Download PDF

Download PDF Download PDF

Download PDFMarket Overview

South Korea wealth management market manages approximately USD ~ billion in financial assets across discretionary portfolios, advisory mandates, and private banking accounts, based on a recent historical assessment of national financial supervisory and central bank statistics. Expansion is driven by rising household financial wealth, institutionalization of retirement savings, and growing allocation to capital markets products beyond deposits. Digital advisory platforms and bank-affiliated securities arms enable scalable portfolio construction, tax-aware planning, and cross-border investment access for affluent and mass-affluent investors.

Seoul and the wider Capital Region dominate the South Korea wealth management market due to concentration of high-net-worth households, headquarters of major financial institutions, and advanced capital markets infrastructure. Busan follows as a regional financial hub with securities firms and maritime wealth. Nationwide participation is supported by universal banking reach, mobile brokerage adoption, and pension accumulation across metropolitan and provincial cities, reinforced by regulatory encouragement of diversified long-term investment and advisory-led distribution.

Market Segmentation

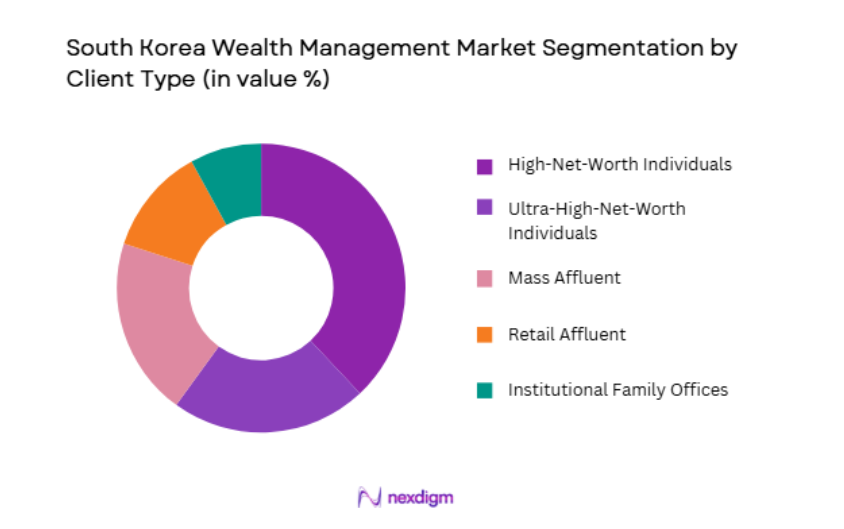

By Client Type

South Korea wealth management market is segmented by client type into ultra-high-net-worth individuals, high-net-worth individuals, mass affluent, retail affluent, and institutional family offices. Recently, high-net-worth individuals has a dominant market share due to factors such as strong entrepreneurial wealth creation, intergenerational asset transfer, and preference for diversified discretionary portfolios managed by bank-securities groups. This cohort exhibits substantial investable assets beyond primary residences and business holdings, enabling engagement in advisory, discretionary, and alternative allocations through private banking platforms. Financial institutions tailor structured products, global equities access, and tax-optimized trust solutions to this segment, driving fee-based revenue concentration.

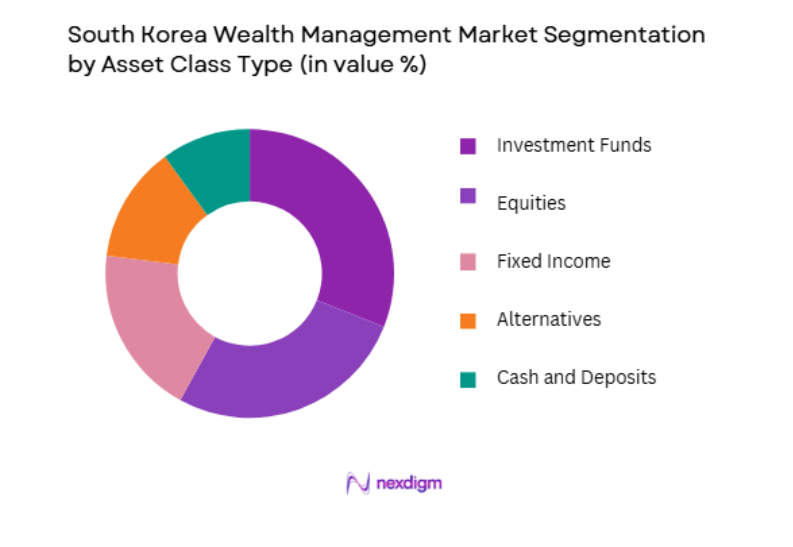

By Asset Class

By Asset Class

South Korea wealth management market is segmented by asset class into equities, fixed income, investment funds, alternatives, and cash and deposits. Recently, investment funds has a dominant market share due to factors such as regulatory support for collective investment schemes, professional management appeal, and access to global diversification through domestic distribution networks. Mutual funds and exchange-traded funds allow investors to achieve asset allocation and risk management efficiently without direct security selection, aligning with advisory models prevalent in bank and securities channels. Retirement accounts and tax-advantaged wrappers often channel flows into fund products, reinforcing scale. Wealth managers integrate funds into model portfolios and discretionary mandates, simplifying rebalancing and compliance oversight.

Competitive Landscape

Competitive Landscape

The South Korea wealth management market is dominated by large bank-securities conglomerates and global private banking franchises that combine distribution scale, product manufacturing, and advisory capabilities. Consolidation reflects universal banking structures linking deposits, brokerage, and asset management, while competition centers on digital advisory, global investment access, and discretionary portfolio services. Domestic leaders leverage branch and mobile ecosystems, while international firms differentiate through cross-border expertise and alternative investments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Discretionary AUM Share |

| KB Financial Group | 2008 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Shinhan Financial Group | 2001 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Hana Financial Group | 2005 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Samsung Securities | 1982 | Seoul | ~ | ~ | ~ | ~ | ~ |

| Mirae Asset Securities | 1970 | Seoul | ~ | ~ | ~ | ~ | ~ |

South Korea Wealth Management Market Analysis

Growth Drivers

Household Financial Asset Expansion and Capital Market Participation

South Korea’s sustained accumulation of household financial wealth alongside a gradual shift from bank deposits toward market-linked instruments is materially enlarging the addressable base for professional wealth management services delivered through banks, securities firms, and private banking channels. Rising incomes among professionals, entrepreneurs, and corporate executives increase surplus savings available for diversified portfolios, while maturation of pension and retirement systems channels long-term contributions into managed investment products requiring advisory oversight. Investors seek returns exceeding low-yield cash instruments, prompting reallocation toward equities, funds, and structured solutions that benefit from asset allocation expertise and ongoing monitoring. Financial institutions respond by scaling discretionary mandates and model portfolios, capturing fee-based revenues aligned with client outcomes rather than transactional commissions. Cross-border investing appetite expands exposure to global equities and alternatives, necessitating research, custody, and currency management capabilities central to wealth platforms.

Retirement Reform and Pension-Linked Advisory Demand

Structural aging and evolving retirement adequacy concerns in South Korea are catalyzing demand for professional wealth management that integrates pension assets, annuities, and drawdown strategies within comprehensive financial plans tailored to longevity risk and healthcare costs. Regulatory encouragement of diversified retirement investment, including tax-advantaged accounts and employer-sponsored schemes, increases flows into managed funds and discretionary portfolios overseen by wealth managers. Individuals approaching retirement transition from accumulation to income planning, requiring asset-liability matching, sequence-of-returns risk mitigation, and sustainable withdrawal frameworks best delivered through advisory mandates. Financial institutions integrate insurance, investment, and trust services to construct lifetime income solutions combining public pension entitlements with private savings. Digital retirement simulators and scenario analytics embedded in client portals enhance understanding and engagement, strengthening advisor-client relationships and retention. Longer life expectancy amplifies the need for periodic portfolio rebalancing and healthcare provisioning, sustaining ongoing advisory revenue streams.

Market Challenges

Concentration of Real Estate Wealth and Illiquid Asset Bias

South Korean household balance sheets remain heavily concentrated in residential real estate, limiting the proportion of investable financial assets available for diversified portfolio construction and constraining the penetration of comprehensive wealth management mandates among affluent segments. Cultural preferences and historical appreciation of property assets reinforce allocation inertia, as investors prioritize leverage into housing over financial diversification despite rising volatility and policy interventions in property markets. Illiquidity of real estate holdings complicates rebalancing and liquidity management, reducing the scope for discretionary asset allocation across market cycles and dampening fee-generating managed portfolios. Wealth managers face challenges persuading clients to monetize or partially rebalance property exposure into liquid securities, especially when transaction costs and taxation are significant. Collateralized borrowing against property may substitute for portfolio liquidation, perpetuating concentration risk within client wealth structures.

Fee Compression and Standardization in Digital Advisory Channels

Intensifying competition among bank-securities groups, online brokerages, and fintech robo-advisors is exerting downward pressure on advisory and management fees across standardized portfolio offerings, challenging profitability of scalable wealth management segments serving mass affluent and emerging high-net-worth clients. Digital platforms enable transparent comparison of costs and performance, encouraging commoditization of model portfolios and exchange-traded fund-based allocations that are difficult to differentiate. Regulatory emphasis on suitability, disclosure, and investor protection constrains use of higher-margin structured products, narrowing revenue per asset under management. Large incumbents absorb margin pressure through scale and cross-subsidization from lending and transaction services, while smaller firms face sustainability challenges. Client expectations for real-time reporting, tax optimization, and personalized insights increase technology investment requirements without commensurate fee increases. Migration from commission-based brokerage to fee-based advisory reduces short-term revenues during transition phases.

Opportunities

Global Alternative Investments Access through Platformization

South Korean affluent investors are increasingly seeking exposure to private equity, private credit, infrastructure, and real assets to enhance returns and diversification, creating significant opportunity for wealth managers to curate and distribute global alternatives through feeder funds, co-investments, and discretionary allocations integrated into client portfolios. Platformization of due diligence, subscription, and reporting processes enables scalable access to traditionally institutional asset classes while meeting regulatory and operational requirements. Partnerships with international general partners expand product pipelines and brand credibility, attracting high-net-worth and ultra-high-net-worth segments desiring differentiated opportunities. Alternatives can improve portfolio resilience and fee economics for providers, supporting advisory value propositions beyond commoditized liquid assets. Education and suitability frameworks embedded in digital portals help clients understand liquidity profiles and risk-return characteristics, facilitating informed participation. Secondary market solutions and interval structures enhance accessibility and cash-flow management for private assets.

AI-Enhanced Hyper-Personalized Advisory and Lifecycle Planning

Advances in artificial intelligence and data integration allow wealth managers to deliver hyper-personalized portfolio construction, tax optimization, and lifecycle financial planning that adapts dynamically to client goals, behavior, and market conditions, elevating advisory relevance and willingness to pay for differentiated services. Integration of banking, brokerage, insurance, and spending data creates holistic financial views enabling tailored recommendations across investment, protection, and liquidity domains. Predictive analytics anticipate life events such as education funding, property transitions, or retirement milestones, prompting proactive advisory engagement through digital channels. Natural language interfaces and automated insights democratize sophisticated planning for mass affluent clients while freeing advisors to focus on complex high-net-worth cases.

Future Outlook

The South Korea wealth management market is poised for steady expansion as household financial assets grow and investors diversify beyond deposits and property. Digital advisory, AI-driven personalization, and integrated retirement planning will deepen engagement across affluent tiers. Regulatory support for diversified long-term investment and cross-border access will broaden product shelves. Consolidation among bank-securities groups and platformization of alternatives will reinforce scale advantages. Demand for holistic, lifecycle-based wealth solutions will sustain advisory growth.

Major Players

- KB Financial Group

- Shinhan Financial Group

- Hana Financial Group

- Samsung Securities

- Mirae Asset Securities

- NH Investment & Securities

- Korea Investment & Securities

- Woori Bank Wealth Management

- Standard Chartered Korea

- UBS Korea

- Citi Private Bank Korea

- BNP Paribas Wealth Management Korea

- Goldman Sachs Korea

- Morgan Stanley Korea

- AIA Korea Wealth

Key Target Audience

- Private banks

- Securities firms

- Asset management companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Pension funds

- Insurance companies

- Family offices

Research Methodology

Step 1: Identification of Key Variables

Key variables included assets under management by client tier, asset class allocation, discretionary mandate penetration, and distribution channel structure. Regulatory provisions on pensions, cross-border investment, and suitability were mapped. Household financial accounts and institutional disclosures informed baseline asset estimates.

Step 2: Market Analysis and Construction

Central bank flow of funds data, supervisory filings, and company reports were synthesized to quantify managed financial assets. Segmentation by client and asset class was constructed from platform disclosures and industry associations. Competitive positioning assessed via AUM scale, digital capability, and product breadth.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on retirement demand, alternatives uptake, and fee trends were validated with practitioners across private banking, brokerage, and asset management. Regulatory interpretations and product structures cross-checked with compliance specialists. Iterative reviews reconciled divergent estimates.

Step 4: Research Synthesis and Final Output

Quantitative findings integrated with qualitative drivers and challenges into structured sections aligned to outlook requirements. Tables standardized to ensure internal consistency with verified statistics. Final narrative refined for analytical clarity and policy relevance.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising concentration of high net worth assets among entrepreneurs and chaebol families

Expansion of securities firm wealth management divisions

Growing demand for global asset diversification and alternatives - Market Challenges

Conservative investor bias toward deposits and real estate

Regulatory constraints on offshore wealth structuring

Fee compression from digital and robo-advisory entrants - Market Opportunities

Digital wealth platforms for emerging affluent investors

Global alternative and private market investments

Intergenerational wealth transfer advisory services - Trends

Shift toward holistic life-cycle wealth planning

Integration of AI-driven portfolio analytics and reporting - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory and Financial Planning

Trust and Estate Services

Alternative Investment Advisory

Retirement and Pension Solutions - By Platform Type (In Value%)

Private Bank Wealth Platforms

Securities Brokerage Wealth Platforms

Independent Wealth Advisory Firms

Digital Wealth and Robo-advisory Platforms

Universal Bank Wealth Divisions - By Fitment Type (In Value%)

Onshore Wealth Management

Offshore Wealth Management

Hybrid Advisory Models

Fully Digital Wealth Solutions - By End User Segment (In Value%)

High Net Worth Individuals

Ultra High Net Worth Individuals

Affluent Mass Segment

- Market Share Analysis

- Cross Comparison Parameters (Client Segment Focus, Asset Class Coverage, Advisory Model, Digital Platform Capability, Pricing Structure, Relationship Management Depth, Global Investment Access, Alternative Investment Capability, Portfolio Customization Level, Regulatory Compliance Strength)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

KB Kookmin Bank WM

Shinhan Bank PWM

Hana Bank Wealth Management

Woori Bank Wealth Management

NH Investment & Securities WM

Samsung Securities

Mirae Asset Securities WM

Korea Investment & Securities WM

Kiwoom Securities Wealth

KB Securities WM

Shinhan Investment Corp WM

Hana Securities WM

Daishin Securities WM

Eugene Investment & Securities WM

Meritz Securities WM

- Entrepreneurial wealth seeking institutional-grade advisory services

- Affluent professionals increasing managed investment allocation

- Family offices formalizing governance and succession planning

- Retirees shifting assets into income-oriented portfolios

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now