Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The South Korea edge computing market is embedded within the country’s advanced 5G and digital infrastructure ecosystem, valued at approximately USD ~ billion based on a recent historical assessment of distributed computing nodes, telecom edge platforms, and enterprise edge deployments. Growth is driven by nationwide 5G coverage, industrial automation, and real-time AI applications across manufacturing, telecom, automotive, and smart city sectors. Investments in multi-access edge computing nodes, micro data centers, and edge AI platforms are expanding localized processing capacity nationwide.

Seoul metropolitan region dominates edge computing deployment due to dense telecom infrastructure, hyperscale interconnection hubs, and enterprise demand concentration enabling low-latency digital services. Gyeonggi Province hosts industrial edge infrastructure supporting smart factories and robotics ecosystems across manufacturing clusters. Busan and Incheon are emerging edge locations supported by smart port, logistics, and mobility platforms requiring localized computing. South Korea benefits from leadership in 5G and semiconductor industries, positioning it as a major edge computing innovation hub within Northeast Asia digital infrastructure networks.

Market Segmentation

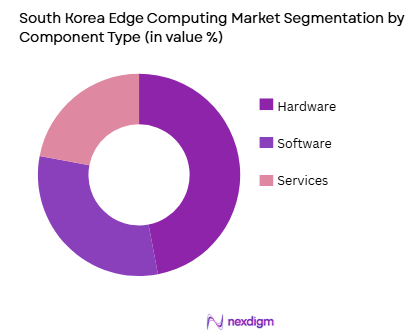

By Component

South Korea Edge Computing market is segmented by component into hardware, software, and services. Recently, hardware has a dominant market share due to factors such as telecom edge node deployment, industrial edge servers, and micro data center expansion supporting nationwide 5G and automation ecosystems. Telecom operators deploy distributed edge hardware at base stations and network aggregation sites to enable ultra-low latency services and traffic processing. Manufacturing and robotics industries invest in ruggedized edge servers and gateways for real-time control and analytics. Software and services adoption is expanding but remains dependent on installed hardware infrastructure across telecom and industrial edge environments.

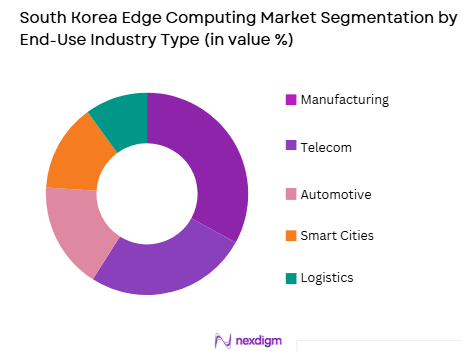

By End-Use Industry

South Korea Edge Computing market is segmented by end-use industry into manufacturing, telecom, automotive, smart cities, and logistics. Recently, manufacturing has a dominant market share due to factors such as smart factory deployment, robotics automation, and industrial IoT integration across South Korea’s advanced manufacturing sector. Industrial facilities deploy edge computing for real-time machine control, predictive maintenance, and computer vision quality inspection requiring localized processing. Telecom and automotive sectors also adopt edge computing, but manufacturing’s automation intensity and robotics density position it as the largest investor in distributed computing infrastructure within South Korea’s industrial economy.

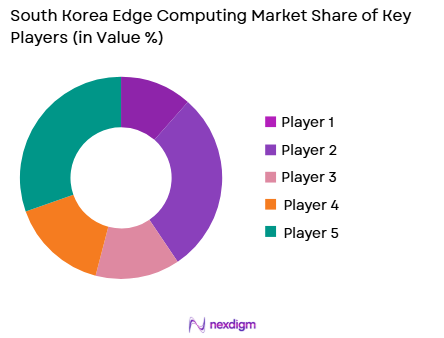

Competitive Landscape

The South Korea edge computing market is led by telecom operators, technology conglomerates, and global cloud providers deploying distributed edge infrastructure integrated with 5G networks and industrial platforms. Market concentration is high among firms combining telecom connectivity, semiconductor hardware, and AI platforms. Domestic telecom operators control nationwide edge node deployment, while technology firms supply hardware and edge software platforms. Competition centers on edge node density, latency performance, and industrial integration capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Focus |

| SK Telecom | 1984 | South Korea | ~ | ~ | ~ | ~ | ~ |

| KT Corp | 1981 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics | 1969 | South Korea | ~ | ~ | ~ | ~ | ~ |

| LG CNS | 1987 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Naver | 1999 | South Korea | ~ | ~ | ~ | ~ | ~ |

South Korea Edge Computing Market Analysis

Growth Drivers

Nationwide 5G Deployment Enabling Ultra-Low Latency Edge Architectures

South Korea’s globally advanced 5G infrastructure rollout has created foundational conditions for large-scale edge computing deployment by enabling distributed processing nodes integrated directly with mobile network architecture across urban and industrial environments. Telecom operators deploy multi-access edge computing nodes at base stations and aggregation points to process data locally and reduce latency for applications such as autonomous mobility, immersive media, and real-time analytics. Ultra-reliable low-latency communication capabilities of 5G networks require localized compute infrastructure to meet performance thresholds. Enterprises adopting mobile IoT and connected device ecosystems depend on edge processing for responsiveness and bandwidth optimization. Telecom providers monetize 5G through edge-enabled enterprise services including industrial automation and smart city platforms. Edge infrastructure reduces backhaul congestion and improves network efficiency across dense urban populations. Integration of edge nodes with cloud platforms creates hybrid computing architectures. Government smart infrastructure initiatives utilize 5G edge platforms for transportation, safety, and urban management. South Korea’s early and comprehensive 5G coverage enables nationwide edge deployment scale unmatched in most markets. Continuous 5G evolution toward advanced releases sustains long-term demand for edge computing infrastructure across sectors.

Industrial Automation and Robotics Ecosystem Driving Real-Time Edge Processing

South Korea’s leadership in industrial automation and robotics is generating strong demand for edge computing infrastructure capable of supporting real-time machine control, sensor processing, and AI-driven manufacturing analytics across advanced production facilities. Smart factories deploy distributed edge servers and gateways to process data from industrial IoT sensors, robotic systems, and computer vision platforms without reliance on distant cloud infrastructure. Real-time responsiveness requirements in robotics control and quality inspection necessitate localized processing environments. Manufacturing enterprises integrate edge computing with digital twin and predictive maintenance systems improving operational efficiency. Automotive and electronics production lines generate continuous high-volume sensor data streams requiring edge analytics. Industrial AI models deployed at factory sites rely on edge compute nodes for inference. Robotics collaboration systems depend on low-latency processing for safety and coordination. Korea’s dense industrial clusters accelerate deployment of localized computing infrastructure across production networks. Integration of edge computing with industrial 5G networks enhances automation performance. As smart manufacturing expands nationwide, industrial edge computing becomes a core infrastructure layer across South Korea’s production ecosystem.

Market Challenges

High Infrastructure Costs and Complexity of Distributed Edge Deployment

Edge computing deployment across South Korea involves significant capital expenditure and operational complexity due to the need for large numbers of distributed computing nodes integrated with telecom networks, industrial facilities, and urban infrastructure environments. Unlike centralized data centers, edge architectures require numerous localized installations increasing hardware, networking, and maintenance costs. Site acquisition, power provisioning, and environmental control for micro data centers add infrastructure complexity. Integration with legacy enterprise and telecom systems requires specialized engineering and orchestration platforms. Managing distributed nodes increases operational monitoring and lifecycle costs. Enterprises must justify investment relative to centralized cloud alternatives. Rapid hardware refresh cycles in edge environments increase capital requirements. Skilled workforce for distributed infrastructure management is limited. Security risks expand with distributed processing endpoints requiring advanced protection. Interoperability across heterogeneous edge platforms remains challenging. These economic and technical complexities constrain broader adoption beyond high-value use cases despite strong performance benefits.

Energy Efficiency and Thermal Management Constraints in Dense Urban Edge Nodes

South Korea’s urban density and energy sustainability targets create challenges for deploying power-intensive edge computing nodes within metropolitan and industrial environments requiring efficient thermal management and low-footprint infrastructure designs. Edge servers and micro data centers generate heat in constrained urban or factory locations lacking traditional data center cooling infrastructure. Power availability and grid constraints in dense city zones affect deployment scalability. Environmental regulations and energy efficiency requirements limit infrastructure expansion. Telecom edge sites must balance compute density with energy consumption and space constraints. Industrial edge nodes require ruggedized cooling systems in manufacturing environments. Sustainable infrastructure design increases deployment cost. Noise and heat emission considerations affect urban siting approvals. Edge hardware performance must align with energy efficiency standards. Operators invest in advanced cooling and low-power processors to mitigate constraints. These energy and spatial limitations challenge scaling of edge infrastructure across densely populated regions.

Opportunities

Edge AI Integration Across Autonomous Mobility and Smart Transportation Systems

South Korea’s leadership in autonomous vehicles, smart transportation, and intelligent mobility platforms creates major opportunities for edge computing infrastructure deployment supporting real-time perception, navigation, and traffic management systems across urban and highway environments. Autonomous driving and connected vehicle platforms require localized processing for sensor fusion, decision making, and safety systems. Smart traffic infrastructure integrates cameras, sensors, and AI analytics deployed on edge nodes. Urban mobility services utilize edge computing for fleet coordination and real-time routing. Public transportation systems adopt edge analytics for operational optimization. Vehicle-to-everything communication networks depend on distributed edge platforms. Logistics and delivery robotics rely on localized computing for navigation. Government smart mobility initiatives expand infrastructure demand. Integration of edge AI with transportation networks enhances safety and efficiency. Korea’s advanced automotive and mobility industries drive adoption. As autonomous and smart transport ecosystems expand, edge computing infrastructure becomes essential nationwide.

Expansion of Edge-Cloud Continuum for AI and Industrial Applications

The evolution toward integrated edge-cloud computing architectures across South Korea’s digital economy creates opportunities for distributed infrastructure deployment enabling seamless processing from device to cloud across AI, manufacturing, telecom, and urban applications. Enterprises adopt hybrid architectures combining centralized cloud training with edge inference processing. Telecom providers integrate edge nodes with cloud platforms for service delivery. Industrial AI systems rely on distributed computing across factory and cloud environments. Digital platforms deploy edge nodes to improve latency and user experience. National AI and smart industry strategies encourage distributed computing models. Edge-cloud orchestration platforms enable workload mobility. Real-time analytics across sectors require localized processing layers. Infrastructure providers develop scalable edge-cloud ecosystems. Integration of 5G, AI, and cloud technologies drives convergence. As distributed computing architectures mature, edge infrastructure demand expands across South Korea’s digital industries.

Future Outlook

The South Korea edge computing market is expected to expand rapidly as 5G-enabled applications and industrial automation continue advancing nationwide. Telecom operators and manufacturing firms will expand distributed edge node deployment across urban and industrial regions. Edge AI integration with mobility and smart city platforms will drive new infrastructure demand. Energy-efficient edge hardware and orchestration technologies will improve scalability. South Korea will remain a global leader in edge computing innovation and deployment.

Major Players

- SK Telecom

- KT Corp

- Samsung Electronics

- LG CNS

- Naver

- Kakao

- SK Hynix

- NHN Cloud

- Amazon Web Services

- Microsoft

- Google Cloud

- NVIDIA

- Intel

- HPE

- Dell Technologies

Key Target Audience

- Telecom operators

- Manufacturing conglomerates

- Automotive companies

- Smart city developers

- Logistics companies

- Cloud service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Edge node deployment scale, 5G coverage, industrial automation intensity, and distributed computing demand were identified as core variables. Energy and infrastructure constraints were mapped. Industry adoption patterns were assessed.

Step 2: Market Analysis and Construction

Market structure was constructed by analyzing component segmentation, industry adoption, and regional deployment across South Korea. Edge hardware and platform ecosystems were evaluated. Demand drivers across sectors were modeled.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding deployment drivers, energy constraints, and industrial demand were validated through technology ecosystem benchmarking and infrastructure analysis. National digital strategy impacts were incorporated. Competitive factors were verified.

Step 4: Research Synthesis and Final Output

All findings were synthesized into a comprehensive model describing segmentation, competition, growth drivers, and opportunities. Distributed infrastructure and industry demand dynamics were integrated. Final outputs reflected technological and industrial trends shaping South Korea edge computing outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Nationwide 5G and ultra-low latency network deployment

Advanced manufacturing and robotics requiring real-time compute

Smart city and autonomous mobility infrastructure expansion - Market Challenges

High deployment cost in dense urban environments

Interoperability complexity across telecom and enterprise edge

Power and thermal constraints in distributed sites - Market Opportunities

Edge AI for industrial automation and robotics control

Autonomous vehicle and mobility edge platforms

Immersive media and cloud gaming edge delivery - Trends

Convergence of telecom and enterprise edge architectures

Adoption of micro modular and containerized edge data centers

Integration of AI accelerators into edge nodes - Government regulations

National 5G and digital infrastructure policies

Smart city and autonomous mobility programs

Data protection and localization compliance frameworks - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units,2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge Data Centers

Micro Edge Nodes

On-Premise Edge Servers

Edge AI Gateways

Ruggedized Edge Platforms - By Platform Type (In Value%)

Telecom Network Edge

Enterprise Campus Edge

Industrial Edge Systems

Autonomous Mobility Edge

Smart City Edge Infrastructure - By Fitment Type (In Value%)

New Edge Deployment

Retrofit Edge Enablement

Integrated OEM Edge Systems

Modular Edge Units

Cloud-Managed Edge Integration - By End-user Segment (In Value%)

Telecommunications Operators

Manufacturing and Robotics Firms

Automotive and Mobility Providers

Media and Content Platforms

Government and Smart City Agencies - By Procurement Channel (In Value%)

Direct OEM Procurement

Telecom Operator Contracts

System Integrator Deployment

Cloud Service Bundling

Public Sector Tenders

- Market Share Analysis

- Cross Comparison Parameters (Latency Performance, Edge Compute Density, Power Efficiency per Node, Network Proximity and Coverage, Scalability Architecture, Edge AI Acceleration Capability, Orchestration and Management Platform, Ruggedization and Environmental Tolerance, Interconnect Bandwidth, Deployment Flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Samsung SDS

KT Corporation

SK Telecom

LG Uplus

Naver Cloud

Kakao Enterprise

LG CNS

Hyundai AutoEver

POSCO DX

Hanwha Systems

Dell Technologies Korea

Hewlett Packard Enterprise Korea

Cisco Systems Korea

Nokia Korea

Ericsson-LG

- Telecom operators deploying dense edge nodes for 5G services

- Manufacturing and robotics firms using edge for real-time control

- Automotive sector building edge for autonomous mobility

- Media platforms using edge for low-latency content delivery

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now