Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The South Africa Oral Care Market is valued at USD ~ million, supported by oral hygiene penetration, toothpaste-led household consumption, pharmacy-led retailing and premium sensitivity-care adoption. Nexdigm research reports that the market reached USD ~ million and is forecast to reach USD ~ million, while some insights places the market at USD ~ million and projects USD ~ million at 6.96% CAGR through its forecast period.

Gauteng, KwaZulu-Natal and Western Cape dominate South Africa’s oral care demand because they combine population scale, income concentration, formal retail depth and stronger pharmacy penetration. Stats SA estimates South Africa’s population at 63.02 million, with Gauteng above 15.9 million people, KwaZulu-Natal at 12.3 million and Western Cape at 7.6 million. Gauteng also contributes the largest provincial GDP, followed by KwaZulu-Natal and Western Cape, strengthening premium oral care uptake.

Market Segmentation

By Product Type

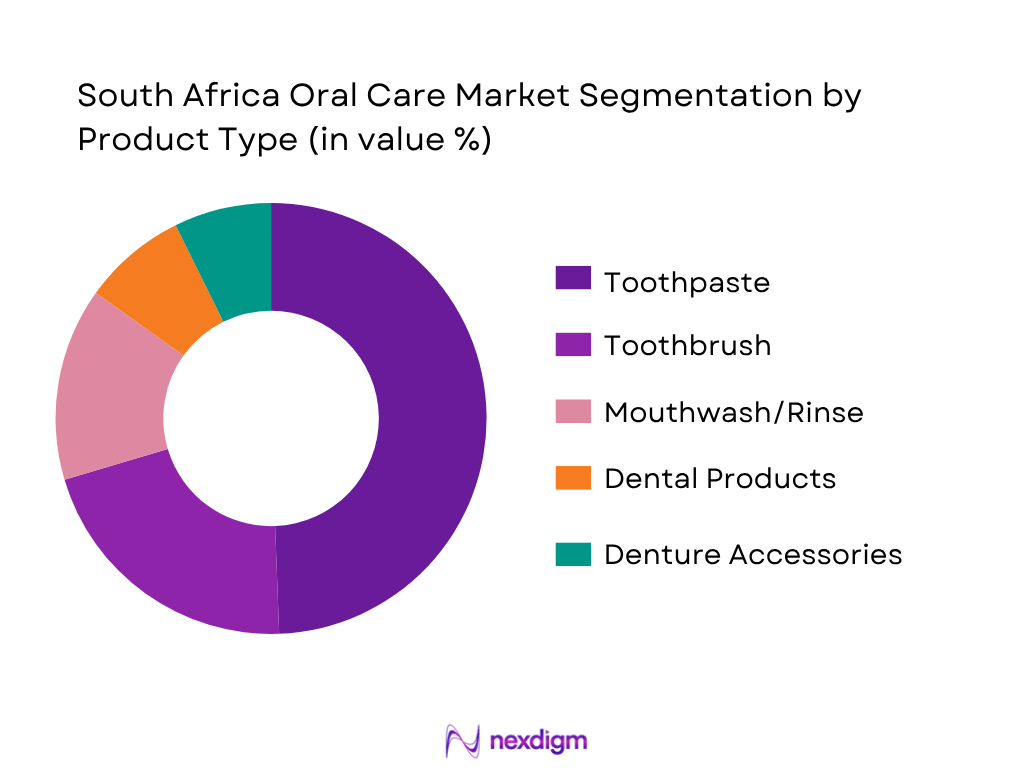

South Africa Oral Care Market is segmented by product type into toothpaste, toothbrushes, mouthwash/rinse, denture products and dental accessories. Toothpaste dominates because it is the most frequently replenished household oral care product and is embedded in daily brushing routines across income groups. Toothpaste is identified as the largest revenue-generating product segment, while Deep Market Insights discloses toothpaste revenue at USD 242.19 million within a USD 489.86 million oral care market. Toothpaste also benefits from multiple benefit ladders, including cavity protection, whitening, sensitivity, gum health, herbal and children’s variants. Premium therapeutic brands such as Sensodyne and Parodontax support value growth, while Colgate, Aquafresh and private-label SKUs sustain mass-market penetration across grocery, pharmacy and online channels.

By Distribution Channel

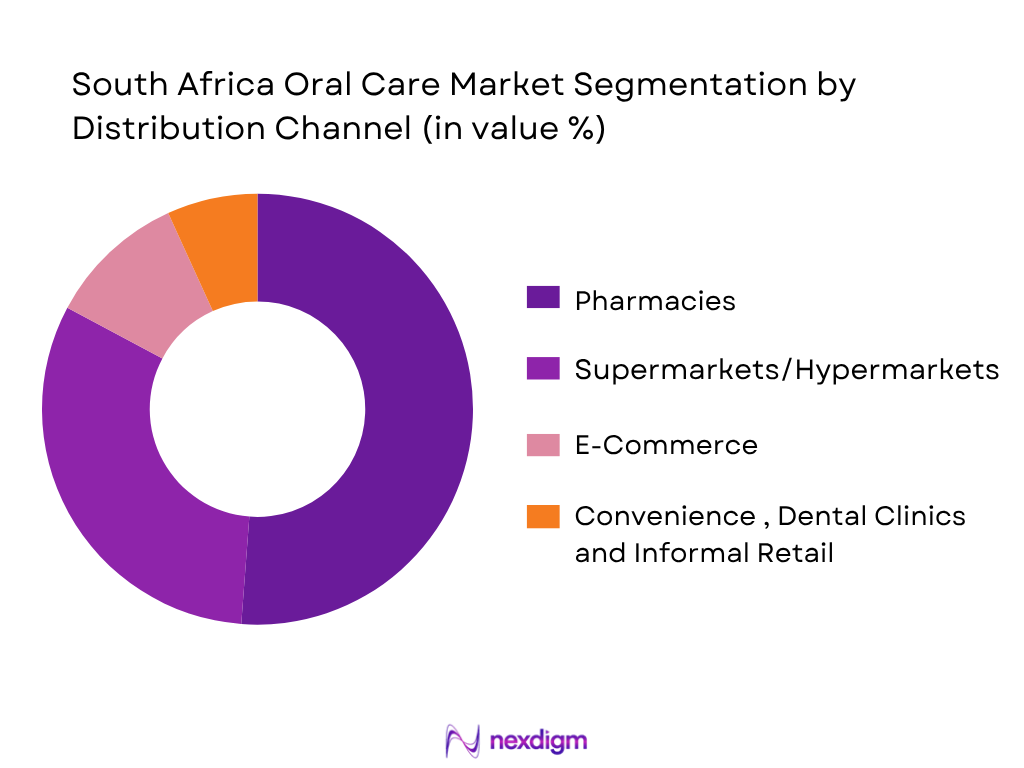

South Africa Oral Care Market is segmented by distribution channel into pharmacies, supermarkets/hypermarkets, e-commerce and other retail formats. Pharmacy dominates because oral care in South Africa is strongly linked with therapeutic needs such as sensitivity, gum care, mouth ulcers, denture maintenance and dentist/pharmacist-led recommendation. Deep Market Insights discloses pharmacy channel revenue of USD 250.61 million, implying a leading position within the national oral care market. The dominance is reinforced by the scale of Clicks and Dis-Chem, which combine medicines, personal care, private labels, loyalty programmes and premium therapeutic oral hygiene ranges. Supermarkets remain important for family toothpaste and toothbrush packs, while e-commerce is gaining relevance through Takealot, retailer apps and online pharmacy purchasing.

Competitive Landscape

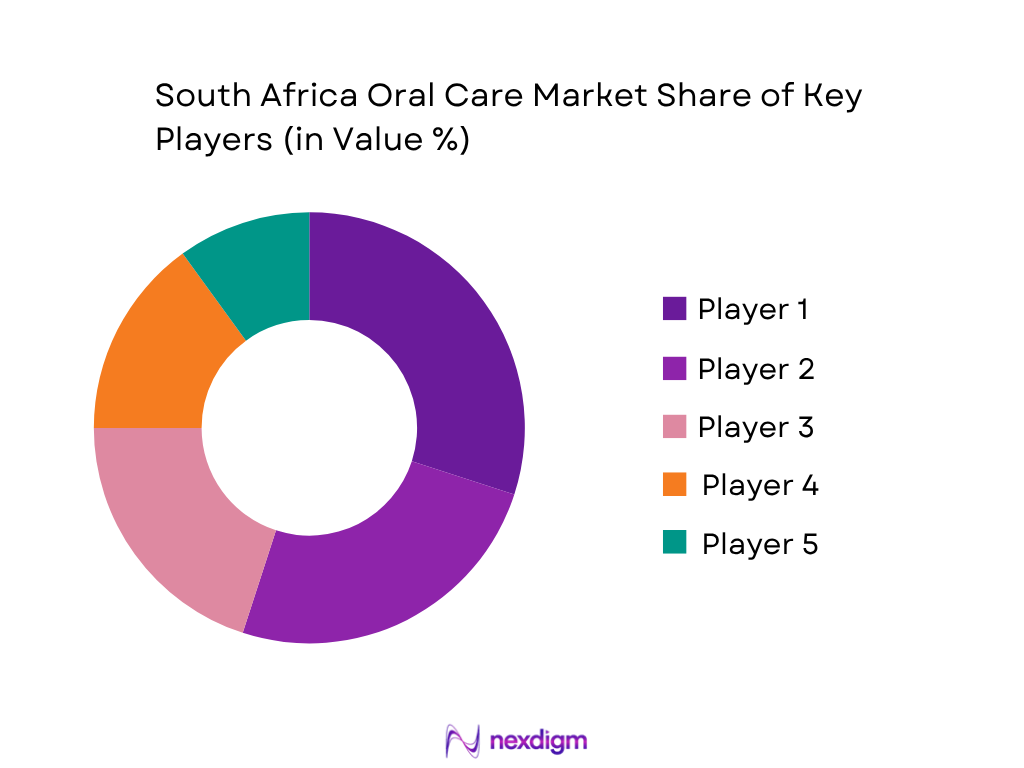

The South Africa Oral Care Market is concentrated around multinational brand owners and large retail pharmacy chains. Colgate-Palmolive leads mass toothpaste visibility; Haleon has a strong therapeutic position through Sensodyne, Aquafresh, Corsodyl and Parodontax; P&G is material in toothbrushes through Oral-B; Kenvue is prominent in mouthwash through Listerine; and Unilever competes through mass oral hygiene brands. Pharmacy chains and private labels intensify competition through shelf control, loyalty pricing and affordable oral care alternatives.

| Company | Establishment Year | Headquarters | Core Oral Care Brands | Key Category Strength | South Africa Channel Strength | Premium/Therapeutic Positioning | Whitening/Sensitivity Exposure | E-Commerce Visibility | Competitive Role |

| Colgate-Palmolive | 1806 | New York, USA | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Haleon | 2022 | Weybridge, UK | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Procter & Gamble | 1837 | Cincinnati, USA | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Kenvue | 2023 | New Jersey, USA | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Unilever | 1929 | London, UK | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

South Africa Oral Care Market Analysis

Growth Drivers

Sensitivity Toothpaste Adoption

Sensitivity toothpaste adoption is supported by South Africa’s large urban consumer base, pharmacy-oriented healthcare behavior and high exposure to gum-related oral health issues. South Africa’s population is 63.02 million, including 32.13 million females, creating a broad household base for daily oral hygiene products. Urban provinces are especially relevant because Gauteng has over 15.9 million people, KwaZulu-Natal has 12.3 million and Western Cape has 7.6 million, giving brands access to dense pharmacy, supermarket and dental-practice networks. Government communication for National Oral Health Month states that gum disease ranks second only to the common cold in prevalence, with an estimated 90 out of every 100 South Africans experiencing it at some point, directly supporting demand for sensitivity, gum-care and dentist-recommended toothpaste formats. Medical-aid access further shapes premium therapeutic purchasing: Stats SA reports that 15.5 out of every 100 South Africans had medical-aid coverage, with Western Cape at 25.4 and Gauteng at 21.3, concentrating private healthcare access in the same provinces where premium toothpaste brands are more visible. The country’s GDP is USD 401.14 billion and GDP per capita is USD 6,267.2, which supports the presence of both mass and therapeutic toothpaste tiers.

Alcohol-Free Mouthwash Demand

Alcohol-free mouthwash demand is linked to South Africa’s preventive-care gap, rising public oral-health messaging and the need for gentler products suitable for families, gum-care users and consumers seeking daily fresh-breath routines. Stats SA estimates the national population at 63.02 million, while World Bank data records 40.77 million urban residents, creating a substantial urban consumer pool exposed to pharmacy shelves, retailer promotions and dentist/pharmacist guidance. The health-service access pattern strengthens the role of over-the-counter prevention: Stats SA’s General Household Survey presentation reports that 73.1 out of every 100 household members first consulted public clinic or hospital personnel, while 25.3 first used the private sector, indicating that many consumers depend on retail oral-care products rather than frequent private dental support. National Oral Health Month communication highlights cavities and gum disease as two of the world’s most common mouth-related health problems, while South Africa’s oral health policy identifies public oral healthcare facilities and private dental surgeries as the main treatment channels. With 96.1 out of every 100 households owning at least one mobile phone and 82.1 having internet access through any means, consumer education around alcohol-free, fluoride, gum-care and antibacterial rinses can scale quickly through digital and retail channels.

Market Challenges

Price Sensitivity

Price sensitivity remains a structural challenge because oral care competes with essential household spending in an economy marked by weak income growth, high unemployment and constrained consumption. World Bank data records South Africa’s GDP growth at 0.5, GDP per capita at USD 6,267.2 and household final consumption expenditure at USD 259.30 billion, indicating a large consumer economy but one exposed to pressure from slow growth and income inequality. Stats SA’s labour-force release reports 17.1 million employed persons and 8.0 million unemployed persons, with the official unemployment rate at 31.9 in the fourth quarter, directly limiting discretionary trade-up into premium sensitivity toothpaste, whitening kits, electric toothbrushes and branded mouthwash. Consumer inflation also affected daily essentials: Stats SA reported annual consumer price inflation of 5.2 in April and 3.0 in December, while miscellaneous goods and services contributed 1.0 point to the December inflation reading. For oral care suppliers, this means value packs, smaller toothpaste tubes, multipacks and private-label alternatives become more important, while premium therapeutic products must justify claims through dentist, pharmacist and brand trust.

Low Dental Visit Frequency

Low dental visit frequency is a market challenge because it reduces professional diagnosis, delays treatment and shifts many oral-health decisions to self-care at pharmacy and grocery shelves. Stats SA reports that only 15.5 out of every 100 South Africans had medical-aid coverage, while medical-aid access is much higher in Western Cape at 25.4 and Gauteng at 21.3 than in Limpopo at 10.0 and KwaZulu-Natal at 10.2. This uneven healthcare financing restricts regular private dental use outside higher-income provinces. The General Household Survey presentation further shows that 73.1 out of every 100 household members first consulted public clinic or hospital personnel, compared with 25.3 using private-sector personnel, indicating a heavy public-sector dependence that can constrain specialist dental access. WHO’s regional oral-health message reports only 0.33 dentists per 10,000 population in the African region, a severe workforce constraint relative to need. South Africa’s Department of Health policy also notes that most dental care is provided by dentists, dental therapists and oral hygienists across public oral healthcare facilities and private dental surgeries, meaning service availability, waiting times and out-of-pocket burden influence consumer reliance on toothpaste, mouthwash, floss and denture-care products.

Market Opportunities

Private-Label Oral Care

Private-label oral care has future growth potential because South Africa’s consumer environment favours affordable, retailer-controlled alternatives across toothpaste, toothbrushes, floss, interdental brushes, denture products and mouthwash. Stats SA reports 63.02 million people nationally, with 35.8 million people living in Gauteng, KwaZulu-Natal and Western Cape combined, creating dense retail markets where supermarket and pharmacy private labels can scale quickly. Household pressure is visible in labour data: Stats SA records 8.0 million unemployed people and 17.1 million employed people, reinforcing demand for lower-priced oral-care choices that retain acceptable quality and convenience. World Bank data records household final consumption expenditure at USD 259.30 billion, confirming a large retail consumption base where private-label penetration can expand through high-frequency necessities such as toothpaste and toothbrushes. Digital reach also supports retailer-owned brand discovery: Stats SA reports 96.1 out of every 100 households owning at least one mobile phone and 82.1 having internet access through any means. These conditions favour pharmacy and grocery chains that can combine loyalty programmes, online catalogues, multipack promotions and essential oral-hygiene ranges to capture budget-conscious shoppers without relying only on multinational brands.

Water Flossers

Water flossers represent a future growth opportunity within South Africa’s premium oral care market because they sit at the intersection of urbanization, digital retail access, orthodontic care, gum-health awareness and higher-income pharmacy shoppers. World Bank data records 40.77 million urban residents in South Africa, while Stats SA shows that Gauteng, KwaZulu-Natal and Western Cape together account for 35.8 million people, giving electric and device-led oral care a large addressable urban base. The same provinces also have stronger medical-aid coverage, with Western Cape at 25.4 and Gauteng at 21.3, supporting demand among consumers already linked to private healthcare and dental recommendation channels. Device discovery and online purchasing are supported by digital access: Stats SA reports 96.1 out of every 100 households owning at least one mobile phone and 82.1 having internet access through any means, while ICASA records South Africa at 103rd position globally for fixed broadband speed-test ranking out of 178 countries. Oral health need remains significant, as government communication highlights gum disease as affecting an estimated 90 out of every 100 South Africans at some point. This creates a clear route for water flossers through pharmacies, e-commerce, orthodontists and premium oral-hygiene bundles.

Future Outlook

The South Africa Oral Care Market is expected to expand steadily, supported by premiumization in sensitivity toothpaste, whitening, gum care and alcohol-free mouthwash. Growth will also be supported by pharmacy chains, digital retailing, children’s oral care and private-label expansion. Toothbrushes are expected to be among the fastest-growing product segments, while toothpaste will remain the anchor product for household penetration. Published South Africa oral care forecasts vary: Nexdigm Research indicates 4.6% CAGR to 2030, while Deep Market Insights indicates 6.96% CAGR across its forward forecast.

Major Players

- Colgate-Palmolive South Africa

- Haleon

- Procter & Gamble

- Kenvue

- Unilever

- Curaden South Africa

- Sunstar

- Jordan

- Philips

- Amka Products

- Clicks Private Label

- Dis-Chem Private Label

- Shoprite/Checkers Private Label

- Spar Private Label

- Total Smile

Key Target Audience

- Oral care product manufacturers

- FMCG companies

- Pharmacy retail chains

- Supermarket and hypermarket chains

- E-commerce and quick-commerce platforms

- Dental product distributors and importers

- Investments and venture capitalist firms

- Government and regulatory bodies (South African Health Products Regulatory Authority, Department of Health, South African Bureau of Standards, National Consumer Commission)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves building an ecosystem map of toothpaste, toothbrush, mouthwash, denture care, dental accessories and whitening product stakeholders. Variables include product mix, SKU price ladders, pharmacy shelf presence, supermarket penetration, e-commerce availability, fluoride compliance and private-label expansion.

Step 2: Market Analysis and Construction

Historical and current market data is compiled from published market research sources, retailer disclosures, product catalogues and pharmacy channel evidence. Market construction uses both top-down market sizing and bottom-up SKU-level mapping across pharmacy, grocery and online retail formats.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through interviews with oral care distributors, retail category managers, pharmacists, dentists and FMCG executives. These consultations help refine assumptions on toothpaste dominance, mouthwash penetration, sensitivity-care premiumization and private-label pricing pressure.

Step 4: Research Synthesis and Final Output

The final phase triangulates published market size data, retailer evidence and primary insights. The output validates segmentation, competitive positioning, growth drivers, future outlook and strategic recommendations for manufacturers, investors, distributors and channel partners in the South Africa Oral Care Market.

- Executive Summary

- Research Methodology (Market definitions and assumptions, SANS 1302 toothpaste compliance assumptions, oral hygiene SKU mapping, primary dentist/pharmacist interviews, retailer shelf audit, pharmacy channel checks, e-commerce price scraping, TAM/SAM/SOM modelling, top-down household oral care spend, bottom-up SKU velocity, limitations and future conclusions)

- Definition and Scope

- Market Genesis and Evolution

- Timeline of Major Brands and Retail Entry

- Business Cycle and Replenishment Frequency

- Supply Chain and Value Chain Analysis

- Import Dependence vs Local Manufacturing Footprint

- Role of Dentists, Pharmacists and Retail Chains in Brand Recommendation

- Growth Drivers (Sensitivity toothpaste adoption, alcohol-free mouthwash demand, dentist/pharmacist recommendation, pharmacy chain expansion, e-commerce penetration, family value packs, kids oral hygiene routines)

- Market Challenges(Price sensitivity, low dental visit frequency, counterfeit/imported grey-market SKUs, township accessibility gaps, premium SKU affordability, fluoride labelling compliance, exchange-rate impact on imports)

- Market Opportunities (Private-label oral care, water flossers, orthodontic care, seniors’ denture care, gum-health products, kids fluoride education, subscription replenishment, township micro-pack distribution)

- Market Trends(Charcoal and herbal claims, enamel repair, whitening kits, alcohol-free rinses, soft-bristle toothbrushes, eco-friendly brushes, refill and recyclable packaging, dentist-endorsed digital campaigns)

- Government Regulations and Standards (SANS 1302 toothpaste standard, Foodstuffs Cosmetics and Disinfectants Act, fluoride labelling, permissible pack volumes, cosmetic product safety, import documentation, consumer protection claims)

- SWOT Analysis(Brand trust, pharmacy reach, imported premium exposure, affordability pressure, private-label threat, oral health education whitespace)

- Stakeholder Ecosystem (Manufacturers, importers, distributors, retailers, pharmacists, dentists, dental associations, schools, medical aid/wellness programmes, e-commerce platforms)

- Porter’s Five Forces(Brand concentration, retailer bargaining power, private-label threat, substitutes, premiumization barriers, new entrant constraints)

- Competition Ecosystem(Multinational FMCG brands, therapeutic oral care brands, private labels, dental-specialist brands, online imported brands)

- By Value (2020-2025)

- By Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Per Capita Oral Care Spend (2020-2025)

- By Household Penetration (2020-2025)

- By Product Type (In Value%)

Toothpaste

Toothbrushes

Mouthwash and Dental Rinses

Floss and Interdental Care

Denture Care

Whitening and Cosmetic Oral Care

Kids Oral Care - By Formulation and Benefit Claim (In Value%)

Sensitivity relief

Cavity protection

Gum health

Plaque control

Enamel repair

Whitening

Fresh breath

Herbal/natural

Alcohol-free

Dentist-recommended - By Consumer Age Group (In Value%)

Toddlers

Children

Teenagers

Adults

Seniors

Denture users

Orthodontic users - By Price Positioning (In Value%)

Value packs

Mass-market SKUs

Mid-tier family packs

Premium therapeutic SKUs

Imported specialist SKUs

Private-label economy SKUs - By Pack Size and SKU Format (In Value%)

50ml toothpaste

75ml toothpaste

100ml toothpaste

Multi-packs

Travel packs

250ml mouthwash

500ml mouthwash

750ml mouthwash

Twin toothbrush packs

Replacement-head packs - By Distribution Channel (In Value%)

Supermarkets/hypermarkets

Pharmacies

Health and beauty chains

Independent pharmacies

E-commerce marketplaces

Dental clinics

Convenience stores

Informal township retail - By Retailer Format (In Value%)

Clicks

Dis-Chem

Shoprite/Checkers

Pick n Pay

Spar

Game/Makro

Takealot

Amazon South Africa

Independent pharmacy networks

Spaza/informal outlets - By Region (In Value%)

Gauteng

Western Cape

KwaZulu-Natal

Eastern Cape

Free State

Limpopo

Mpumalanga

North West

Northern Cape

- Market Share of Major Players (Value share, volume share, toothpaste share, toothbrush share, mouthwash share, pharmacy channel share, grocery channel share)

- Cross Comparison Parameters (Company overview, oral care portfolio breadth, toothpaste SKU count, mouthwash SKU count, sensitivity-care presence, whitening-care presence, kids oral care portfolio, denture-care portfolio, pharmacy distribution strength, grocery distribution strength, e-commerce availability, average price index, promotion frequency, local manufacturing/import model, dentist/pharmacist endorsement strategy, recent developments)

- SWOT Analysis of Major Players (Brand equity, therapeutic credibility, price architecture, retailer dependence, innovation pipeline, private-label exposure)

Pricing Analysis by SKU (75ml toothpaste, 100ml toothpaste, 500ml mouthwash, twin toothbrush packs, electric toothbrushes, denture adhesive, whitening kits, floss packs) - Detailed Profiles of Major Companies

Colgate-Palmolive South Africa

Haleon

Procter & Gamble

Kenvue

Unilever

Curaden South Africa

Sunstar

Jordan

Philips

Amka Products

Clicks Private Label

Dis-Chem Private Label

Shoprite/Checkers Private Label

Spar Private Label

Total Smile

- Household Demand and Utilization(Brushing frequency, family pack usage, children’s oral care routines, mouthwash adoption, interdental care gap)

- Purchasing Power and Budget Allocation(Value packs, promotion sensitivity, pharmacy rewards, bulk buying, premium therapeutic trade-up)

- Decision-Making Process(Dentist recommendation, pharmacist recommendation, brand trust, price promotion, retailer loyalty, flavour preference, pack size)

- Needs, Desires and Pain Points(Sensitivity relief, bleeding gums, whitening, fresh breath, kids compliance, denture comfort, affordable fluoride toothpaste)

- Consumer Cohort Analysis (Urban middle-income households, township value buyers, premium pharmacy shoppers, parents with young children, denture users, orthodontic users, online convenience shoppers)

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

- By Premiumization Index (2026-2035)

- By Channel Shift (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now