Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Recent industry assessments place the South Africa Diagnostic Labs Market at approximately USD ~ billion, driven primarily by rising diagnostic testing demand associated with chronic disease monitoring, infectious disease screening, and preventive healthcare services across both public and private healthcare systems. Expanding clinical laboratory networks, increasing utilization of pathology testing, and wider adoption of automated diagnostic technologies significantly strengthen testing capacity. Government investment in healthcare infrastructure and laboratory modernization programs also supports higher diagnostic volumes and sustained operational growth.

Johannesburg, Cape Town, and Durban function as dominant diagnostic laboratory hubs because they host large hospital networks, advanced pathology laboratories, and extensive private healthcare infrastructure capable of supporting high testing volumes. These metropolitan areas attract major diagnostic service providers due to stronger healthcare spending, higher population density, and better access to specialized medical professionals. Large private laboratory chains concentrate operations in these cities to optimize logistics, laboratory automation investment, and centralized testing facilities that support nationwide diagnostic service coverage.

Market Segmentation

By Product Type

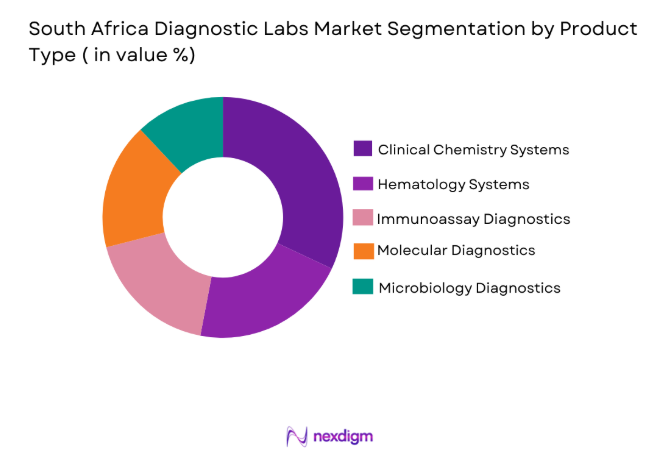

South Africa Diagnostic Labs market is segmented by product type into clinical chemistry testing, hematology testing, immunoassay diagnostics, molecular diagnostics, and microbiology diagnostics. Recently, clinical chemistry testing has a dominant market share due to factors such as high testing frequency for routine health screenings, strong hospital laboratory demand, and widespread use in chronic disease monitoring. Clinical chemistry analyzers are widely deployed across hospitals and independent laboratories because they support high throughput testing for metabolic disorders, liver function analysis, and kidney function assessments. The routine nature of these tests ensures continuous demand across both private and public healthcare facilities, reinforcing the dominant position of clinical chemistry diagnostics within laboratory operations nationwide.

By Platform Type

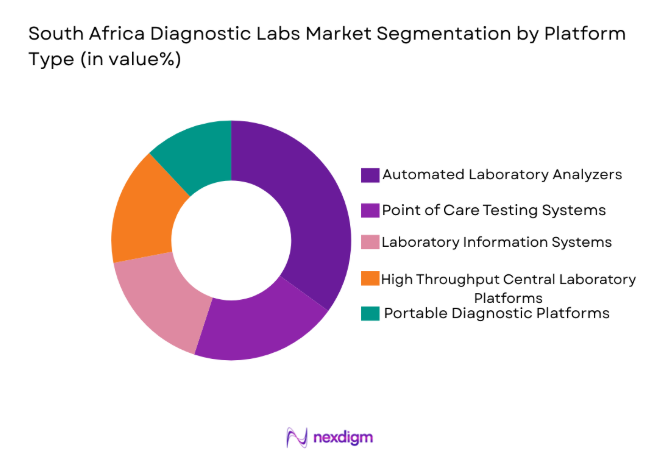

South Africa Diagnostic Labs market is segmented by platform type into automated laboratory analyzers, point of care testing systems, laboratory information systems, high throughput central laboratory platforms, and portable diagnostic platforms. Recently, automated laboratory analyzers have a dominant market share due to factors such as large scale testing requirements, operational efficiency improvements, and increasing laboratory automation investments. Diagnostic laboratories rely heavily on automated analyzers to process large test volumes with higher accuracy and faster turnaround times. These systems reduce manual errors, improve laboratory workflow efficiency, and allow laboratories to expand service capacity while managing operational costs, making automated diagnostic platforms central to modern laboratory infrastructure development across South Africa.

Competitive Landscape

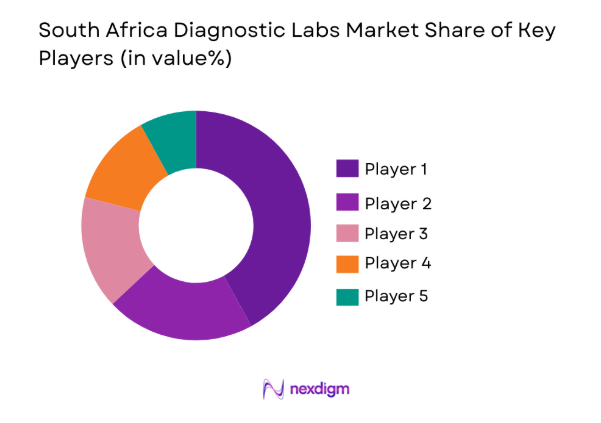

The South Africa Diagnostic Labs Market demonstrates moderate consolidation with several dominant pathology networks operating extensive laboratory infrastructure across the country. Large diagnostic chains control substantial testing volumes through centralized laboratories, national specimen collection networks, and advanced laboratory automation capabilities. Private laboratory groups continue expanding through acquisitions and regional laboratory partnerships while international diagnostic technology providers strengthen the competitive environment by supplying advanced testing platforms, reagents, and laboratory information systems.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Laboratory Network Size |

| Lancet Laboratories | 1948 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| Ampath Laboratories | 1996 | Centurion | ~ | ~ | ~ | ~ | ~ |

| PathCare Laboratories | 1922 | Cape Town | ~ | ~ | ~ | ~ | ~ |

| National Health Laboratory Service | 2000 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| Intercare Laboratories | 2000 | Pretoria | ~ | ~ | ~ | ~ | ~ |

South Africa Diagnostic Labs Market Analysis

Growth Drivers

Rising Burden of Infectious and Chronic Diseases Driving Diagnostic Testing Demand

Increasing prevalence of infectious diseases and chronic health conditions significantly expands diagnostic testing requirements across South Africa’s healthcare system. High incidence of HIV tuberculosis diabetes and cardiovascular diseases requires continuous laboratory monitoring and routine testing services across both public hospitals and private healthcare providers. Diagnostic laboratories play a central role in disease detection treatment monitoring and preventive healthcare programs which strengthens testing volumes nationwide. Healthcare providers increasingly rely on laboratory diagnostics to guide clinical decision making and improve treatment outcomes. Expanding screening programs for infectious diseases further increase demand for laboratory testing infrastructure. Chronic disease management also requires repeated blood testing pathology screening and biochemical analysis which generates sustained diagnostic demand. Government public health programs encourage large scale screening initiatives for communicable diseases and maternal health monitoring. These initiatives significantly increase laboratory workloads and create long term growth opportunities for diagnostic laboratories operating across urban and rural healthcare facilities.

Expansion of Private Healthcare Infrastructure and Diagnostic Laboratory Networks

Rapid development of private healthcare infrastructure across South Africa significantly strengthens the growth of diagnostic laboratory services and testing volumes. Private hospitals outpatient clinics and specialized medical centers increasingly integrate laboratory services to support faster patient diagnosis and clinical treatment decisions. Diagnostic companies continue expanding nationwide specimen collection networks allowing patients to access testing services conveniently across multiple cities and regional healthcare facilities. Advanced laboratory automation technologies improve operational efficiency enabling laboratories to process larger sample volumes with faster turnaround times. Private healthcare providers also invest heavily in modern pathology laboratories equipped with high throughput analyzers and digital laboratory information systems. These investments enhance diagnostic capacity and encourage the adoption of advanced molecular testing technologies. Growing middle class healthcare spending and rising demand for preventive health screenings further support laboratory service utilization. As private healthcare infrastructure expands diagnostic laboratory companies continue strengthening their national service networks to capture increasing patient testing demand.

Market Challenges

High Cost of Advanced Diagnostic Equipment and Laboratory Automation Infrastructure

Diagnostic laboratories require substantial capital investment to establish modern testing facilities capable of processing high sample volumes with accurate results. Advanced diagnostic analyzers automated laboratory systems and molecular testing platforms involve high procurement and maintenance costs which create financial pressure for smaller laboratory operators. Laboratories must continuously upgrade technology to remain competitive and maintain high quality testing standards. Costly reagent supplies calibration materials and maintenance contracts further increase operational expenditures for diagnostic service providers. Smaller laboratories often struggle to adopt modern automation technologies due to budget constraints which can reduce their competitiveness against larger laboratory networks. Healthcare reimbursement limitations also affect laboratory profitability and restrict investment in new diagnostic equipment. In addition laboratories must comply with strict quality accreditation standards which require additional infrastructure investment. These financial pressures create operational challenges particularly for independent laboratories attempting to expand testing capacity across regional healthcare markets.

Shortage of Skilled Laboratory Professionals and Diagnostic Specialists

The availability of trained laboratory technologists pathologists and molecular diagnostics specialists remains limited across the South African healthcare sector which creates workforce challenges for diagnostic laboratories. Modern laboratory technologies require specialized expertise to operate automated analyzers perform molecular testing and interpret complex diagnostic results. Diagnostic companies face difficulties recruiting experienced professionals particularly in rural regions where skilled healthcare workers are scarce. Training programs for laboratory technicians and pathologists require significant time and educational resources which slows workforce development. As diagnostic technologies become more sophisticated laboratories must invest in continuous professional training to ensure operational efficiency. Staffing shortages can increase workload pressure for existing personnel and extend diagnostic test turnaround times. Laboratories also compete with hospitals research institutions and international healthcare organizations for qualified professionals. Workforce limitations therefore restrict laboratory expansion and may affect the ability of diagnostic companies to scale testing operations across the country.

Opportunities

Expansion of Molecular Diagnostics and Genomic Testing Services

Rapid advancement in molecular diagnostics technologies creates significant opportunities for diagnostic laboratories to expand specialized testing services across South Africa. Molecular diagnostic techniques enable early detection of infectious diseases genetic disorders and cancer biomarkers which improves treatment outcomes and supports personalized medicine strategies. Healthcare providers increasingly rely on molecular testing to identify disease pathogens and guide targeted therapies. Diagnostic laboratories that invest in advanced molecular platforms can offer high value specialized tests that generate stronger revenue streams. Demand for genetic testing cancer screening and precision medicine diagnostics continues increasing among healthcare providers and research institutions. Pharmaceutical companies conducting clinical trials also require molecular diagnostic services to support drug development programs. Government health programs targeting infectious diseases further stimulate demand for advanced molecular diagnostics capabilities. As technology costs gradually decline diagnostic laboratories have greater opportunities to adopt genomic testing services and expand their clinical diagnostic portfolios.

Growth of Preventive Healthcare and Routine Diagnostic Screening Programs

Increasing awareness of preventive healthcare and routine health monitoring significantly strengthens opportunities for diagnostic laboratories to expand testing services. Healthcare providers encourage regular laboratory screening for chronic diseases metabolic disorders and infectious disease detection to support early treatment intervention. Preventive health checkup packages offered by private hospitals and clinics drive consistent demand for blood testing pathology services and biochemical analysis. Employers also introduce corporate wellness programs that include routine health screening for employees which increases diagnostic testing volumes. Public healthcare authorities promote screening programs for maternal health infectious disease detection and chronic disease monitoring which expands national diagnostic service utilization. Technological improvements in laboratory automation enable laboratories to handle large screening volumes efficiently. Diagnostic service providers that expand specimen collection centers and mobile diagnostic services can capture growing demand for routine testing across urban and semi urban populations.

Future Outlook

The South Africa Diagnostic Labs Market is expected to experience steady expansion as healthcare systems increasingly prioritize early disease detection and diagnostic driven treatment decisions. Technological advancements in molecular diagnostics laboratory automation and digital laboratory management systems will strengthen testing efficiency and service quality. Government healthcare infrastructure investments and public health screening programs are likely to sustain testing demand. Private healthcare expansion combined with rising preventive health awareness will further increase diagnostic testing utilization across the country.

Major Players

- Lancet Laboratories

- Ampath Laboratories

- PathCare Laboratories

- National Health Laboratory Service

- Intercare Laboratories

- Vermaak and Partners Pathologists

- Synlab South Africa

- Cerba Lancet Africa

- Roche Diagnostics South Africa

- Abbott Laboratories South Africa

- Siemens Healthineers South Africa

- BioRad Laboratories

- Thermo Fisher Scientific

- Quest Diagnostics

- Beckman Coulter Diagnostics

Key Target Audience

- Diagnostic laboratory service providers

- Hospital and healthcare facility operators

- Medical diagnostic equipment manufacturers

- Pharmaceutical and biotechnology companies

- Healthcare technology solution providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying major variables influencing the South Africa Diagnostic Labs Market including diagnostic demand patterns laboratory infrastructure capacity and technological adoption across healthcare providers. Market influencing indicators such as healthcare spending diagnostic volumes and disease prevalence trends are evaluated to define the analytical framework.

Step 2: Market Analysis and Construction

Primary and secondary research sources are used to construct the market structure including laboratory service providers diagnostic equipment suppliers and healthcare institutions. Market segmentation analysis evaluates product type platform adoption and end user demand patterns across different healthcare sectors.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including diagnostic laboratory executives healthcare professionals and technology providers are consulted to validate market assumptions. Expert interviews help refine demand projections technology adoption patterns and competitive dynamics influencing diagnostic laboratory operations.

Step 4: Research Synthesis and Final Output

All research findings are synthesized through structured market modeling and data triangulation to produce the final analytical report. Insights are validated through cross verification with industry publications healthcare databases and regulatory documentation to ensure analytical accuracy.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Burden of Infectious Diseases Including HIV Tuberculosis and Malaria

Expansion of Public Healthcare Infrastructure and Universal Health Coverage Programs

Growing Adoption of Advanced Molecular and Genetic Testing Technologies - Market Challenges

High Cost of Advanced Diagnostic Equipment and Laboratory Infrastructure

Shortage of Skilled Laboratory Technologists and Pathologists

Regulatory Compliance and Quality Accreditation Requirements - Market Opportunities

Increasing Demand for Molecular Diagnostics and Genomic Testing

Expansion of Private Diagnostic Laboratory Networks in Urban Areas

Growing Public Private Partnerships in Healthcare Diagnostics - Trends

Adoption of Automation and Digital Laboratory Information Systems

Growing Use of Point of Care Diagnostic Testing in Primary Healthcare Facilities - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Testing Systems

Hematology Testing Systems

Immunoassay Testing Systems

Molecular Diagnostics Systems

Microbiology Testing Systems - By Platform Type (In Value%)

Automated Laboratory Analyzers

Point-of-Care Diagnostic Platforms

High Throughput Central Lab Platforms

Integrated Laboratory Information Systems

Portable Diagnostic Testing Platforms - By Fitment Type (In Value%)

Standalone Diagnostic Systems

Integrated Laboratory Automation Systems

Modular Diagnostic Platforms

Cloud Connected Diagnostic Systems - By End User Segment (In Value%)

Hospitals and Healthcare Facilities

Independent Diagnostic Laboratories

Research and Academic Institutions

- Market Share Analysis

- Cross Comparison Parameters (Test Portfolio Breadth, Laboratory Network Coverage, Technology Adoption Level, Accreditation and Compliance Standards, Turnaround Time Efficiency, Pricing Structure, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Lancet Laboratories

Ampath Laboratories

PathCare Laboratories

National Health Laboratory Service

Intercare Laboratories

Drs Dietrich Voigt Mia and Partners

Synlab South Africa

Vermaak and Partners Pathologists

Cerba Lancet Africa

Roche Diagnostics South Africa

Abbott Laboratories South Africa

Siemens Healthineers South Africa

BioRad Laboratories

Thermo Fisher Scientific

Quest Diagnostics

- Hospitals expanding in-house laboratory capabilities to support faster clinical decision making

- Independent diagnostic chains increasing collection centers to improve geographic coverage

- Research institutions driving demand for advanced molecular testing and pathology services

- Private healthcare providers investing in high throughput diagnostic laboratories

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now