Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Spain’s cloud infrastructure market reached approximately USD ~ billion based on a recent historical assessment, reflecting sustained enterprise and public sector investment in hyperscale data centers, virtualization platforms, and hybrid cloud environments according to European Commission digital infrastructure statistics and Spain’s Ministry of Economic Affairs ICT investment disclosures. Growth is driven by enterprise migration from legacy IT to scalable cloud architectures, rising AI and analytics workloads, and telecom operator expansion of edge computing infrastructure supporting digital services and 5G ecosystems nationwide.

Madrid and Barcelona dominate Spain’s cloud infrastructure landscape due to dense enterprise concentration, strong fiber connectivity, and established data center clusters supported by national digitalization programs and European cloud initiatives. These metropolitan regions host hyperscale facilities, telecom cloud nodes, and financial sector infrastructure modernization projects, while secondary hubs such as Valencia and Zaragoza expand colocation and edge deployments because of renewable energy access, land availability, and proximity to national connectivity corridors linking Iberian and European digital networks.

Market Segmentation

By Product Type

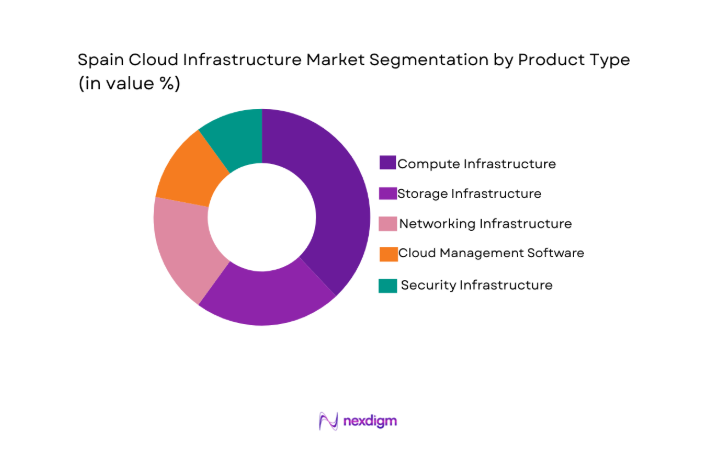

Spain Cloud Infrastructure market is segmented by product type into compute infrastructure, storage infrastructure, networking infrastructure, cloud management software, and security infrastructure. Recently, compute infrastructure has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. The segment leads because hyperscale data center expansion and enterprise cloud migration require high density servers, accelerators, and virtualization stacks that form the foundational layer of all cloud deployments across public, private, and hybrid environments in Spain.

By Platform Type

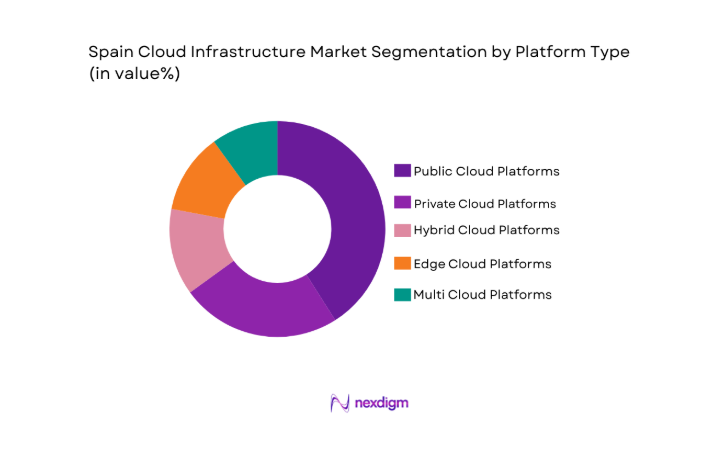

Spain Cloud Infrastructure market is segmented by platform type into public cloud platforms, private cloud platforms, hybrid cloud platforms, edge cloud platforms, and multi cloud platforms. Recently, public cloud platforms have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Public platforms lead because enterprises and government agencies increasingly adopt scalable pay as you go infrastructure hosted in hyperscale facilities across Madrid and Barcelona, reducing capital expenditure while enabling rapid deployment of digital services and analytics workloads.

Competitive Landscape

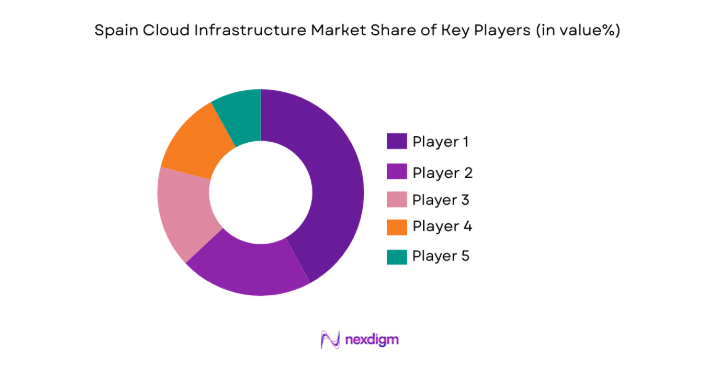

Spain’s cloud infrastructure market shows moderate consolidation with global hyperscale providers and large telecom-integrated technology firms controlling core infrastructure layers, while domestic hosting and colocation companies compete in regulated and sovereign cloud segments. International vendors shape technology standards and enterprise adoption, whereas local operators leverage regional data residency, connectivity assets, and public sector relationships to sustain competitive positioning in government and financial industry deployments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Spain Data Center Presence |

| Amazon Web Services Spain | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Spain | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud Spain | 2008 | USA | ~ | ~ | ~ | ~ | ~ |

| Telefónica Tech | 2019 | Spain | ~ | ~ | ~ | ~ | ~ |

| OVHcloud Spain | 1999 | France | ~ | ~ | ~ | ~ | ~ |

Spain Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise Digital Transformation and Hybrid Cloud Migration Acceleration

Spain’s cloud infrastructure demand is strongly propelled by large scale enterprise digital transformation programs that prioritize hybrid and multi cloud adoption across banking, telecom, manufacturing, and retail sectors seeking operational agility and cost optimization. Organizations are replacing legacy on premise systems with scalable virtualized infrastructure to support data intensive workloads, advanced analytics, and AI driven applications required for competitiveness in digital markets. National digitalization funding and EU recovery investments encourage cloud adoption among mid sized enterprises, expanding infrastructure demand beyond large corporations into broader economic segments. Telecom operators and system integrators promote hybrid architectures combining private enterprise clouds with hyperscale public platforms, creating sustained procurement cycles for compute, storage, and networking infrastructure across Spain. Data sovereignty requirements in regulated industries further drive domestic cloud infrastructure deployment, as enterprises prefer locally hosted environments meeting EU compliance standards while still leveraging hyperscale scalability. Rapid growth of software as a service ecosystems and cloud native development practices requires container platforms, orchestration layers, and distributed compute clusters, intensifying infrastructure expansion within enterprise and service provider data centers. Spanish companies increasingly deploy cloud based ERP, CRM, and digital customer platforms, which depend on resilient infrastructure layers and high availability architectures to support business continuity and digital commerce operations. The combination of modernization urgency, regulatory compliance, and competitive digitalization pressure ensures sustained expansion of hybrid cloud infrastructure investments across Spain’s enterprise landscape.

Hyperscale Data Center Expansion and Telecom Edge Infrastructure Deployment

The Spanish cloud infrastructure market experiences strong growth from hyperscale data center investments and telecom operator edge computing rollout that together expand national cloud capacity and distributed processing capabilities. Global cloud providers continue establishing large scale facilities in Madrid and Barcelona due to connectivity density, renewable energy availability, and proximity to enterprise demand centers, significantly increasing national compute and storage supply. Telecom companies deploy edge cloud nodes within 5G networks to support latency sensitive services such as autonomous systems, smart cities, and industrial IoT applications, creating new distributed infrastructure layers beyond centralized data centers. Government digital sovereignty initiatives encourage domestic cloud regions and regulated industry hosting environments, reinforcing local hyperscale and edge infrastructure investments. Rising adoption of AI training and inference workloads requires high performance computing clusters and GPU dense architectures that are primarily delivered through hyperscale cloud facilities, intensifying infrastructure procurement cycles. Content delivery networks, streaming platforms, and digital media services further stimulate edge and core cloud capacity expansion to manage growing data traffic volumes across Spain’s digital economy. Infrastructure colocation providers and telecom carriers collaborate with hyperscalers to integrate connectivity and cloud services, accelerating deployment of integrated cloud ecosystems nationwide. The combined effect of hyperscale expansion and edge distribution creates a layered national cloud architecture that continuously drives infrastructure investment and market growth.

Market Challenges

High Energy Costs and Sustainability Constraints in Data Center Operations

Spain’s cloud infrastructure expansion faces structural challenges from rising electricity costs and sustainability requirements that significantly influence data center economics and long term infrastructure planning. Cloud facilities demand large continuous power loads for compute clusters and cooling systems, making operational costs sensitive to energy price volatility in European electricity markets. Environmental regulations and carbon reduction targets require operators to adopt renewable energy sourcing, advanced cooling technologies, and energy efficient hardware, increasing capital expenditure and deployment complexity. Grid capacity limitations in major metropolitan areas constrain new hyperscale construction and require coordination with national energy infrastructure upgrades to support cloud expansion. Enterprises and public sector clients increasingly demand low carbon digital services, forcing providers to invest in green data center certifications and energy optimization technologies to remain competitive. Thermal management challenges intensify with high density AI and GPU workloads, raising cooling infrastructure requirements and facility design complexity in Spain’s climate conditions. Water usage constraints and environmental permitting processes extend project timelines for new cloud facilities, affecting market supply responsiveness to demand growth. Smaller domestic hosting firms face financial strain adapting to sustainability standards compared to global hyperscale providers with larger capital resources. These energy and environmental constraints collectively slow infrastructure deployment cycles and increase operational costs across Spain’s cloud ecosystem.

Data Sovereignty Compliance and Cybersecurity Risk Complexity

Spain’s cloud infrastructure market must navigate complex regulatory frameworks governing data sovereignty, privacy protection, and cybersecurity resilience that create operational and architectural challenges for providers and users. European data protection regulations require strict localization, access control, and processing transparency for sensitive data, compelling cloud operators to design region specific infrastructure and governance models. Regulated sectors such as finance, healthcare, and government demand sovereign cloud environments with domestic hosting, certified security controls, and restricted cross border data flows, limiting scalability of standardized global cloud architectures. Increasing cyber threats targeting cloud platforms necessitate continuous investment in security monitoring, encryption, and resilience capabilities, raising infrastructure costs and technical complexity. Multi cloud and hybrid architectures expand attack surfaces and integration risks, requiring sophisticated identity management and network segmentation solutions across distributed environments. Compliance audits, certifications, and reporting obligations create administrative burdens and slow deployment of new cloud services within regulated organizations. Enterprises often maintain parallel private infrastructure to meet compliance requirements, reducing full public cloud adoption and complicating hybrid deployments. Geopolitical concerns over foreign technology providers encourage sovereign infrastructure initiatives, reshaping competitive dynamics and procurement decisions in Spain’s cloud market. These regulatory and security complexities impose persistent barriers to seamless cloud infrastructure scaling.

Opportunities

Sovereign Cloud and Regulated Industry Infrastructure Development

Spain’s cloud infrastructure market holds significant opportunity in sovereign and regulated sector cloud platforms tailored to national data residency and compliance requirements across government, finance, and critical industries. European digital sovereignty initiatives encourage domestic cloud ecosystems independent of extraterritorial jurisdiction, driving demand for locally controlled infrastructure and software stacks. Spanish public sector modernization programs prioritize sovereign cloud adoption for sensitive administrative and citizen data, generating sustained infrastructure procurement and long term service contracts. Financial institutions and healthcare providers increasingly seek compliant private and hybrid cloud environments hosted within national borders, expanding market space for certified data center and cloud platforms. Domestic telecom and technology firms can leverage local presence and regulatory alignment to compete against global hyperscalers in sovereign segments, strengthening national cloud capacity. Development of trusted cloud certification frameworks and interoperability standards further supports adoption across regulated sectors requiring verifiable compliance and security assurance. Integration of sovereign cloud platforms with EU digital identity, cybersecurity, and data space initiatives will create interconnected national cloud infrastructures across Europe, enhancing Spain’s strategic cloud role. The expansion of sovereign and regulated cloud ecosystems represents a major structural growth avenue for Spain’s infrastructure providers.

Edge Cloud Infrastructure for 5G, Smart Cities, and Industrial IoT Ecosystems

Spain’s advancing 5G deployment and digital infrastructure strategies create strong opportunity for distributed edge cloud architectures supporting latency sensitive applications across urban, industrial, and transportation environments. Telecom operators are integrating edge computing nodes within network infrastructure to enable real time analytics, automation, and immersive services requiring local processing capacity. Smart city initiatives in metropolitan regions demand edge cloud platforms for traffic management, surveillance analytics, and connected public services operating with minimal latency. Industrial IoT adoption in manufacturing and logistics sectors requires localized cloud processing for robotics control, predictive maintenance, and autonomous systems functioning within private networks. Autonomous mobility and intelligent transportation systems depend on edge infrastructure along highways and urban corridors to process sensor and navigation data in real time. Content delivery and media streaming services expand edge caching and processing nodes to meet growing digital consumption across Spain’s population centers. Integration of edge and core cloud layers creates distributed national cloud fabrics, generating sustained demand for micro data centers and telecom cloud hardware. The proliferation of edge driven digital ecosystems positions distributed cloud infrastructure as a central growth frontier in Spain’s cloud market.

Future Outlook

Spain’s cloud infrastructure market is expected to expand steadily as hyperscale capacity, sovereign cloud initiatives, and telecom edge deployments reshape national digital architecture. Continued enterprise hybrid adoption, AI workload growth, and EU backed digital sovereignty programs will stimulate sustained infrastructure investment. Renewable energy integration and green data center innovation will shape facility expansion strategies. Regional edge nodes and industry specific clouds will broaden market depth across sectors and geographies.

Major Players

- Amazon Web Services Spain

- Microsoft Spain

- Google Cloud Spain

- Telefónica Tech

- OVHcloud Spain

- IBM Spain

- Oracle Spain

- NTT DATA Spain

- Capgemini Spain

- Atos Spain

- Indra Sistemas

- Equinix Spain

- Gigas Hosting

- Arsys

- Huawei Cloud Spain

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Telecom operators

- Cloud service providers

- Data center operators

- Banking and financial institutions

- Large enterprises undergoing digital transformation

- Industrial and manufacturing corporations

Research Methodology

Step 1: Identification of Key Variables

Key demand and supply variables such as data center capacity, enterprise cloud adoption, hyperscale investment, and regulatory drivers were identified through European ICT databases and national digital economy indicators. Market boundaries and infrastructure categories were defined to isolate Spain’s cloud infrastructure components from broader IT services sectors.

Step 2: Market Analysis and Construction

Infrastructure spending, capacity deployment, and enterprise adoption patterns were synthesized using government ICT investment reports, telecom infrastructure disclosures, and European cloud market datasets. Segment structures were constructed around product and platform architecture layers to reflect actual procurement and deployment behavior in Spain.

Step 3: Hypothesis Validation and Expert Consultation

Findings and assumptions were validated against cloud provider announcements, data center operator disclosures, and telecom infrastructure expansion plans within Spain. Regulatory and sovereignty factors were cross checked with EU digital policy frameworks and national cybersecurity strategies influencing infrastructure investment decisions.

Step 4: Research Synthesis and Final Output

All validated data streams were integrated into a coherent market model reflecting Spain’s cloud infrastructure ecosystem structure, segmentation, and competitive dynamics. Final outputs were synthesized to ensure consistency across quantitative indicators, qualitative drivers, and forward outlook aligned with national digitalization trajectories.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National digital transformation and cloud first government policies

Expansion of hyperscale data center investments across Spain

Rising enterprise adoption of hybrid and multi cloud architectures

Growth of AI, analytics, and high performance computing workloads

5G and edge computing infrastructure deployment acceleration - Market Challenges

Data sovereignty and EU compliance complexity for cloud deployments

High energy costs impacting data center and cloud operations

Legacy IT integration barriers in traditional enterprises

Shortage of skilled cloud and DevOps professionals

Cybersecurity risks in distributed cloud environments - Market Opportunities

Expansion of sovereign and regulated industry clouds

Edge cloud infrastructure for smart cities and IoT ecosystems

Sustainable green data center and cloud infrastructure initiatives - Trends

Shift toward sovereign cloud and regional data residency solutions

Adoption of containerized and cloud native platforms

Integration of AI infrastructure within cloud environments

Rise of edge cloud nodes in telecom networks

Growth of managed multi cloud services - Government Regulations & Defense Policy

EU GDPR and data residency enforcement frameworks

Spanish national cybersecurity and digital infrastructure policies

Green energy and sustainable data center compliance mandates - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Edge Cloud Infrastructure

Multi Cloud Management Infrastructure - By Platform Type (In Value%)

Hyperscale Data Center Platforms

Enterprise Virtualization Platforms

Container and Kubernetes Platforms

Serverless Computing Platforms

Edge and Distributed Cloud Platforms - By Fitment Type (In Value%)

Greenfield Cloud Deployments

Brownfield Data Center Modernization

Colocation Integrated Cloud

On Premise Cloud Stacks

Hosted Private Cloud Installations - By EndUser Segment (In Value%)

Telecom and Digital Service Providers

Banking and Financial Institutions

Government and Public Sector

Retail and E Commerce Enterprises

Manufacturing and Industrial Enterprises - By Procurement Channel (In Value%)

Direct OEM Procurement

Cloud Service Provider Contracts

System Integrator Partnerships

Telecom Operator Bundled Procurement

Government Framework Agreements

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Cloud Service Portfolio Breadth, Data Center Presence in Spain, Sovereign Cloud Capability, Edge Infrastructure Integration, Industry Specific Cloud Solutions)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Telefónica Tech

Indra Sistemas

Atos Spain

Capgemini Spain

IBM Spain

Microsoft Spain

Amazon Web Services Spain

Google Cloud Spain

Oracle Spain

Arsys

Gigas Hosting

OVHcloud Spain

Equinix Spain

NTT DATA Spain

Huawei Cloud Spain

- Telecom operators driving edge and distributed cloud deployments

- Financial institutions prioritizing secure private and hybrid clouds

- Public sector accelerating sovereign and compliant cloud adoption

- Enterprises modernizing legacy IT through hybrid architectures

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now