Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the South Korea Cold Chain Logistics market reached approximately USD ~ billion, supported by expanding pharmaceutical distribution networks, rising demand for temperature-controlled food logistics, and strong seafood export infrastructure. The Ministry of Oceans and Fisheries reported seafood exports valued above USD ~ billion, while the Korea Agro Fisheries and Food Trade Corporation recorded processed food exports exceeding USD ~ billion, requiring specialized refrigerated logistics. Rapid expansion of e-commerce grocery distribution and pharmaceutical bioproduct transportation further strengthens the requirement for advanced cold storage and refrigerated transportation systems across national supply chains.

Major cold chain logistics activities are concentrated around Seoul Metropolitan Area, Incheon, and Busan due to advanced port infrastructure, pharmaceutical manufacturing clusters, and dense urban consumption centers. Busan functions as a critical maritime gateway for seafood exports and international refrigerated cargo movements. Incheon supports temperature controlled pharmaceutical imports and exports through its international airport logistics facilities. Seoul dominates domestic food distribution because of extensive retail networks and high population density, while surrounding Gyeonggi Province hosts large automated cold storage facilities supporting national food and healthcare logistics networks.

Market Segmentation

By Product Type

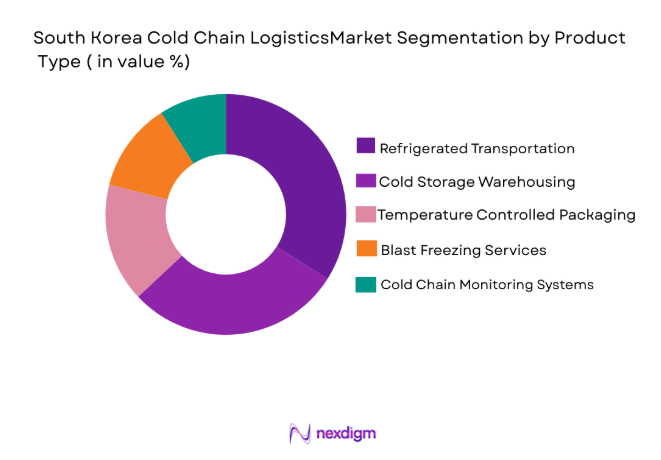

South Korea Cold Chain Logistics market is segmented by product type into cold storage warehousing, refrigerated transportation, temperature controlled packaging, blast freezing services, and cold chain monitoring systems. Recently, refrigerated transportation has a dominant market share due to strong demand from food distribution networks, pharmaceutical shipments, and seafood export logistics. The country’s advanced retail and e commerce sectors require fast temperature controlled delivery between ports, processing facilities, warehouses, and urban supermarkets. Refrigerated trucking fleets and intercity distribution networks therefore play a critical role in maintaining product quality and ensuring timely supply of perishable goods.

By Platform Type

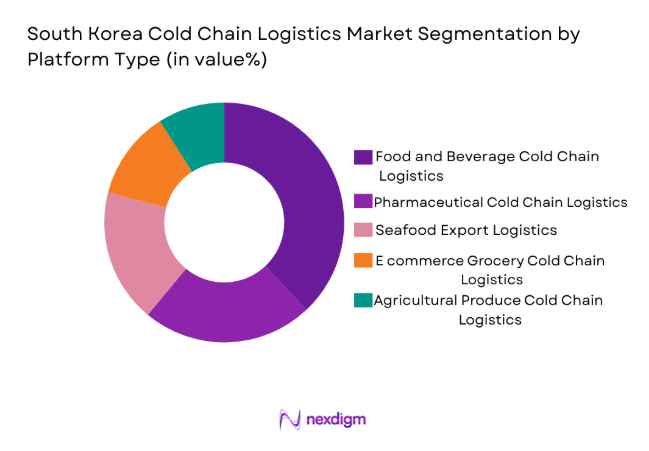

South Korea Cold Chain Logistics market is segmented by platform type into food and beverage cold chain logistics, pharmaceutical cold chain logistics, seafood export logistics, agricultural produce cold chain logistics, and e commerce grocery cold chain logistics. Recently, food and beverage cold chain logistics has a dominant market share due to strong supermarket networks, increasing consumption of frozen and processed foods, and widespread convenience store distribution systems. National food supply chains depend heavily on refrigerated storage and transportation to maintain freshness across urban retail outlets and restaurant supply channels.

Competitive Landscape

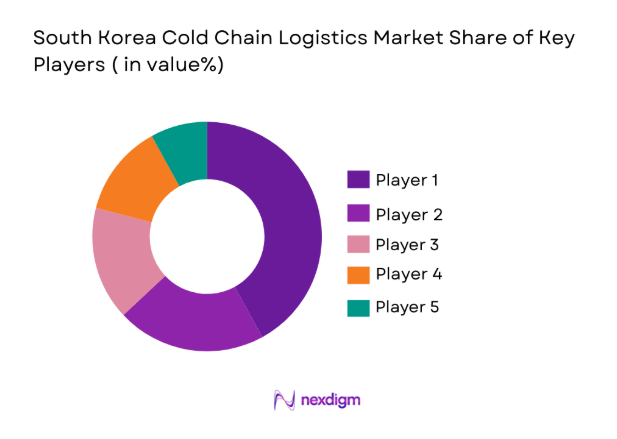

The South Korea Cold Chain Logistics market is moderately consolidated with several large logistics groups controlling extensive refrigerated storage infrastructure and transportation fleets. Leading logistics companies invest heavily in automated cold storage facilities, temperature monitoring technology, and nationwide distribution networks. Global logistics providers also maintain strong operational presence through partnerships with domestic distributors and pharmaceutical supply chain operators. Strategic investments in smart warehousing, automation, and IoT based temperature monitoring systems strengthen competitive differentiation across the market.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cold Storage Capacity |

| CJ Logistics | 1930 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Lotte Global Logistics | 1988 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Hanjin Transportation | 1945 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Hyundai Glovis | 2001 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Dongwon Logistics | 1973 | Seoul | ~ | ~ | ~ | ~ | ~ |

South Korea Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of E Commerce Grocery and Online Food Distribution Networks

Rapid expansion of digital grocery platforms and convenience retail chains significantly strengthens demand for temperature controlled logistics services across South Korea. Online grocery delivery platforms require reliable cold storage facilities and refrigerated transportation to maintain product quality during last mile delivery operations. Urban consumers increasingly purchase frozen meals, dairy products, seafood, and fresh produce through mobile commerce applications, which increases daily shipment volumes requiring precise temperature management. Logistics providers therefore invest in automated cold warehouses, urban micro fulfillment centers, and high capacity refrigerated trucking fleets designed for rapid distribution. South Korea’s advanced retail ecosystem includes thousands of convenience stores and supermarkets that require continuous replenishment of chilled and frozen food products. Distribution companies operate sophisticated cold chain infrastructure connecting food manufacturers, import terminals, warehouses, and retail outlets across metropolitan areas. Integrated logistics management systems monitor temperature conditions throughout transportation and storage processes, ensuring regulatory compliance and food safety standards. Growing consumer preference for fresh packaged foods and ready to eat meal solutions further increases the need for efficient cold chain logistics networks capable of maintaining product freshness during transportation and distribution activities.

Growth of Biopharmaceutical Manufacturing and Temperature Controlled Healthcare Logistics

South Korea has emerged as a major global hub for pharmaceutical and biotechnology manufacturing, which significantly increases demand for temperature controlled healthcare logistics services. Biopharmaceutical products including vaccines, biologic medicines, and specialty drugs require precise temperature control during storage and transportation to maintain chemical stability and therapeutic effectiveness. Pharmaceutical companies rely on specialized logistics providers capable of operating validated cold storage facilities and GDP compliant distribution networks. Healthcare supply chains therefore integrate temperature monitoring systems, insulated packaging technologies, and specialized refrigerated transportation solutions designed for pharmaceutical shipments. Major biotechnology clusters located in Incheon, Songdo, and Seoul support large scale pharmaceutical manufacturing and international drug exports. Pharmaceutical logistics providers collaborate with hospitals, distributors, and research laboratories to maintain secure and compliant cold chain transportation for sensitive medical products. The growth of biotechnology exports and international clinical trial logistics further increases the requirement for advanced cold chain distribution infrastructure. These developments collectively strengthen long term demand for specialized cold chain logistics services within the pharmaceutical and healthcare sectors.

Market Challenges

High Energy Consumption and Operating Costs of Refrigerated Infrastructure

Cold storage warehouses and refrigerated transportation systems require substantial electricity consumption to maintain stable temperature conditions for perishable goods and pharmaceutical products. Refrigeration compressors, insulated warehouse facilities, and specialized cooling equipment operate continuously, which significantly increases operating expenses for logistics providers. Rising energy costs and environmental sustainability requirements further increase the financial burden associated with operating large temperature controlled logistics facilities. Cold storage warehouses require advanced insulation materials, backup power systems, and redundant refrigeration equipment to prevent temperature fluctuations that could damage stored goods. Logistics companies must also invest in monitoring technology capable of tracking temperature stability throughout storage and transportation processes. These infrastructure requirements increase capital expenditure for warehouse construction, equipment installation, and fleet modernization. Smaller logistics providers may face financial barriers when attempting to expand cold chain operations due to the high cost of refrigeration infrastructure. Additionally, stricter environmental regulations regarding energy efficiency and carbon emissions require companies to adopt advanced refrigeration technologies, further increasing operational complexity within the cold chain logistics sector.

Urban Land Constraints for Large Cold Storage Infrastructure Development

The construction of large temperature controlled warehouses requires significant land availability and specialized infrastructure that can support heavy refrigeration equipment and distribution operations. South Korea’s densely populated metropolitan areas limit the availability of suitable land parcels for large scale cold storage facility development. Logistics companies often face zoning restrictions, land acquisition costs, and regulatory approval procedures when planning new refrigerated distribution centers near major consumption markets. Urban land scarcity increases property prices around logistics hubs located near ports, airports, and industrial zones. Cold chain operators therefore face challenges when attempting to build large automated warehouses capable of supporting national food distribution networks. Limited land availability also restricts the expansion of last mile cold chain distribution centers required by e commerce grocery platforms. Companies may need to invest in vertical warehouse structures or satellite distribution facilities to optimize space utilization. These infrastructure constraints complicate long term planning for cold chain logistics providers seeking to expand capacity while maintaining proximity to major consumer markets.

Opportunities

Expansion of International Seafood Export Logistics and Temperature Controlled Trade Corridors

South Korea maintains a strong seafood processing and export industry that relies heavily on efficient cold chain logistics to deliver fresh and frozen seafood products to international markets. Export oriented seafood processors require temperature controlled storage facilities and refrigerated transport systems capable of maintaining product freshness during international shipping operations. Maritime ports and airport cargo terminals therefore play a critical role in supporting seafood export logistics infrastructure. Logistics providers continue expanding refrigerated container handling capacity and temperature controlled warehouse facilities near export processing zones. International seafood trade corridors require reliable cold chain systems that can maintain consistent temperatures from harvesting locations to overseas retail markets. Global demand for premium seafood products such as tuna, crab, and shellfish further strengthens the importance of advanced cold chain infrastructure supporting export logistics. Shipping companies and freight forwarders collaborate with cold storage operators to provide integrated refrigerated cargo transportation services. These developments create long term growth opportunities for logistics providers capable of supporting high value seafood export supply chains.

Adoption of Smart Cold Chain Technologies and Automated Temperature Monitoring Systems

The integration of advanced digital technologies within cold chain logistics operations presents significant opportunities for efficiency improvements and service differentiation. Smart sensors, IoT enabled monitoring systems, and cloud based logistics platforms allow real time tracking of temperature conditions during transportation and storage processes. Logistics providers deploy automated monitoring systems capable of detecting temperature deviations and triggering alerts that prevent product spoilage. Data analytics platforms also allow companies to optimize warehouse operations, transportation routes, and refrigeration energy consumption. Pharmaceutical logistics providers particularly benefit from digital monitoring systems that ensure compliance with strict regulatory requirements for drug storage and distribution. Automated cold warehouses equipped with robotics and intelligent storage systems further improve operational efficiency and reduce labor requirements. These technological developments enable logistics companies to provide higher reliability and transparency across temperature controlled supply chains. As digital logistics solutions continue expanding across the industry, technology adoption creates significant competitive advantages for cold chain operators capable of implementing smart logistics infrastructure.

Future Outlook

The South Korea Cold Chain Logistics market is expected to expand steadily over the coming years due to increasing demand from pharmaceutical distribution, seafood exports, and e commerce grocery delivery networks. Technological advancements in automated warehousing, IoT based temperature monitoring, and smart logistics platforms will improve operational efficiency across supply chains. Government initiatives supporting food safety standards and pharmaceutical distribution infrastructure will further strengthen cold chain logistics capabilities. Growing consumer demand for fresh and frozen foods will continue driving investment in advanced refrigerated transportation and storage infrastructure.

Major Players

- CJ Logistics

- Lotte Global Logistics

- Hanjin Transportation

- Hyundai Glovis

- Dongwon Logistics

- Korea Cold Storage

- Hyosung Logistics

- CJ Freshway Logistics

- Orion Logistics

- LF Logistics Korea

- Kerry Logistics Korea

- Maersk Logistics Korea

- DB Schenker Korea

- DHL Supply Chain Korea

- Kuehne + Nagel Korea

Key Target Audience

- Pharmaceutical and biotechnology companies

- Food and beverage manufacturers

- Seafood export companies

- E-commerce grocery platforms

- Logistics and cold storage infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Researchers identify key variables including cold storage capacity, refrigerated transportation infrastructure, pharmaceutical logistics demand, seafood export flows, and food retail distribution networks influencing the South Korea cold chain logistics sector.

Step 2: Market Analysis and Construction

Primary data from logistics companies, government trade agencies, and port authorities is combined with secondary research to construct an integrated model representing national cold chain logistics infrastructure and operational capacity.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics operators, cold storage facility managers, and pharmaceutical supply chain specialists validate market assumptions and provide insights regarding infrastructure investments and technology adoption.

Step 4: Research Synthesis and Final Output

Collected information is synthesized into comprehensive market insights supported by trade data, infrastructure assessments, and industry expert validation to ensure accuracy and reliability of final market analysis.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E-commerce Grocery and Online Food Delivery Platforms

Rising Demand for Pharmaceutical and Biologics Cold Chain Distribution

Increasing Seafood and Processed Food Export Activities - Market Challenges

High Infrastructure Investment and Energy Consumption in Cold Storage Facilities

Operational Complexity in Maintaining Consistent Temperature Control

Limited Availability of Urban Land for Large Cold Storage Facilities - Market Opportunities

Expansion of Biopharmaceutical Manufacturing and Vaccine Distribution Networks

Growth of Cross Border Cold Chain Trade for Seafood and Perishable Foods

Development of Smart Temperature Monitoring and IoT Enabled Logistics Systems - Trends

Adoption of Automated Cold Storage Warehouses and Robotics

Integration of Real Time Temperature Monitoring and Data Analytics - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Cold Storage Warehousing

Refrigerated Transportation

Temperature Controlled Packaging

Blast Freezing and Processing Systems

Cold Chain Monitoring and Tracking Systems - By Platform Type (In Value%)

Pharmaceutical Cold Chain Logistics

Food and Beverage Cold Chain Logistics

Seafood and Meat Cold Chain Logistics

Ecommerce Grocery Cold Chain Logistics

Agricultural Produce Cold Chain Logistics - By Fitment Type (In Value%)

Integrated Cold Chain Logistics Services

Third Party Cold Storage Services

Dedicated Contract Logistics

On Demand Refrigerated Logistics - By End User Segment (In Value%)

Food Processing and Retail Companies

Pharmaceutical and Biotechnology Companies

Ecommerce Grocery and Food Delivery Platforms

- Market Share Analysis

- Cross Comparison Parameters (Cold Storage Capacity, Refrigerated Fleet Size, Geographic Distribution Network, Temperature Monitoring Technology, Industry Specialization, Logistics Automation Level, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

CJ Logistics

Lotte Global Logistics

Hanjin Transportation

Hyundai Glovis

Dongwon Logistics

Korea Cold Storage

Hyosung Logistics

CJ Freshway Logistics

Orion Logistics

LF Logistics Korea

Kerry Logistics Korea

Maersk Logistics Korea

DB Schenker Korea

DHL Supply Chain Korea

Kuehne + Nagel Korea

- Food retailers increasingly require reliable refrigerated distribution

- networks to support fresh and frozen product supply across supermarkets and convenience stores

- Pharmaceutical manufacturers depend on validated temperature

- controlled logistics for vaccine distribution and biologic drug transportation

- Ecommerce grocery platforms require urban cold storage hubs and rapid last mile refrigerated delivery infrastructure

- Food export companies rely on cold chain logistics to maintain seafood and meat quality for international markets

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now