Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Korea cloud infrastructure market is valued at approximately USD ~ billion based on a recent historical assessment, driven by hyperscale data center expansion, enterprise cloud migration, and national digital platform initiatives. Strong demand from telecommunications, finance, and manufacturing sectors supports investment in compute, storage, and networking infrastructure. Growth of AI and data-intensive workloads further accelerates deployment of high-performance servers and advanced networking systems across domestic cloud and colocation facilities operated by global and local providers.

Seoul metropolitan region dominates the South Korea cloud infrastructure market due to concentration of hyperscale data centers, enterprise headquarters, and advanced connectivity infrastructure. Gyeonggi Province hosts large data center campuses benefiting from land availability and proximity to fiber networks and power supply. Incheon supports subsea cable landing stations and international connectivity. National digital transformation programs and enterprise cloud adoption reinforce regional leadership in cloud infrastructure deployment and operational scale across the country.

Market Segmentation

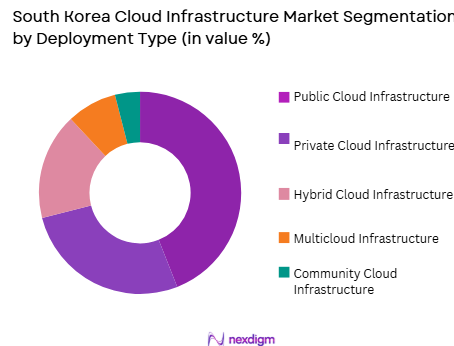

By Deployment Type

South Korea Cloud Infrastructure market is segmented by product type into public cloud infrastructure, private cloud infrastructure, hybrid cloud infrastructure, multicloud infrastructure, and community cloud infrastructure. Recently, public cloud infrastructure has a dominant market share due to factors such as hyperscale provider expansion, enterprise migration to scalable compute platforms, and strong ecosystem of cloud-native services. Global and domestic cloud operators continue building large data centers to support SaaS, AI, and digital platform workloads. Public cloud offers elasticity, cost efficiency, and rapid deployment compared with private environments. Government and enterprise digital transformation strategies prioritize public cloud adoption. Integration with AI and analytics services further increases demand for hyperscale public cloud infrastructure in South Korea.

By End-Use Industry

South Korea Cloud Infrastructure market is segmented by end-use industry into telecommunications, financial services, manufacturing, public sector, and media and gaming. Recently, telecommunications has a dominant market share due to factors such as nationwide 5G network virtualization, edge cloud deployment, and large-scale subscriber data processing requirements. Telecom operators deploy distributed cloud infrastructure to support network functions virtualization and digital services. Integration of AI-driven network analytics and content delivery platforms increases infrastructure demand. Telecom firms also act as cloud providers offering enterprise services. These factors position telecommunications as the largest consumer of cloud infrastructure capacity in South Korea.

Competitive Landscape

The South Korea cloud infrastructure market is moderately consolidated with strong presence of global hyperscale providers and domestic telecom-cloud operators. Large data center investments and long-term enterprise contracts shape competitive positioning. Partnerships between cloud platforms, telecom networks, and hardware vendors determine infrastructure scale. Domestic firms leverage connectivity and regulatory alignment, while global providers lead in platform breadth and hyperscale efficiency.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Data Center Footprint in Korea |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| 1998 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ | |

| Naver Cloud | 2017 | Seongnam, South Korea | ~ | ~ | ~ | ~ | ~ |

| KT Cloud | 2022 | Seoul, South Korea | ~ | ~ | ~ | ~ | ~ |

South Korea Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise Digital Transformation and Cloud Migration Acceleration

South Korea’s enterprises across finance, manufacturing, telecommunications, and retail sectors are rapidly migrating applications and data to cloud platforms to enhance agility, scalability, and digital competitiveness, creating sustained demand for cloud infrastructure capacity. Legacy IT modernization programs require replacement of on-premise servers with virtualized and containerized cloud environments. Digital services such as mobile banking, e-commerce, and smart factory systems rely on elastic compute and storage resources. Enterprises seek cost optimization through pay-as-you-go infrastructure consumption models. Adoption of cloud-native architectures increases demand for distributed data center capacity. Hybrid integration with existing systems expands infrastructure complexity. Data analytics and AI workloads further elevate compute intensity. Regulatory support for digital transformation encourages enterprise cloud adoption. Domestic cloud providers and hyperscalers expand local regions to meet enterprise demand. Continuous migration of mission-critical workloads sustains long-term growth of cloud infrastructure in South Korea.

AI, Data-Intensive Workloads, and Hyperscale Data Center Expansion

Rapid proliferation of artificial intelligence, big data analytics, and digital content services in South Korea is driving hyperscale data center construction and high-performance cloud infrastructure deployment nationwide. AI training and inference workloads require GPU-accelerated compute clusters and high-throughput storage systems. Streaming, gaming, and metaverse platforms generate massive data processing demand. Hyperscale cloud providers invest in large facilities with advanced networking and cooling systems. Telecom edge computing integration expands distributed cloud nodes. Enterprises deploy AI services on cloud platforms to avoid capital investment. Growth of generative AI applications increases resource consumption per workload. Data localization requirements favor domestic data center expansion. Continuous increase in digital platform usage drives infrastructure scaling. These factors collectively accelerate hyperscale cloud infrastructure growth across South Korea.

Market Challenges

Data Sovereignty, Security Compliance, and Regulatory Constraints

Cloud infrastructure deployment in South Korea must comply with stringent data protection, localization, and cybersecurity regulations that affect architecture design and operational practices. Sensitive financial, healthcare, and public sector data require domestic storage and processing. Compliance frameworks increase infrastructure complexity and certification costs. Cloud providers must maintain high security standards and audit readiness. Regulatory approvals can delay deployment of new regions or services. Enterprises may restrict cloud adoption for critical workloads due to compliance concerns. Cross-border data transfer limitations affect global cloud architectures. Security breach risks increase operational requirements. These constraints create barriers to rapid scaling of cloud infrastructure. Providers must invest heavily in compliant infrastructure and governance systems.

Power Availability, Land Constraints, and Data Center Sustainability

Expansion of hyperscale cloud infrastructure in South Korea faces constraints related to limited land availability near urban demand centers and high power consumption of data centers. Suitable sites with access to reliable electricity and cooling resources are scarce. Data centers require large contiguous land parcels and grid capacity. Urban density increases land costs and zoning complexity. Power demand of hyperscale facilities strains regional grids. Sustainability targets require energy-efficient design and renewable integration. Environmental regulations govern heat and water usage. Infrastructure expansion timelines are extended by permitting processes. These factors limit speed of new cloud facility deployment. Balancing growth with sustainability remains a key challenge.

Opportunities

Development of Sovereign Cloud and Domestic Hyperscale Platforms

South Korea has opportunity to expand sovereign cloud infrastructure operated by domestic providers to ensure data governance, security control, and technological independence. Government and regulated industries increasingly prefer local cloud platforms compliant with national standards. Domestic hyperscale providers can expand data center regions and cloud services portfolios. Integration with national digital platforms and public sector systems strengthens demand. Sovereign cloud initiatives encourage investment in domestic infrastructure capacity. Partnerships between telecom operators and cloud firms accelerate deployment. Local platforms can tailor services to Korean language and regulatory requirements. Expansion of sovereign cloud reduces reliance on foreign providers. Domestic ecosystem growth supports long-term infrastructure demand. This opportunity aligns with national digital sovereignty objectives.

Regional Cloud Hub Development and Cross-Border Digital Services

South Korea can position itself as a regional cloud infrastructure hub serving Northeast Asia by leveraging advanced connectivity, semiconductor ecosystem, and digital economy maturity. Subsea cable connectivity through Incheon enables international data traffic flows. Cloud providers can deploy regional availability zones serving neighboring markets. Cross-border digital services such as gaming, fintech, and media platforms require regional infrastructure. Data center investment for regional workloads expands domestic capacity. Partnerships with global cloud firms support hub development. Export of cloud services enhances digital economy growth. Regional positioning attracts multinational enterprises. This opportunity strengthens South Korea’s role in global cloud infrastructure networks.

Future Outlook

South Korea cloud infrastructure market is expected to expand steadily as enterprise cloud migration, AI workloads, and hyperscale data center construction accelerate nationwide. Government digital policies and sovereign cloud initiatives will support domestic infrastructure investment. Advances in high-density computing and energy-efficient data center design will enable scaling. Increasing digital platform adoption across industries will sustain long-term demand for cloud infrastructure capacity.

Major Players

- Amazon Web Services

- Microsoft

- Naver Cloud

- KT Cloud

- Samsung SDS

- LG CNS

- SK Telecom

- NHN Cloud

- Oracle

- IBM

- Alibaba Cloud

- Equinix

- Digital Realty

- CyrusOne

Key Target Audience

- Hyperscale cloud providers

- Telecommunications operators

- Data center operators

- Enterprise IT service providers

- Financial institutions

- Investments and venture capitalist firms

- Government and regulatory bodies

- Digital platform companies

Research Methodology

Step 1: Identification of Key Variables

Key variables include cloud infrastructure spending, data center capacity, enterprise cloud adoption rates, hyperscale deployment activity, and industry demand patterns. Variables are mapped across deployment models and industries to define market structure.

Step 2: Market Analysis and Construction

Supply-side analysis evaluates cloud provider infrastructure expansion and data center construction, while demand-side analysis examines enterprise migration and digital workload growth. Data triangulation constructs market size and segmentation estimates.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from cloud providers, telecom operators, and data center firms validate assumptions on infrastructure growth, regulatory impact, and technology adoption. Feedback refines segmentation shares and competitive positioning.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights are synthesized into market forecasts, competitive analysis, and strategic outlook. Consistency checks ensure alignment across market size, segmentation, and trend narratives.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Advanced digital economy and cloud-native enterprise adoption

Strong hyperscale and telecom data center expansion

National investment in sovereign and AI cloud platforms - Market Challenges

Strict data sovereignty and compliance requirements

High data center energy and cooling demand

Urban land and power constraints for hyperscale sites - Market Opportunities

Industry cloud platforms for manufacturing and finance

Sovereign cloud for government and regulated sectors

Edge cloud for low-latency digital services and 5G - Trends

Shift toward multi-cloud and hybrid architectures

Adoption of hyperconverged and software-defined infrastructure

Integration of edge and telecom cloud environments - Government regulations

Data protection and localization regulations

Cloud security and certification standards

Digital government and sovereign cloud initiatives - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Platforms

Cloud Storage Infrastructure

Cloud Networking Infrastructure - By Platform Type (In Value%)

Hyperscale Data Centers

Colocation Facilities

Enterprise On-Premise Cloud

Telecom Cloud Platforms

Edge Cloud Infrastructure - By Fitment Type (In Value%)

Greenfield Cloud Deployment

Data Center Cloud Retrofit

Hyperconverged Infrastructure Integration

Containerized Cloud Modules

Cloud Expansion Clusters - By End User Segment (In Value%)

Financial Services Institutions

Telecommunications Providers

E-commerce and Internet Platforms

Government and Public Sector

Manufacturing and Industrial Firms - By Procurement Channel (In Value%)

Direct Hyper scaler Contracts

Cloud Service Providers

System Integrators and MSPs

Telecom Operator Partnerships

Public Sector Procurement

- Market Share Analysis

- Cross Comparison Parameters (Compute Density, Storage Performance Scalability, Network Throughput Capacity, Data Center Power Efficiency, Cloud Platform Integration, Multi-Cloud Interoperability, Security and Compliance Certifications, Automation and Orchestration Capability, Edge Cloud Integration, Service Availability SLA, Data Sovereignty Controls, AI and HPC Cloud Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Naver Cloud

Kakao Enterprise

KT Cloud

NHN Cloud

Samsung SDS

LG CNS

SK Telecom

KT Corporation

LG Uplus

Amazon Web Services Korea

Microsoft Azure Korea

Google Cloud Korea

Oracle Cloud Korea

Equinix Korea

Digital Realty Korea

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now