Download PDF

Download PDFMarket Overview

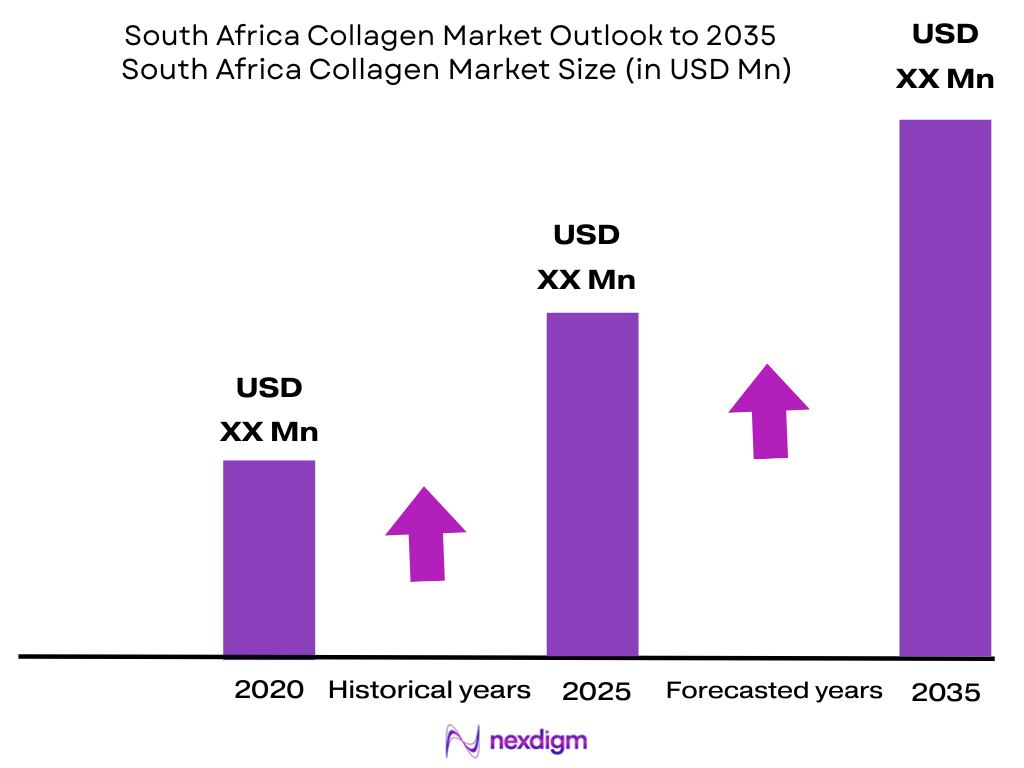

The South Africa collagen market is valued at USD ~ million, based on a five-year historical analysis, and is supported by gelatin, hydrolyzed collagen, food applications, healthcare use, beauty supplements and pharmaceutical excipients. The country’s GDP moved from USD 380.69 billion in the previous base year to USD 401.14 billion in the latest base year, while GDP per capita reached USD 6,267.2, supporting premium wellness and supplement purchases. Gauteng, Western Cape and KwaZulu-Natal dominate South Africa collagen demand because they concentrate pharmacies, wellness retailers, e-commerce fulfilment, beauty clinics, sports nutrition outlets and higher-income urban consumers. Gauteng has approximately 15.83 million residents, while KwaZulu-Natal has 12.34 million residents, making them the strongest retail demand pools. South Africa’s population reached 64.01 million, supporting wider use of collagen powders, capsules, gummies and beauty supplements.

Market Segmentation

By Product Type

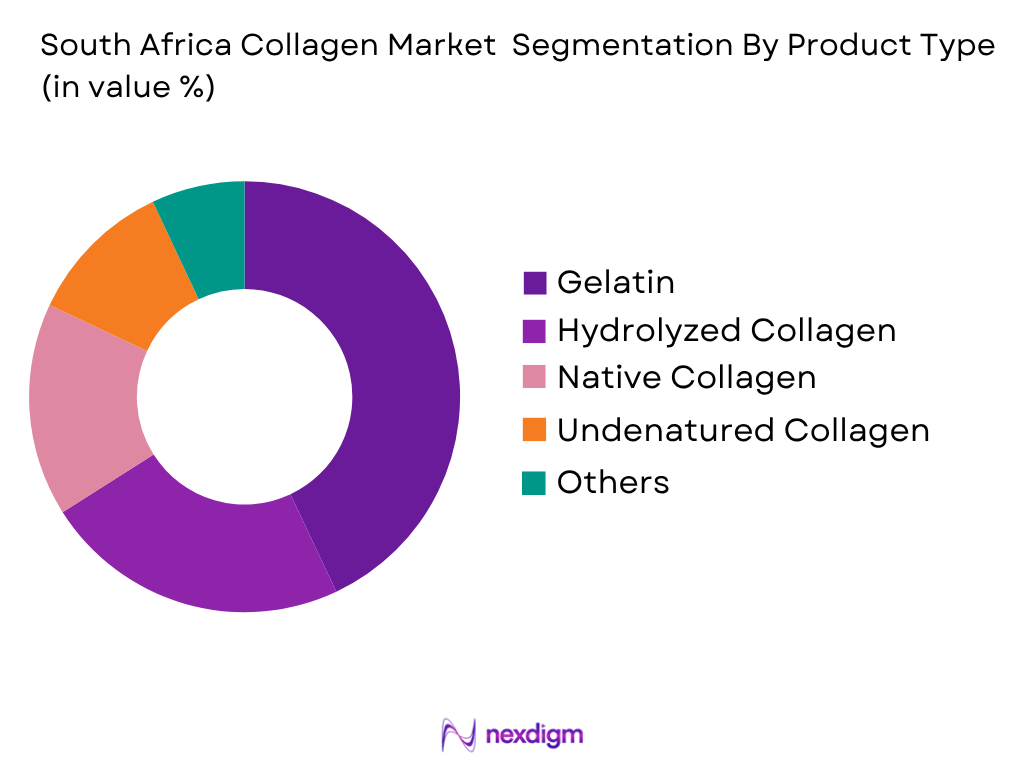

South Africa collagen market is segmented by product type into gelatin, hydrolyzed collagen peptides, native collagen, undenatured Type II collagen and other collagen products. Recently, gelatin has a dominant market share in South Africa under the product type segmentation, because it has stronger B2B use across food, confectionery, gummies, pharmaceutical capsules, dairy desserts and technical food systems. Gelatin is also commercially broader than premium collagen peptides because it acts as a gelling, stabilizing, binding and film-forming ingredient, rather than only a beauty or joint-health supplement ingredient. Hydrolyzed collagen is gaining faster adoption in powders, capsules and marine collagen beauty products, but gelatin continues to dominate because of its use in food manufacturing and pharmaceutical dosage formats. Grand View Research identifies gelatin as the largest revenue-generating product segment in South Africa collagen market.

By Source

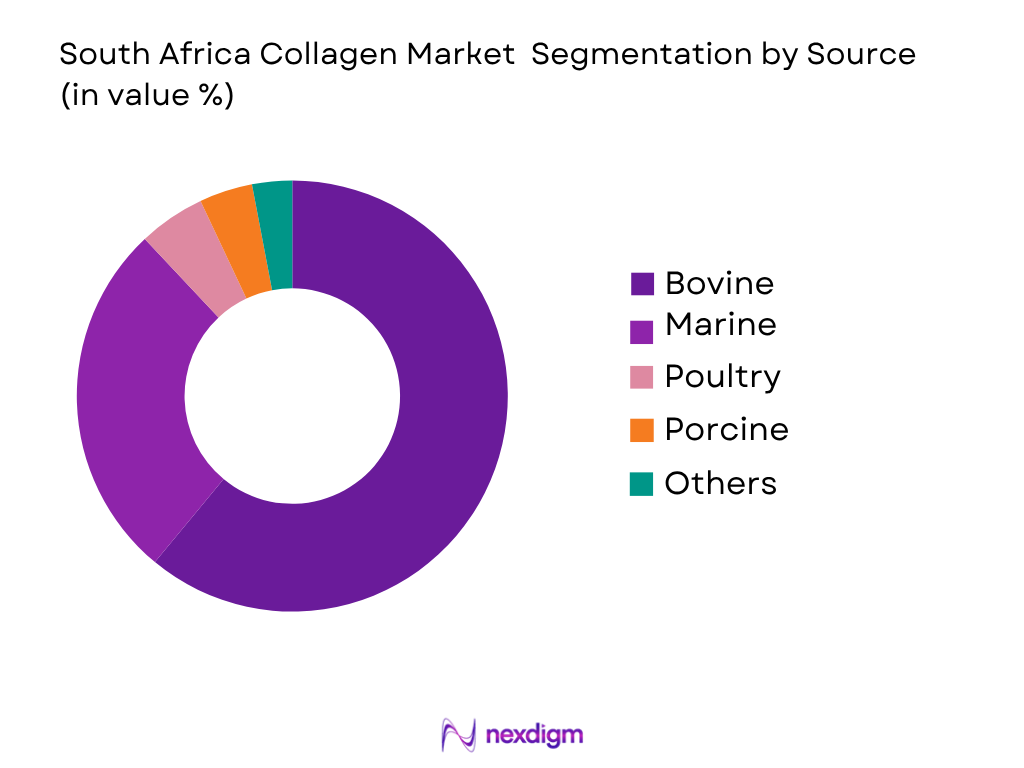

South Africa collagen market is segmented by source into bovine, marine, porcine, poultry and other sources. Recently, bovine collagen has a dominant market share in South Africa under source segmentation because the country has a significant livestock and meat-processing base that supports animal by-product availability, including hides, bones and connective tissues. Bovine collagen is also more scalable and cost-effective for powders, capsules, gummies and sports nutrition products than premium marine collagen. It contains Type I and Type III collagen, allowing brands to position products for skin, hair, nails, bones, joints and recovery. Marine collagen is more visible in premium beauty and clean-label products, especially among urban consumers in Cape Town and Johannesburg, but bovine collagen remains broader in mass wellness and functional nutrition formats.

Competitive Landscape

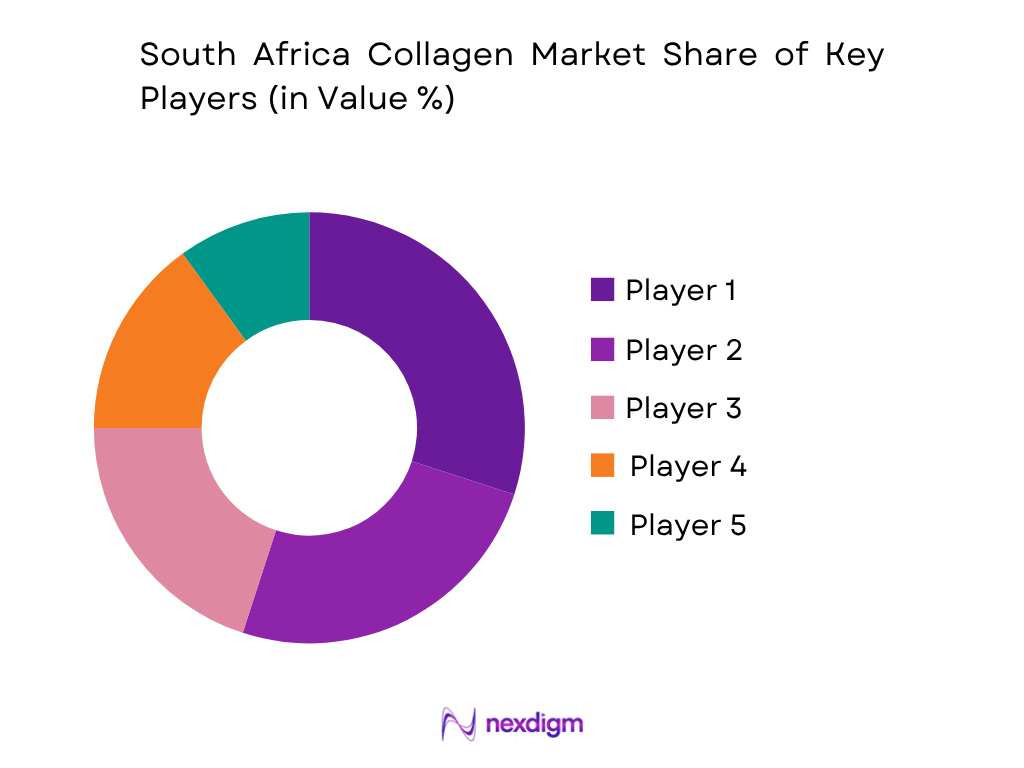

The South Africa collagen market includes domestic wellness brands, imported global supplement brands, pharmacy private-label ranges, sports nutrition companies and clean-label online retailers. Local brands such as The Harvest Table and MojoMe compete through bovine, marine and multi-collagen powders, while global brands such as Vital Proteins, NeoCell and Youtheory compete through imported collagen peptides, tablets and beauty-positioned products. Pharmacy chains and wellness retailers shape demand because consumers rely on trusted channels for source disclosure, quality assurance, dosage guidance and authenticity. The market is therefore fragmented at the consumer-brand level, while ingredient supply remains more dependent on imported collagen peptide and gelatin suppliers.

| Company | Establishment Year | Headquarters | Collagen Portfolio | Main Source Focus | Application Coverage | South Africa Market Role | Distribution Model | Strategic Strength |

| The Harvest Table | 2017 | KwaZulu-Natal, South Africa | ~ | ~ | ~ | ~ | ~ | ~ |

| MojoMe | 2014 | Cape Town, South Africa | ~ | ~ | ~ | ~ | ~ | ~ |

| Vital Proteins / Nestlé Health Science | 2013 | Chicago, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| NeoCell | 1998 | Irvine, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Youtheory | 2010 | Irvine, USA | ~ | ~ | ~ | ~ | ~ | ~ |

South Africa Collagen Market Analysis

Growth Drivers

Urban Consumer Base Supporting Beauty and Joint-Health Collagen Demand

South Africa collagen market is supported by urban consumers purchasing bovine collagen powders, marine collagen capsules, gummies and multi-collagen blends for skin hydration, hair support, nail health, joint mobility and sports recovery. Statistics South Africa reports the national population at 63.02 million in 2024, with Gauteng at 15.83 million people and KwaZulu-Natal at 12.34 million people, creating concentrated pharmacy and wellness-retail demand. World Bank reports GDP at USD 401.14 billion and GDP per capita at USD 6,267.2 in 2024, supporting collagen purchases among urban middle- and upper-income consumers.

Ageing and Active-Wellness Consumers Supporting Mobility Collagen Products

South Africa collagen market benefits from active-aging demand because collagen is positioned for cartilage support, joint mobility, bone health, tendon recovery and senior wellness. Statistics South Africa reports 6.13 million people aged 60 years or older in 2024, creating a direct consumer base for Type II collagen, hydrolyzed bovine collagen and joint-health capsules. Life expectancy is estimated at 63.6 years for males and 69.2 years for females, strengthening healthy-aging positioning. World Bank reports South Africa’s GDP at USD 401.14 billion and population growth at 1.2 in 2024, supporting wider long-term supplement consumption.

Market Challenges

Premium Affordability Pressure for Imported Marine and Multi-Collagen Products

South Africa collagen market faces affordability pressure because marine collagen, multi-collagen blends and imported peptide powders are discretionary health products. World Bank reports GDP per capita at USD 6,267.2 in 2024 and unemployment at 32.4 in 2025, limiting regular purchases of premium collagen formats for many households. Inflation stood at 4.4 in 2024, adding pressure on supplement baskets sold through pharmacies, wellness retailers and marketplaces. This challenge is market-specific because collagen products often require repeat monthly use, while consumers may switch to smaller tubs, sachets, value packs or lower-cost bovine collagen.

Regulatory Compliance Burden for Health Supplement Positioning

South Africa collagen market faces a compliance challenge because collagen supplements making beauty, joint, recovery or general-health claims may fall under health supplement and complementary medicine expectations. SAHPRA states health supplements allow only low-risk indications and must follow listed substances, dosage ranges and indications in its guidelines. SAHPRA also identifies 11 annexures for health supplement substances, including proteins and amino acids, animal extracts, fats and oils, carotenoids and bioflavonoids. World Bank reports GDP at USD 401.14 billion in 2024, making compliant national distribution commercially important for collagen brands entering pharmacies, e-commerce and wellness retail.

Market Opportunities

Bovine Collagen Development from Domestic Livestock and Meat-Processing Linkages

South Africa collagen market has an opportunity in bovine collagen powders and gelatin-linked applications because domestic cattle and meat-processing channels support animal by-product availability. The Department of Agriculture’s Abstract of Agricultural Statistics states South African agricultural statistics cover livestock and the contribution of primary agriculture to the economy, with cattle herd composition tracked in million head across bulls, cows, heifers, calves and oxen. This supports feedstock mapping for hides, bones and connective tissues used in bovine collagen. World Bank reports GDP at USD 401.14 billion and GDP per capita at USD 6,267.2 in 2024, supporting localized wellness manufacturing opportunities.

E-Commerce Expansion Supporting D2C Collagen Powders and Capsules

South Africa collagen market has an opportunity in e-commerce because collagen brands depend on product education, reviews, subscription packs, bundle offers and direct-to-consumer repeat purchases. World Bank reports that individuals using the internet reached 78 per 100 people in 2024, creating a large digital audience for collagen powders, capsules, gummies and beauty supplements. The same source reports net migration of 146,370 in 2025 and GDP per capita of USD 6,267.2 in 2024, supporting digitally exposed urban consumption. This helps domestic brands scale beyond pharmacy shelves through Takealot, Amazon South Africa, brand websites and wellness platforms.

Future Outlook

South Africa collagen market is expected to expand steadily over the next decade, supported by beauty-from-within consumption, active-aging demand, sports nutrition products, pharmacy retail trust, e-commerce expansion and wider adoption of collagen in functional foods. The country market is projected to move from USD 29.9 million to USD 49.2 million in the published country outlook, while the wider Africa collagen market is expected to grow at 6.20% CAGR in the long-term outlook to 2035. The South Africa-specific public forecast available from Grand View Research covers the country outlook only to 2030, with 8.9% CAGR in that published period. For the 2026–2035 report horizon, the most relevant long-term benchmark is the Africa collagen market CAGR of 6.20%, which reflects regional collagen demand growth across functional supplements, food applications, wound care and cosmetic applications.

Future growth will be driven by bovine collagen powders, marine collagen beauty products, multi-collagen blends, Type II joint-health capsules, collagen coffees, gummies, skin-health powders, sports recovery formulations and pet collagen supplements. Gauteng and Western Cape will remain the strongest demand centres because they combine urban income, pharmacy density, wellness retail, online ordering and fitness culture. The market will also remain sensitive to affordability and source trust. South African consumers are likely to favour products with clear bovine or marine sourcing, BSE-free documentation, halal or kosher certification where relevant, third-party testing, clean-label positioning and transparent dosage. Brands that can balance credible formulations with value packs and strong retail access will be better positioned.

Major Players

- The Harvest Table

- MojoMe

- Vital Proteins / Nestlé Health Science

- NeoCell

- Youtheory

- Nutritech

- Solgar

- Nature’s Nutrition

- Wellness Warehouse Collagen Range

- Faithful to Nature Collagen Range

- Clicks Collagen Range

- Dis-Chem Collagen Range

- NPL

- USN

- Evox Nutrition

Key Target Audience

- Collagen ingredient manufacturers

- Dietary supplement and nutraceutical brands

- Pharmacy and drugstore chains

- Health and wellness retailers

- Sports nutrition brands and distributors

- Beauty and nutricosmetic brands

- Investments and venture capitalist firms

- Government and regulatory bodies, South African Health Products Regulatory Authority, National Department of Health, Department of Agriculture, Land Reform and Rural Development, National Regulator for Compulsory Specifications

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map of South Africa collagen market, covering domestic wellness brands, imported supplement brands, pharmacies, e-commerce platforms, sports nutrition retailers, ingredient distributors, contract packers and regulators. The objective is to identify key variables such as source, product type, form factor, channel, application, grade, pricing architecture and claims positioning.

Step 2: Market Analysis and Construction

In this phase, historical and current data is compiled across collagen revenue, gelatin demand, hydrolyzed peptide adoption, pharmacy listings, e-commerce SKUs, sports nutrition products, source mix and consumer use cases. The analysis evaluates bovine, marine, porcine, poultry and multi-collagen products across beauty, joint-health, food, pharma and recovery applications.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted interviews with supplement distributors, pharmacy buyers, wellness retailers, e-commerce sellers, sports nutrition stores, domestic collagen brands and imported-product distributors. These consultations help validate assumptions around gelatin dominance, bovine source leadership, marine premiumization, affordability constraints and pharmacy channel trust.

Step 4: Research Synthesis and Final Output

The final phase combines top-down macroeconomic and category indicators with bottom-up SKU, channel and company-level checks. This approach validates South Africa collagen market size, segmentation, competitive intensity, regulatory risk, demand outlook and growth opportunities for investors, manufacturers, retailers, distributors and consumer-health companies.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Validation, Bottom-Up Validation, Import Mapping, SKU Benchmarking, Primary Interviews, Regulatory Review, Competitive Mapping, Forecast Model, Limitations)

- Definition and Scope

- Market Genesis and Evolution

- Timeline of Major Players

- Business Cycle and Supplement Consumption Seasonality

- Growth Drivers (Beauty-from-Within Demand, Sports Nutrition Adoption, Bovine Collagen Acceptance, Active Aging Demand, Pharmacy Channel Trust, E-Commerce Reach, Clean-Label Wellness Retail)

- Market Challenges (Imported Peptide Dependency, Currency Exposure, SAHPRA Compliance, Claim Restrictions, Price Sensitivity, Counterfeit Risk, Source Transparency)

- Market Opportunities (Premium Marine Collagen, Grass-Fed Bovine Collagen, Multi-Collagen Blends, Collagen Coffee, Sports Recovery, Pharmacy-Led Joint Health, Pet Collagen, Medical-Grade Collagen)

- Market Trends (Multi-Collagen Blends, Clean-Label Collagen, Marine Premiumization, Collagen Coffee, Third-Party Testing, Grass-Fed Claims, Sugar-Free Gummies, Influencer Education)

- SWOT Analysis

- Porter’s Five Forces

- PESTLE Analysis

- By Value (2020-2025)

- By Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Source (In Value %)

Bovine Collagen

Marine Collagen

Porcine Collagen

Poultry Collagen - By Product Type (In Value %)

Gelatin

Hydrolyzed Collagen Peptides

Native Collagen

Undenatured Type II Collagen

Multi-Collagen Blends

Collagen Beauty Foods - By Distribution Channel (In Value %)

Pharmacies and Drugstores

Health and Wellness Retailers

E-Commerce Marketplaces

Supermarkets and Hypermarkets - By Province (In Value %)

Gauteng

Western Cape

KwaZulu-Natal

Eastern Cape

Free State

Mpumalanga

- Market Share of Major Players on the Basis of Value and Volume

- Cross Comparison Parameters (Collagen Source Portfolio, Product Format Portfolio, SAHPRA Compliance Readiness, Pharmacy and E-Commerce Reach, Country-of-Origin Positioning, Certification and Traceability, Ingredient Stacking Capability, Influencer and D2C Strength)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

The Harvest Table

MojoMe

Vital Proteins / Nestlé Health Science

NeoCell

Youtheory

Nutritech

Solgar

Nature’s Nutrition

NutriTech Collagen

Wellness Warehouse Own-Brand and Curated Collagen Range

Faithful to Nature Collagen Range

Clicks Collagen Range

Dis-Chem Collagen Range

NPL

USN

- Supplement Brand and Importer Demand

- Beauty and Nutricosmetic Brand Demand

- Pharmacy and Drugstore Buyer Demand

- E-Commerce Seller Demand

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now