Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The South Africa Insecticide Market was valued at approximately USD ~ million in 2024, supported by the country’s position as the largest agricultural producer in Sub-Saharan Africa and a major exporter of citrus, grapes, maize, deciduous fruits, and sugarcane.

According to the South African Department of Agriculture and Statistics South Africa, agricultural exports exceeded USD ~ billion in 2023 and surpassed USD ~ billion in 2024, creating sustained demand for crop protection products. Insecticide consumption is driven by increasing pest pressure, export-quality requirements, resistance management programs, and the expansion of commercial farming operations across horticulture and row crops.

Market Segmentation

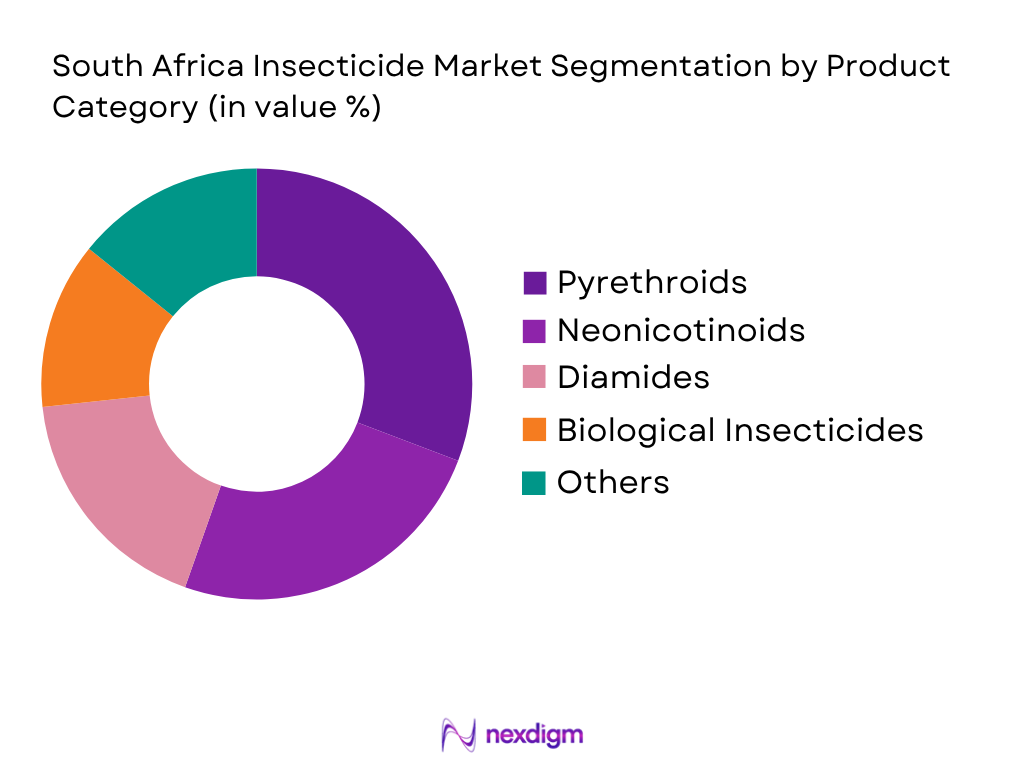

By Product Category

South Africa Insecticide Market is segmented by product class into pyrethroids, neonicotinoids, diamides, biological insecticides, and others. Recently, pyrethroids have held the dominant market share in South Africa under the product class segment due to their broad-spectrum effectiveness against key agricultural pests affecting maize, citrus, sugarcane, vegetables, and fruit crops. Commercial growers rely heavily on pyrethroid-based formulations for managing armyworms, stem borers, aphids, thrips, and fruit flies. Products based on lambda-cyhalothrin, cypermethrin, and deltamethrin remain widely adopted because of their cost-effectiveness, quick knockdown effect, and compatibility with integrated pest management programs. The segment also benefits from strong distribution through agro-dealer networks and extensive registration across multiple crop categories. Their widespread application in both agricultural and public-health pest control programs continues to reinforce their leadership position within the South African insecticide market.

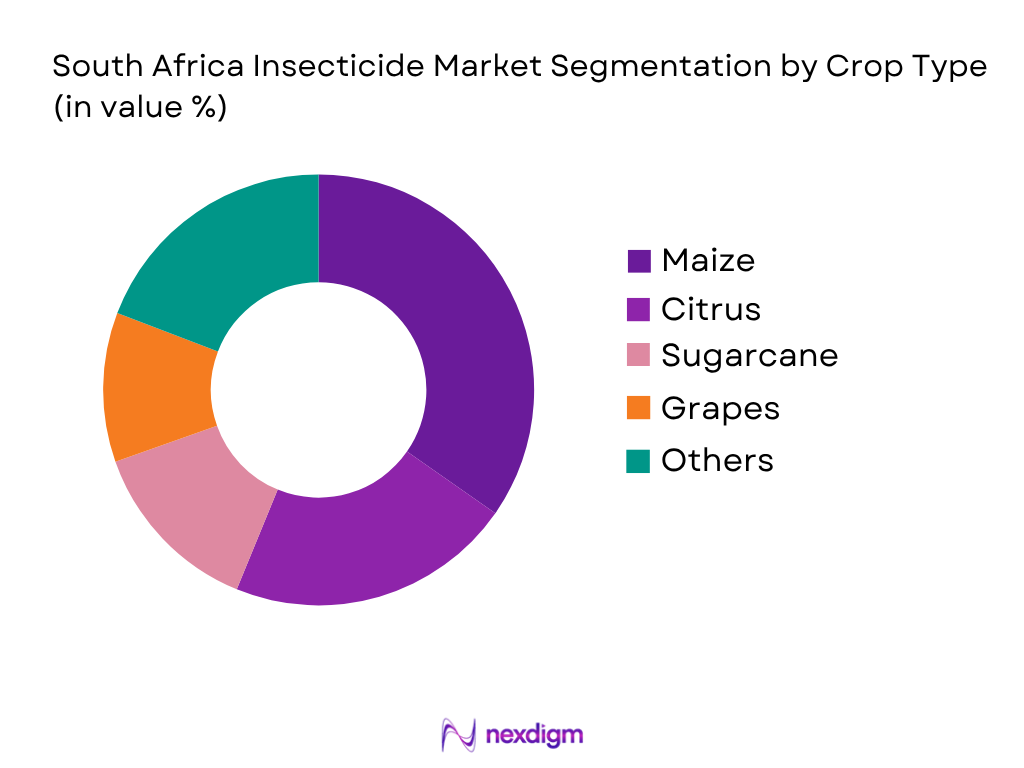

By Crop Type

South Africa Insecticide Market is segmented by crop type into maize, citrus, sugarcane, grapes, and others. Recently, maize has held the dominant market share in South Africa under crop type because it remains the country’s largest field crop by cultivated acreage and production volume. Maize cultivation is highly vulnerable to pests such as fall armyworm, stem borers, cutworms, and aphids, creating consistent demand for insecticide applications throughout the growing season. The commercial nature of South Africa’s maize industry encourages growers to invest heavily in crop protection technologies to safeguard yields and profitability. Furthermore, maize serves as a key staple crop and livestock feed input, increasing its strategic importance within the agricultural economy. The need for resistance management, preventive spraying programs, and integrated pest management strategies further strengthens insecticide consumption within the maize segment, ensuring its continued leadership in the market.

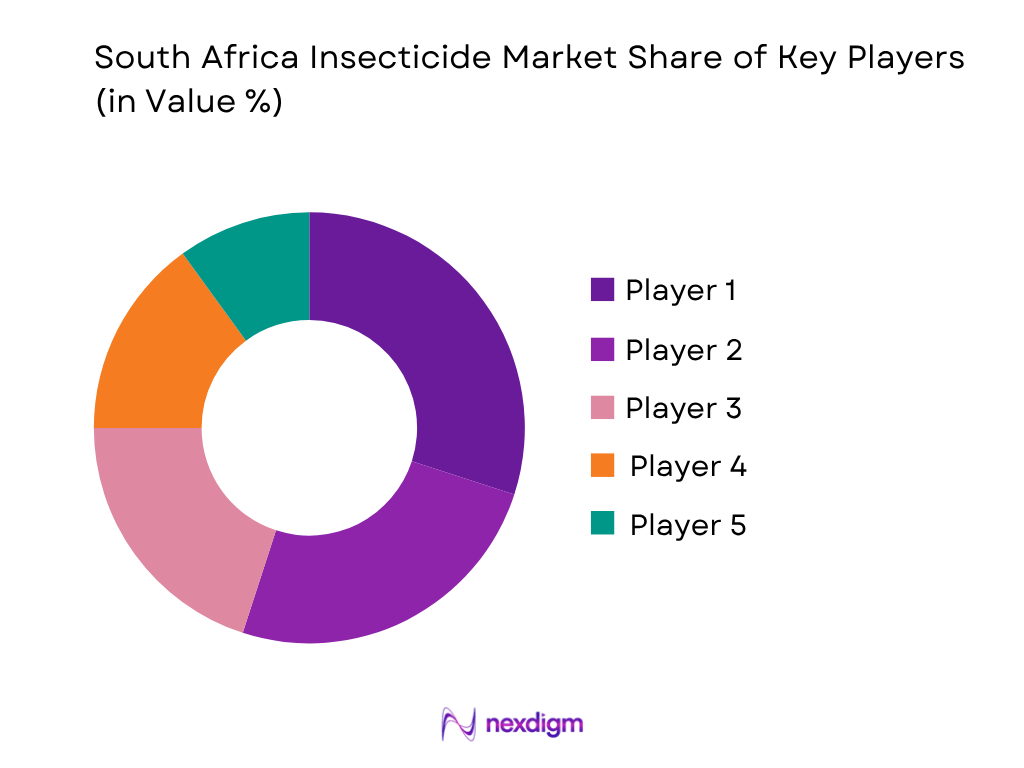

Competitive Landscape

The South Africa Insecticide Market is characterized by the presence of multinational agrochemical manufacturers alongside regional crop-protection companies and local formulators. Competition is driven by product efficacy, active ingredient registrations, biological portfolio strength, agronomic support services, distributor relationships, and crop-specific solutions. Companies increasingly focus on resistance management, biological alternatives, precision agriculture technologies, and export-compliant crop protection products to strengthen their market position.

| Company | Establishment Year | Headquarters | Product Portfolio Strength | Biological Portfolio | Local Formulation Capability | Crop Focus | Distribution Network | Technical Support Infrastructure |

| Bayer Crop Science | 1863 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Syngenta | 2000 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| BASF | 1865 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| FMC Corporation | 1883 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Corteva Agriscience | 2019 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

South Africa Insecticide Market Analysis

Growth Drivers

Expansion of Commercial Agriculture and High-Value Crop Production

South Africa’s insecticide market is strongly supported by the scale and commercialization of the country’s agricultural sector. According to the World Bank, South Africa’s agricultural land covers approximately 96.4 million hectares, providing a substantial production base for crops vulnerable to insect infestations. The country remains one of Africa’s leading exporters of citrus fruits, grapes, apples, pears, maize, and sugar. Data from the South African Department of Agriculture, Land Reform and Rural Development (DALRRD) indicates that agricultural exports exceeded USD 13.7 billion in 2024, reflecting the growing importance of export-oriented farming systems that require strict pest-control measures to meet international phytosanitary standards. The citrus industry alone exported more than 165 million cartons of citrus fruit during recent export seasons, while South Africa produced over 16 million tonnes of maize, according to DALRRD and the Citrus Growers’ Association. These crops are highly susceptible to pests such as fall armyworm, citrus blackfly, false codling moth, aphids, and stem borers, driving sustained demand for insecticide applications. Furthermore, according to the IMF, South Africa’s nominal GDP exceeded USD 400 billion, supporting investment in modern farming inputs and crop protection technologies. The combination of large-scale commercial farming, export-driven production systems, and increasing pest pressure continues to strengthen insecticide consumption across major agricultural provinces.

Rising Pest Pressure and Food Security Priorities

Increasing pest outbreaks and food security concerns are creating sustained demand for insecticides across South Africa’s agricultural sector. The country’s population exceeded 63 million people according to Statistics South Africa, increasing pressure on domestic food production systems. At the same time, climate variability, changing rainfall patterns, and warmer temperatures have expanded the prevalence of destructive pests across major crop-growing regions. The Food and Agriculture Organization (FAO) identifies fall armyworm as one of the most significant threats to maize production across Southern Africa. South Africa cultivates more than 2.5 million hectares of maize annually, making effective insect control essential for maintaining yields. The country also maintains approximately 1.4 million hectares of horticultural production, including citrus, grapes, vegetables, and deciduous fruits, all of which require regular insect management programs. According to Statistics South Africa, agriculture contributed over ZAR 140 billion to gross value added in recent periods, highlighting the sector’s strategic importance to the national economy. The World Bank reports South Africa’s urban population exceeded 40 million residents, increasing demand for stable food supplies. To protect crop productivity and support export competitiveness, farmers continue investing in advanced insecticide solutions, integrated pest management programs, and resistance-management technologies, making pest control a critical growth driver for the insecticide market.

Market Challenges

Stringent Regulatory Compliance and Active Ingredient Restrictions

One of the key challenges facing the South Africa insecticide market is the increasingly stringent regulatory environment governing pesticide registration, use, storage, and environmental safety. The registration of agricultural remedies is regulated under Act No. 36 of 1947, requiring extensive efficacy, environmental, and toxicological assessments before commercialization. These regulatory requirements have become more complex as South Africa aligns various standards with international export market requirements. South Africa exported agricultural products worth more than USD 13.7 billion according to DALRRD, making compliance with European Union, United Kingdom, and Asian residue standards essential for producers. Export-oriented sectors such as citrus, grapes, and deciduous fruits face strict maximum residue limits, forcing growers to continually modify insecticide programs. Additionally, the European Union’s increasing restrictions on certain active ingredients have indirectly affected South African producers supplying export markets. According to the World Bank, South Africa’s merchandise exports exceeded USD 120 billion, emphasizing the importance of maintaining market access through regulatory compliance. Manufacturers must invest significant resources in product stewardship, registration renewals, environmental monitoring, and residue-management programs. These regulatory complexities increase operational burdens and slow the introduction of new insecticide technologies into the South African market.

Climate Variability and Pest Resistance Development

Climate variability and growing insect resistance are major challenges affecting the long-term effectiveness of insecticide applications in South Africa. The country regularly experiences droughts, heatwaves, irregular rainfall patterns, and extreme weather events, which influence pest population dynamics and increase unpredictability in pest outbreaks. According to the World Bank Climate Portal, South Africa remains one of the most climate-vulnerable agricultural economies in Africa. The country’s maize production area exceeds 2.5 million hectares, while fruit and horticultural production occupies more than 1 million hectares, exposing a large portion of cultivated land to evolving pest threats. Continuous use of similar active ingredients has accelerated resistance development among pests such as fall armyworm, aphids, thrips, and codling moth populations. Resistance management therefore requires growers to rotate products and adopt integrated pest management strategies. According to Statistics South Africa, agriculture supports hundreds of thousands of direct jobs across rural regions, making crop losses from resistant pests a significant economic concern. As resistance increases, farmers require more sophisticated insecticide programs, biological alternatives, and monitoring systems. These factors create operational complexity and increase pressure on manufacturers to continually develop innovative pest-control technologies.

Market Opportunities

Growth of Biological and Sustainable Crop Protection Solutions

The transition toward sustainable agriculture presents a significant opportunity for the South Africa insecticide market, particularly in biological insecticides and environmentally friendly pest-management solutions. South Africa’s export-driven agricultural sector increasingly serves markets with stringent environmental and residue requirements, encouraging the adoption of biological alternatives. According to DALRRD, agricultural exports exceeded USD 13.7 billion, with citrus, grapes, apples, pears, and vegetables representing major export categories. Exporters supplying European and premium international markets are increasingly required to demonstrate sustainable production practices and reduced chemical residues. South Africa’s certified agricultural export industries therefore provide a favorable environment for biological insecticide adoption. The country also possesses more than 96 million hectares of agricultural land, according to the World Bank, creating substantial opportunities for integrated pest management implementation across multiple crop systems. Biological products can support resistance management while helping growers comply with evolving sustainability standards. Furthermore, rising investment in regenerative agriculture and environmental stewardship programs across commercial farming operations is creating demand for innovative biological formulations. These trends position sustainable crop protection technologies as one of the most attractive opportunities within the South African insecticide market.

Precision Agriculture and Digital Pest Monitoring Technologies

Precision agriculture technologies are creating substantial growth opportunities for the South Africa insecticide market by improving application efficiency and enhancing pest management outcomes. South Africa has one of the most advanced commercial farming sectors in Africa, supported by strong mechanization levels and increasing adoption of digital agriculture tools. According to the World Bank, South Africa’s GDP exceeds USD 400 billion, providing a strong economic base for investment in agricultural technology. Mobile connectivity continues expanding across rural regions, while commercial farms increasingly utilize satellite imagery, drones, geographic information systems, and remote sensing technologies to monitor crop health and pest activity. These tools allow farmers to optimize insecticide usage and improve application timing. South Africa cultivates millions of hectares of maize, citrus, sugarcane, and horticultural crops, creating large-scale opportunities for targeted pest-management programs. Precision spraying technologies can reduce unnecessary chemical applications while improving efficacy against pest infestations. Additionally, digital monitoring systems help growers identify outbreaks earlier, reducing crop losses and supporting higher productivity. The integration of insecticides with smart farming technologies is therefore emerging as a major opportunity for long-term market expansion.

Future Outlook

The South Africa Insecticide Market is expected to witness steady growth over the forecast period, supported by rising agricultural exports, increasing pest infestations, climate variability, and the expansion of commercial farming operations. Export-oriented fruit and citrus production will remain a major demand generator due to stringent phytosanitary requirements imposed by international markets. Biological insecticides are expected to gain significant traction as growers seek sustainable crop protection solutions and regulators emphasize environmental stewardship. Precision agriculture technologies, drone spraying, smart monitoring systems, and integrated pest management programs are likely to transform insecticide application practices across the country. The market is also expected to benefit from increasing adoption of resistance-management strategies and growing awareness of crop yield optimization. Based on industry trends and agricultural development indicators, the South Africa Insecticide Market is forecast to grow at a CAGR of approximately 4.8% during 2026-2035.

Major Players

- Bayer Crop Science South Africa

- Syngenta South Africa

- BASF South Africa

- FMC Corporation South Africa

- Corteva Agriscience South Africa

- UPL South Africa

- ADAMA South Africa

- Sumitomo Chemical South Africa

- Nufarm South Africa

- Villa Crop Protection

- Philagro South Africa

- Arysta LifeScience South Africa

- Koppert South Africa

- Amiran South Africa

- Farm Ag International

Key Target Audience

- Agrochemical Manufacturers

- Insecticide Formulators and Registrants

- Commercial Grain Farming Enterprises

- Citrus and Fruit Export Producers

- Sugarcane Plantation Operators

- Agricultural Input Distributors and Agro-Dealer Networks

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the South Africa Insecticide Market. This includes insecticide manufacturers, formulators, distributors, agro-dealers, commercial farmers, horticulture exporters, plantation operators, regulators, and pest management specialists. The objective is to identify critical variables such as crop-specific demand, active ingredient usage, distribution structures, and regulatory influences affecting market performance.

Step 2: Market Analysis and Construction

In this phase, historical market information relating to the South Africa Insecticide Market is compiled and analyzed. This includes evaluating crop acreage, export volumes, pest infestation patterns, insecticide consumption trends, import-export flows, and registration databases. Both top-down and bottom-up methodologies are utilized to estimate market size and segment-level performance accurately.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through structured interviews with agrochemical companies, distributors, crop consultants, commercial farmers, agronomists, and industry experts. These consultations provide valuable insights into pest management practices, resistance challenges, biological product adoption, purchasing behavior, and competitive dynamics. The findings help refine assumptions and strengthen the reliability of market estimates.

Step 4: Research Synthesis and Final Output

The final phase integrates secondary research, primary interviews, trade analysis, company benchmarking, and regulatory assessments. Information obtained through both top-down and bottom-up approaches is triangulated to ensure consistency and accuracy. The final output delivers a comprehensive assessment of market size, segmentation, competition, growth drivers, challenges, opportunities, and future outlook for the South Africa Insecticide Market.

- Executive Summary

- Research Methodology (Market definitions and assumptions, abbreviations, insecticide market taxonomy, active ingredient classification, agricultural and non-agricultural scope, market sizing approach, top-down and bottom-up triangulation, distributor and agro-dealer interviews, farmer and plantation surveys, import-export analysis, regulatory assessment, limitations and future conclusions)

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (Agricultural export expansion, citrus production growth, maize cultivation intensity, pest infestation pressure, food security initiatives, precision agriculture adoption, biological crop protection demand, commercial farming modernization)

- Market Challenges (Pesticide resistance, regulatory compliance costs, climate variability, counterfeit agrochemicals, import dependence for active ingredients, water scarcity, logistics inefficiencies, commodity price volatility)

- Opportunities (Biological insecticides, integrated pest management, drone-based spraying, export-oriented horticulture, greenhouse cultivation, digital farming platforms, sustainable crop protection, specialty crop expansion)

- Market Trends (Resistance management programs, low-residue insecticides, precision application technologies, biopesticide adoption, regenerative agriculture practices, smart spraying systems, AI-enabled pest monitoring, climate-smart farming)

- Government Regulation (Act No. 36 of 1947 compliance, Department of Agriculture registrations, Maximum Residue Limits compliance, export phytosanitary standards, environmental impact regulations, hazardous substance handling requirements, worker safety protocols)

- SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces

- Competition Ecosystem

- By Market Revenue (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Realization per Ton (2020-2025)

- By Product Category (In Value %)

Pyrethroids

Neonicotinoids

Diamides

Organophosphates

Biological Insecticides

Others - By Crop Type (In Value %)

Maize

Citrus

Grapes

Sugarcane

Vegetables & Fruits

Others - By Formulation Type (In Value %)

Emulsifiable Concentrates (EC)

Suspension Concentrates (SC)

Wettable Powders (WP)

Water Dispersible Granules (WDG)

Ultra-Low Volume Formulations (ULV)

Others - By Application Method (In Value %)

Foliar Spray

Seed Treatment

Soil Treatment

Chemigation

Aerial Application - By End User (In Value %)

Commercial Crop Farms

Plantation Growers

Greenhouse Producers

Public Health & Vector Control Authorities

Professional Pest Control Operators - By Region (In Value %)

Gauteng

KwaZulu-Natal

Western Cape

Eastern Cape

Mpumalanga

Limpopo

Free State

North West

Northern Cape

- Market Share of Major Players (Market revenue, product portfolio strength, active ingredient registrations, distributor penetration, export crop presence, biological portfolio contribution, regional reach)

- Cross Comparison Parameters (Product portfolio breadth, active ingredient registrations, biological insecticide portfolio, citrus and horticulture penetration, distributor and agro-dealer network, local manufacturing and formulation capability, farmer technical support infrastructure, export-crop compliance solutions)

- SWOT Analysis of Major Players

- Pricing Analysis Basis SKUs (Lambda-cyhalothrin, Deltamethrin, Imidacloprid, Chlorantraniliprole, Thiamethoxam, Spinosad, Abamectin, Cypermethrin, Emamectin Benzoate, Fipronil)

- Detailed Profiles of Major Companies

Bayer Crop Science South Africa

Syngenta South Africa

BASF South Africa

FMC Corporation South Africa

Corteva Agriscience South Africa

UPL South Africa

ADAMA South Africa

Sumitomo Chemical South Africa

Nufarm South Africa

Villa Crop Protection

Arysta LifeScience South Africa

Philagro South Africa

Koppert South Africa

Amiran South Africa

Farm Ag International

- Commercial Grain Farmer Analysis

- Citrus and Fruit Exporter Analysis

- Sugarcane Grower Analysis

- Vegetable and Horticulture Producer Analysis

- Public Health Vector Control Authority Analysis

- Professional Pest Control Operator Analysis

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Realization per Ton (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now