Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Spain AI infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by hyperscale cloud expansion, enterprise AI adoption, and public sector digitalization programs across industries such as finance, manufacturing, and healthcare. Investments in GPU servers, AI accelerators, high-performance storage, and data center upgrades increased infrastructure demand. European digital sovereignty initiatives and national AI strategies further stimulated deployment of domestic compute capacity and advanced networking infrastructure across Spain.

Madrid and Barcelona dominate Spain AI infrastructure deployment due to data center concentration, research ecosystem presence, and enterprise headquarters density supporting AI workloads and cloud adoption. Aragón and Catalonia regions are emerging hyperscale corridors driven by renewable energy availability and large campus developments. Spain leads Southern Europe AI infrastructure growth due to strong telecom networks, EU digital funding access, and expanding hyperscale and colocation operator presence supporting regional AI computing demand.

Market Segmentation

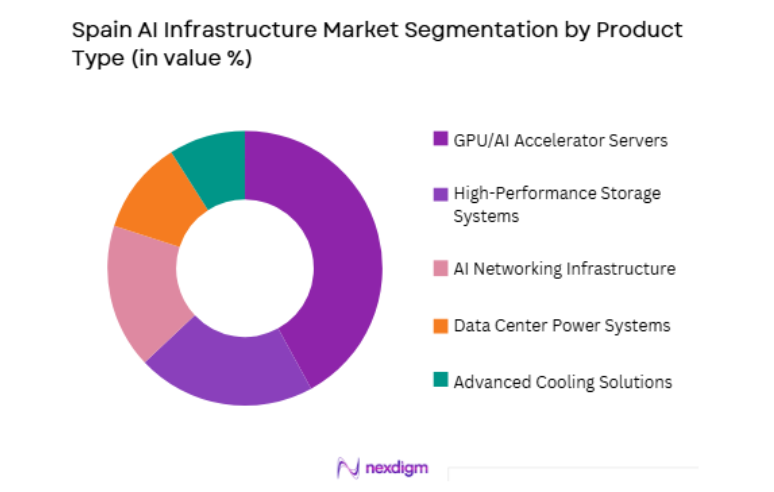

By Product Type

Spain AI Infrastructure market is segmented by product type into GPU/AI accelerator servers, high-performance storage systems, AI networking infrastructure, data center power systems, and advanced cooling solutions. Recently, GPU/AI accelerator servers has a dominant market share due to rapid AI model training and inference workload growth across enterprises and research institutions. Spanish hyperscale and enterprise data centers prioritize GPU clusters for generative AI, analytics, and computer vision applications. National AI programs and university research projects require high-performance compute nodes. Cloud providers expanding Spain regions deploy GPU-dense racks. Financial and manufacturing sectors adopt AI platforms needing accelerators.

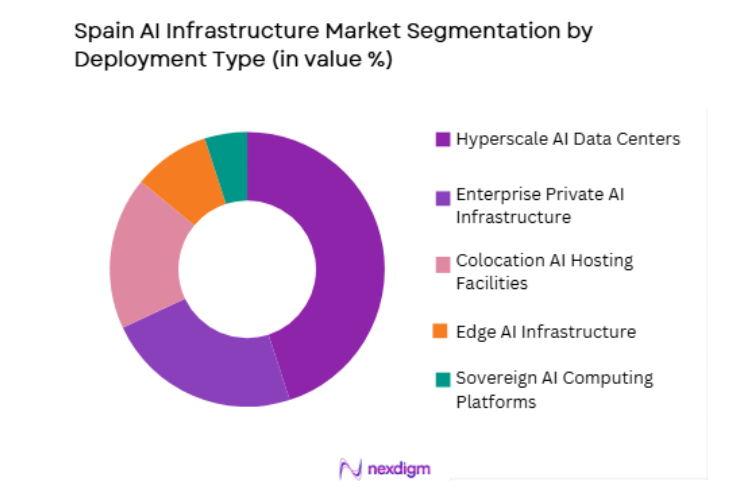

By Deployment Type

Spain AI Infrastructure market is segmented by deployment type into hyperscale AI data centers, enterprise private AI infrastructure, colocation AI hosting facilities, edge AI infrastructure, and sovereign AI computing platforms. Recently, hyperscale AI data centers has a dominant market share due to global cloud providers expanding AI-optimized regions in Spain to serve European demand. Large-scale campuses in Aragón and Madrid provide GPU clusters and high-bandwidth networks for AI workloads. Enterprises prefer hyperscale AI platforms for scalability and cost efficiency. EU digital funding and renewable energy availability support hyperscale expansion. Research and startup ecosystems leverage hyperscale compute access.

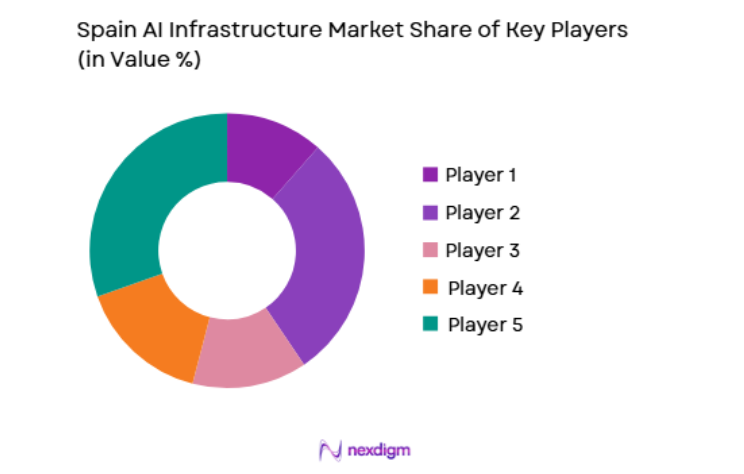

Competitive Landscape

Spain AI infrastructure market is moderately concentrated, shaped by hyperscale cloud providers, global GPU hardware vendors, and European data center operators expanding AI-optimized facilities. International technology firms lead GPU and AI platform deployment, while Spanish telecom and colocation companies enable regional hosting and connectivity. EU digital infrastructure funding and sovereign AI initiatives influence competitive positioning. Strategic partnerships between hardware vendors and cloud providers accelerate AI infrastructure expansion across Spain.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Spain AI Data Center Presence |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | USA | ~ | ~ | ~ | ~ | ~ |

| Equinix | 1998 | USA | ~ | ~ | ~ | ~ | ~ |

Spain AI Infrastructure Market Analysis

Growth Drivers

Enterprise and public sector AI adoption acceleration

Rapid adoption of artificial intelligence across Spanish enterprises and public sector institutions is significantly increasing demand for dedicated AI infrastructure including GPU servers, high-bandwidth networking, and scalable storage deployed within national data center regions. Financial services, healthcare providers, manufacturing firms, and retail companies are integrating AI into analytics, automation, and customer engagement platforms, requiring large-scale compute resources for model training and inference workloads locally. Public administration modernization programs and national digital services initiatives rely on AI-enabled platforms for citizen services, fraud detection, and decision support, further expanding infrastructure deployment requirements across Spain. Universities and research institutes conducting machine learning and scientific computing projects require high-performance clusters, contributing to sustained procurement of accelerators and AI-optimized systems nationwide. Hyperscale cloud providers expanding Spanish regions offer AI compute instances, enabling enterprises to scale AI workloads without building private clusters, accelerating infrastructure consumption within the country. Startup ecosystems in Madrid and Barcelona leverage cloud-based GPU infrastructure for generative AI and data analytics innovation, driving continuous utilization growth and regional data center capacity expansion. Industrial digitalization programs in automotive, energy, and logistics sectors adopt AI for predictive maintenance, quality control, and optimization, increasing demand for edge and core AI compute nodes deployed domestically. Spanish language AI model development and localized data processing requirements further encourage deployment of national compute capacity aligned with European data governance expectations.

Hyperscale and sovereign AI computing investments in Spain

Spain is emerging as a strategic location for hyperscale AI computing infrastructure within Europe due to renewable energy availability, EU digital funding, and supportive national AI strategy encouraging domestic compute capacity development. Global cloud providers are establishing AI-optimized data center campuses in regions such as Aragón and Madrid, deploying high-density GPU clusters and advanced cooling systems to serve European AI workloads locally. Government initiatives supporting sovereign AI capabilities encourage partnerships between hyperscalers, telecom operators, and research institutions to build compliant national AI computing platforms. EU recovery and digital transformation funds are financing AI supercomputing facilities, research infrastructure, and cloud expansion projects across Spain. Renewable energy resources including solar and wind enable sustainable operation of energy-intensive AI data centers, attracting providers seeking low-carbon infrastructure footprints within Europe. Spain’s geographic position and connectivity links to Europe, Africa, and Latin America enhance its attractiveness as regional AI infrastructure hub serving multilingual markets. Colocation and telecom operators expand AI-ready facilities with liquid cooling and high-capacity power systems to host hyperscale and enterprise GPU deployments. Semiconductor supply chain partnerships and European chip initiatives support long-term AI hardware availability and infrastructure expansion across Spain.

Market Challenges

High capital intensity and energy demand of AI infrastructure

Spain AI infrastructure development faces substantial capital and operational challenges due to the high cost and energy intensity of GPU-dense data centers and AI supercomputing facilities required for advanced workloads. AI accelerator servers and high-performance networking equipment are significantly more expensive than conventional IT hardware, increasing upfront investment requirements for hyperscale and enterprise operators deploying AI clusters. Power consumption of large AI training environments is extremely high, requiring robust grid connectivity, dedicated substations, and advanced cooling systems that elevate construction and operational expenditure across Spain facilities. Renewable energy procurement and long-term power agreements are necessary to maintain sustainability and cost stability, adding complexity and financial commitments for infrastructure developers. Rapid hardware obsolescence in AI accelerators requires frequent refresh cycles, increasing lifecycle costs and financial risk for operators and investors in Spanish AI infrastructure. Smaller enterprises and research organizations face affordability barriers to deploying private AI infrastructure, limiting adoption outside hyperscale and government funded environments. Grid capacity constraints and regional permitting processes can delay AI data center projects, affecting deployment timelines and capacity planning across Spain. Environmental regulations and community concerns regarding energy consumption and land use impose additional compliance and mitigation costs for new facilities.

Dependence on external semiconductor and accelerator supply chains

Spain AI infrastructure market depends heavily on global semiconductor and AI accelerator supply chains dominated by a limited number of international hardware vendors, creating strategic vulnerability and procurement risks for national infrastructure expansion. GPU and AI chip availability fluctuations and export control policies can affect procurement timelines and costs for hyperscale and enterprise deployments within Spain. Concentration of advanced semiconductor manufacturing outside Europe limits local sourcing options, exposing Spanish infrastructure projects to geopolitical and supply disruptions. Long lead times for high-end accelerators delay deployment of AI clusters and supercomputing facilities required by enterprises and research institutions nationwide. Price volatility in AI hardware components increases capital planning uncertainty for infrastructure investors and operators in Spain. European semiconductor initiatives are still developing and may not immediately address short term AI accelerator supply constraints affecting infrastructure deployment. Dependence on external hardware ecosystems also affects software compatibility and vendor lock-in risks across AI infrastructure environments. National sovereignty objectives for AI computing are challenged by reliance on foreign semiconductor technology platforms and supply chains.

Opportunities

Development of sovereign European AI supercomputing hubs in Spain

Spain has strong opportunity to become a leading location for sovereign European AI supercomputing and high-performance computing hubs aligned with EU digital sovereignty and AI strategy objectives. Government and EU funded supercomputing initiatives support deployment of large GPU clusters and AI-optimized facilities serving research, public sector, and industrial applications across Europe. Spain’s renewable energy resources and available land enable construction of sustainable AI campuses meeting environmental and regulatory requirements. Collaboration between hyperscalers, telecom operators, and national research centers can create hybrid sovereign AI platforms combining commercial and public infrastructure capabilities. European language model development and regional data processing requirements create sustained demand for domestic AI compute capacity hosted within Spain. Integration of national supercomputing centers with cloud platforms enables scalable access to AI infrastructure for enterprises and startups across Spain and neighboring regions. Spain’s connectivity to Africa and Latin America positions it as multilingual AI computing gateway supporting cross-regional digital services. EU semiconductor and digital funding programs can finance infrastructure expansion and hardware procurement for sovereign AI facilities in Spain.

Expansion of AI infrastructure for industrial and edge applications

Spain presents significant opportunity for distributed AI infrastructure supporting industrial automation, smart cities, autonomous systems, and edge computing applications across sectors such as manufacturing, energy, transportation, and agriculture. Industrial digitalization initiatives require localized AI processing near factories, logistics hubs, and energy facilities, driving deployment of edge GPU nodes and micro data centers nationwide. Smart city programs in Spanish municipalities integrate AI for mobility, surveillance, and environmental monitoring, creating demand for urban edge infrastructure and connectivity platforms. Renewable energy sector digitization uses AI for grid optimization, forecasting, and asset management, requiring distributed compute resources across energy networks. Autonomous transport and drone applications require low latency AI inference infrastructure deployed closer to operational environments. Telecom operators can leverage 5G networks to host AI edge platforms supporting enterprise and public services applications. Spanish industrial clusters and ports present concentrated demand zones for localized AI compute deployment. Integration of edge and hyperscale AI architectures creates multi tier infrastructure ecosystem expanding national hardware demand. EU industrial digital transformation funding supports deployment of AI infrastructure across regional economic sectors.

Future Outlook

Spain AI infrastructure market is expected to expand rapidly driven by hyperscale AI campus development, sovereign computing initiatives, and enterprise AI adoption across industries. Renewable energy integration and EU digital funding will support sustainable data center growth. Expansion of edge AI and industrial applications will diversify infrastructure deployment.

Major Players

- NVIDIA

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Oracle

- IBM

- Equinix

- Telefónica

- Submer

- Iberdrola Digital Infra

- NxN Data Centers

- ODATA

- Digital Realty

- NTT Global Data Centers

- Lenovo

Key Target Audience

- Cloud service providers

- Telecommunications operators

- Data center operators

- Enterprise AI platform buyers

- Government and regulatory bodies

- Investments and venture capitalist firms

- Industrial automation companies

- Financial institutions

Research Methodology

Step 1: Identification of Key Variables

AI infrastructure components including accelerators, networking, storage, and facility systems were mapped across hyperscale, enterprise, edge, and sovereign platforms. Demand drivers, regulatory factors, and technology adoption indicators were identified across Spain regions.

Step 2: Market Analysis and Construction

Supply and demand trends were analyzed using data center deployments, AI hardware adoption, and hyperscale expansion indicators across Spain. Market sizing integrated accelerator procurement, facility investment, and AI workload growth patterns.

Step 3: Hypothesis Validation and Expert Consultation

Infrastructure deployment assumptions and growth drivers were validated through consultation with data center operators, AI hardware vendors, and telecom providers. Policy and funding dynamics were cross-checked against EU and national sources.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into structured estimates, segmentation, and forecasts. Competitive positioning, investment trends, and infrastructure scenarios were consolidated into final analytical outputs.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of European AI and cloud infrastructure programs

Rising enterprise adoption of AI and data analytics

Growth of hyperscale and colocation AI data centers - Market Challenges

High energy costs for AI compute intensive facilities

Dependence on imported AI chips and hardware

Data sovereignty and regulatory compliance complexity - Market Opportunities

Sovereign AI cloud and HPC infrastructure initiatives

AI adoption across manufacturing and public services

Renewable powered AI data center expansion - Trends

Adoption of GPU dense AI clusters

Liquid cooling deployment in AI data centers - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Compute Servers

GPU and Accelerator Hardware

AI Storage Infrastructure

High Speed Networking Systems

AI Data Center Power and Cooling - By Platform Type (In Value%)

Hyperscale AI Cloud Infrastructure

Enterprise AI Data Centers

Edge AI Infrastructure

Telecom AI Infrastructure

Government and Research AI Clusters - By Fitment Type (In Value%)

New AI Data Center Builds

AI Infrastructure Retrofits

Modular AI Data Centers

Integrated Turnkey AI Facilities - By End User Segment (In Value%)

Cloud Service Providers

Enterprises

Government and Research Institutions

Telecom Operators

- Market Share Analysis

- Cross Comparison Parameters (Compute Density, Energy Efficiency, Cooling Architecture, AI Accelerator Integration, Network Bandwidth, Scalability, Power Utilization Effectiveness, Deployment Flexibility, Latency Performance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

AMD

Intel

Dell Technologies

Hewlett Packard Enterprise

Lenovo

Supermicro

IBM

Cisco

Oracle

Microsoft

Google

Amazon Web Services

Equinix

OVHcloud

- Cloud providers expanding AI regions in Spain

- Enterprises deploying private AI infrastructure

- Public sector investing in sovereign AI capacity

- Telecom operators integrating AI into networks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now