Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Africa Edge Computing market reached approximately USD ~ million based on a recent historical assessment, supported by accelerated enterprise digitalization, telecom network densification, and localized data processing demand. Expansion of 5G infrastructure by major operators and deployment of distributed micro data centers by colocation providers have driven adoption across latency sensitive applications such as video analytics, industrial automation, and financial services processing. Public sector smart infrastructure programs and cloud providers’ regional edge expansion have further strengthened infrastructure investments nationwide.

Johannesburg and Cape Town dominate the South Africa Edge Computing market due to concentration of hyperscale data centers, telecom exchange hubs, and enterprise headquarters. Johannesburg benefits from financial sector digital transformation and dense fiber interconnection corridors, while Cape Town hosts major submarine cable landings and cloud regions enabling edge proximity services. Durban and Pretoria are emerging secondary nodes driven by logistics, port automation, and government digital service platforms requiring localized processing and resilient distributed compute environments.

Market Segmentation

By Product Type

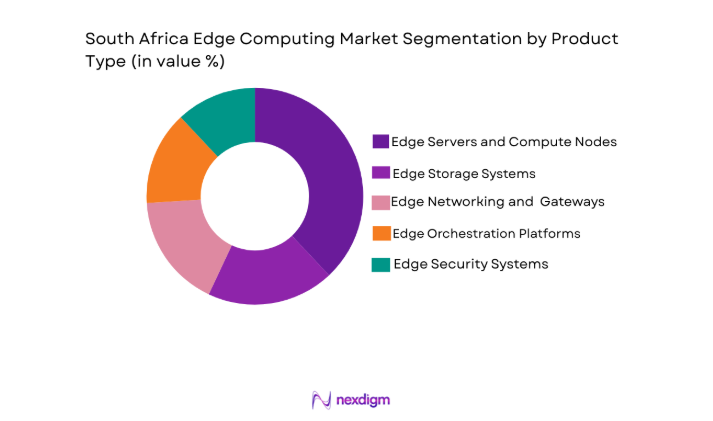

South Africa Edge Computing market is segmented by product type into edge servers and compute nodes, edge storage systems, edge networking and gateways, edge orchestration platforms, and edge security systems. Recently, edge servers and compute nodes has a dominant market share due to factors such as enterprise demand patterns for localized processing, strong vendor presence in modular compute hardware, and infrastructure availability across telecom and data center edge facilities. Growth of AI inference workloads, video analytics processing, and private 5G applications has further reinforced adoption of high performance compute nodes at distributed edge locations nationwide.

By Platform Type

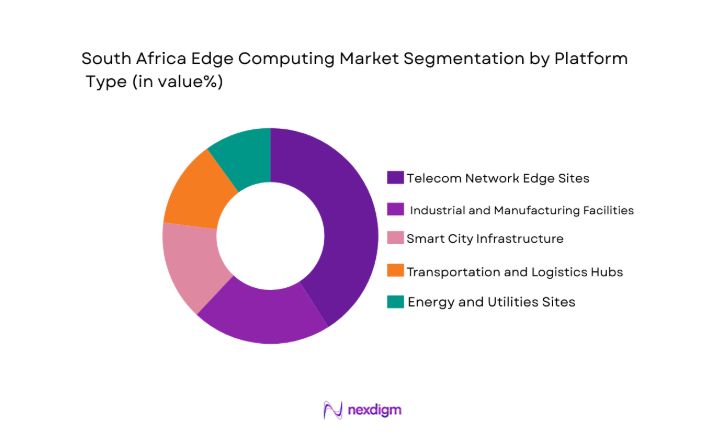

South Africa Edge Computing market is segmented by platform type into telecom network edge sites, industrial and manufacturing facilities, smart city infrastructure, transportation and logistics hubs, and energy and utilities sites. Recently, telecom network edge sites has a dominant market share due to factors such as extensive base station footprint, telecom operator investments in distributed compute infrastructure, and infrastructure availability at 5G aggregation points. Mobile traffic growth, content delivery caching, and multi access edge computing services deployed by operators have accelerated adoption across national telecom edge locations.

Competitive Landscape

South Africa Edge Computing market exhibits moderate consolidation with telecom operators, colocation providers, and global infrastructure vendors shaping deployment ecosystems. Large telecom groups control distributed network edge sites, while data center operators extend micro data center footprints near enterprise clusters. Global technology vendors supply compute, orchestration, and networking stacks through partnerships with operators and integrators. Hyperscale cloud providers influence architecture standards and platform adoption through regional edge services and hybrid cloud integration models.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Model |

| Liquid Intelligent Technologies | 2005 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Teraco Data Environments | 2008 | Johannesburg, South Africa | ~ | ~ | ~ | ~ | ~ |

| Africa Data Centres | 2010 | Johannesburg, South Africa | ~ | ~ | ~ | ~ | ~ |

| MTN Group | 1994 | Johannesburg, South Africa | ~ | ~ | ~ | ~ | ~ |

| Vodacom | 1994 | Midrand, South Africa | ~ | ~ | ~ | ~ | ~ |

South Africa Edge Computing Market Analysis

Growth Drivers

5G Infrastructure Expansion and Multi Access Edge Computing Adoption

South Africa’s nationwide rollout of fifth generation mobile networks and fiber backhaul has fundamentally reshaped the computing topology by distributing processing closer to users and devices, thereby accelerating demand for edge computing infrastructure across telecom aggregation layers and enterprise campuses. Telecom operators are integrating multi access edge computing platforms within base station clusters and central offices to support ultra low latency services such as immersive media, industrial robotics control, and connected vehicle telemetry, which require localized compute and deterministic network performance. The deployment of 5G standalone cores and network slicing capabilities has further enabled differentiated edge service tiers for enterprise customers, including private network segments for mining automation, manufacturing analytics, and logistics tracking, each requiring embedded compute nodes at radio access and aggregation points. Enterprises are increasingly adopting private fifth generation networks integrated with on site edge servers to ensure data sovereignty, operational resilience, and real time decision making for mission critical applications such as predictive maintenance, autonomous haulage, and video based safety monitoring in remote environments. Content providers and digital platforms are also deploying edge caching and processing infrastructure within telecom edge facilities to optimize streaming latency and bandwidth utilization, particularly in urban corridors with high mobile traffic density and multimedia consumption patterns. Public safety agencies and municipalities are leveraging telecom edge deployments to support intelligent surveillance, traffic management, and emergency response analytics, integrating sensor networks and camera feeds with localized processing to reduce response times and backhaul costs. The convergence of telecom, cloud, and enterprise ecosystems around distributed 5G edge architectures has therefore created a structural demand driver for scalable edge computing hardware, orchestration platforms, and secure distributed networking across South Africa.

Enterprise Digitalization and Real Time Data Processing Requirements

Rapid enterprise digital transformation across financial services, manufacturing, mining, retail, and public administration has created a surge in latency sensitive workloads that cannot be efficiently processed in centralized data centers, thereby driving sustained investment in localized edge computing infrastructure across metropolitan and industrial regions. Organizations are deploying edge servers within branch offices, factories, warehouses, and retail outlets to process transactional, video, and sensor data in real time, enabling immediate analytics, automation, and customer interaction without dependence on distant cloud regions or unstable wide area connectivity. The financial sector is implementing edge processing within trading floors, ATM networks, and fraud detection systems to ensure millisecond level transaction verification and compliance monitoring, particularly in high frequency payment environments requiring continuous availability. Manufacturing enterprises are adopting edge analytics integrated with industrial internet of things platforms to enable predictive maintenance, quality inspection using machine vision, and closed loop process optimization on production lines, all of which demand deterministic local compute capacity. Retail and logistics companies are installing edge nodes within distribution centers and stores to support inventory vision analytics, autonomous checkout systems, and route optimization engines that rely on continuous data ingestion from cameras, scanners, and sensors. Government digital service platforms are increasingly deploying localized processing within municipal facilities to support citizen services, smart metering, and surveillance analytics, ensuring data privacy and operational continuity under variable connectivity conditions. As enterprises seek to minimize latency, bandwidth costs, and data exposure risks while enabling advanced analytics and automation, the shift toward distributed computing architectures has become a central growth driver for the South Africa edge computing market.

Market Challenges

Power Reliability Constraints and Distributed Infrastructure Resilience Requirements

South Africa’s persistent power instability and load shedding cycles create a structural challenge for distributed edge computing deployments, as edge nodes are typically installed in remote, industrial, or urban roadside environments where power continuity and conditioning are more difficult to guarantee than in centralized data centers. Edge infrastructure must therefore incorporate battery systems, generators, and ruggedized power management units, increasing deployment complexity, operational cost, and maintenance requirements across geographically dispersed sites. Telecom base station edge installations face uptime risks during grid disruptions, potentially affecting latency critical services such as industrial automation control and real time analytics streams that depend on continuous edge availability. Enterprises deploying on premise edge nodes in factories, warehouses, and branch facilities must invest in localized uninterruptible power systems and cooling redundancies, which can raise capital expenditure and slow adoption among cost sensitive organizations. Environmental conditions such as heat, dust, and vibration in mining and industrial settings further strain power and thermal management systems, necessitating specialized ruggedized hardware and enclosure designs that elevate total cost of ownership. Distributed energy management across hundreds of micro data centers and edge cabinets requires sophisticated monitoring and predictive maintenance systems, adding operational complexity for operators lacking large scale infrastructure management expertise. Until national grid reliability and distributed energy solutions mature sufficiently, power resilience constraints will continue to limit optimal scaling and performance consistency of edge computing infrastructure across South Africa.

Skills Shortage in Edge Architecture Deployment and Lifecycle Management

The South Africa edge computing ecosystem faces a significant human capital constraint due to limited availability of professionals skilled in distributed systems architecture, edge orchestration platforms, network slicing integration, and lifecycle management of geographically dispersed compute infrastructure. Edge environments require interdisciplinary expertise spanning telecom networking, cloud native software, cybersecurity, industrial automation protocols, and hardware maintenance, creating a complex skills profile not yet widely available in the domestic workforce. Telecom operators and enterprises deploying edge nodes must manage provisioning, orchestration, monitoring, and security across thousands of endpoints, requiring advanced automation and specialized operational knowledge that many organizations lack internally. Integration of edge platforms with private fifth generation networks, industrial internet of things systems, and hybrid cloud environments demands engineers capable of cross domain architecture design and troubleshooting, increasing reliance on scarce specialists and external vendors. Training programs and academic curricula have only recently begun addressing edge computing and distributed infrastructure competencies, resulting in a transitional period where demand for expertise exceeds supply. Smaller enterprises and municipalities face particular challenges in recruiting and retaining skilled personnel to operate localized edge systems, leading to underutilization or delayed deployments. Without accelerated workforce development and ecosystem capability building, the skills gap will remain a structural barrier to efficient scaling and optimization of edge computing deployments across South Africa.

Opportunities

Private Industrial Edge Networks for Mining and Manufacturing Automation

South Africa’s globally significant mining and industrial sectors present a major opportunity for deployment of private edge computing networks integrated with localized wireless connectivity and industrial automation platforms to enable real time control, analytics, and safety monitoring in geographically dispersed and harsh operating environments. Mining operations increasingly require autonomous haulage, remote drilling control, and environmental sensing systems that generate high volumes of latency sensitive data best processed at on site edge nodes rather than distant cloud facilities. Integration of private fifth generation or dedicated wireless networks with ruggedized edge servers allows deterministic communication between machinery, sensors, and analytics applications, supporting predictive maintenance, worker safety monitoring, and energy optimization across large mining complexes. Manufacturing plants similarly benefit from localized edge analytics for machine vision inspection, robotics coordination, and production optimization requiring millisecond level response times and data sovereignty within factory boundaries. Vendors and telecom operators can develop industry specific edge platforms tailored to mining and manufacturing workflows, including pre integrated analytics stacks, industrial protocol support, and environmental ruggedization, reducing deployment complexity for enterprises. Government industrial modernization programs and digital transformation initiatives further reinforce demand for localized computing infrastructure within resource extraction and manufacturing clusters. As industries prioritize automation, safety, and productivity improvements, private industrial edge networks represent a scalable and high value growth opportunity for edge infrastructure providers in South Africa.

Smart Infrastructure and Urban Digitalization Edge Platforms

Rapid urbanization and municipal digital transformation initiatives across South African metropolitan regions create a significant opportunity for deployment of edge computing platforms embedded within smart infrastructure systems supporting transportation management, public safety, utilities monitoring, and citizen services delivery. Cities are deploying sensor networks, connected traffic signals, surveillance cameras, and environmental monitoring devices that generate continuous data streams requiring localized processing to enable real time analytics and decision making without dependence on centralized data centers. Edge nodes integrated within street cabinets, transport hubs, and municipal facilities can support video analytics for traffic optimization, automated incident detection, and crowd monitoring while reducing backhaul bandwidth and latency constraints. Utilities providers are installing smart grid and smart metering systems generating distributed telemetry that can be processed at neighborhood level edge platforms to enhance grid resilience, outage prediction, and energy optimization. Public safety agencies benefit from localized facial recognition, anomaly detection, and emergency response analytics executed at city edge nodes to accelerate situational awareness and operational coordination. Collaboration between municipalities, telecom operators, and technology vendors can establish shared urban edge platforms supporting multiple city services and commercial applications. As cities invest in digital infrastructure to improve efficiency, safety, and sustainability, urban edge computing platforms represent a long term expansion opportunity for the South Africa edge computing market.

Future Outlook

South Africa Edge Computing market is expected to expand steadily over the next five years driven by continued 5G densification, enterprise automation adoption, and urban digital infrastructure investments. Growth will be supported by telecom operator edge expansion, industrial private network deployments, and hyperscale cloud regional edge integration. Regulatory emphasis on data localization and digital sovereignty will further encourage distributed computing architectures. Advancements in AI inference hardware and modular micro data centers will improve cost efficiency and scalability across distributed edge environments.

Major Players

- Liquid Intelligent Technologies

- TeracoData Environments

- Africa Data Centres MTN Group

- Vodacom

- Huawei Technologies

- Nokia

- Ericsson

- Amazon Web Services

- Microsoft

- Dell Technologies

- Hewlett Packard Enterprise

- Cisco Systems

- Schneider Electric

Key Target Audience

- Telecom operators

- Data center operators

- Mining and industrial enterprises

- Manufacturing companies

- Smart city authorities

- Energy and utilities providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including edge infrastructure deployments, telecom network expansion, enterprise digitalization levels, and distributed data processing demand were identified through secondary industry reports and regulatory publications to define market structure and segmentation foundations.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using triangulation of telecom infrastructure investments, enterprise IT spending, and data center capacity expansion across South Africa, supported by vendor shipment data and operator deployment disclosures.

Step 3: Hypothesis Validation and Expert Consultation

Findings and assumptions were validated through consultations with telecom infrastructure specialists, data center operators, and enterprise IT architects to confirm deployment trends, technology adoption patterns, and realistic segmentation weightings.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into a structured market model integrating supply side vendor data and demand side adoption indicators, ensuring internal consistency and alignment with observed infrastructure expansion trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of 5G and Fiber Network Infrastructure

Rising Industrial Automation and IoT Adoption

Data Localization and Low Latency Requirements

Growth of Smart Cities and Public Safety Systems

Enterprise Demand for Real Time Analytics - Market Challenges

Power Reliability and Energy Costs

Skills Shortage in Edge Infrastructure Management

Cybersecurity Risks at Distributed Sites

High Initial Deployment and Integration Costs

Limited Rural Connectivity Infrastructure - Market Opportunities

Private 5G and Industrial Edge Integration

Edge AI for Video and Surveillance Analytics

Distributed Edge for Renewable Energy Grids - Trends

Convergence of Cloud and Telco Edge Platforms

Adoption of Modular Micro Data Centers

AI Enabled Edge Processing in Industry

Edge as a Service Business Models

Integration of Edge with National Broadband Initiatives - Government Regulations & Defense Policy

Data Protection and Localization under POPIA

National 5G Spectrum and ICT Policy Frameworks

Public Infrastructure Digitalization Programs - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge Servers and Compute Nodes

Edge Storage Systems

Edge Networking and Gateways

Edge Orchestration and Management Platforms

Edge Security and Monitoring Systems - By Platform Type (In Value%)

Telecom Network Edge Sites

Industrial and Manufacturing Facilities

Smart City and Public Infrastructure

Transportation and Logistics Hubs

Energy and Utilities Sites - By Fitment Type (In Value%)

On Premise Enterprise Edge Deployments

On Site Micro Data Centers

Telco Colocation Edge Installations

Embedded Industrial Edge Systems

Outdoor Ruggedized Edge Units - By End User Segment (In Value%)

Telecom Operators

Mining and Natural Resources Firms

Manufacturing Enterprises

Retail and Logistics Providers

Public Sector and Smart City Authorities - By Procurement Channel (In Value%)

Direct Enterprise Procurement

Telecom Managed Edge Services

Cloud Marketplace Procurement

System Integrator Contracts

Government and Municipal Tenders - By Material / Technology (in Value %)

Multi Access Edge Computing Platforms

GPU Accelerated Edge Infrastructure

Ruggedized Industrial Hardware

5G Enabled Edge Architectures

IoT Integrated Edge Gateways

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Deployment Scale, Edge Hardware Portfolio, Software Stack Capability, Telco Partnerships, Industry Vertical Focus)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Liquid Intelligent Technologies

Teraco Data Environments

Africa Data Centres

MTN Group

Vodacom

Huawei Technologies

Nokia

Ericsson

Amazon Web Services

Microsoft

Google

Dell Technologies

Hewlett Packard Enterprise

Cisco Systems

Schneider Electric

- Telecom operators expanding distributed compute at base stations

- Mining sector deploying rugged edge for remote automation

- Manufacturers adopting edge for predictive maintenance

- Municipalities integrating edge in smart city systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now