Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The South Africa Electric Bus Market reached approximately USD ~ billion based on a recent historical assessment, supported by increasing investments in zero-emission transportation and public transit electrification programs. Growth in the market is primarily driven by urban mobility modernization initiatives, rising environmental concerns, and electrification strategies adopted by public transport agencies. Government-backed pilot programs, international funding support, and partnerships between local transit authorities and global manufacturers are accelerating the procurement of battery-electric buses across metropolitan public transport systems.

Major urban regions such as Johannesburg, Cape Town, and Pretoria represent the most active deployment centers due to established bus rapid transit networks and supportive municipal transport policies. These cities dominate adoption because of stronger infrastructure readiness, higher passenger mobility demand, and municipal sustainability targets. Additionally, international technology providers and electric bus manufacturers collaborate with local transport authorities in these urban centers to introduce charging infrastructure, fleet management systems, and electrified public transportation corridors.

Market Segmentation

By Product Type

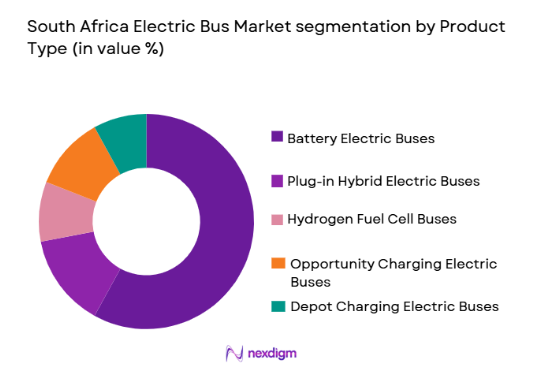

South Africa Electric Bus market is segmented by product type into battery electric buses, plug-in hybrid electric buses, hydrogen fuel cell buses, opportunity charging electric buses, and depot charging electric buses. Recently, battery electric buses has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Battery electric buses are widely adopted because they align with municipal sustainability targets and integrate effectively with existing charging infrastructure deployed in major urban transport corridors. Public transport authorities prefer this technology due to lower operational emissions, reduced fuel dependency, and compatibility with renewable energy integration initiatives. Global manufacturers entering the South African transit market predominantly offer battery electric bus models, strengthening their presence in large municipal fleet tenders. Furthermore, improved battery energy density and declining battery production costs are encouraging transit operators to replace conventional diesel buses with fully electric alternatives across bus rapid transit systems.

By End User

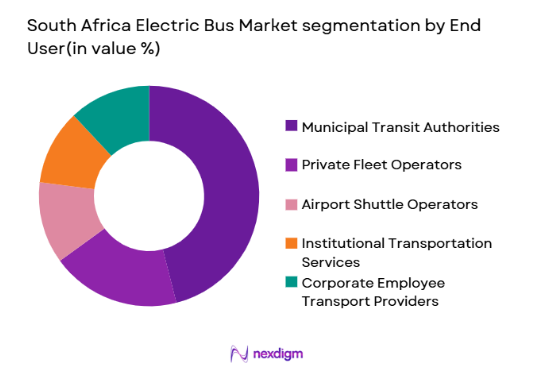

South Africa Electric Bus market is segmented by end user into municipal transit authorities, private fleet operators, airport shuttle operators, institutional transportation services, and corporate employee transport providers. Recently, municipal transit authorities has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Municipal authorities are responsible for large-scale public transportation networks including bus rapid transit corridors, which require high-capacity fleets capable of operating in densely populated urban areas. Electrification strategies introduced by metropolitan municipalities are encouraging procurement of electric buses for sustainable urban mobility programs. Government support programs and green transport initiatives have further strengthened the role of municipal authorities in fleet electrification projects. As a result, large-scale fleet tenders issued by these authorities are shaping procurement volumes, infrastructure investments, and long-term electrification roadmaps for public transportation across major South African metropolitan regions.

Competitive Landscape

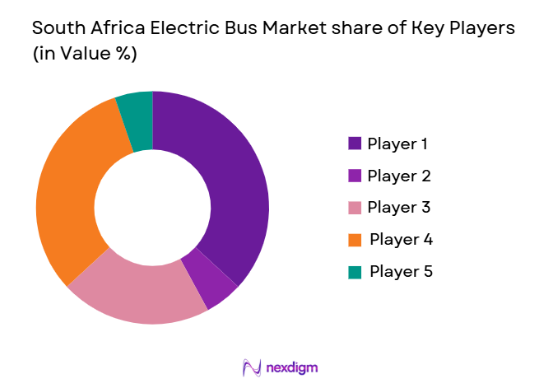

The South Africa Electric Bus Market demonstrates moderate consolidation with global electric bus manufacturers partnering with regional transport operators to deploy electrified fleets. Large international manufacturers dominate early deployments due to their advanced battery technologies and large-scale manufacturing capacity. At the same time, regional vehicle assemblers and transit solution providers collaborate with municipalities to establish localized electric mobility ecosystems. Strategic partnerships, fleet electrification tenders, and charging infrastructure projects are shaping the competitive positioning of major companies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Electrification Projects |

| BYD Company | 1995 | Shenzhen, China | ~ | ~ | ~ | ~ | ~ |

| Yutong Bus | 1963 | Zhengzhou, China | ~ | ~ | ~ | ~ | ~ |

| Volvo Buses | 1928 | Gothenburg, Sweden | ~ | ~ | ~ | ~ | ~ |

| Daimler Buses | 1895 | Stuttgart, Germany | ~ | ~ | ~ | ~ | ~ |

| Solaris Bus & Coach | 1996 | Bolechowo, Poland | ~ | ~ | ~ | ~ | ~ |

South Africa Electric Bus Market Analysis

Growth Drivers

Electric Public Transportation Transition Initiatives:

Governments and municipal transport authorities are prioritizing sustainable mobility strategies aimed at reducing urban pollution and carbon emissions across public transport systems. South Africa’s major metropolitan municipalities have initiated programs to transition diesel-based bus fleets toward electric alternatives within urban transit corridors. Electrification initiatives are supported by climate action commitments and environmental policies encouraging adoption of zero-emission transportation solutions. These initiatives are driving procurement of electric buses through municipal fleet modernization programs and pilot projects. Electric bus deployments are also aligned with national renewable energy expansion programs that support cleaner transportation energy sources. Urban transit operators benefit from lower fuel and maintenance costs associated with electric buses compared with diesel-powered fleets. International financial institutions and development banks are supporting electrified public transport infrastructure through financing programs. These initiatives enable municipalities to procure electric buses and establish charging infrastructure networks required for operational efficiency. As cities continue implementing sustainable mobility frameworks, electric bus adoption is expected to accelerate significantly across major metropolitan transit systems.

Declining Battery Technology Costs and Efficiency Improvements:

Advancements in lithium-ion battery technology have significantly improved the feasibility of electric bus deployments across public transport systems. Battery energy density improvements allow electric buses to operate longer distances while maintaining efficient performance across urban transit routes. Continuous technological innovation in battery management systems also enhances reliability and operational safety of electric bus fleets. As battery production scales globally, manufacturing efficiencies have reduced costs associated with battery packs used in electric buses. These developments are improving the economic viability of electric fleets for transit operators and municipalities. Longer battery life cycles are reducing lifecycle costs associated with fleet electrification programs. Additionally, improved charging technologies allow faster recharging of buses at depots or charging hubs, improving operational scheduling flexibility. Vehicle manufacturers are investing in battery research and modular battery designs that further enhance vehicle range and durability. These technological improvements are strengthening confidence among transit authorities considering large-scale adoption of electric buses across urban mobility networks.

Market Challenges

High Capital Investment Requirements for Electric Bus Deployment:

One of the most significant barriers to electric bus adoption is the high initial capital cost associated with vehicle procurement and supporting infrastructure deployment. Electric buses require advanced battery systems and integrated electric drivetrains that increase manufacturing costs compared with conventional diesel buses. Transit authorities must also invest in charging infrastructure including depot chargers, grid upgrades, and energy management systems. These infrastructure investments require substantial upfront funding before large-scale fleet electrification becomes operationally feasible. Budget constraints faced by municipalities often slow procurement timelines and limit deployment volumes of electric buses. Financing mechanisms such as green loans or public-private partnerships are still evolving in several regions. The high capital cost also creates uncertainty among transit operators regarding long-term financial returns. Additionally, electric bus fleet electrification requires workforce training and operational adjustments that further increase transition costs. These financial challenges continue to influence the pace of adoption across emerging electric bus markets.

Charging Infrastructure and Grid Capacity Limitations:

The development of reliable charging infrastructure remains a critical challenge for large-scale electric bus fleet deployment across metropolitan transit networks. Electric buses require high-capacity charging systems capable of supporting multiple vehicles simultaneously within operational depots. Existing urban electricity grids often require upgrades to handle increased energy demand associated with electric bus charging operations. Grid reliability concerns and energy distribution constraints may affect charging schedules and fleet availability. Infrastructure planning must ensure adequate charging stations are installed along major transit corridors and within bus depots. However, infrastructure deployment requires coordination between municipal authorities, energy providers, and technology suppliers. Delays in infrastructure development can limit the expansion of electric bus fleets across urban transit systems. Transit operators must also consider energy pricing and peak demand charges associated with electricity consumption. Addressing these infrastructure challenges is essential to ensure reliable operation of electric public transportation networks.

Opportunities

Expansion of Zero Emission Public Transport Policies:

National and municipal governments are increasingly implementing policies that encourage the adoption of zero-emission transportation technologies within public mobility systems. Policy frameworks promoting electric vehicles are creating favorable regulatory conditions for electric bus procurement programs. Environmental commitments aimed at reducing urban emissions are encouraging municipalities to transition conventional bus fleets toward electric alternatives. Incentives such as tax benefits, clean mobility grants, and public infrastructure funding are supporting adoption of electric buses. International climate funding programs are also supporting developing economies in electrifying public transport systems. Electric buses align with sustainability targets aimed at improving urban air quality and reducing greenhouse gas emissions. Municipal authorities are increasingly integrating electric bus fleets within long-term sustainable transport plans. As regulatory frameworks evolve to support clean mobility, the electric bus market is expected to experience expanded demand from urban transit systems.

Development of Local Electric Bus Manufacturing Ecosystems:

Establishing local electric vehicle manufacturing capabilities presents a significant opportunity for the electric bus industry in South Africa. Domestic assembly facilities can reduce dependence on imported vehicles while supporting regional industrial development. Local manufacturing initiatives also encourage technology transfer, workforce development, and supply chain expansion within the electric mobility sector. Government incentives aimed at strengthening domestic electric vehicle production can attract international manufacturers to establish assembly operations. Localized production also reduces logistics costs associated with importing fully built electric buses. Additionally, regional manufacturing hubs can support exports of electric buses to neighboring African markets adopting sustainable transportation technologies. Domestic manufacturing partnerships can stimulate innovation in electric powertrain systems, battery technologies, and charging infrastructure development. These developments may strengthen the long-term competitiveness of the electric bus industry within the regional transportation sector.

Future Outlook

The South Africa Electric Bus Market is expected to experience significant transformation driven by urban mobility electrification strategies and sustainability policies. Over the next five years, technological improvements in battery systems, expansion of charging infrastructure, and government-supported clean mobility initiatives will accelerate electric bus adoption. Municipal transit authorities are likely to expand electrified fleets as operational costs decline and environmental regulations strengthen. Partnerships between international manufacturers and local transit agencies will also support large-scale deployment.

Major Players

- BYD Company

- Yutong Bus

- Volvo Buses

- Daimler Buses

- Solaris Bus & Coach

- Tata Motors

- Ashok Leyland

- Zhongtong Bus

- CRRC Electric Bus

- Proterra

- Scania Group

- MAN Truck & Bus

- Irizar e-Mobility

- Golden Dragon Bus

- Anhui Ankai Automobile

Key Target Audience

- Public transportationauthorities

- Electric vehicle manufacturers

- Bus fleet operators

- Automotive component suppliers

- Infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Renewable energy infrastructure providers

Research Methodology

Step 1: Identification of Key Variables

Market variables such as electric bus deployment levels, transit electrification programs, government policies, and infrastructure development were identified to understand the dynamics shaping the South Africa Electric Bus Market.

Step 2: Market Analysis and Construction

Comprehensive evaluation of industry data, transportation infrastructure initiatives, and manufacturer activities was conducted to construct market segmentation, adoption patterns, and competitive positioning within the electric bus ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions were validated through consultation with transportation experts, electric vehicle specialists, and transit authorities involved in electrified mobility initiatives.

Step 4: Research Synthesis and Final Output

All validated insights were consolidated to produce an analytical market report highlighting growth drivers, challenges, opportunities, technological developments, and future outlook for the electric bus industry.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government initiatives promoting zero emission public transportation

Expansion of urban transit electrification programs

Declining battery costs improving electric bus economics

Growing environmental regulations on diesel bus fleets

Integration of renewable energy charging infrastructure - Market Challenges

High upfront acquisition cost of electric bus fleets

Limited charging infrastructure across secondary cities

Grid capacity constraints for large scale depot charging

Dependence on imported battery systems and components

Operational range limitations for long distance routes - Market Opportunities

Development of local electric bus assembly and manufacturing

Adoption of hydrogen fuel cell buses for long route transport

Growth in fleet electrification through leasing and financing models - Trends

Deployment of depot based fast charging infrastructure

Adoption of telematics and battery monitoring systems

Integration of renewable powered charging depots

Expansion of electric bus pilot projects by metropolitan municipalities

Partnerships between OEMs and local transit operators - Government Regulations & Defense Policy

National policies supporting low emission public transportation fleets

Incentives for clean mobility adoption in urban transport systems

Regulatory standards for electric vehicle charging infrastructure - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Buses

Plug-in Hybrid Electric Buses

Fuel Cell Electric Buses

Opportunity Charging Electric Buses

Depot Charging Electric Buses - By Platform Type (In Value%)

Urban Public Transit Buses

Intercity Electric Coaches

Airport Shuttle Electric Buses

School Electric Buses

Corporate and Institutional Shuttle Buses - By Fitment Type (In Value%)

Fully Built Electric Bus Units

Chassis Integrated Electric Bus Platforms

Retrofit Electric Bus Conversions

Modular Electric Bus Platforms

Body on Chassis Electric Bus Assemblies - By EndUser Segment (In Value%)

Municipal Public Transport Authorities

Private Bus Fleet Operators

Airport Transport Service Providers

Educational Institution Transport Fleets

Corporate and Industrial Shuttle Services - By Procurement Channel (In Value%)

Government Tenders and Public Procurement

Direct OEM Procurement Contracts

Public Private Partnership Projects

Transit Authority Framework Agreements

Fleet Leasing and Financing Contracts - By Material / Technology (in Value %)

Lithium Iron Phosphate Battery Technology

Nickel Manganese Cobalt Battery Technology

Solid State Battery Technology

Hydrogen Fuel Cell Powertrain Systems

Advanced Thermal Battery Management Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Battery Capacity Range, Charging Infrastructure Compatibility, Vehicle Range per Charge, Passenger Seating Capacity, Total Cost of Ownership, Local Manufacturing Capability, Energy Efficiency Performance, Warranty and Service Coverage, Fleet Management Integration, Charging Time Duration)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

BYD Company

Yutong Bus

Zhongtong Bus

CRRC Electric Bus

Proterra

Volvo Buses

Daimler Buses

MAN Truck and Bus

Scania Group

Solaris Bus and Coach

Irizar e-mobility

Ashok Leyland

Tata Motors

Golden Dragon Bus

Anhui Ankai Automobile

- Municipal transit authorities increasingly electrifying urban bus fleets

- Private operators adopting electric buses to reduce long term operating costs

- Airport and institutional shuttle services transitioning to zero emission fleets

- Corporate mobility providers integrating electric buses in employee transport

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now