Download PDF

Download PDFMarket Overview

South Africa Fats and Oil Market is valued at USD ~ billion, based on a five-year historical analysis, and is forecasted to grow at a CAGR of ~% during the forecast period. Demand is driven by sunflower oil, canola oil, soybean oil, palm oil, margarine, baking fats, foodservice frying oils, and packaged retail oils. South Africa crushed 2.6 MMT of oilseeds after lower production, while GDP reached USD 401.14 billion and GDP per capita reached USD 6,267.2. Gauteng, KwaZulu-Natal, Western Cape, Free State, North West, Mpumalanga, and Durban-linked import corridors dominate South Africa Fats and Oil Market due to household consumption density, sunflowerseed production, canola processing, food manufacturing, retail concentration, port logistics, and QSR demand. Sunflowerseed production stood at 632,000 MT before rising to 770,000 MT, while rapeseed output increased from 236,000 MT to 288,000 MT, strengthening domestic crushing and refining clusters.

Market Segmentation

By Product Type

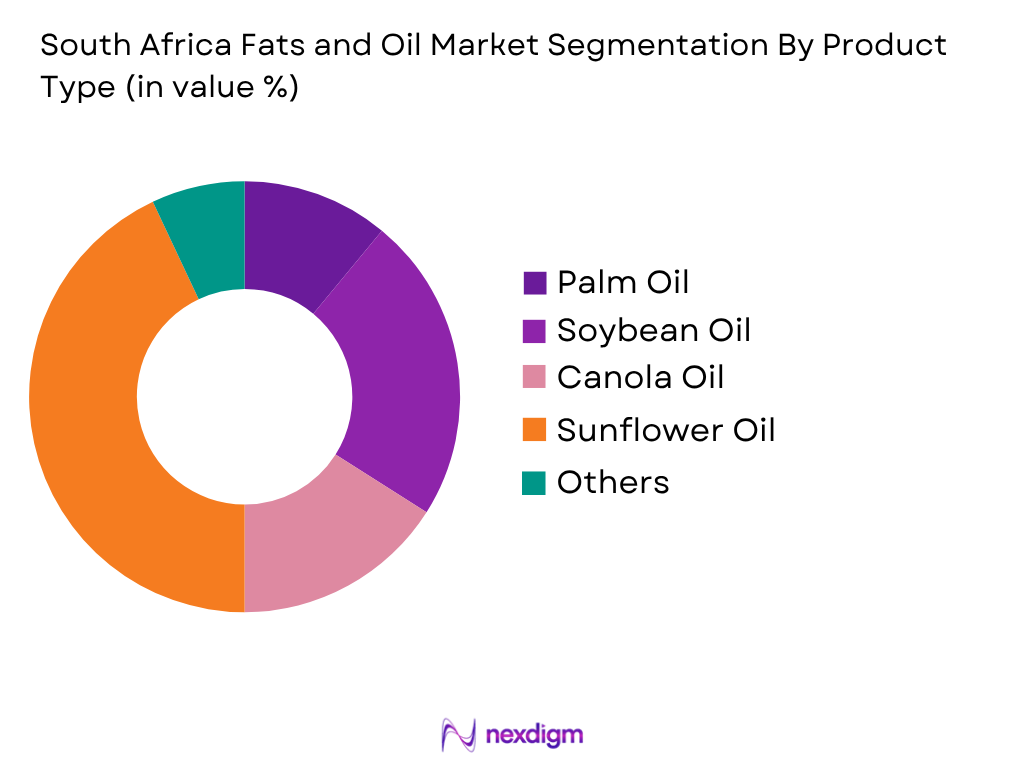

South Africa Fats and Oil Market is segmented by product type into sunflower oil, canola oil, soybean oil, palm oil, palm olein, palm kernel oil, corn oil, olive oil, coconut oil, blended vegetable oils, butter, dairy fats, margarine, spreads, shortening, baking fats, beef tallow, poultry fat, lard, and specialty fats. Recently, sunflower oil has had the dominant market share under the product type segmentation because it is deeply embedded in household cooking, deep-frying, township food preparation, fast food, and supermarket packaged oil baskets. Sunflower oil benefits from domestic seed production, local crushing capacity, consumer familiarity, neutral taste, and broad retail availability. Canola oil is gaining share through health positioning, especially in Western Cape-linked brands, while palm oil is important in bakery fats, margarine, confectionery, and industrial applications. However, sunflower oil remains the structural anchor because it connects farm production, crushing, refined retail packs, informal retail, and foodservice frying demand.

By Distribution Channel

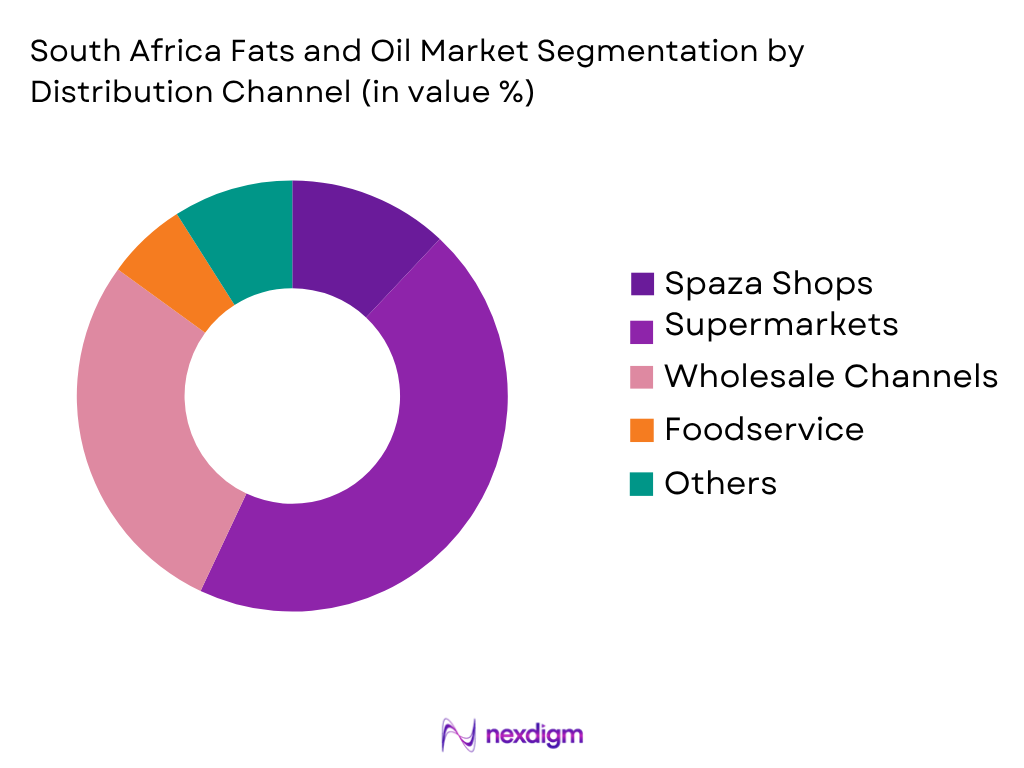

South Africa Fats and Oil Market is segmented by distribution channel into supermarkets and hypermarkets, independent grocery stores, wholesale and cash-and-carry channels, spaza shops and informal retail, convenience stores, online grocery, foodservice distributors, hotel and catering suppliers, industrial ingredient suppliers, commodity traders, and regional export channels. Recently, supermarkets and hypermarkets have had the dominant market share under the distribution channel segmentation because edible oil is a high-frequency grocery staple purchased in planned household baskets. Large retail chains offer sunflower oil, canola oil, blended oils, margarine, butter, olive oil, and private-label formats in multiple pack sizes. Supermarkets also drive price promotions, bulk family packs, and private-label penetration. Spaza shops and cash-and-carry channels remain essential for township and informal retail demand, while foodservice distributors serve restaurants, QSR chains, catering firms, bakeries, and hotels. However, supermarkets dominate value visibility because they combine national reach, promotions, branded assortment, and packaged oil replenishment.

Competitive Landscape

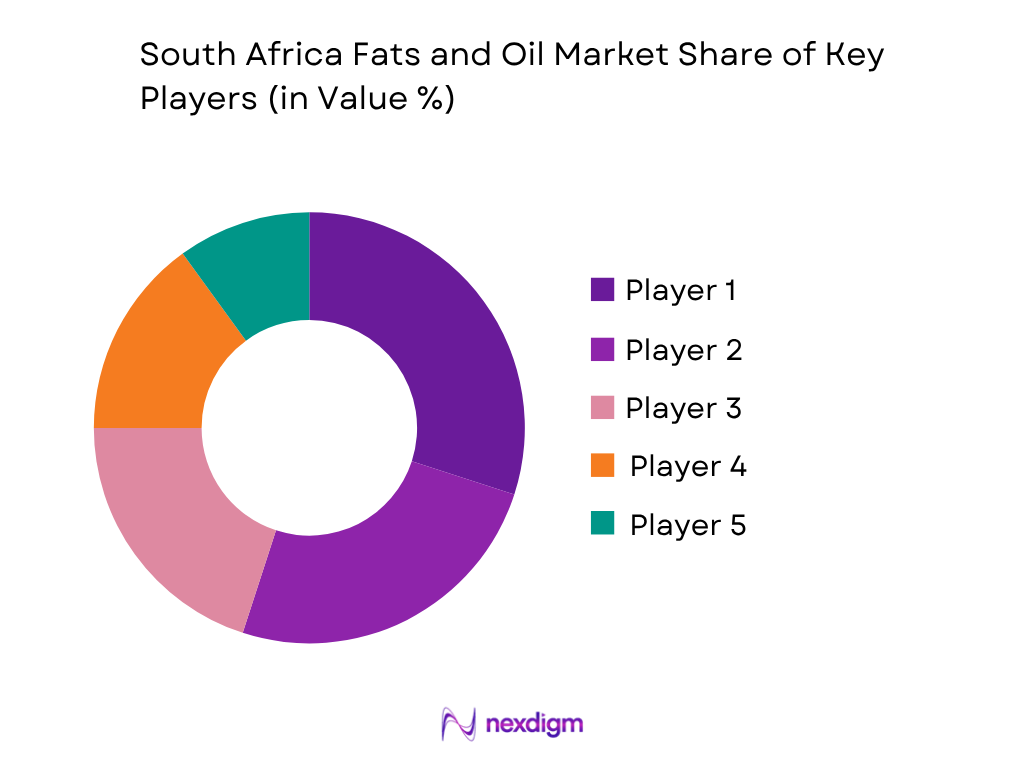

South Africa Fats and Oil Market is led by integrated edible oil processors, sunflowerseed crushers, canola oil specialists, FMCG groups, margarine and baking fat producers, and industrial ingredient suppliers. Willowton Group, Wilmar Continental Edible Oils and Fats, Southern Oil, Tiger Brands, and RCL Foods are key players due to brand strength, domestic processing, retail distribution, foodservice supply, and industrial fat capability. Competition is shaped by sunflower oil availability, canola positioning, supermarket listings, informal retail reach, bulk oil supply, margarine portfolios, and certification-led differentiation. Willowton’s portfolio includes Sunfoil, Wooden Spoon, D’lite and Sunshine D, while Southern Oil positions B-well canola oil around cholesterol-free, Omega 3 and non-GMO canola attributes.

| Company | Establishment Year | Headquarters | Core Portfolio | Processing Strength | Key End Users | Channel Strength | Certification / Health Focus | Market-Specific Advantage |

| Willowton Group | 1970 | Pietermaritzburg, South Africa | ~ | ~ | ~ | ~ | ~ | ~ |

| Wilmar Continental Edible Oils and Fats | 1990s operating base | Randfontein, South Africa | ~ | ~ | ~ | ~ | ~ | ~ |

| Southern Oil | 1993 | Swellendam, South Africa | ~ | ~ | ~ | ~ | ~ | ~ |

| Tiger Brands | 1921 | Johannesburg, South Africa | ~ | ~ | ~ | ~ | ~ | ~ |

| RCL Foods | 1960 | Durban, South Africa | ~ | ~ | ~ | ~ | ~ | ~ |

South Africa Fats and Oil Market Analysis

Growth Drivers

Domestic Sunflowerseed, Soybean and Rapeseed Crushing Base

Domestic oilseed crushing is a core growth driver for the South Africa Fats and Oil Market because sunflower oil, soybean oil, canola oil, oilcake, margarine fats, baking fats and foodservice frying oils are supported by local crop-processing capacity. USDA FAS reports South Africa’s oilseed processing capacity at 2.8 MMT, with facilities dedicated to soybeans and sunflowerseed and some plants able to switch between both crops. The same source reports soybean production moving from 1.848 MMT to 2.390 MMT, sunflowerseed production from 632,000 MT to 770,000 MT, and rapeseed production from 236,000 MT to 288,000 MT, creating feedstock for crushers, refiners and retail oil brands. World Bank data records South Africa’s GDP at USD 401.14 billion, GDP per capita at USD 6,267.2 and GDP growth at 0.5, confirming a large but low-growth economy where essential cooking staples remain structurally important. The market impact is direct because refined sunflower oil dominates household cooking and deep-frying, while canola oil supports health-positioned retail oils and soybean oil supports food manufacturing and blended oils.

Foodservice, Informal Retail and Packaged Household Oil Demand

Foodservice and informal retail demand drive the South Africa Fats and Oil Market because sunflower oil, palm olein, canola oil, margarine, shortening, baking fats, tallow and blended frying oils are used across QSRs, fish-and-chip shops, township vendors, bakeries, supermarkets, spaza shops and cash-and-carry outlets. South Africa’s population scale supports recurring cooking oil consumption, with IMF listing the country population at 63.97 million and World Bank recording GDP per capita at USD 6,267.2. USDA FAS notes that sunflowerseed is primarily used for edible oil production, while sunflower meal is sold into animal feed, showing the linkage between edible oil refining and broader agri-processing. Rapeseed processing capacity is around 250,000 MT annually, supporting canola oil, premium retail oils and foodservice use. The same USDA report indicates South Africa crushed 2.6 MMT of oilseeds, linking household cooking oils and industrial fats to domestic processing. The driver is market specific because South African retail demand depends on high-frequency pantry replenishment, family-size packs, private-label oils, township affordability and bulk frying applications in restaurants and informal food outlets.

Market Challenges

Oilseed Crop Volatility and Supply Balancing Pressure

Oilseed crop volatility is a major challenge for the South Africa Fats and Oil Market because domestic sunflower oil, canola oil and soybean oil supply depends on seasonal production, crushing availability, crop quality, and substitution between imported and locally processed oils. USDA FAS reports sunflowerseed production at 632,000 MT before rising to 770,000 MT and rapeseed production at 236,000 MT before rising to 288,000 MT, showing the scale of crop movement that processors must manage. Soybean output is reported at 1.848 MMT before rising to 2.390 MMT, which improves crushing feedstock but also creates balancing needs across meal, crude oil, refined oil and export channels. World Bank records South Africa’s GDP growth at 0.5 and GDP at USD 401.14 billion, reflecting a restrained economic environment where food-price sensitivity can limit easy pass-through of supply shocks. This challenge is specific to fats and oils because a short sunflowerseed crop can affect refined sunflower oil availability, private-label pricing, spaza-pack supply, QSR frying oil procurement and bakery-fat input planning.

Import Exposure, Infrastructure Constraints and Processing Reliability

Import exposure and infrastructure constraints restrain the South Africa Fats and Oil Market because palm oil, palm kernel oil, selected soft oils, olive oil, coconut oil and specialty fats depend on external supply, while domestic refining and distribution depend on reliable electricity, port logistics, tank storage, road freight and food-grade warehousing. USDA FAS states that South Africa’s soybean oil and sunflower oil imports are expected to remain flat across recent marketing years, while palm-based oils remain important for margarine, shortening, bakery fats, confectionery and frying applications. World Bank data records South Africa’s GDP at USD 401.14 billion, GDP per capita at USD 6,267.2 and unemployment as a key national indicator, while the IMF lists projected real GDP change at 1.0 for 2026 and population at 63.97 million. These macro indicators signal a large consumer base but limited growth cushion for processors and retailers facing energy, freight and import disruptions. The restraint is market specific because edible oil firms must maintain continuous refining, bottling, labelling, certification, bulk delivery and shelf replenishment across supermarkets, spaza channels, foodservice buyers and industrial manufacturers.

Market Opportunities

Canola Oil Premiumization and Health-Positioned Retail Expansion

Canola oil premiumization creates a future growth opportunity for the South Africa Fats and Oil Market because canola is positioned as a health-oriented edible oil for households, foodservice kitchens and packaged food users seeking lower saturated fat profiles and neutral cooking performance. USDA FAS identifies rapeseed primarily as an edible oil crop and reports rapeseed production rising from 236,000 MT to 288,000 MT, with rapeseed processing capacity around 250,000 MT annually. This supports local canola crushing, refined canola oil, oilcake by-products and premium retail packs linked to the Western Cape crop base. World Bank data records GDP per capita at USD 6,267.2 and population-linked household demand through a large national consumer base, while IMF lists South Africa’s population at 63.97 million. These numbers support a broad addressable market for health-positioned oils even in a price-sensitive environment. The opportunity is market specific because canola oil can be developed across retail bottles, private-label premium tiers, bakery applications, foodservice frying blends, plant-based spreads and trans-fat-compliant industrial fats.

Regional Export, Foodservice Oil Management and Industrial Fat Innovation

Regional exports, foodservice oil management and industrial fat innovation create future growth opportunities for the South Africa Fats and Oil Market because the country has a domestic crushing base, established retail brands, foodservice buyers and access to neighboring SADC markets. USDA FAS reports that South Africa’s oilseed exports serve destinations including Zimbabwe, Vietnam, Kenya, Eswatini, Botswana and Mozambique, showing regional trade relevance when domestic supply allows. The same report records total oilseed processing capacity at 2.8 MMT and crushed oilseed volume at 2.6 MMT, giving processors a base for refined oils, oilcake, margarine fats, shortening and frying blends. World Bank data records GDP at USD 401.14 billion and GDP per capita at USD 6,267.2, while IMF lists 2026 projected real GDP change at 1.0, pointing to a market where companies need value-added growth rather than relying only on volume expansion. The opportunity is specific to fats and oils because suppliers can offer high-stability frying oils, fryer-management support, trans-fat-compliant bakery fats, palm-based specialty fats, small-pack township oils and regional export packs.

Future Outlook

South Africa Fats and Oil Market is expected to expand steadily during the forecast period, supported by sunflower oil household demand, canola oil health positioning, foodservice frying requirements, private-label retail growth, bakery and margarine consumption, and informal retail penetration. Sunflower oil will remain central because it is familiar, affordable, locally processed, and widely used in deep-frying and everyday cooking. Domestic oilseed supply will remain a decisive factor. USDA FAS estimates soybean production rising from 1.848 MMT to 2.390 MMT, sunflowerseed output rising from 632,000 MT to 770,000 MT, and rapeseed output rising from 236,000 MT to 288,000 MT. This supports domestic crushing, edible oil production, oilcake supply, and retail pack availability. Foodservice and QSR demand will continue to support bulk frying oils and high-stability blends. Fast-food outlets, fish-and-chip shops, township vendors, hotels, catering firms, and restaurant chains require oils with consistent fry life, neutral flavor, smoke-point stability, and reliable supply. Suppliers that provide bulk packs, drums, filtration guidance, delivery reliability, and certification documentation will be better positioned.

Canola oil will gain relevance in health-positioned retail and foodservice applications. Southern Oil highlights B-well oils as cholesterol-free, high in Omega 3, and made from non-GMO canola seeds, which reflects the broader opportunity for differentiated fats and oils positioned around wellness and provenance. The market will remain exposed to affordability pressure, load-shedding-related processing risk, crop volatility, imported palm oil exposure, currency movement, and retail price competition. Companies with integrated crushing, diversified oil portfolios, flexible sourcing, informal retail reach, and value-pack strategy will have stronger resilience.

Major Players

- Willowton Group

- Wilmar Continental Edible Oils and Fats

- Southern Oil

- Tiger Brands

- RCL Foods

- Epic Foods

- Africa Sun Oil Refineries

- Amanah Oil

- CEOCO

- Goldenglo

- Sime Darby Oils South Africa

- Unilever South Africa

- FR Waring Holdings

- Lactalis South Africa

- Ladismith Cheese

Key Target Audience

- Edible Oil Manufacturers

- Oilseed Crushers and Refiners

- Food Processing Companies

- Foodservice and QSR Operators

- Supermarket, Wholesale and Private Label Buyers

- Spaza and Informal Retail Distributors

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Department of Agriculture Land Reform and Rural Development, Department of Health South Africa, South African Revenue Service, National Consumer Commission, South African Bureau of Standards)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the South Africa Fats and Oil Market. This includes oilseed farmers, crushers, refiners, importers, renderers, supermarket buyers, wholesalers, spaza distributors, foodservice suppliers, industrial ingredient buyers, and regulators. The objective is to identify variables such as product type, source, application, channel, pack format, regional demand, and import exposure.

Step 2: Market Analysis and Construction

In this phase, historical data is compiled and analyzed for the South Africa Fats and Oil Market. The assessment covers sunflowerseed output, soybean crushing, rapeseed processing, refined oil supply, retail packaged oils, foodservice frying oils, margarine, baking fats, animal fats, and imported palm-based ingredients. Top-down validation uses crop, trade, and macroeconomic datasets, while bottom-up validation uses SKU mapping and channel checks.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted interviews with crushers, refiners, packaged oil brands, retail category managers, foodservice distributors, spaza wholesalers, bakery ingredient suppliers, and industrial food manufacturers. These consultations provide operational insights into sourcing, processing, pack-size movement, price sensitivity, substitution behavior, informal trade, certification, and product positioning.

Step 4: Research Synthesis and Final Output

The final phase integrates desk research, primary interviews, retail audits, trade mapping, supply-chain analysis, and competitive benchmarking into a consolidated market model. Supplier inputs are compared with observed shelf presence, bulk oil movement, crop availability, foodservice procurement, and industrial fat usage. The final output provides a validated view of market size, segmentation, competition, future outlook, and strategic implications.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Edible Fats and Oils Classification, Vegetable Oil and Animal Fat Inclusion Criteria, Packaged Cooking Oil vs Bulk Oil Inclusion Criteria, Sunflower Oil and Canola Oil Supply Mapping, Palm Oil and Soft Oil Import Assessment, Domestic Crushing and Refining Capacity Assessment, Retail vs Foodservice vs Industrial Demand Mapping, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, SAGIS Oilseed Supply-Use Validation, DALRRD Crop and Trade Assessment, Retail SKU Audits, Distributor and Foodservice Channel Interviews, Industrial Ingredient Buyer Interviews, Primary Industry Interviews, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Business Cycle and Seasonal Demand Pattern

- Sunflowerseed Crushing and Refining Value Chain Analysis

- Growth Drivers (Sunflower Oil Household Demand, Canola Oil Health Positioning, Domestic Oilseed Crushing Base, Foodservice and QSR Frying Demand, Bakery and Margarine Manufacturing, Informal Retail Penetration, Private Label Expansion, Regional Export Potential, Halaal and Kosher Certified Product Demand)

- Market Challenges (Oilseed Crop Volatility, Sunflowerseed Supply Constraints, Import Dependence for Palm and Specialty Oils, Exchange Rate Exposure, Food Inflation Pressure, Load-Shedding Impact on Processing, Retail Price Competition, Informal Retail Distribution Complexity, Compliance with Trans Fat and Food Safety Standards)

- Market Opportunities (Canola Oil Premiumization, Cold-Pressed and Health Oils, Foodservice Frying Oil Management, Private Label Cooking Oils, Sustainable Palm Oil Sourcing, Township Retail Pack Optimization, Bakery and Confectionery Specialty Fats, Regional SADC Export Growth, Used Cooking Oil Collection)

- Market Trends (Shift Toward Branded Sunflower Oil, Growth of Canola-Based Health Oils, Private Label Retail Expansion, Palm-Based Industrial Fat Use, High-Stability Frying Oil Adoption, Trans-Fat-Compliant Bakery Fats, Informal Retail Small-Pack Demand, Premium Olive Oil Growth, Halaal and Kosher Certification Visibility)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Product Type (In Value %)

Sunflower Oil

Canola Oil

Soybean Oil

Palm Oil

Palm Olein

Palm Kernel Oil

Poultry Fat - By Source Type (In Value %)

Vegetable Oils

Animal-Based Fats

Dairy-Based Fats

Blended Oils and Fats

Domestic Oilseed-Based Oils - By Application (In Value %)

Household Cooking and Retail Consumption

Foodservice Frying and Cooking

Bakery and Confectionery

Snack Food Processing

Packaged Food Manufacturing

Margarine and Spread Manufacturing

Meat Processing

QSR and Fast Food Frying

Hotels, Restaurants and Catering

Animal Feed

Oleochemicals

Cosmetics and Personal Care Ingredients

Export and Regional Trade - By Distribution Channel (In Value %)

Supermarkets and Hypermarkets

Independent Grocery Stores

Wholesale and Cash-and-Carry Channels

Spaza Shops and Informal Retail

Convenience Stores

Online Grocery and E-Commerce - By Region (In Value %)

Gauteng

Western Cape

KwaZulu-Natal

Eastern Cape

Free State

Mpumalanga

- Market Share of Major Players (By Value, Volume, Product Type, Application, Channel, Source Type)

- Competitive Positioning Matrix (Sunflower Oil Portfolio Strength, Domestic Crushing Capacity, Canola Oil Positioning, Retail Distribution Reach, Informal Retail Penetration, Foodservice Bulk Supply, Industrial Fat Capability, Certification Coverage)

- Cross Comparison Parameters (Sunflower Oil Brand Strength, Domestic Oilseed Crushing Capacity, Canola Oil Portfolio Strength, Margarine and Baking Fat Capability, Supermarket and Wholesale Distribution Reach, Informal Retail and Spaza Penetration, Foodservice Bulk Oil Capability, Halaal and Kosher Certification Coverage)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Willowton Group

Wilmar Continental Edible Oils and Fats

Southern Oil

Tiger Brands

RCL Foods

Epic Foods

Africa Sun Oil Refineries

Amanah Oil

CEOCO

Goldenglo

Sime Darby Oils South Africa

Unilever South Africa

FR Waring Holdings

Lactalis South Africa

Ladismith Cheese

- Household Consumption Behavior Assessment

- Regional Oil Preference Assessment

- Foodservice Demand Assessment

- Industrial Food Manufacturer Demand Assessment

- Health and Wellness Influence on Purchase Decisions

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now