term growth opportunity within the national cloud infrastructure market.

Edge Cloud Deployment for Low Latency Digital Services and Industry 4.0 Applications

The proliferation of latency sensitive digital services and industrial automation across South Africa is generating emerging demand for edge cloud infrastructure deployed closer to end users and operational environments, creating opportunity for cloud providers to extend computing capacity beyond centralized hyperscale data centers into distributed regional nodes integrated with telecom networks. Applications such as real time financial transactions, autonomous mining operations, smart manufacturing systems, video analytics, and connected healthcare monitoring require ultra low latency processing and localized data handling that centralized cloud regions cannot consistently provide due to network propagation delays. Telecom operators expanding 5G networks are positioned to integrate edge computing nodes within base station and metro aggregation facilities, enabling cloud platforms to deliver compute and analytics services at the network edge while maintaining connectivity to central cloud regions for orchestration and data aggregation. Industrial sectors including mining, energy, and logistics are adopting automation and sensor driven monitoring systems that generate large volumes of operational data requiring immediate analysis for safety and efficiency optimization, which edge cloud architectures can support. Retail and media enterprises deploying immersive digital experiences and streaming services also benefit from localized content caching and processing to improve user experience. Edge cloud deployments reduce bandwidth consumption and backhaul costs by processing data locally before transmission to central cloud platforms, improving economic viability for high volume IoT and video workloads. As digital transformation extends into operational technology environments beyond traditional IT domains, demand for distributed computing infrastructure integrated with connectivity networks is expected to expand. Providers that build hybrid edge to core cloud ecosystems combining central hyperscale capacity with regional edge nodes can capture new enterprise segments and industry verticals, positioning edge cloud as a significant long term growth vector within South Africa’s cloud infrastructure landscape.

Future Outlook

South Africa’s cloud infrastructure market is expected to expand steadily over the next five years supported by hyperscale data center capacity growth, enterprise digital transformation acceleration, and telecom driven edge computing expansion. Regulatory emphasis on data sovereignty will encourage localized cloud deployments and sovereign cloud offerings. Adoption of artificial intelligence workloads and hybrid architectures will increase infrastructure demand. Continued fiber connectivity investment and regional digital service growth will reinforce South Africa’s role as a Southern African cloud hub.

Major Players

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Oracle Cloud

- IBM Cloud

- Huawei Cloud

- Alibaba Cloud

- NTT Ltd

- BCX

- Vodacom Business

- MTN Business

- Liquid Intelligent Technologies

- TeracoData Environments

- Africa Data Centres

- Openserve

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Telecom operators

- Hyperscale cloud providers

- Data center developers

- Financial institutions

- Large enterprises

- IT infrastructure vendors

Research Methodology

Step 1: Identification of Key Variables

Demand drivers, infrastructure capacity indicators, regulatory constraints, and enterprise adoption patterns were identified across cloud service models, deployment architectures, and end user sectors. Data points included data center capacity, enterprise IT spending distribution, connectivity infrastructure, and sector digitization metrics influencing cloud infrastructure demand.

Step 2: Market Analysis and Construction

Market sizing and segmentation were constructed through bottom up assessment of cloud service revenues, infrastructure deployment capacity, and enterprise adoption across industries. Supply side analysis incorporated hyperscaler presence, telecom cloud offerings, and data center ecosystem expansion within South Africa’s metropolitan regions.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding adoption drivers, regulatory impact, and infrastructure constraints were validated through consultation with cloud architects, telecom infrastructure specialists, and enterprise IT decision makers. Cross verification ensured alignment with regulatory frameworks, technology trends, and regional infrastructure realities.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into structured market segmentation, competitive landscape, and forecast models reflecting South Africa’s cloud infrastructure ecosystem. Findings were consolidated into an analytical framework linking infrastructure supply, enterprise demand, and regulatory context to future market evolution.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising enterprise digital transformation and cloud migration programs

Expansion of hyperscale data center investments in major metros

Growth in fintech, e commerce, and digital services demand

Government digital services and e government initiatives

Telecom 5G and edge computing ecosystem development - Market Challenges

Power reliability constraints affecting data center uptime

Data sovereignty and localization compliance complexities

Skills shortage in cloud architecture and cybersecurity

High bandwidth costs in regional connectivity

Legacy IT lock in across public sector entities - Market Opportunities

Expansion of sovereign cloud and regulated industry clouds

Growth of edge cloud for low latency enterprise use cases

Hybrid and multi cloud management services demand - Trends

Rapid hyperscale campus expansion around Johannesburg region

Integration of AI and analytics services into cloud stacks

Shift toward consumption based IT procurement models

Increasing colocation to cloud interconnection ecosystems

Sustainability driven green data center architectures - Government Regulations & Defense Policy

Data protection and POPIA compliance requirements

National broadband and digital infrastructure strategies

Cross border data transfer and localization frameworks - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Infrastructure as a Service Platforms

Platform as a Service Environments

Cloud Storage and Backup Systems

Cloud Networking and Connectivity Systems

Cloud Security and Identity Systems - By Platform Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Multi Cloud Management Platforms

Edge Cloud Infrastructure - By Fitment Type (In Value%)

Greenfield Cloud Deployments

Legacy IT Modernization Integrations

Colocation Integrated Cloud

Telco Network Integrated Cloud

On Premise Cloud Stack Installations - By End User Segment (In Value%)

Large Enterprises

Small and Medium Enterprises

Government and Public Sector

Telecommunications and Media Firms

Financial Services Institutions - By Procurement Channel (In Value%)

Direct Hyperscaler Contracts

Managed Service Provider Channels

Telecom Operator Bundled Cloud

System Integrator Led Procurement

Marketplace Based Cloud Procurement - By Material / Technology (in Value %)

Virtualization and Containerization Technologies

Software Defined Networking Technologies

Hyperconverged Infrastructure Technologies

AI Accelerated Cloud Hardware

Energy Efficient Data Center Technologies

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Service Model Breadth, Deployment Flexibility, Data Center Footprint, Connectivity Integration, Compliance and Data Residency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft Azure

Google Cloud

Oracle Cloud

IBM Cloud

Huawei Cloud

Alibaba Cloud

NTT Ltd

BCX

Vodacom Business

MTN Business

Liquid Intelligent Technologies

Teraco Data Environments

Africa Data Centres

Openserve

- Financial institutions accelerating core banking cloud migration

- Public sector adopting sovereign and private cloud models

- Telecom operators embedding cloud in connectivity services

- SMEs leveraging public cloud for scalability and cost efficiency

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now