Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The South Africa Electric Two-Wheeler Market demonstrates steady expansion supported by urban mobility shifts and growing environmental policy focus. Based on a recent historical assessment, the market reached approximately USD ~ billion, driven by increasing adoption of electric scooters and motorcycles for short-distance commuting and delivery services. Industry data referenced from the International Energy Agency and national transport transition initiatives highlight the role of rising fuel costs and electrification policies accelerating demand for battery-powered two-wheelers.

Urban mobility adoption is concentrated in metropolitan areas where infrastructure, logistics demand, and consumer awareness are higher. Johannesburg, Cape Town, and Durban represent key centers for electric two-wheeler deployment due to dense urban populations and expanding e-commerce logistics networks. These cities benefit from municipal sustainability strategies, startup mobility platforms, and pilot electrification programs for delivery fleets. Regional dominance is supported by charging infrastructure experimentation and corporate fleet electrification initiatives across South Africa’s major economic hubs.

Market Segmentation

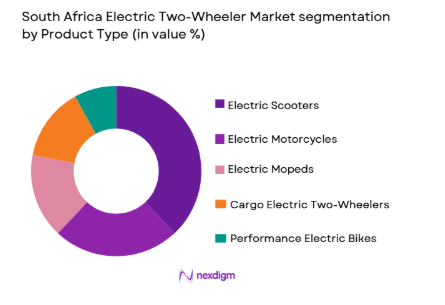

By Product Type

South Africa Electric Two-Wheeler Market market is segmented by product type into electric scooters, electric motorcycles, electric mopeds, cargo electric two-wheelers, and performance electric bikes. Recently, electric scooters has a dominant market share due to factors such as strong demand from urban commuters, affordability relative to electric motorcycles, and compatibility with delivery fleet operations. Scooters offer lightweight mobility solutions suitable for congested urban environments and short-distance travel patterns common in South African cities. Logistics companies increasingly adopt electric scooters for last-mile delivery due to lower operating costs and reduced fuel dependency. Municipal sustainability initiatives and startup micro-mobility platforms have further accelerated adoption, particularly for app-based delivery drivers and gig economy workers. Additionally, scooters require relatively smaller battery packs, reducing purchase costs and enabling easier charging infrastructure deployment in residential or commercial areas.

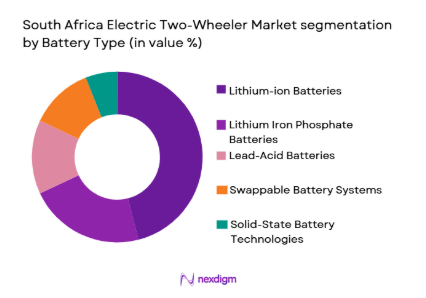

By Battery Type

South Africa Electric Two-Wheeler Market market is segmented by battery type into lithium-ion batteries, lithium iron phosphate batteries, lead-acid batteries, swappable battery systems, and solid-state battery technologies. Recently, lithium-ion batteries has a dominant market share due to factors such as superior energy density, longer lifecycle performance, and compatibility with modern electric vehicle powertrains. Manufacturers prefer lithium-ion chemistry for electric scooters and motorcycles because it provides higher range and improved charging efficiency compared with traditional battery systems. Growing global battery manufacturing capacity and technological innovation have improved reliability and cost structures, encouraging wider adoption in emerging electric mobility markets. Additionally, lithium-ion systems support integration with smart battery management technologies that enhance vehicle safety and operational efficiency. These advantages make lithium-ion battery technology the preferred energy storage solution for both personal commuters and commercial electric mobility fleets.

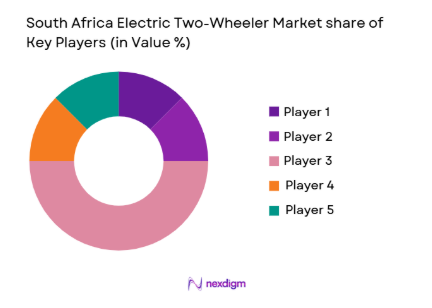

Competitive Landscape

The South Africa Electric Two-Wheeler Market exhibits a moderately fragmented competitive landscape characterized by the presence of international electric mobility manufacturers and emerging regional electric mobility startups. Global brands leverage advanced battery technology, established distribution networks, and research capabilities, while local companies focus on affordability, fleet solutions, and logistics partnerships. Strategic collaborations with delivery platforms and mobility service providers influence competitive positioning. The market is gradually consolidating as technology providers, battery innovators, and vehicle manufacturers form partnerships to accelerate adoption across urban transportation and last-mile logistics sectors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Integration Capability |

| NIU Technologies | 2014 | China | ~ | ~ | ~ | ~ | ~ |

| Vmoto Limited | 1999 | Australia | ~ | ~ | ~ | ~ | ~ |

| Yadea Group | 2001 | China | ~ | ~ | ~ | ~ | ~ |

| Hero Electric | 2007 | India | ~ | ~ | ~ | ~ | ~ |

| Gogoro | 2011 | Taiwan | ~ | ~ | ~ | ~ | ~ |

South Africa Electric Two-Wheeler Market Analysis

Growth Drivers

Urban Last-Mile Delivery Electrification:

Urban logistics and last-mile delivery operations are rapidly transforming transportation demand patterns across South Africa’s major metropolitan areas. E-commerce platforms and food delivery services require cost-efficient and flexible transportation solutions capable of navigating congested urban streets. Electric two-wheelers provide lower operational costs compared with internal combustion engine motorcycles due to reduced fuel consumption and minimal maintenance requirements. Fleet operators recognize that electricity costs remain significantly lower than gasoline prices when calculated per kilometer traveled. This economic advantage encourages delivery companies to transition gradually toward electric scooters and motorcycles within their vehicle fleets. In addition, compact electric two-wheelers enable faster delivery times in dense urban environments where parking availability and traffic congestion create operational barriers for larger vehicles. Environmental considerations also influence fleet decisions because companies increasingly align sustainability goals with electric mobility adoption. Government urban mobility initiatives and pilot electrification projects in metropolitan regions further strengthen adoption momentum. As logistics platforms expand across South Africa, electric two-wheelers are becoming essential infrastructure for efficient urban commerce networks.

Rising Fuel Prices and Urban Commuter Cost Sensitivity:

African consumers are increasingly sensitive to transportation costs due to volatility in fuel prices and rising household expenses. Motorcycles and scooters already represent an affordable transportation option compared with passenger vehicles, and electrification further reduces operating costs. Electric two-wheelers eliminate the need for gasoline purchases, replacing them with lower-cost electricity consumption that significantly reduces commuting expenses. Over time, the savings generated through reduced fuel and maintenance costs offset the initial purchase price of electric mobility vehicles. Urban commuters who travel relatively short distances each day benefit most from this cost advantage, making electric scooters an attractive option. Additionally, battery technology improvements have increased driving range, enabling riders to complete daily travel without frequent charging interruptions. Public awareness regarding air pollution and carbon emissions has also contributed to the appeal of electric mobility solutions among younger consumers. Retail financing programs and emerging electric mobility subscription models further reduce financial barriers to adoption. These economic and environmental factors collectively support sustained demand growth for electric two-wheelers across South Africa.

Market Challenges

Limited Charging and Battery Infrastructure Availability:

Electric mobility expansion in South Africa faces infrastructure challenges related to charging networks and battery ecosystem development. Many urban and suburban areas lack dedicated charging stations designed specifically for electric two-wheelers, which can discourage potential consumers from transitioning away from gasoline-powered vehicles. Without convenient charging access, users may experience range anxiety when considering electric mobility alternatives. Battery swapping networks remain at an early development stage, limiting operational efficiency for commercial delivery fleets that require continuous vehicle availability. Residential charging is possible but depends on access to reliable electricity infrastructure and safe charging facilities. Businesses interested in deploying electric fleets must invest in private charging systems, which increases operational costs during the early stages of market adoption. Furthermore, standardization challenges across battery technologies complicate infrastructure development, as different manufacturers employ distinct charging architectures. Policymakers and energy stakeholders must collaborate to expand electric mobility infrastructure in order to support large-scale market growth. Without coordinated infrastructure development, adoption of electric two-wheelers may progress slower than expected.

High Upfront Vehicle Cost Relative to Conventional Alternatives:

Electric two-wheelers typically require a higher initial purchase price compared with traditional internal combustion engine scooters and motorcycles available in the South African market. Battery technology represents the most expensive component of electric vehicles, significantly influencing retail pricing structures. For price-sensitive consumers, this upfront investment can discourage adoption even though long-term operating costs are lower. Financing solutions for electric mobility products remain limited compared with established vehicle loan programs offered for conventional motorcycles. Import duties and limited local manufacturing capabilities further increase the retail cost of electric two-wheelers in South Africa. Manufacturers must often rely on imported battery packs and electronic components, increasing production expenses and supply chain complexity. Consumer uncertainty regarding battery lifespan and replacement costs also contributes to hesitation during purchasing decisions. Without supportive policy incentives or subsidy programs, many consumers continue to favor lower-priced gasoline scooters despite higher operating costs. Addressing cost barriers through local manufacturing development and innovative financing models will be essential for broader market adoption.

Opportunities

Expansion of Battery Swapping Infrastructure for Urban Fleets:

Battery swapping systems represent a transformative opportunity for the electric two-wheeler ecosystem in South Africa because they dramatically reduce vehicle downtime associated with charging. Instead of waiting for batteries to recharge, riders can exchange depleted batteries for fully charged units at dedicated swap stations. This system is particularly attractive for delivery fleets and ride-sharing operators that require vehicles to remain operational throughout the day. Battery swapping also reduces upfront vehicle costs because batteries can be leased separately from the vehicle itself. As a result, fleet operators gain flexibility in managing energy costs and battery lifecycle maintenance. Technology providers developing standardized battery modules could accelerate ecosystem expansion across multiple vehicle manufacturers. Urban mobility startups and logistics platforms increasingly recognize the efficiency advantages of swappable battery networks. Collaboration between energy companies, vehicle manufacturers, and municipal authorities could establish a scalable battery infrastructure model across major South African cities. If implemented effectively, battery swapping networks could significantly accelerate adoption of electric two-wheelers in commercial and consumer markets.

Localization of Electric Two-Wheeler Manufacturing in South Africa:

Establishing domestic manufacturing capabilities for electric two-wheelers presents a major economic and strategic opportunity for the South African mobility sector. Local production facilities would reduce dependence on imported vehicles and components, lowering overall manufacturing costs and improving supply chain resilience. Governments and industry stakeholders increasingly explore incentives that encourage global electric vehicle manufacturers to establish assembly operations within the country. Local manufacturing could stimulate job creation across multiple sectors including battery assembly, electronics integration, vehicle design, and distribution logistics. Additionally, domestic production enables manufacturers to tailor vehicle designs specifically for regional transportation conditions and consumer preferences. Partnerships between international technology providers and South African automotive firms may accelerate knowledge transfer and industrial capability development. A localized electric vehicle supply chain would also strengthen export potential to neighboring African markets experiencing similar mobility transitions. Over time, domestic manufacturing could reduce vehicle pricing, improve accessibility for consumers, and significantly expand the electric two-wheeler market across the region.

Future Outlook

The South Africa Electric Two-Wheeler Market is expected to expand steadily over the next five years as urban mobility electrification accelerates. Increasing adoption of delivery fleets and urban commuting solutions will drive demand for electric scooters and motorcycles. Technological progress in battery performance, charging efficiency, and vehicle connectivity will enhance product attractiveness. Government sustainability strategies and transportation electrification initiatives are likely to support adoption. Additionally, expanding logistics networks and shared mobility services will further strengthen market growth.

Major Players

- NIU Technologies

- Vmoto Limited

- Yadea Group

- Hero Electric

- Gogoro

- TVS Motor Company

- Bajaj Auto

- Honda Motor Company

- Yamaha Motor Company

- BMW Motorrad

- Silence Urban Ecomobility

- Super Soco

- KYMCO

- Roam Electric

- Daymak

Key Target Audience

- Electric vehicle manufacturers

- Battery technology manufacturers

- Automotive component suppliers

- Urban mobility platform operators

- Logistics and delivery companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Electric charging infrastructure providers

Research Methodology

Step 1: Identification of Key Variables

Researchers identify major variables influencing the South Africa Electric Two-Wheeler Market including vehicle adoption patterns, battery technology trends, policy frameworks, and mobility infrastructure development across urban centers and logistics networks.

Step 2: Market Analysis and Construction

Market structure is analyzed by evaluating product categories, supply chains, technology providers, and demand sectors. Quantitative data and industry indicators are used to construct market size and segmentation models.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions are validated through consultations with electric mobility experts, transportation analysts, and logistics operators. Expert insights help refine demand projections and confirm market drivers and challenges.

Step 4: Research Synthesis and Final Output

Validated data points and qualitative insights are integrated into a structured market report. Final outputs include segmentation analysis, competitive landscape evaluation, and strategic outlook for the South Africa Electric Two-Wheeler Market

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Growing urban congestion driving demand for compact electric mobility

Rising fuel costs encouraging transition toward electric two wheeler transportation

Government initiatives promoting electric mobility adoption in urban logistics

Expansion of e commerce delivery networks requiring cost efficient last mile vehicles

Technological improvements in battery energy density and charging efficiency - Market Challenges

Limited public charging and battery swapping infrastructure across cities

High upfront vehicle costs compared to conventional internal combustion two wheelers

Consumer concerns regarding battery durability and replacement expenses

Limited local manufacturing ecosystem for electric two wheeler components

Import dependency for advanced battery cells and electronic drivetrain systems - Market Opportunities

Expansion of battery swapping networks for urban delivery fleets

Localization of electric two wheeler manufacturing within South Africa

Integration of smart connectivity and fleet management solutions - Trends

Increasing deployment of electric two wheelers in last mile logistics fleets

Growing adoption of battery swapping models for commercial mobility

Entry of international electric scooter manufacturers into African markets

Integration of IoT based telematics in electric mobility platforms

Development of lightweight modular electric vehicle architectures - Government Regulations & Defense Policy

National policies promoting clean mobility and low emission transport adoption

Import duty adjustments encouraging electric mobility technologies

Municipal incentives for electric delivery fleets and shared mobility operators - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Electric Scooters

Electric Motorcycles

Electric Mopeds

Electric Cargo Two Wheelers

High Performance Electric Bikes - By Platform Type (In Value%)

Urban Commuter Mobility Platforms

Shared Micro Mobility Platforms

Delivery and Logistics Platforms

Fleet Mobility Platforms

Personal Mobility Platforms - By Fitment Type (In Value%)

Fully Built Electric Two Wheelers

Retrofit Electric Conversion Kits

Swappable Battery Ready Vehicles

Integrated Smart Connected Vehicles

Modular Platform Based Vehicles - By EndUser Segment (In Value%)

Individual Urban Commuters

Delivery and E Commerce Logistics Operators

Ride Sharing and Micro Mobility Companies

Corporate and Institutional Fleets

Government and Municipal Utility Services - By Procurement Channel (In Value%)

Authorized Dealer Networks

Direct Manufacturer Sales

Online Vehicle Sales Platforms

Fleet Procurement Contracts

Leasing and Subscription Mobility Programs - By Material / Technology (in Value %)

Lithium Ion Battery Powered Vehicles

Lithium Iron Phosphate Battery Systems

Swappable Battery Architecture

Connected Telematics Enabled Vehicles

Lightweight Aluminum Frame Platforms

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Vehicle Range, Battery Capacity, Charging Time, Top Speed, Payload Capacity, Fleet Integration Capability, Battery Swapping Compatibility, Connectivity Features, Pricing Tier, Dealer Network Strength)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

NIU Technologies

Yadea Group

Vmoto Limited

Hero Electric

TVS Motor Company

Bajaj Auto

Honda Motor Company

Yamaha Motor Company

BMW Motorrad

KYMCO

Gogoro

Roam Electric

Daymak

Super Soco

Silence Urban Ecomobility

- Urban commuters increasingly adopting electric scooters for short distance mobility

- Logistics companies integrating electric two wheelers for cost efficient delivery operations

- Shared mobility operators expanding electric micro mobility services in metropolitan areas

- Government and municipal agencies exploring electric mobility solutions for urban services

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now