Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Africa cold chain logistics market is valued at approximately USD ~ billion based on a recent historical assessment, according to industry data published by the Department of Trade Industry and Competition and logistics sector reports. Market growth is strongly supported by expanding pharmaceutical distribution networks, rising demand for temperature controlled food storage, and increasing exports of perishable agricultural commodities. Cold chain infrastructure investments across refrigerated transportation, cold storage facilities, and monitoring technologies further strengthen logistics capabilities supporting national food security and pharmaceutical supply reliability.

Johannesburg, Cape Town, and Durban represent the most dominant logistics hubs supporting cold chain distribution across South Africa due to extensive port infrastructure, advanced warehousing networks, and well developed transportation corridors. Durban’s major seaport facilitates temperature controlled export shipments of citrus, seafood, and meat products. Cape Town supports fruit export logistics and refrigerated maritime trade routes. Johannesburg operates as the country’s largest inland logistics hub supported by distribution centers, pharmaceutical warehouses, and major retail supply chain networks.

Market Segmentation

By Product Type

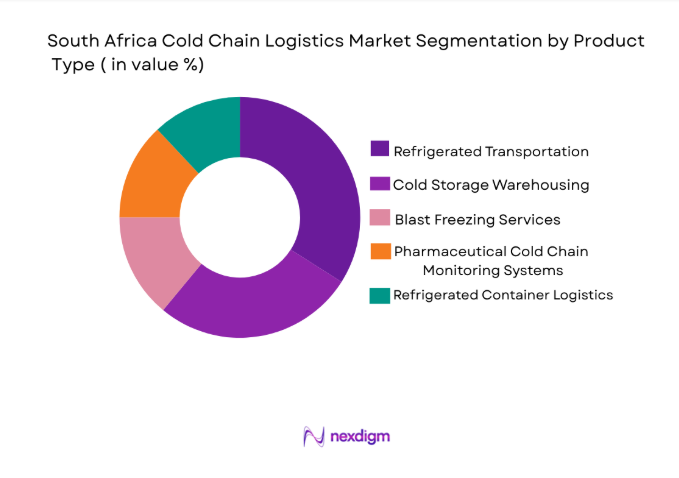

South Africa Cold Chain Logistics market is segmented by product type into refrigerated transportation, cold storage warehousing, blast freezing systems, pharmaceutical cold chain monitoring systems, and refrigerated container logistics. Recently, refrigerated transportation has a dominant market share due to extensive national food distribution requirements, strong supermarket supply chains, and the need to transport perishable agricultural products across long distances between production zones and urban consumption centers. Fresh produce exports such as citrus, grapes, and seafood also require continuous temperature controlled logistics from farms to seaports. Expanding pharmaceutical distribution networks further increase demand for refrigerated trucks and specialized temperature controlled transport solutions supporting vaccines and biologics distribution across regional healthcare facilities and distribution hubs.

By Platform Type

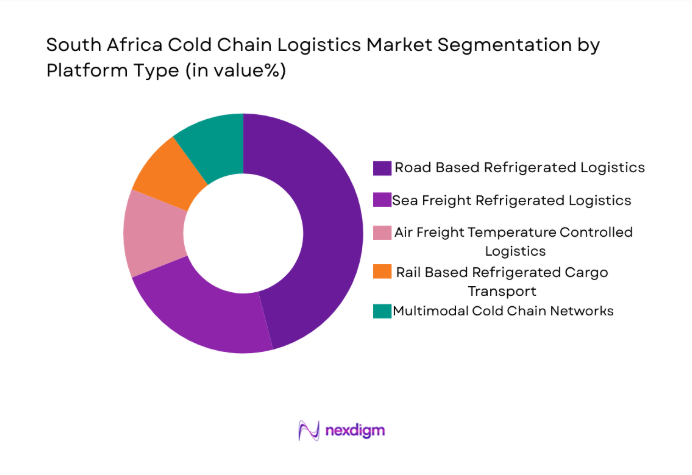

South Africa Cold Chain Logistics market is segmented by platform type into road based refrigerated logistics, sea freight refrigerated logistics, air freight temperature controlled logistics, rail based refrigerated cargo transport, and multimodal cold chain networks. Recently, road based refrigerated logistics has a dominant market share due to the country’s strong reliance on truck transportation for domestic distribution of food, pharmaceuticals, and agricultural products. Large distances between agricultural regions and metropolitan retail markets make refrigerated trucking essential for maintaining product quality. Logistics operators maintain large fleets of temperature controlled trucks supporting supermarket distribution, pharmaceutical supply chains, and cross provincial food transportation across the national highway network.

Competitive Landscape

South Africa cold chain logistics market remains moderately consolidated with several global logistics providers operating alongside established regional supply chain companies. Large international logistics operators provide advanced cold storage infrastructure, refrigerated transport fleets, and pharmaceutical distribution capabilities. Domestic logistics companies maintain strong distribution networks serving food processing companies, agricultural exporters, and national retail chains. Strategic partnerships between global logistics firms and local operators further strengthen cold chain capabilities supporting perishable exports and healthcare distribution networks across the country.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cold Storage Capacity |

| Imperial Logistics | 1946 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| Bidvest Panalpina Logistics | 1988 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Bonn | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Lineage Logistics | 2012 | Michigan | ~ | ~ | ~ | ~ | ~ |

South Africa Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Pharmaceutical Distribution and Vaccine Logistics Infrastructure

South Africa’s healthcare distribution system increasingly depends on advanced temperature controlled logistics capable of transporting vaccines, biologics, and specialty pharmaceuticals across hospitals, clinics, and medical distribution centers. National immunization programs and expanding pharmaceutical manufacturing activity significantly increase demand for specialized refrigerated transport systems and validated cold storage facilities. Pharmaceutical products such as insulin, vaccines, and biologic medicines require strict temperature control during transportation and storage to maintain efficacy and regulatory compliance. Healthcare logistics providers therefore invest heavily in refrigerated warehouses, temperature monitoring sensors, and validated pharmaceutical handling infrastructure. Pharmaceutical distribution networks increasingly extend beyond metropolitan areas to support rural healthcare facilities and regional hospitals. Logistics operators expand refrigerated transportation fleets equipped with real time temperature tracking technologies ensuring regulatory compliance and product safety throughout distribution. Partnerships between pharmaceutical companies, healthcare providers, and logistics firms strengthen cold chain infrastructure supporting large scale medicine distribution networks. Growth of biotechnology medicines and specialty pharmaceutical products further increases demand for precision temperature controlled logistics solutions across pharmaceutical supply chains nationwide.

Expansion of Perishable Food Export Supply Chains and Agricultural Trade

South Africa remains one of the largest exporters of fresh fruit and agricultural products including citrus, grapes, avocados, and seafood which require advanced cold chain logistics to maintain quality during long distance transportation. Export oriented agricultural production significantly increases demand for refrigerated storage facilities located near farming regions and major export ports. Cold chain logistics operators coordinate temperature controlled transportation from farms to packing facilities and subsequently to maritime export terminals ensuring product freshness. Fresh fruit exports transported through major ports such as Durban and Cape Town rely heavily on refrigerated containers and temperature controlled logistics systems. Logistics companies therefore expand cold storage capacity near export terminals enabling efficient consolidation of agricultural shipments before international transportation. Retail food supply chains within domestic markets also require temperature controlled logistics to transport meat, dairy products, frozen foods, and fresh produce across national distribution networks. Increasing demand for high quality perishable foods among urban consumers further strengthens the need for reliable refrigerated logistics infrastructure across food supply chains nationwide.

Market Challenges

High Energy Consumption and Rising Electricity Costs for Refrigerated Infrastructure

Cold chain logistics operations require continuous refrigeration systems to maintain precise temperature conditions within warehouses, transport vehicles, and distribution facilities. Refrigerated storage facilities consume large amounts of electricity for compressors, cooling equipment, and automated monitoring systems required to maintain stable temperature ranges. Rising electricity tariffs and periodic power supply disruptions increase operational costs for cold storage providers and logistics operators. Energy intensive refrigeration infrastructure therefore represents a major cost component within temperature controlled logistics operations. Companies increasingly invest in backup power systems, energy efficient refrigeration technologies, and solar power integration to reduce operational risks associated with power interruptions. Cold chain operators also upgrade insulation systems and adopt energy efficient cooling technologies to minimize electricity consumption across storage facilities. However the capital investment required for advanced refrigeration equipment remains significant for logistics providers. High operating costs therefore create financial pressure on logistics companies and can increase transportation and storage costs across food and pharmaceutical supply chains nationwide.

Limited Cold Chain Infrastructure in Rural Agricultural Production Regions

Agricultural production regions across South Africa often lack sufficient refrigerated storage facilities and temperature controlled transportation infrastructure necessary for maintaining product quality after harvest. Farmers located in remote regions frequently face logistical challenges transporting perishable produce to centralized cold storage hubs located near major urban markets. Delays in refrigerated transportation and limited access to cold storage infrastructure can reduce product shelf life and increase post harvest losses. Agricultural exporters therefore depend heavily on efficient logistics coordination between farms packing facilities and export terminals. Cold chain infrastructure development within rural regions remains uneven due to high capital investment requirements and limited access to financing for logistics expansion projects. Government infrastructure programs and private logistics investments attempt to address these infrastructure gaps but progress remains gradual. Strengthening rural cold chain networks remains critical for improving agricultural export efficiency and reducing food waste across national supply chains.

Opportunities

Development of Pharmaceutical Grade Cold Chain Infrastructure for Biologics and Vaccines

Pharmaceutical supply chains increasingly require specialized temperature controlled logistics capable of maintaining highly precise storage conditions for biologic medicines vaccines and advanced therapeutics. Expansion of pharmaceutical manufacturing and biotechnology research across Africa significantly increases demand for validated pharmaceutical cold chain logistics infrastructure. Logistics companies therefore invest in specialized pharmaceutical warehouses equipped with validated temperature monitoring systems regulatory compliance infrastructure and controlled environment storage facilities. Pharmaceutical distribution networks require end to end temperature monitoring across transportation storage and last mile delivery operations. Cold chain providers implementing digital temperature tracking systems real time monitoring sensors and automated alert systems strengthen pharmaceutical distribution reliability. Healthcare providers and pharmaceutical manufacturers increasingly collaborate with logistics companies to ensure regulatory compliance within medicine supply chains. Expansion of pharmaceutical cold chain infrastructure therefore creates significant opportunities for logistics operators specializing in healthcare distribution and medical logistics services.

Expansion of Export Oriented Cold Chain Corridors for Agricultural Commodities

South Africa’s agricultural sector produces large volumes of export oriented fruit seafood and meat products requiring advanced refrigerated logistics networks linking farms processing centers and international shipping ports. Logistics operators therefore develop integrated cold chain corridors connecting agricultural production zones with major maritime export terminals. Development of cold storage clusters near farming regions enables producers to maintain product freshness before international transportation. Export oriented cold chain logistics also supports international trade relationships with European Asian and Middle Eastern markets demanding high quality agricultural products. Logistics companies invest in advanced refrigerated container handling facilities port storage infrastructure and temperature monitoring technologies supporting global agricultural supply chains. Expansion of integrated cold chain corridors therefore strengthens export competitiveness and supports long term growth of temperature controlled logistics infrastructure nationwide.

Future Outlook

South Africa cold chain logistics market is expected to experience strong expansion driven by increasing demand for pharmaceutical distribution, growth in agricultural exports, and modernization of food supply chains. Technological developments in temperature monitoring, automation, and refrigerated fleet management will strengthen logistics efficiency. Government initiatives supporting agricultural trade infrastructure and healthcare distribution will further expand cold chain capabilities. Increasing private sector investments in advanced cold storage facilities and refrigerated transport networks will continue supporting long term logistics sector development.

Major Players

- Imperial Logistics

- Bidvest Panalpina Logistics

- DHL Supply Chain

- Kuehne + Nagel

- Lineage Logistics

- Americold Logistics

- Unitrans Supply Chain Solutions

- Value Logistics

- Cold Chain Africa

- Barloworld Logistics

- Vector Logistics

- DP World Logistics

- RCL Foods Logistics

- Clover Logistics

- Kühne + Nagel South Africa

Key Target Audience

- Cold chain logistics operators

- Pharmaceutical manufacturers

- Food processing companies

- Agricultural export companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Retail supermarket supply chain operators

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the South Africa cold chain logistics market were identified including refrigerated transportation demand, cold storage capacity, pharmaceutical distribution infrastructure, and agricultural export logistics networks supporting perishable food supply chains.

Step 2: Market Analysis and Construction

Comprehensive analysis of logistics infrastructure, trade flows, agricultural exports, and pharmaceutical distribution networks was conducted to estimate market size and evaluate industry structure, operational capabilities, and supply chain dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Industry insights were validated through consultations with logistics professionals, supply chain managers, and regulatory experts to confirm market drivers, infrastructure challenges, and technology adoption across cold chain logistics operations.

Step 4: Research Synthesis and Final Output

Collected data was synthesized using industry reports, trade statistics, logistics infrastructure assessments, and expert inputs to produce a structured analysis describing market size, segmentation, competitive dynamics, and strategic growth opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Fresh Food Retail and Supermarket Distribution Networks

Rising Pharmaceutical Distribution Requiring Temperature Controlled Logistics

Growth of Agricultural Exports Including Fruit Seafood and Meat Products - Market Challenges

High Energy Costs for Refrigerated Storage and Transport

Infrastructure Gaps in Rural and Agricultural Production Regions

Limited Availability of Advanced Temperature Monitoring Technologies - Market Opportunities

Expansion of Pharmaceutical Cold Chain Distribution Infrastructure

Development of Export Oriented Temperature Controlled Logistics Corridors

Adoption of Digital Temperature Monitoring and Smart Cold Chain Systems - Trends

Adoption of IoT Based Temperature Monitoring and Fleet Tracking Systems

Development of Large Scale Integrated Cold Storage Facilities Near Export Ports - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Transportation

Temperature Controlled Warehousing

Blast Freezing and Chilling Systems

Cold Storage Distribution Systems

Pharmaceutical Cold Chain Monitoring Systems - By Platform Type (In Value%)

Road Based Refrigerated Logistics

Air Freight Temperature Controlled Logistics

Sea Freight Refrigerated Container Logistics

Rail Based Refrigerated Cargo Transport

Integrated Multimodal Cold Chain Networks - By Fitment Type (In Value%)

New Cold Chain Infrastructure Installations

Retrofit Refrigeration Systems

Portable Refrigeration Units

Integrated Cold Chain Logistics Solutions - By End User Segment (In Value%)

Food and Beverage Producers

Pharmaceutical and Healthcare Companies

Agricultural Exporters and Seafood Processors

- Market Share Analysis

- Cross Comparison Parameters (Cold Storage Capacity, Refrigerated Fleet Size, Temperature Monitoring Technology, Distribution Network Coverage, Pharmaceutical Handling Capability, Export Logistics Integration, Warehouse Automation Level)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Imperial Logistics

Bidvest Panalpina Logistics

Kuehne + Nagel

DHL Supply Chain

Lineage Logistics

Americold Logistics

Cold Chain Africa

Value Logistics

Barloworld Logistics

DP World Logistics South Africa

Vector Logistics

Unitrans Supply Chain Solutions

CSX Logistics

RCL Foods Logistics

Clover Logistics

- Food processing companies requiring refrigerated logistics for national retail distribution

- Pharmaceutical distributors maintaining strict temperature control for vaccines and biologics

- Agricultural exporters depending on cold chain networks for fruit and seafood shipments

- Retail supermarket chains expanding chilled food distribution infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now