Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the South Africa warehousing market recorded an estimated value of USD ~ Billion according to logistics infrastructure and supply chain industry data from the Department of Trade Industry and Competition and national logistics associations. Demand is driven by expansion of organized retail distribution systems, rising e commerce fulfillment activity, and increasing investment in cold storage facilities supporting food and pharmaceutical supply chains. Warehousing infrastructure supports the storage and distribution of consumer goods, agricultural commodities, and industrial products across national and international logistics networks.

Johannesburg and the broader Gauteng region dominate the warehousing landscape due to their role as the country’s primary industrial and logistics hub connecting inland manufacturing centers with national road and rail freight corridors. Durban also maintains a major warehousing concentration because of its proximity to the Port of Durban which handles large volumes of containerized cargo for international trade. Cape Town hosts extensive warehousing infrastructure supporting agricultural exports, retail distribution operations, and temperature controlled logistics services for pharmaceutical and food supply chains.

Market Segmentation

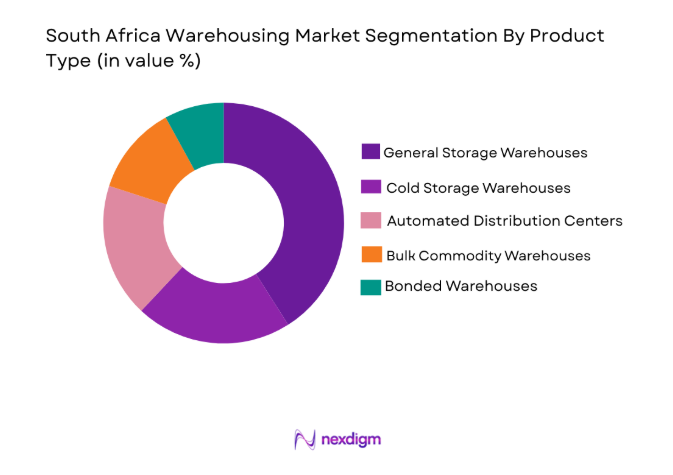

By Product Type

South Africa Warehousing market is segmented by product type into general storage warehouses, cold storage warehouses, automated distribution centers, bulk commodity warehouses, and bonded warehouses. Recently, general storage warehouses have a dominant market share due to factors such as widespread demand from retail supply chains, consumer goods distribution, manufacturing storage requirements, and broad infrastructure availability across major logistics corridors supporting national freight transportation and inventory consolidation operations.

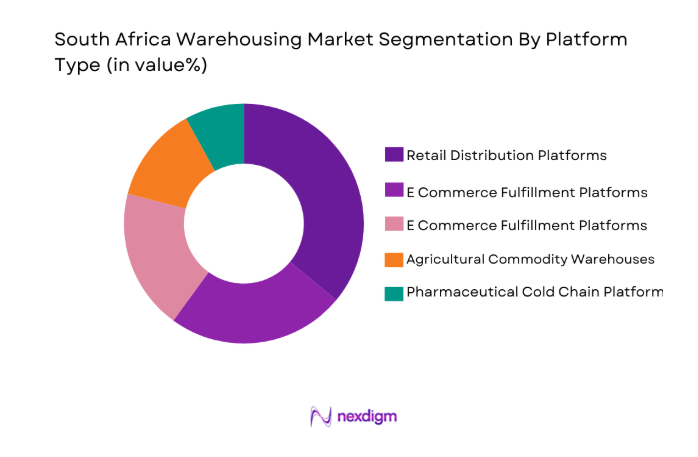

By Platform Type

South Africa Warehousing market is segmented by platform type into e commerce fulfillment platforms, retail distribution platforms, manufacturing logistics platforms, agricultural commodity platforms, and pharmaceutical cold chain platforms. Recently, retail distribution platforms have a dominant market share due to factors such as the presence of national supermarket chains, organized retail logistics networks, centralized distribution strategies, and continuous inventory replenishment systems supporting high consumer goods movement across the country.

Competitive Landscape

The South Africa warehousing market exhibits a moderately consolidated competitive structure where large logistics companies and integrated supply chain operators manage extensive warehouse networks across major logistics corridors. Market competition is shaped by infrastructure capacity, cold chain capabilities, automation technology adoption, and long term contracts with retailers and manufacturing companies. Large third party logistics providers dominate national distribution operations while specialized cold storage providers and e commerce fulfillment operators expand rapidly in response to growing demand for temperature controlled logistics and rapid order fulfillment services.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity |

| Imperial Logistics | 1969 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| Bidvest Panalpina Logistics | 1988 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| DSV South Africa | 1976 | Johannesburg | ~ | ~ | ~ | ~ | ~ |

| Kuehne+Nagel South Africa | 1890 | Schindellegi | ~ | ~ | ~ | ~ | ~ |

| Unitrans Supply Chain Solutions | 1962 | Stellenbosch | ~ | ~ | ~ | ~ | ~ |

South Africa Warehousing Market Analysis

Growth Drivers

Expansion of E Commerce Distribution Infrastructure

expansion of online retail ecosystems significantly increases demand for warehousing infrastructure capable of storing large volumes of consumer goods and enabling rapid order fulfillment across urban markets. Major e commerce platforms depend on strategically located distribution centers to manage inventory flows between suppliers retailers and consumers. Automated sorting systems robotics assisted storage technologies and digital warehouse management systems improve operational efficiency and enable companies to process thousands of orders daily. Logistics providers therefore expand fulfillment networks near major metropolitan areas where consumer demand remains concentrated. Urban logistics hubs enable faster delivery timelines and reduce transportation costs for last mile operations. Retailers increasingly integrate online and offline distribution strategies requiring warehouses to function as centralized inventory hubs supporting both store replenishment and digital commerce channels. This operational shift significantly expands warehouse capacity requirements across South Africa’s logistics sector. As digital retail penetration grows further warehousing infrastructure continues evolving into technologically advanced fulfillment ecosystems capable of supporting high volume parcel processing and nationwide distribution networks.

Growth in Organized Retail and National Distribution Networks

expansion of supermarket chains and organized retail distribution systems significantly increases demand for large scale warehousing infrastructure across South Africa. Major retail companies operate centralized distribution centers responsible for managing inventory flows between suppliers manufacturers and retail stores located across multiple provinces. These warehouses consolidate large volumes of consumer products including food beverages household goods electronics and pharmaceuticals. Centralized logistics systems enable retailers to improve inventory control reduce transportation inefficiencies and maintain consistent product availability across store networks. Cold storage facilities also expand to support food distribution operations for perishable goods requiring temperature controlled logistics environments. Retail distribution warehouses located near major transportation corridors facilitate efficient movement of goods to supermarkets convenience stores and wholesale outlets across the country. Growing urbanization and consumer spending further strengthen retail supply chain activity which requires scalable warehousing capacity capable of supporting high frequency product distribution cycles throughout the national retail ecosystem.

Market Challenges

Electricity Supply Instability Affecting Warehouse Operations

unreliable electricity supply across industrial zones significantly challenges warehouse operators that depend heavily on automated equipment refrigeration systems and digital inventory management platforms. Warehouses storing perishable products such as food pharmaceuticals and agricultural commodities require continuous refrigeration to maintain product integrity. Frequent power disruptions therefore increase operational costs as companies invest in backup generators fuel systems and alternative energy solutions. Cold storage facilities particularly face substantial financial pressure because temperature fluctuations can compromise stored goods. Logistics providers must also maintain uninterrupted power supply for automated sorting conveyors robotics equipment and warehouse management software systems responsible for coordinating inventory movements. Energy instability therefore reduces operational efficiency and increases maintenance costs across warehouse networks. Companies increasingly explore renewable energy systems and battery storage technologies to mitigate energy risk but these infrastructure investments require significant capital expenditure which many mid sized logistics firms struggle to afford.

High Infrastructure and Land Development Costs in Logistics Corridors

development of large warehousing facilities requires substantial capital investment due to land acquisition costs construction expenses and installation of advanced logistics technologies. Industrial land located near major transportation corridors including Johannesburg Durban and Cape Town commands high property prices because of strong demand from logistics providers manufacturing companies and retail distributors. Warehouse developers must also invest heavily in specialized infrastructure including automated storage systems refrigeration units high capacity loading docks and integrated warehouse management software. Financing such large infrastructure projects becomes difficult for smaller logistics operators that lack access to large investment capital. Long regulatory approval processes and zoning compliance requirements further increase development timelines and project costs. As demand for modern distribution centers grows logistics companies must carefully evaluate investment strategies to balance infrastructure expansion with financial sustainability across evolving supply chain networks.

Opportunities

Expansion of Cold Chain Infrastructure for Food and Pharmaceutical Logistics

Increasing demand for temperature controlled logistics solutions creates major opportunities for cold storage warehouse development across South Africa. Agricultural exporters pharmaceutical distributors and food processing companies require reliable cold chain systems capable of preserving product quality throughout storage and transportation stages. Cold warehouses equipped with advanced refrigeration technologies allow companies to maintain strict temperature conditions required for vaccines pharmaceuticals fresh produce and processed food products. Growth of pharmaceutical manufacturing and international food exports further strengthens demand for temperature controlled storage facilities located near airports seaports and agricultural production regions. Logistics providers therefore invest in modern cold storage warehouses integrated with digital monitoring systems capable of maintaining precise temperature control throughout the supply chain.

Development of Smart Automated Warehousing Facilities

technological advancement in warehouse automation systems creates significant opportunities for logistics companies to improve operational efficiency and storage capacity. Robotics assisted picking systems automated guided vehicles and advanced warehouse management software allow companies to manage large inventory volumes with greater accuracy and speed. Smart warehouses integrate real time inventory tracking technologies data analytics platforms and artificial intelligence driven logistics planning tools to optimize storage utilization and order fulfillment processes. Adoption of automation also reduces labor dependency while improving productivity across large distribution centers. As supply chains become increasingly digitalized smart warehousing infrastructure will play a crucial role in supporting efficient national logistics networks and high volume retail distribution operations.

Future Outlook

The South Africa warehousing market is expected to experience steady expansion as logistics infrastructure continues evolving to support national trade distribution networks and digital commerce supply chains. Growth in retail logistics, expansion of cold chain facilities, and adoption of automation technologies will strengthen warehouse capacity across major logistics hubs. Increasing investments in smart warehouses and regional distribution centers will further improve supply chain efficiency while supporting rising demand for rapid order fulfillment and temperature controlled logistics services.

Major Players

- Imperial Logistics

- Bidvest Panalpina Logistics

- DSV South Africa

- Kuehne+Nagel South Africa

- Unitrans Supply Chain Solutions

- Grindrod Logistics

- Barloworld Logistics

- Value Logistics

- DB Schenker South Africa

- Bolloré Logistics South Africa

- DHL Supply Chain South Africa

- Shoprite Checkers Distribution

- Takealot Fulfillment Solutions

- Super Group Supply Chain

- DP World Logistics South Africa

Key Target Audience

- Retail and E-commerce Companies

- Manufacturing and Industrial Corporations

- Agricultural Export Companies

- Pharmaceutical Distribution Firms

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Logistics Infrastructure Developers

Research Methodology

Step 1: Identification of Key Variables

Primary research identifies key warehousing infrastructure variables including storage capacity, facility automation levels, cold chain infrastructure availability, logistics corridor connectivity, and demand patterns across retail manufacturing and export supply chains within South Africa’s distribution ecosystem.

Step 2: Market Analysis and Construction

Secondary data from government trade statistics logistics infrastructure reports industry associations and company disclosures is analyzed to construct market size estimates and segmentation structures representing warehouse demand across industrial retail and export logistics sectors.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics managers supply chain consultants infrastructure developers and warehouse operators validate market assumptions and provide insights on technology adoption infrastructure investment trends and operational challenges within national logistics networks.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights are synthesized to produce the final research framework combining market size analysis segmentation competitive benchmarking and strategic outlook assessments for the South Africa warehousing industry.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E-commerce Distribution Networks

Growth in Retail Supply Chain Infrastructure Development

Rising Demand for Cold Storage for Food and Pharmaceutical Logistics - Market Challenges

High Infrastructure Development and Land Acquisition Costs

Electricity Supply Instability Affecting Warehouse Operations

Limited Transportation Infrastructure in Secondary Regions - Market Opportunities

Development of Smart Automated Warehousing Facilities

Expansion of Cold Chain Logistics for Food Exports

Investment in Urban Micro Fulfillment Warehouses - Trends

Adoption of Warehouse Automation and Robotics Systems

Development of E-commerce Fulfillment Mega Warehouses - Government Regulations

Logistics Infrastructure Development Policies

Industrial Zoning and Warehouse Development Regulations

Food Safety and Cold Chain Compliance Standards - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

General Storage Warehouses

Cold Storage Warehouses

Automated High Bay Warehouses

Distribution Fulfillment Centers

Bulk Commodity Storage Facilities - By Platform Type (In Value%)

E-commerce Fulfillment Platforms

Retail Distribution Platforms

Industrial Manufacturing Storage Platforms

Agricultural Commodity Storage Platforms

Pharmaceutical Logistics Platforms - By Fitment Type (In Value%)

Built-to-Suit Warehousing Facilities

Shared Multi Client Warehousing

Dedicated Contract Warehousing

Automated Smart Warehousing - By End User Segment (In Value%)

Retail and E-commerce Companies

Manufacturing and Industrial Firms

Agriculture and Food Processing Companies

- Market Share Analysis

- Cross Comparison Parameters (Warehouse Capacity, Automation Level, Cold Storage Capability, Geographic Coverage, Client Industry Focus, Technology Integration, Pricing Structure)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Imperial Logistics

Bidvest Panalpina Logistics

Bolloré Logistics South Africa

DP World Logistics South Africa

Unitrans Supply Chain Solutions

Kuehne+Nagel South Africa

DB Schenker South Africa

DSV South Africa

Value Logistics

UTi South Africa

Grindrod Logistics

Barloworld Logistics

Super Group Supply Chain

Takealot Fulfillment Solutions

Shoprite Checkers Distribution

- Retailers Increasing Demand for Regional Distribution Hubs

- Manufacturers Expanding Storage Capacity Near Industrial Corridors

- Agricultural Exporters Requiring Temperature Controlled Storage Facilities

- E-commerce Platforms Investing in Automated Fulfillment Infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now