Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The South Korea semiconductor manufacturing market is experiencing significant growth, driven by demand for high-performance electronics and advancements in chip technology. The market is valued in the billions ~ USD, fueled by the increasing adoption of semiconductor components in various industries, including consumer electronics, automotive, and telecommunications. In particular, the rise in mobile device usage and the expansion of 5G networks have contributed to the growing demand for memory chips and logic semiconductors. With major players investing heavily in production capabilities, South Korea remains a leader in the semiconductor manufacturing space.

South Korea is a dominant player in the global semiconductor market, driven by its robust industrial infrastructure and government support for technological advancements. The country’s capital city, Seoul, serves as a hub for major semiconductor manufacturers such as Samsung Electronics and SK hynix, attracting international investments and research. Key factors driving South Korea’s dominance include its highly skilled workforce, cutting-edge research facilities, and strong export channels. The country benefits from strategic partnerships, technological innovation, and a supportive regulatory environment, positioning it as a global leader in semiconductor production.

Market Segmentation

By Product Type

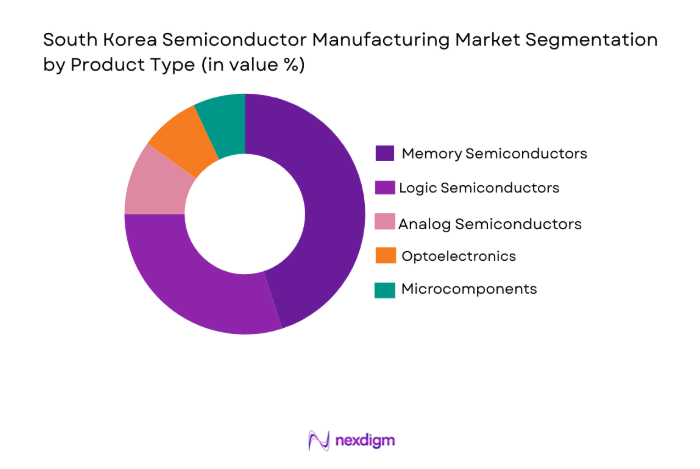

The South Korea semiconductor manufacturing market is segmented by product type into memory semiconductors, logic semiconductors, analog semiconductors, optoelectronics, and microcomponents. Recently, memory semiconductors have dominated the market share due to high demand from the consumer electronics and mobile industries. The proliferation of smartphones, smart devices, and the demand for high-capacity data storage solutions have driven the increased consumption of memory chips. Additionally, advancements in memory technology, such as DRAM and NAND, have further boosted their market dominance.

By Platform Type

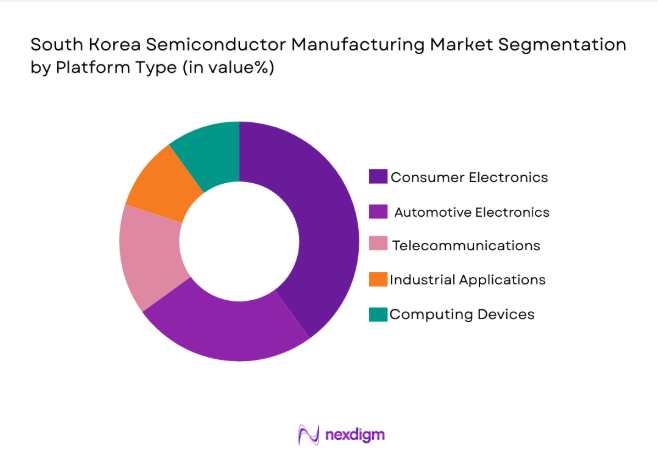

The market is segmented by platform type into consumer electronics, automotive electronics, telecommunications, industrial applications, and computing devices. The consumer electronics segment holds the largest market share, driven by the widespread use of semiconductor components in smartphones, tablets, and wearables. As the demand for next-generation devices like 5G smartphones and AI-powered gadgets continues to rise, semiconductor manufacturers are focusing on innovating to meet the high-performance requirements of this market. The presence of key industry players in South Korea and their strong export channels further solidify the dominance of this segment.

Competitive Landscape

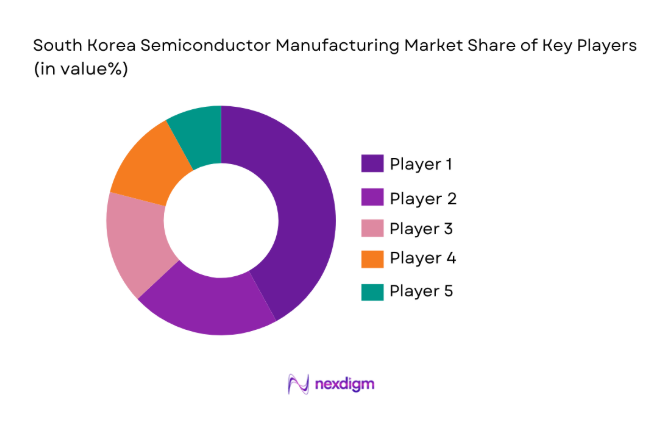

The South Korea semiconductor manufacturing market is highly competitive, with significant consolidation among major players. The market is dominated by large multinational companies, such as Samsung Electronics and SK hynix, which leverage their technological expertise, large-scale manufacturing facilities, and strategic global presence. These companies continue to invest heavily in research and development, fueling market growth and innovation. Smaller players are also emerging, particularly in niche areas like advanced packaging and optoelectronics, contributing to a dynamic competitive environment.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Market-Specific Parameter |

| Samsung Electronics | 1938 | Seoul, South Korea | ~ | ~ | ~ | ~ | ~ |

| SK hynix | 1983 | Icheon, South Korea | ~ | ~ | ~ | ~ | ~ |

| LG Electronics | 1958 | Seoul, South Korea | ~ | ~ | ~ | ~ | ~ |

| Intel Corporation | 1968 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ |

| Micron Technology | 1978 | Boise, USA | ~ | ~ | ~ | ~ | ~ |

South Korea Semiconductor Manufacturing Market Analysis

Growth Drivers

Rising Demand for High-Performance Computing

The growing need for advanced computing devices has been a major driver of the semiconductor market in South Korea. As industries such as gaming, cloud computing, and artificial intelligence continue to expand, the demand for high-performance chips, particularly in data centers and server applications, has surged. With the rise of big data analytics, machine learning, and real-time processing, there is an increased requirement for chips that can handle massive amounts of data efficiently and at high speeds. South Korea’s semiconductor manufacturers, such as Samsung Electronics and SK hynix, are at the forefront of developing cutting-edge chips that cater to this growing demand, leading to continued investment in R&D and manufacturing capacity expansion. As the demand for data storage, faster computing speeds, and low-latency connectivity grows, South Korean companies are well-positioned to drive the innovation needed to meet these industry requirements, solidifying their role as key players in the global semiconductor market. The proliferation of artificial intelligence (AI) and machine learning (ML) applications further underscores the critical need for high-performance chips in driving technological advancements across various sectors.

Expansion of 5G Networks

The ongoing rollout of 5G networks worldwide has accelerated the demand for advanced semiconductor technologies. South Korea, as one of the early adopters of 5G technology, has seen a rise in the demand for semiconductors used in 5G infrastructure, smartphones, and connected devices. The development of 5G-enabled applications, including autonomous vehicles, smart cities, and industrial automation, has created a significant market opportunity for semiconductor manufacturers to meet the increasing demand for high-speed, low-latency chip solutions. The need for high-performance chips to support 5G base stations, antennas, and data transmission networks is expected to drive considerable growth in South Korea’s semiconductor industry. Furthermore, the demand for 5G-enabled consumer devices such as smartphones, tablets, and wearables is also fueling the market for memory chips, processors, and communication semiconductors. As 5G technologies enable real-time connectivity and faster data speeds, the market for chips that support these innovations will continue to expand, positioning South Korean manufacturers at the forefront of this technological revolution.

Market Challenges

Global Supply Chain Disruptions

The global semiconductor industry faces significant challenges due to ongoing supply chain disruptions. The COVID-19 pandemic, geopolitical tensions, and natural disasters have strained the production and distribution of semiconductor materials, leading to shortages and delays in product deliveries. South Korean semiconductor manufacturers, heavily reliant on global supply chains for raw materials and components, have been particularly affected. The disruption in supply chains has resulted in increased production costs, limited availability of critical components, and longer lead times, which pose challenges to the timely delivery of products to customers. The semiconductor supply chain is complex, involving multiple suppliers for raw materials, equipment, and parts, and any disruption at one stage of the process can impact the entire supply chain. Furthermore, competition for scarce resources, such as advanced chip manufacturing tools and rare earth materials, adds to the challenges faced by South Korean manufacturers, as these resources are critical to the production of advanced semiconductor nodes. The ongoing global shortage of chips has created volatility in the market, requiring manufacturers to adapt to changing conditions and find new ways to secure the necessary materials for production.

High Capital Investment in Manufacturing Plants

Building and maintaining advanced semiconductor manufacturing plants requires significant capital investment, often running into billions of dollars. South Korea’s semiconductor market, although robust, faces the challenge of balancing these high upfront costs with the need for continuous innovation and production capacity expansion. The capital-intensive nature of the industry poses challenges for smaller players, who may struggle to compete with the large, well-funded corporations that dominate the market, thus limiting overall market growth. South Korean semiconductor manufacturers are investing heavily in next-generation fabs to keep up with increasing demand for cutting-edge chips, such as those used in AI and 5G applications. However, the cost of developing, operating, and upgrading these advanced manufacturing plants requires substantial financial resources, and not all companies can afford to make these significant investments. This creates a high barrier to entry for new entrants and limits the growth potential for smaller players. The need for consistent technological advancements further complicates the capital investment issue, as manufacturers must continually innovate to stay competitive in an ever-evolving market.

Opportunities

Shift to Advanced Semiconductor Nodes

There is a growing opportunity for South Korea to lead the development of next-generation semiconductor nodes. The demand for smaller, more energy-efficient chips is increasing across various applications, including mobile devices, computing, and IoT. As the market shifts towards advanced nodes such as 5nm and 3nm technologies, South Korea’s semiconductor manufacturers, particularly Samsung and SK hynix, are well-positioned to capitalize on this trend through continued innovation in fabrication technologies. The shift to smaller nodes offers a chance for manufacturers to enhance chip performance while reducing power consumption, creating a strong competitive advantage. These advanced semiconductor nodes are expected to be in high demand for a variety of applications, including high-performance computing, AI, and 5G connectivity, where power efficiency, processing speed, and miniaturization are essential. Furthermore, as semiconductor technologies continue to evolve, South Korea’s established infrastructure and technological expertise provide a significant advantage in the global race to develop the smallest, most efficient chips. The transition to smaller nodes also opens up new opportunities for semiconductor manufacturers to target emerging markets, such as automotive electronics, where high-performance, energy-efficient chips are essential for the development of electric vehicles and autonomous driving technologies.

Growth in AI and Machine Learning Applications

The increasing use of artificial intelligence (AI) and machine learning (ML) across various industries presents a significant growth opportunity for South Korea’s semiconductor manufacturers. AI and ML applications require high-performance chips capable of processing large amounts of data quickly. South Korean companies, with their advanced semiconductor technologies, are well-positioned to meet the growing demand for AI-specific chips used in data centers, automotive applications, and consumer electronics. The expansion of AI and ML technologies will drive innovation in chip design, boosting the overall semiconductor market. As AI and ML continue to gain traction in areas such as image recognition, natural language processing, and predictive analytics, the need for specialized chips optimized for these workloads will increase. South Korea’s semiconductor companies are already at the forefront of developing AI accelerators, such as graphics processing units (GPUs) and neural processing units (NPUs), which are tailored for AI and ML tasks. This growing demand for AI-specific chips presents a major market opportunity for South Korean manufacturers to expand their product offerings and capture a larger share of the rapidly evolving AI semiconductor market. As industries from healthcare to finance integrate AI into their operations, the demand for high-performance chips will continue to rise, presenting significant growth opportunities for semiconductor manufacturers

Future Outlook

The South Korea semiconductor manufacturing market is expected to continue its growth over the next five years, driven by technological advancements, demand for next-generation computing devices, and the expansion of 5G networks. The market will likely see increased investments in advanced semiconductor nodes and manufacturing capabilities, especially in response to the growing demand for AI, automotive electronics, and IoT devices. Furthermore, government support for innovation and infrastructure development will contribute to the market’s future expansion.

Major Players

- Samsung Electronics

- SK hynix

- LG Electronics

- Intel Corporation

- Micron Technology

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Broadcom Inc.

- Qualcomm Incorporated

- Texas Instruments

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- STMicroelectronics

- NXP Semiconductors

- Infineon Technologies

- MediaTek

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Semiconductor manufacturers

- Electronics and telecommunications companies

- Automotive manufacturers

- Data center operators

- Research and development institutions

Research Methodology

Step 1: Identification of Key Variables

We begin by identifying the critical variables that drive the semiconductor manufacturing market, including technology trends, market demand, and economic factors.

Step 2: Market Analysis and Construction

Data is gathered through primary and secondary research to build a comprehensive market analysis, focusing on key regions, applications, and trends.

Step 3: Hypothesis Validation and Expert Consultation

We validate hypotheses and refine our analysis by consulting with industry experts, stakeholders, and professionals from key market sectors.

Step 4: Research Synthesis and Final Output

The final research output synthesizes all findings into a comprehensive market report, ensuring that conclusions are backed by credible data and insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Demand for High-Performance Computing

Expansion of 5G Networks

Increase in Automotive Semiconductor Usage - Market Challenges

Global Supply Chain Disruptions

High Capital Investment in Manufacturing Plants

Environmental and Regulatory Compliance - Market Opportunities

Shift to Advanced Semiconductor Nodes

Growth in AI and Machine Learning Applications

Emerging Opportunities in Automotive Electrification - Trends

Advancements in Chip Fabrication Technology

Miniaturization and Integration of Semiconductors - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Memory Semiconductors

Logic Semiconductors

Analog Semiconductors

Optoelectronics

Microcomponents - By Platform Type (In Value%)

Consumer Electronics

Automotive Electronics

Telecommunications

Industrial Applications

Computing Devices - By Fitment Type (In Value%)

Integrated Systems

Modular Systems

Custom Systems

OEM Systems - By End User Segment (In Value%)

Consumer Electronics Manufacturers

Automotive Manufacturers

Telecommunication Providers

Industrial Electronics Manufacturers

- Market Share Analysis

- Cross Comparison Parameters (Memory Semiconductors, Logic Semiconductors, Consumer Electronics, Automotive Electronics, 5G Networks, Semiconductor Fabrication Technology, Microcomponents)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Samsung Electronics

SK hynix

LG Electronics

Taiwan Semiconductor Manufacturing Company (TSMC)

Micron Technology

Intel Corporation

Broadcom Inc.

Qualcomm Incorporated

Texas Instruments

NVIDIA Corporation

Advanced Micro Devices (AMD)

STMicroelectronics

NXP Semiconductors

Infineon Technologies

MediaTek

- Increasing Focus on Energy-Efficient Devices

- Growing Demand for Autonomous Vehicles

- Shift to Smart Manufacturing Processes

- Need for Specialized Semiconductors in Telecom

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now