Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Korea home finance market holds approximately USD ~ billion in outstanding residential mortgage and housing-related loans, based on a recent historical assessment of central bank financial accounts and supervisory housing credit statistics. Demand is driven by high urban housing values, long-term mortgage adoption, and policy-backed lending programs supporting first-time buyers and refinancing. Commercial banks, policy lenders, and savings institutions dominate origination, while digital loan platforms and automated underwriting improve accessibility, processing speed, and refinancing uptake across borrower segments.

Seoul and the Capital Region dominate the South Korea home finance market due to dense housing stock, elevated property prices, and concentration of mortgage lenders and digital banking infrastructure. Gyeonggi and Incheon follow with large commuter populations and new residential developments requiring financing. Secondary metropolitan areas such as Busan and Daegu show strong participation linked to industrial employment and urban redevelopment. Nationwide mortgage penetration reflects universal banking reach, standardized collateral systems, and government housing finance programs supporting home ownership across cities.

Market Segmentation

By Product Type

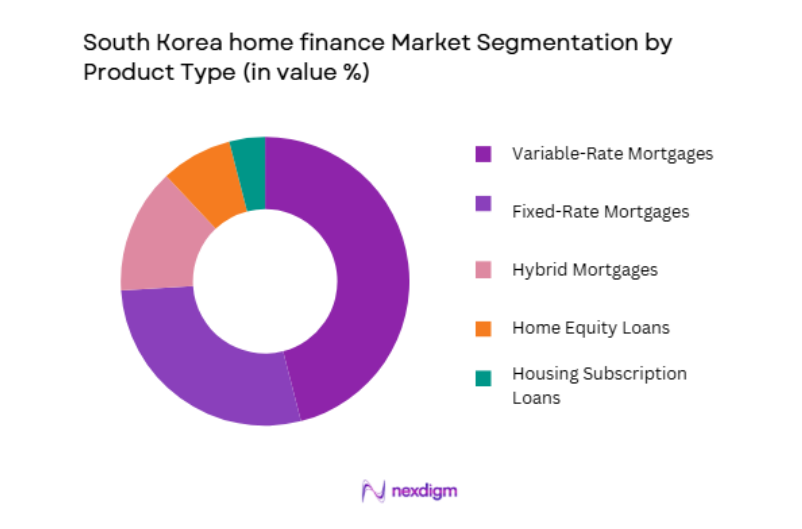

South Korea home finance market is segmented by product type into fixed-rate mortgages, variable-rate mortgages, hybrid mortgages, home equity loans, and housing subscription loans. Recently, variable-rate mortgages has a dominant market share due to factors such as historically lower initial interest costs, borrower preference for affordability, and widespread bank promotion during periods of stable policy rates. Many households prioritize short-term repayment burden over long-term rate certainty, especially in high-priced urban housing markets requiring large loan principal. Financial institutions structure adjustable loans with flexible repricing and refinancing options, encouraging uptake among salaried borrowers expecting income growth. Government policy loans and refinancing programs have also frequently referenced floating benchmarks, reinforcing familiarity and accessibility of variable structures.

By Lender Type

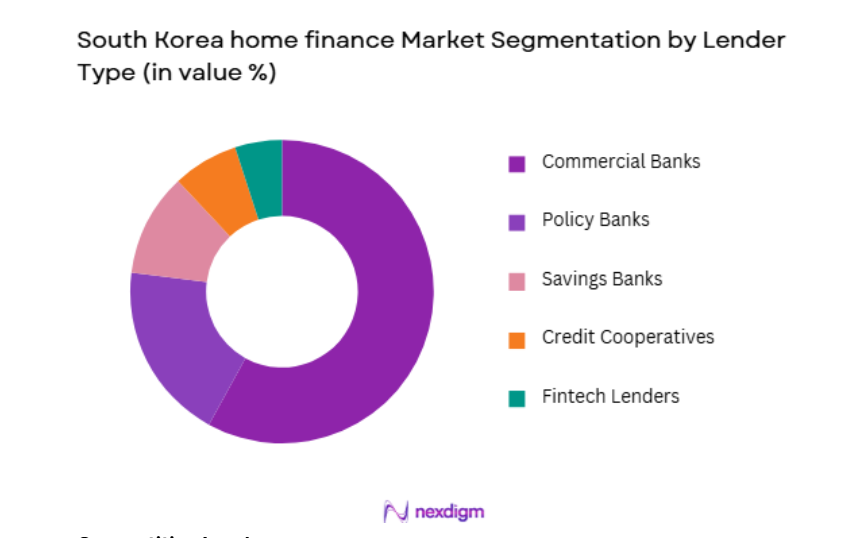

South Korea home finance market is segmented by lender type into commercial banks, policy banks, savings banks, credit cooperatives, and fintech lenders. Recently, commercial banks has a dominant market share due to factors such as nationwide branch networks, deposit funding advantages, and integrated mortgage servicing capabilities. Large banks offer competitive pricing and bundled financial services including insurance, deposits, and refinancing, strengthening borrower retention across loan lifecycles. Advanced underwriting analytics and property valuation systems enable efficient approval at scale, supporting large origination volumes in urban markets. Regulatory capital strength and government coordination on housing policy programs position banks as primary distribution channels for subsidized and conventional mortgages. Digital mortgage application and servicing platforms further enhance customer acquisition and refinancing within bank ecosystems.

Competitive Landscape

Competitive Landscape

The South Korea home finance market is highly concentrated among major commercial banks and policy-backed housing finance institutions that control origination, securitization, and servicing infrastructure. Competition centers on mortgage pricing, refinancing offerings, and digital application experiences. Large banks leverage deposit funding and cross-selling advantages, while policy lenders support affordability and stabilization. Fintech entrants focus on digital comparison and brokerage rather than balance-sheet lending, reinforcing incumbents’ structural dominance.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Portfolio Size |

| KB Kookmin Bank | 2001 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Shinhan Bank | 1897 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Hana Bank | 1971 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Woori Bank | 1899 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Korea Housing Finance Corp | 2004 | Busan | ~ | ~ | ~ | ~ | ~ |

South Korea Home Finance Market Analysis

Growth Drivers

Urban Housing Price Levels and Mortgage Dependency

South Korea’s persistently elevated urban housing prices relative to household income necessitate widespread reliance on mortgage financing, structurally anchoring demand for home finance products across metropolitan regions and sustaining large outstanding loan balances within the banking system. Limited land supply in core urban districts and continued migration toward employment centers concentrate demand in high-value housing markets where loan-to-value constrained purchases still require substantial borrowing. Households treat mortgage debt as essential leverage for home ownership and asset accumulation, normalizing long-duration repayment commitments supported by stable salaried employment structures. Financial institutions respond with diversified mortgage offerings, refinancing programs, and maturity extensions to maintain affordability and borrower retention. Government housing supply and stabilization policies indirectly reinforce mortgage demand by sustaining transaction volumes and encouraging ownership pathways. Urban redevelopment and apartment reconstruction cycles generate recurring financing needs as households upgrade or relocate within metropolitan areas. Digital mortgage processing reduces barriers to application and refinancing, increasing accessibility across income tiers. Banks’ balance-sheet capacity and securitization channels ensure continuous credit availability aligned with housing cycles. Elevated urban housing price levels therefore act as a foundational growth driver of the South Korea home finance market.

Government Housing Policy and Subsidized Lending Programs

South Korea’s housing finance system is strongly shaped by government policy interventions aimed at improving affordability, supporting first-time buyers, and stabilizing property markets through subsidized mortgages, guarantees, and refinancing schemes delivered via policy institutions and commercial banks. Preferential interest programs and guarantee-backed loans lower entry barriers for young households and lower-income borrowers, expanding the borrower base eligible for formal mortgage financing and encouraging transition from rental to ownership. Policy coordination with banks standardizes underwriting criteria and documentation, enabling efficient scale distribution of subsidized products through nationwide banking networks. Refinancing initiatives and fixed-rate conversion programs mitigate interest rate volatility risk for borrowers, sustaining repayment stability and preventing market disruptions. Public securitization channels recycle mortgage credit capacity, allowing continuous origination without excessive balance-sheet strain. Housing savings subscription schemes integrate with lending pathways, linking long-term deposit behavior to mortgage eligibility and reinforcing formal financial intermediation. Regulatory oversight ensures prudent loan-to-value and debt-service ratios while maintaining credit flow.

Market Challenges

Household Debt Saturation and Macroprudential Constraints

South Korea exhibits one of the highest household debt levels relative to income globally, prompting authorities to impose strict macroprudential controls on mortgage lending including debt-service ratio caps, loan-to-value limits, and stress-testing requirements that directly constrain credit expansion within the home finance market. These regulations reduce borrowing capacity for prospective buyers and limit refinancing flexibility for existing borrowers, suppressing loan origination growth despite persistent housing demand. Banks must allocate capital cautiously and prioritize lower-risk borrowers, narrowing eligibility among younger and self-employed households. Tighter underwriting standards increase approval times and documentation burdens, reducing transaction velocity in property markets. Policy adjustments to cooling or stabilizing housing prices can abruptly shift lending conditions, creating uncertainty for borrowers and lenders alike. High indebtedness also elevates systemic risk sensitivity to interest rate changes, compelling conservative lending strategies that restrict product innovation. Mortgage growth becomes dependent on policy relaxation cycles rather than purely market demand dynamics.

Interest Rate Volatility and Refinancing Risk Exposure

Fluctuating monetary policy and funding costs create significant interest rate risk within South Korea’s predominantly variable-rate mortgage portfolio, exposing borrowers to payment shocks and lenders to refinancing waves that disrupt profitability and portfolio stability. Borrowers facing rising rates may experience repayment stress, increasing delinquency risk and prompting regulatory or policy responses that alter lending frameworks. Conversely, declining rates trigger large-scale refinancing, compressing net interest margins as existing loans are replaced with lower-yield contracts. Banks must manage duration mismatch between fixed funding and adjustable loan assets, complicating asset-liability management strategies. Interest rate uncertainty discourages long-term fixed mortgage uptake among borrowers concerned about affordability trade-offs, perpetuating system sensitivity to rate cycles. Policy interventions to stabilize borrower payments can impose caps or conversion mandates affecting lender revenues. Market volatility also influences housing transaction volumes, indirectly affecting mortgage demand. Interest rate fluctuations thus generate cyclical risk and operational complexity across the South Korea home finance market.

Opportunities

Digital Mortgage Platforms and End-to-End Online Origination

South Korea’s advanced digital banking infrastructure and high consumer adoption of mobile financial services create substantial opportunity for fully digital mortgage origination platforms that streamline application, underwriting, approval, and servicing processes, reducing costs and expanding access across borrower segments. Integration of property registry data, income verification systems, and credit analytics enables near-instant eligibility assessment and automated documentation, improving borrower convenience and lender efficiency. Digital platforms also facilitate refinancing comparison and switching, enhancing competition and market transparency. Younger homebuyers increasingly prefer online channels over branch-based processes, accelerating digital loan penetration. Banks can cross-sell insurance, deposits, and wealth products within integrated homeownership ecosystems, increasing lifetime customer value. Remote property valuation and electronic contract execution further reduce transaction friction. Fintech partnerships extend reach to underserved or digitally native borrowers. End-to-end digitalization therefore offers scalable growth and operational improvement potential within the South Korea home finance market.

Green Housing Finance and Energy-Efficient Mortgage Products

Rising policy emphasis on sustainability and building efficiency in South Korea opens opportunities for green mortgages and renovation financing tied to energy-efficient housing standards, enabling lenders to support environmental goals while expanding specialized loan portfolios. Preferential rates or incentives for certified green buildings or retrofits encourage borrower adoption and differentiate mortgage offerings. Government climate programs and urban redevelopment initiatives increasingly integrate efficiency upgrades requiring financing, creating new lending demand streams. Green securitization channels and sustainable finance frameworks attract institutional funding aligned with environmental mandates. Homeowners benefit from lower utility costs and improved property value, enhancing repayment capacity and credit quality. Banks can integrate energy performance data into underwriting and risk assessment models. Public awareness of sustainability supports marketing and uptake. Green housing finance thus represents an emerging growth avenue in the South Korea home finance market.

Future Outlook

The South Korea home finance market is expected to remain large and structurally important as urban housing demand persists and policy frameworks support ownership. Digital mortgage platforms will expand accessibility and efficiency across borrower segments. Government programs and refinancing mechanisms will continue stabilizing affordability. Sustainability-linked housing finance will emerge alongside redevelopment cycles.

Major Players

- KB Kookmin Bank

- Shinhan Bank

- Hana Bank

- Woori Bank

- Korea Housing Finance Corp

- NH NongHyup Bank

- Industrial Bank of Korea

- Standard Chartered Korea

- Citi Korea

- KEB Savings Bank

- SBI Savings Bank Korea

- Korea Investment Savings Bank

- OK Savings Bank

- Toss Bank

- Kakao Bank

Key Target Audience

- Commercial banks

- Mortgage lenders

- Housing finance institutions

- Investments and venture capitalist firms

- Government and regulatory bodies

- Real estate developers

- Construction companies

- Fintech lending platforms

Research Methodology

Step 1: Identification of Key Variables

Core variables included outstanding mortgage balances, lender share, product mix, and borrower characteristics. Housing price indices, transaction volumes, and policy lending frameworks were mapped. Regulatory limits on lending ratios and refinancing programs were incorporated.

Step 2: Market Analysis and Construction

Central bank financial accounts, housing finance corporation data, and bank disclosures were synthesized to quantify market size. Segmentation by product and lender derived from supervisory statistics and institutional reports. Competitive structure assessed through portfolio scale and origination capacity.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on digital mortgage growth, policy lending influence, and borrower demand validated with banking and housing finance practitioners. Regulatory interpretations cross-checked with compliance experts. Iterative reviews reconciled institutional data differences.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights integrated into structured sections aligned with outlook requirements. Tables harmonized with verified statistics and market definitions. Final narrative refined for consistency and analytical clarity.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Strong urban housing demand concentrated in metropolitan regions

Government mortgage support programs for first-time buyers

Competitive bank lending and refinancing activity - Market Challenges

High household debt and tightening mortgage regulations

Elevated housing prices reducing affordability

Interest rate volatility affecting borrower demand - Market Opportunities

Digital mortgage origination and remote approval services

Green housing and energy-efficient home financing

Refinancing demand amid rate cycles - Trends

Growth of jeonse deposit financing products

Expansion of fintech-enabled mortgage comparison platforms - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Mortgage Loans for Apartments

Jeonse Deposit Loans

Home Equity Loans

Refinancing and Balance Transfer Loans

Policy-supported Housing Loans - By Platform Type (In Value%)

Commercial Bank Mortgage Channels

Digital Mortgage Platforms

Savings Bank Lending Channels

Government Housing Finance Platforms

Fintech Mortgage Intermediaries - By Fitment Type (In Value%)

Fixed Rate Home Loans

Variable Rate Home Loans

Hybrid Rate Mortgages

Subsidized Policy Mortgages - By End User Segment (In Value%)

Urban Salaried Households

Young First-time Buyers

Multi-home Investors

- Market Share Analysis

- Cross Comparison Parameters (Loan Type, Interest Rate Structure, Distribution Channel, Borrower Segment Focus, Approval Criteria, Loan Tenure Options, Loan-to-Value Limits, Debt-to-Income Assessment, Digital Application Capability, Policy Program Eligibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Kookmin Bank Mortgage

Shinhan Bank Mortgage

Hana Bank Mortgage

Woori Bank Mortgage

NH NongHyup Bank Mortgage

Korea Housing Finance Corporation

KakaoBank Mortgage

K Bank Mortgage

Samsung Life Mortgage Loans

Hanwha Life Mortgage Loans

Kyobo Life Mortgage Loans

Mirae Asset Capital Housing Finance

Hyundai Capital Housing Loans

OK Savings Bank Mortgage

SBI Savings Bank Mortgage

- Young buyers leveraging policy mortgages for entry housing

- Urban households refinancing to manage debt burdens

- Investors utilizing leverage for multi-property ownership

- Self-employed borrowers seeking flexible underwriting loans

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now