Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The South Africa insect repellent market is valued at an estimated USD ~ million in 2024 according to regional insect repellent estimates that break down the Middle East & Africa market by country. This market reflects the total revenue generated from personal and household insect repellent products across formal distribution channels in South Africa. Market growth is driven by heightened consumer awareness of insect‑borne diseases such as malaria and dengue, strong demand for both chemical and natural repellents, and increasing product innovation in sprays, lotions, and plug‑ins that address diverse protection needs. Sales are reinforced by widespread outdoor activities, tourism in wildlife areas, and growing preference for eco‑friendly formulations tailored to personal protection.

Key urban and peri‑urban centers such as Johannesburg, Cape Town, Durban, and Pretoria dominate insect repellent consumption due to higher population density, stronger retail infrastructure, and greater awareness of vector exposure across outdoor, leisure, and tourism contexts. These cities serve as major tourism and travel hubs, with South Africa recording 8.92 million international tourist arrivals in 2024, an increase from 2023, which drives seasonal demand for protective products particularly in lifestyle, hospitality, and travel retail channels. Accessibility via supermarkets, pharmacies, and expanding e‑commerce platforms in these metros supports broader consumer uptake. Tourism growth also stimulates demand as visitors and residents seek reliable protection against mosquito and insect nuisance during travel and outdoor exploration.

Market Segmentation

By Insect Type

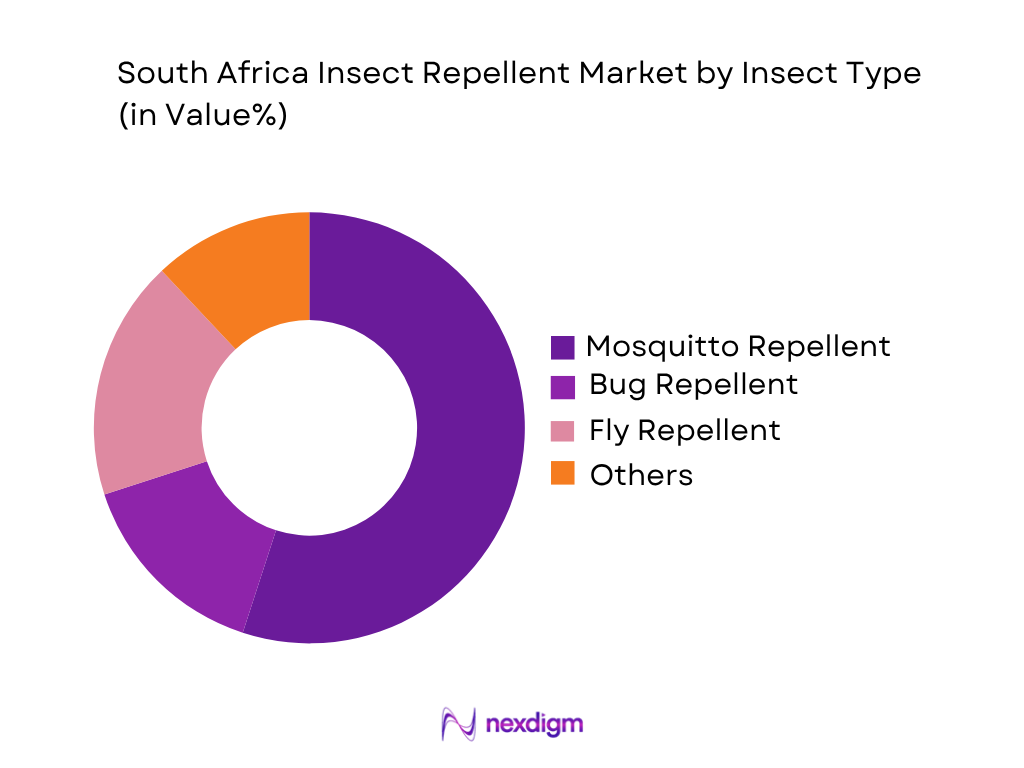

The South Africa insect repellent market segmented by insect target shows mosquito repellents leading the share. Mosquito‑specific products dominate because mosquito‑borne illnesses such as malaria remain a significant public health concern in many regions of South Africa, especially in subtropical and rural areas. Mosquito repellents also benefit from wider product availability across multiple formats, including sprays, lotions, patches, and plug‑in devices, making them a go‑to choice for both personal protection and household use. Additionally, consumer perceptions of mosquito threats—heightened by media and tourism‑related health advisories—translate into higher product trial and repeat purchase relative to fly or general pest formats, which are viewed as supplementary rather than primary protective products. Innovation in long‑lasting formulas and natural alternatives further expands the appeal of mosquito‑targeted repellents.

By Product Format

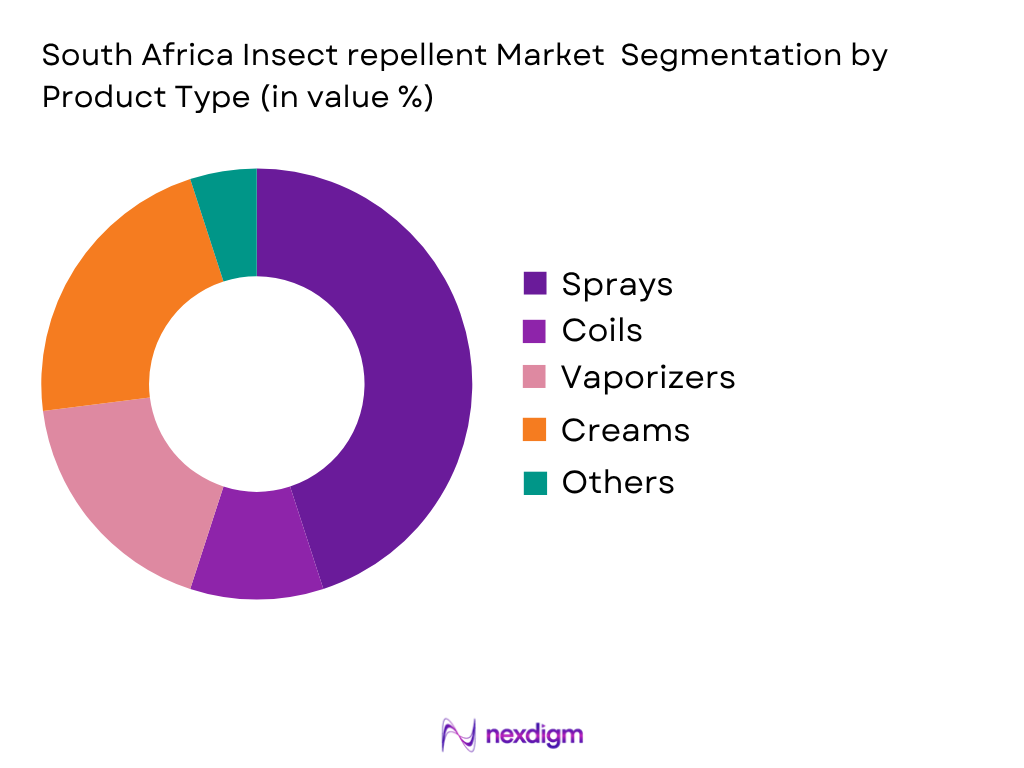

Among product formats in South Africa, sprays and aerosols are the most widely adopted segment, driven by consumer familiarity, perceived effectiveness, and convenience of application for rapid coverage. Sprays provide flexible use cases across personal, residential, and travel scenarios, capturing loyalty among both urban and rural consumers. Creams and lotions also maintain notable share due to skin‑friendly formulations and preference among families and sensitive users who avoid aerosol chemicals. Electric vaporizers and plug‑ins support household usage, especially in coastal and high‑mosquito zones, while wearable patches/bands appeal to outdoor recreation enthusiasts and travelers seeking hands‑free solutions. Retail availability through supermarkets, pharmacies, and digital channels further reinforces the distribution and consumption of sprays relative to other formats.

Competitive Landscape

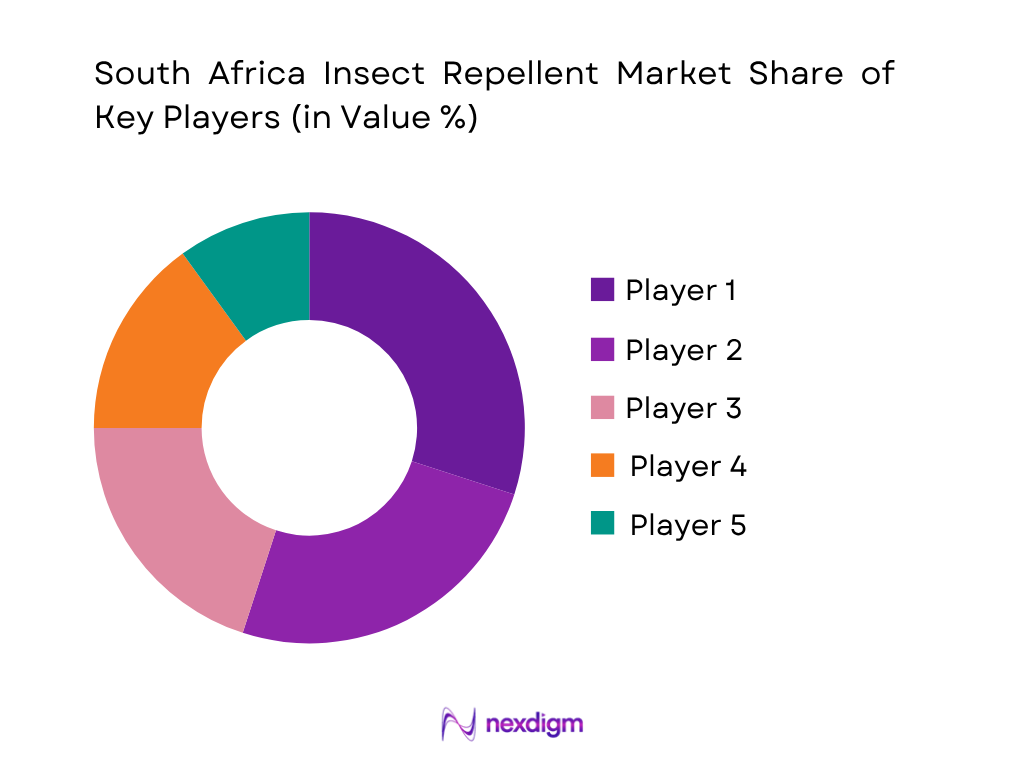

The South Africa insect repellent market exhibits moderate competitive concentration with both global consumer brands and regional distributors shaping product portfolios and distribution channels. Key companies differentiate through product innovation, ingredient focus, and channel partnerships to address consumer protection and convenience demands.

| Company | Establishment | Headquarters | Product Portfolio Breadth | Active Ingredient Diversity | Retail Coverage | Channel Penetration | Safety / Certification Focus | R&D Innovation |

| Reckitt Benckiser | 1823 | UK | ~ | ~ | ~ | ~ | ~ | ~ |

| SC Johnson | 1886 | US | Broad | Medium | National | Multi‑channel | Moderate | Moderate |

| Godrej Consumer Products | 1897 | India | ~ | ~ | ~ | ~ | ~ | ~ |

| Henkel AG | 1876 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Johnson & Johnson | 1886 | US | ~ | ~ | ~ | ~ | ~ | ~ |

South Africa Insect Repellent Market Analysis

Growth Drivers

Rising Inbound Travel and Domestic Mobility Increasing Exposure to Vector Environments

South Africa’s insect repellent demand is substantially supported by significant inbound travel and domestic mobility, which correlates with increased exposure to environments where insect‑borne diseases are prevalent. According to the South African Department of Home Affairs, international arrivals reached approximately 8 937 000 visitors in 2024, a rise over recent tourism figures, reflecting strong global interest in South Africa as a leisure and business destination. Concurrently, domestic travel activity remains high with millions of South Africans engaging in inter‑provincial travel annually, particularly to wildlife and coastal zones such as Kruger National Park, KwaZulu‑Natal beaches, and Eastern Cape reserves where mosquito and biting insects are part of the natural ecosystem. South African government tourism data also highlights that travel receipts approached USD 7 billion, signaling robust overall human mobility. The combination of expanding international arrivals, strong domestic recreation movement, and popular outdoor experiences in subtropical regions directly amplifies the need for personal insect protection products. Increased awareness of conditions like malaria in northeastern provinces drives consumer purchase of repellents for travel preparedness, outdoor comfort, and daily protection in higher‑risk environments, tying broader mobility trends to market demand growth.

High Urban Population and Health Awareness Supporting Preventive Consumer Behavior

Urbanization and health awareness form a foundational driver for insect repellent adoption in South Africa’s major cities. The World Bank reports that approximately 67 percent (about 40 million people) of South Africa’s population lived in urban areas in 2024, with a significant concentration in Johannesburg, Cape Town, Durban, and Pretoria. These urban centers host dense living environments, active outdoor leisure activities, and retail ecosystems that accelerate consumer access to protective products. South Africa’s National Department of Health reported over 3 million outpatient visits related to mosquito‑borne discomfort and allergic reactions in 2024, indicating notable concern among urban populations regarding insect exposure. Educational campaigns delivered through municipal health departments amplify awareness of mosquito management, leading consumers to proactively purchase repellents for evening outdoor socialization and residential use. Government public health bulletins also stress preventive measures in peri‑urban regions bordering conservation areas, reinforcing insect repellent usage as part of everyday health habits. Coupled with robust retail reach—over 7 000 formal pharmacies and personal care outlets across the country—urban health consciousness directly supports regular repellent consumption. These factors illustrate how concentrated population hubs and consumer understanding of vector risks promote market expansion across personal protection categories.

Challenges

Seasonal Vector Patterns Creating Demand Fluctuation and Supply Chain Variability

One of the most significant challenges facing the South Africa insect repellent market is seasonal demand fluctuation driven by climatic and vector activity patterns, which affects inventory planning and supply chain optimization. South Africa’s climatic zones vary from temperate regions in the southwest to subtropical conditions in the northeast, where mosquito populations intensify after rainfall and warmer months. The South African Weather Service records that average rainfall in subtropical regions exceeded 800 millimeters annually, with pronounced peaks in summer periods, which historically align with higher insect breeding. These seasonal spikes lead to concentrated purchasing during peak months and slower turnover in cooler or drier intervals, creating volatility for manufacturers and distributors. Retail analytics further indicate that inventory turnover rates for repellent products can vary by as much as 200 percent between peak and off‑peak months, forcing supply chain inefficiencies such as overstocking and wastage in slow seasons or stockouts during demand surges. Moreover, regional disparities in climate mean that demand forecasting models must account for micro‑climate data across provinces such as KwaZulu‑Natal, Limpopo, and Eastern Cape. Failure to accurately predict these variable patterns increases logistical costs and places pressure on pricing stability and distributor confidence.

Regulatory and Compliance Framework Increasing Time to Market and Label Requirements

The regulatory landscape governing insect repellent products imposes compliance requirements that challenge swift product launches and formulation diversity. In South Africa, the Department of Agriculture, Forestry and Fisheries (DAFF) regulates the approval of biocidal and pesticidal claims associated with insect repellent products, mandating rigorous testing and registration for active ingredients offering insect‑repellency. As of mid‑2026, DAFF’s published register lists over 1 200 active ingredient submissions pending or under review for pest management and repellency effect, reflecting a backlog that can slow market entry for new formulations and botanical alternatives. Additionally, the South African Health Products Regulatory Authority (SAHPRA) requires detailed ingredient disclosure and safety assessments for consumer products marketed for personal protection, extending time‑to‑market for innovation or natural‑based offerings that deviate from established synthetic profiles. These procedural demands require manufacturers to allocate substantial technical resources to comply with label claims regulation, safety data submission, and post‑market surveillance. Small and medium enterprises, in particular, face capital constraints while meeting these administrative obligations, which can deter broader competition and delay the introduction of differentiated products. The cumulative impact of regulatory compliance lengthens cycle times for new repellent introductions and elevates upfront development costs within the market ecosystem.

Opportunities

Expansion of Natural and Botanical Repellent Segment Driven by Consumer Health Preferences

A significant opportunity within the South Africa insect repellent market lies in the expansion of natural and botanical formulations, which resonate with growing health‑conscious consumer segments. South African consumer health surveys conducted by Statistics South Africa indicate that over 48 percent of adults reported a preference for products labeled “natural” or “plant‑based” across personal care categories in 2024, reflecting a strong shift toward ingredient transparency and perceived safety. This preference extends into vector protection, where botanicals such as citronella, lemon eucalyptus, and neem are gaining traction as alternatives to traditional chemical repellents. This trend is reinforced by urban wellness movements in key metropolitan zones—Johannesburg, Cape Town, Pretoria—where demand for eco‑friendly and skin‑gentle products is notably high. Retail audit data shows that botanical repellent SKUs in pharmacy chains have grown their shelf presence by over 150 positions nationally in the past two sales cycles, indicating retailer response to consumer demand. Additionally, partnerships with outdoor travel and safari tour operators highlight a premium placement opportunity, as eco‑tourism guests seek repellents aligning with sustainability values. The alignment between consumer health preferences and sustainable product narratives presents a compelling growth avenue for brands willing to invest in botanical formulation R&D and certification, positioning them to capture an expanding niche within the broader protection market.

Increasing Outdoor Tourism and Recreational Activities Supporting Broader Demand

South Africa’s vibrant outdoor tourism and recreational sector creates a salient opportunity for insect repellent adoption across diverse consumer segments. Tourism and hospitality data from South African Tourism reveal that total tourism expenditure reached USD 7 billion in 2024, supported by 8 937 000 international arrivals. Nature reserves, wildlife experiences, and coastal recreational spaces attract both domestic and global visitors, who frequently require protective products against biting insects in outdoor settings. Furthermore, public recreation data from the Department of Sports, Arts and Culture indicates that participation in outdoor sports and organized activities—such as hiking, camping, and coastal beach events—involves more than 5 million adult engagements annually. These documented activities translate into natural touchpoints where insect repellents become essential for comfort and safety, particularly in parks and reserves where mosquito habitats are integral to the environment. Retail data indicate that point‑of‑sale purchase rates for repellents spike considerably at travel hubs, regional retailers near attraction sites, and outdoor gear outlets, reflecting episodic but meaningful adoption. Outdoor recreation tourism revenues combined with widespread participation present a compelling narrative that expands insect repellent use cases beyond traditional in‑home protection, enabling brands to target segmented outdoor lifestyle channels and integrated travel partnerships.

Future Outlook

The South Africa insect repellent market is expected to maintain steady expansion influenced by sustained vector awareness, tourism growth, and diversified product innovation across personal and household protection formats. Continued urbanization and outdoor lifestyle trends will support product adoption in both metropolitan and peri‑urban sectors. Key future drivers include technological advancements in wearable and long‑duration repellents, broader availability through e‑commerce platforms, and growing supply of natural botanical products led by consumer demand for health‑aligned formulations. Product portfolios that integrate multi‑insect protection and safe ingredients will gain traction as the market evolves with regulatory emphasis on safety and environmental considerations.

Major Players

- Reckitt Benckiser Group plc

- SC Johnson & Son Inc.

- Godrej Consumer Products Ltd.

- Henkel AG & Co. KGaA

- Johnson & Johnson

- Dabur India Ltd.

- Spectrum Brands Holdings Inc.

- Pigeon Corporation

- Murphy’s Naturals / Essential Labs

- Sawyer Products

- Avon & Outdoor Safety Brands

- Coleman Company

- Omega Pharma

Key Target Audience

- Personal care & FMCG buyers and category managers

- Retail Chain Procurement Heads

- Investments and venture capitalist firms

- Government and regulatory bodies

- Travel & tourism service companies

- Outdoor recreation product distributors

- Safety and workplace health procurement teams

- Distribution and logistics partners

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping all stakeholders in the South Africa insect repellent market, defining product categories (personal vs household repellents), ingredient types (synthetic vs natural), and relevant distribution channels. Secondary data from government tourism, health, and trade sources combined with industry databases help establish foundational variables.

Step 2: Market Analysis and Construction

This phase compiles and analyzes historical industry data, including retail revenue, product sales volumes, and channel adoption patterns. Metrics such as unit sales per format, import/export shipment counts, and tourism inflows provide quantitative grounding for revenue estimates and demand drivers.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses concerning consumer behavior, product preference, and competitive dynamics are validated through expert interviews with retail category managers, distribution partners, and formulation specialists. These interviews provide operational and strategic context for validating assumptions.

Step 4: Research Synthesis and Final Output

The final stage synthesizes bottom‑up sales data with top‑down market indicators—such as vector prevalence awareness and tourism statistics—to produce a validated analysis. Cross‑comparison with regional benchmarks ensures consistency and reliability of forecasts and segment estimates.

- Executive Summary

- Research Methodology (Market Definitions & Assumptions, Abbreviations & Conversion Metrics, Data Collection Framework, Top‑Down & Bottom‑Up Revenue Validation, Primary Interview Structure, Secondary Government & Industry Data Sourcing, Forecasting Models & Scenario Analysis, Limitations & Boundary Conditions)

- Definition and Scope

- Insect Repellent Product Definitions

- Market Genesis & Evolution

- Mosquito & Vector Disease Landscape Impact

- Consumer Behaviour & Usage Patterns

- Insect Ecology and Environmental Influence

- Growth Drivers (Public Health Awareness of Vector Diseases (Malaria, dengue risk zones, Indoor‑Outdoor Lifestyle & Travel Patterns)

- Market Challenges (Regulatory & Safety Compliance Constraints, Climate Seasonality & Uneven Demand Cycles)

- Market Opportunities (Rising Demand for Eco‑Friendly & Botanical Repellents, Expanding Retail & E‑commerce Access)

- Market Trends (Technological Convergence, Product Format Diversification)

- Government Policies & Vector Surveillance Initiatives (Public health campaigns, Department of Agriculture insecticide approvals, vector control programmes)

- SWOT Analysis

- Porter’s Five Forces

- Stakeholder Ecosystem Mapping

- Market Value Overview (2020-2026)

- Volume Consumption Metrics (2020-2026)

- Product Format Average Selling Price Analytics (2020-2026)

- Trade & Import‑Export Vectors (2020-2026)

- By Insect Target (In Value %)

Mosquito Repellent

Fly Repellent

Bug & Tick Repellent

Other Insect Types - By Product Format (In Value %)

Sprays & Aerosols

Creams & Lotions

Electric Vaporizers / Plug‑ins

Wearables & Patches

Coils & Other Formats - By Active Ingredient Base (In Value %)

Synthetic Repellents

Natural / Botanical Repellents

Hybrid Formulations

Repellent Treatments Integrated in Textiles & Apparel - By Distribution Channel (In Value %)

Supermarkets & Hypermarkets

Pharmacy & Personal Care Outlets

E‑commerce & Online Retail Partners

Traditional Retail & General Trade

Specialised Outdoor & Travel Retail

- By End‑User Application (In Value %)

Personal Protection

Household Protection

Institutional & Commercial

Tourism & Outdoor Recreation

Pet Protection & Animal Care

- Market Share of Leading Players (Revenues & Units)

(Detailed ranking by revenue contribution & distribution footprint) - Cross‑Comparison Parameters (Company Overview, Product Portfolio Breadth, Active Ingredient Technology, Distribution, Network & Coverage, Retail Channel Partnerships, SKU Depth & Variation, Packaging Innovation & Safety Certifications, Yearly Launch Count & Marketing Spend)

- SWOT Profiles of Major Players

- Pricing Analysis by SKU & Format

- Key Company Profiles

Reckitt Benckiser (Consumer Health)

SC Johnson & Son Inc.

Godrej Consumer Products Ltd.

Henkel AG & Co – Personal Care Segment

Johnson & Johnson Consumer Health

Spectrum Brands Holdings Inc.

Pigeon Corporation – Outdoor Protection Brands

Murphy’s Naturals / Essential Labs

Sawyer Products

Avon & Outdoor Safety Category

Coleman Company – Outdoor Sports Protection

Tender Corporation – Regional Distributors

Omega Pharma – Personal Care Vector Products

Dainihon Jochugiku – Imported Repellents

Local South African Brands & Distributors

- Consumer Demand Drivers & Usage Scenarios

- Purchasing Power & Consumer Spend Patterns

- Regulatory & Compliance Awareness

- Pain Points & Protection Prioritisation

- Decision‑Making Logic

- Forecasted Revenue & Volume Scenarios (2026-2035)

- Consumption Pattern Shifts by Format (2026-2035)

- Evolving Distribution Channel Mix (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now