Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Africa medical devices market was valued at approximately USD ~ billion based on a recent historical assessment supported by healthcare import statistics and medical equipment procurement data reported by the South African Department of Trade, Industry and Competition and the South African Medical Technology Industry Association. Demand is driven by expanding hospital infrastructure, increasing procurement of diagnostic imaging equipment, rising chronic disease burden, and strong reliance on imported advanced medical technologies used in private hospital networks and specialized treatment centers.

Johannesburg, Cape Town, and Durban dominate the South Africa medical devices market because these metropolitan regions host the country’s largest hospital networks, private healthcare groups, and specialized medical treatment centers that require advanced diagnostic and surgical technologies. These cities also serve as major medical technology distribution hubs with strong logistics infrastructure, medical training institutions, and international supplier networks, enabling faster technology adoption and higher medical equipment procurement compared with smaller regional healthcare facilities.

Market Segmentation

By Product Type

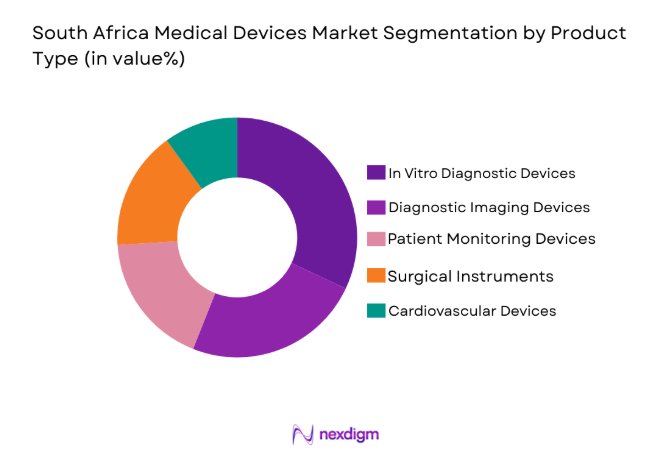

South Africa Medical Devices Market is segmented by product type into Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Instruments, In Vitro Diagnostic Devices, and Cardiovascular Devices. Recently, In Vitro Diagnostic Devices has a dominant market share due to factors such as strong demand for laboratory testing services, expansion of diagnostic laboratories, and rising demand for infectious disease screening across hospitals and pathology laboratories. Diagnostic testing services remain essential for managing infectious diseases, chronic illnesses, and preventive healthcare screening programs. Public health initiatives and private pathology networks significantly increase laboratory test volumes nationwide. Diagnostic equipment procurement by hospitals and laboratory chains further strengthens demand. Growing adoption of automated laboratory analyzers and molecular diagnostic platforms also contributes to the dominance of this segment in the South Africa medical devices market.

By Platform Type

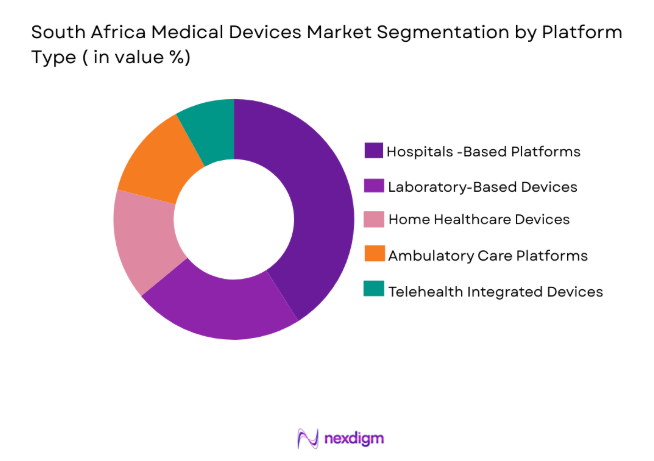

South Africa Medical Devices Market is segmented by platform type into Hospital-based Devices, Laboratory-based Devices, Home Healthcare Devices, Ambulatory Care Devices, and Telehealth Integrated Devices. Recently, Hospital-based Devices has a dominant market share due to factors such as the concentration of advanced medical treatment facilities within private hospital groups and specialized healthcare centers. Hospitals procure large volumes of imaging systems, surgical devices, patient monitoring systems, and intensive care equipment required for complex clinical procedures. The private healthcare sector in South Africa maintains modern hospital infrastructure with strong investment in advanced medical technologies. High patient volumes across tertiary hospitals and specialized treatment centers further increase equipment utilization rates. Hospital networks also maintain long-term procurement agreements with global medical technology manufacturers, strengthening the dominance of hospital-based device platforms.

Competitive Landscape

The South Africa medical devices market is moderately consolidated and strongly influenced by multinational medical technology companies that supply advanced diagnostic, monitoring, and surgical equipment to both public and private healthcare providers. Global manufacturers dominate due to strong brand recognition, regulatory approvals, and established distribution networks across hospitals and diagnostic laboratories. Local distributors and regional suppliers play an important role in equipment servicing, import logistics, and hospital procurement partnerships. Private hospital groups often establish long term technology partnerships with international suppliers, further strengthening market concentration among major players.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Distribution Network Strength |

| Medtronic | 1949 | Ireland | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~~ |

| GE HealthCare | 1892 | USA | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| Abbott Laboratories | 1888 | USA | ~ | ~ | ~ | ~ | ~ |

South Africa Medical Devices Market Analysis

Growth Drivers

Expansion of Private Healthcare Infrastructure and Hospital Modernization

Expansion of private healthcare infrastructure significantly strengthens demand for medical devices across South Africa as hospital groups continuously invest in advanced clinical technologies to improve treatment quality and operational efficiency. Private healthcare providers operate large hospital networks equipped with specialized surgical units, diagnostic laboratories, and advanced imaging departments requiring modern medical equipment. Hospitals frequently upgrade diagnostic imaging technologies, patient monitoring systems, and surgical platforms to maintain international healthcare standards. Increasing patient demand for specialized treatments such as cardiology procedures, oncology care, and minimally invasive surgery further encourages hospitals to procure advanced medical technologies. Private hospital groups also compete through service quality and technological capability, which encourages continuous investment in modern equipment. Healthcare infrastructure expansion across urban regions increases the number of operating theaters, intensive care units, and diagnostic departments requiring advanced equipment. Medical tourism demand also motivates hospitals to maintain modern clinical infrastructure with globally recognized medical technologies. Equipment replacement cycles and continuous technological innovation therefore sustain strong procurement activity across private hospital networks nationwide.

Rising Burden of Chronic Diseases and Diagnostic Testing Demand

Rising prevalence of chronic diseases significantly drives demand for medical devices in South Africa because healthcare providers require advanced diagnostic and monitoring equipment to manage long term patient conditions. Cardiovascular diseases, diabetes, cancer, and respiratory disorders require continuous clinical monitoring, laboratory testing, and diagnostic imaging procedures. Hospitals therefore invest in imaging systems, laboratory analyzers, cardiac monitoring equipment, and patient monitoring technologies to support treatment programs. Increasing patient volumes within hospitals and outpatient clinics further increase equipment utilization rates and replacement demand. Diagnostic laboratories expand testing capacity to support screening programs and disease management services for large patient populations. Government healthcare initiatives promoting early disease detection also increase diagnostic testing volumes nationwide. Private pathology laboratory chains continuously expand laboratory networks and procure automated diagnostic equipment to improve testing efficiency. Growing awareness of preventive healthcare among urban populations further increases demand for diagnostic procedures. As chronic disease prevalence continues rising, hospitals and laboratories require more advanced medical technologies to support long term patient management.

Market Challenges

High Dependence on Imported Medical Equipment and Currency Volatility

The South Africa medical devices market faces significant challenges due to strong dependence on imported medical technologies supplied by international manufacturers. Advanced diagnostic imaging systems, surgical platforms, and specialized medical equipment are primarily imported from Europe and the United States. Import dependence increases equipment costs because currency fluctuations directly influence procurement pricing for hospitals and distributors. Healthcare providers often experience budgeting pressure when exchange rate volatility raises the cost of imported technologies. Public hospitals operating under fixed healthcare budgets face additional financial constraints when medical equipment procurement costs increase. Import logistics, customs duties, and regulatory approval processes further extend procurement timelines for healthcare providers. Local manufacturing capacity for high technology medical equipment remains limited, preventing domestic production from offsetting import dependency. Hospitals therefore rely heavily on international suppliers for advanced diagnostic and surgical technologies. This structural reliance on imported medical technologies increases cost uncertainty and creates procurement challenges for healthcare institutions.

Limited Healthcare Infrastructure Capacity in Rural Regions

Uneven healthcare infrastructure distribution across South Africa creates significant challenges for the medical devices market because many rural healthcare facilities lack advanced diagnostic and treatment equipment. Urban hospitals benefit from strong infrastructure investments and private healthcare participation, while rural clinics and regional hospitals often operate with limited medical technology resources. Limited infrastructure capacity reduces equipment procurement volumes outside major metropolitan areas. Rural healthcare facilities frequently lack specialized clinical departments that require advanced imaging systems or surgical technologies. Budget constraints within public healthcare systems also restrict equipment modernization across smaller hospitals. Limited availability of trained medical technicians and biomedical engineers further complicates the deployment of complex medical equipment in remote regions. Healthcare infrastructure expansion programs are gradually improving access, but equipment distribution remains uneven nationwide. Medical device suppliers therefore experience concentrated demand within major urban hospital networks. This regional imbalance limits broader nationwide equipment adoption despite growing healthcare needs.

Market Opportunities

Growth of Diagnostic Laboratory Networks and Pathology Services

Expansion of diagnostic laboratory networks across South Africa creates major opportunities for medical device manufacturers supplying laboratory analyzers and diagnostic technologies. Pathology laboratory groups continue expanding testing facilities across urban and semi urban regions to meet growing demand for medical diagnostics. Laboratories require automated analyzers, molecular diagnostic systems, and laboratory information systems to process increasing testing volumes efficiently. Growing emphasis on early disease detection programs also strengthens demand for advanced diagnostic technologies. Healthcare providers increasingly rely on laboratory testing to support treatment planning and patient monitoring. Private laboratory networks continue investing in new facilities and advanced diagnostic platforms to improve service capacity. Public healthcare programs also depend heavily on laboratory testing for infectious disease monitoring and preventive screening programs. Technology providers therefore find expanding opportunities in supplying laboratory automation systems and advanced diagnostic equipment. The growing scale of diagnostic laboratory services significantly expands the addressable market for medical device manufacturers.

Adoption of Digital Health Technologies and Remote Patient Monitoring Systems

Increasing adoption of digital health technologies presents significant opportunities for medical device companies developing connected healthcare equipment and remote patient monitoring systems. Hospitals increasingly integrate digital patient monitoring devices with hospital information systems to improve clinical efficiency and patient data management. Remote monitoring technologies allow physicians to track patient conditions outside hospital environments, supporting chronic disease management programs. Healthcare providers also deploy wearable monitoring devices and connected diagnostic platforms that transmit patient data through digital networks. Telehealth platforms further expand the use of remote monitoring technologies for outpatient care and home healthcare services. Private healthcare providers increasingly invest in digital health infrastructure that supports connected medical devices. Technology integration improves patient monitoring accuracy and enables real time clinical decision making. Medical device manufacturers therefore expand product portfolios to include digitally integrated equipment. The expansion of digital healthcare ecosystems across hospitals and outpatient care networks creates substantial long term market opportunities.

future Outlook

The South Africa medical devices market is expected to experience steady growth supported by expanding healthcare infrastructure, increasing hospital modernization, and rising demand for advanced diagnostic technologies. Private healthcare providers will continue investing in modern equipment to enhance clinical capabilities and patient care quality. Technological innovation including digital health integration and remote monitoring solutions will influence procurement strategies. Government healthcare expansion initiatives and rising diagnostic demand are also expected to sustain equipment adoption across hospitals and laboratories.

Major Players

- Medtronic

- Siemens Healthineers

- GE HealthCare

- Philips Healthcare

- Abbott Laboratories

- Becton Dickinson

- Boston Scientific

- Roche Diagnostics

- Johnson & Johnson MedTech

- Smith & Nephew

- Olympus Corporation

- Stryker Corporation

- Terumo Corporation

- Mindray Medical

- Fujifilm Healthcare

Key Target Audience

- Medical device manufacturers

- Private hospital groups

- Diagnostic laboratory networks

- Healthcare technology distributors

- Healthcare investment firms

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the South Africa medical devices market were identified through healthcare infrastructure data, hospital procurement trends, diagnostic laboratory capacity, and medical equipment import statistics. These variables form the base indicators used for market structure analysis.

Step 2: Market Analysis and Construction

Market data was constructed using healthcare expenditure statistics, medical equipment trade data, hospital infrastructure records, and procurement patterns across public and private healthcare providers. Industry datasets and regulatory records were integrated for comprehensive market mapping.

Step 3: Hypothesis Validation and Expert Consultation

Initial market insights were validated through consultation with healthcare technology experts, hospital procurement managers, and medical equipment distributors. Industry professionals provided operational insights into equipment demand trends and technology adoption.

Step 4: Research Synthesis and Final Output

Validated data was synthesized through structured analysis models to generate final insights, segmentation frameworks, and competitive landscape mapping. The resulting analysis provides an integrated view of market structure, demand drivers, and industry dynamics.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Private Healthcare Infrastructure

Rising Burden of Chronic Diseases and Diagnostic Testing Demand

Increasing Adoption of Digital Health and Telemedicine Technologies - Market Challenges

High Dependence on Imported Medical Equipment

Limited Healthcare Infrastructure in Rural Regions

Regulatory Compliance and Approval Complexity - Market Opportunities

Expansion of Diagnostic Laboratory Networks

Growth of Remote Patient Monitoring Technologies

Local Medical Device Manufacturing Development - Trends

Integration of Artificial Intelligence in Diagnostic Equipment

Growing Demand for Portable and Wearable Medical Devices - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Diagnostic Imaging Devices

Patient Monitoring Systems

In Vitro Diagnostic Devices

Surgical and Therapeutic Devices

Cardiovascular and Implantable Devices - By Platform Type (In Value%)

Hospital-based Medical Devices

Diagnostic Laboratory Platforms

Ambulatory Care Device Platforms

Home Healthcare Devices

Telehealth Integrated Devices - By Fitment Type (In Value%)

Fixed Clinical Equipment

Portable Medical Devices

Wearable Medical Devices

Integrated Digital Health Devices - By End User Segment (In Value%)

Hospitals and Surgical Centers

Diagnostic Laboratories

Home Healthcare Providers

- Market Share Analysis

- Cross Comparison Parameters (Technology Portfolio, Product Range, Distribution Network Strength, Regulatory Compliance Capability, Manufacturing Presence, Pricing Strategy, After-Sales Service Network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Medtronic

Siemens Healthineers

GE HealthCare

Philips Healthcare

Abbott Laboratories

Boston Scientific

Becton Dickinson

Fresenius Medical Care

Johnson & Johnson MedTech

Stryker Corporation

Terumo Corporation

Mindray Medical

B Braun Medical

Teleflex Medical

Akacia Medical

- Private Hospitals Driving Advanced Technology Adoption

- Diagnostic Laboratories Expanding Testing Infrastructure

- Public Healthcare Facilities Increasing Equipment Procurement

- Home Healthcare Providers Increasing Use of Monitoring Devices

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now