Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Spain cold chain logistics market is valued at approximately USD ~ billion based on data reported by Eurostat and the Spanish Ministry of Transport, Mobility and Urban Agenda reflecting the scale of refrigerated transportation and temperature controlled warehousing infrastructure. The market is primarily driven by expanding pharmaceutical distribution networks, increasing frozen food consumption, and strong agricultural export activity. Logistics providers operate extensive refrigerated fleets and cold storage facilities supporting food processing companies, supermarkets, and pharmaceutical manufacturers requiring strict temperature management across national supply chains.

Madrid, Barcelona, Valencia, and Seville function as dominant logistics hubs due to strong transportation infrastructure, high population density, and concentration of food processing and pharmaceutical industries. These metropolitan areas host large cold storage warehouses, distribution centers, and intermodal transport terminals that connect production regions with domestic retail markets and international export routes. Coastal cities such as Valencia and Barcelona also benefit from major seaports facilitating refrigerated container exports of seafood, fruits, and vegetables across European and global supply chains.

Market Segmentation

By Product Type

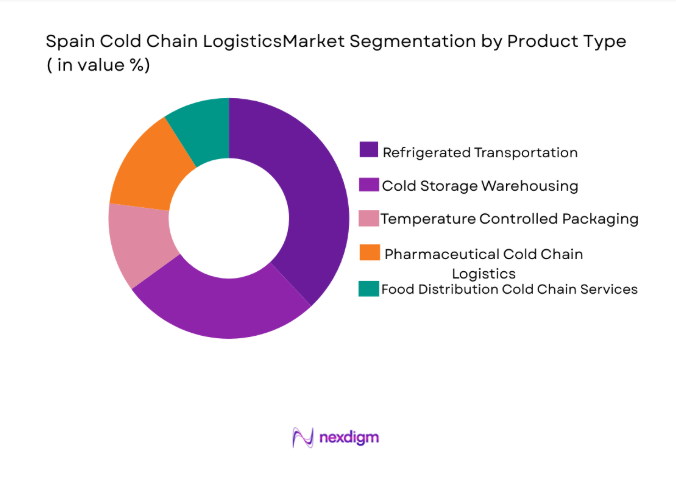

Spain Cold Chain Logistics market is segmented by product type into refrigerated transportation, cold storage warehousing, temperature controlled packaging, pharmaceutical cold chain logistics, and food distribution cold chain services. Recently, refrigerated transportation has a dominant market share due to factors such as nationwide food distribution requirements, strong agricultural exports, and large supermarket retail networks demanding continuous temperature controlled deliveries. Supermarkets, food processors, and pharmaceutical distributors rely heavily on refrigerated trucking fleets capable of maintaining precise temperature conditions during long distance transportation across Spain. Increasing consumption of frozen food products and expansion of pharmaceutical distribution further strengthens demand for refrigerated transport infrastructure linking manufacturing facilities, warehouses, ports, and retail distribution networks throughout the country.

By Platform Type

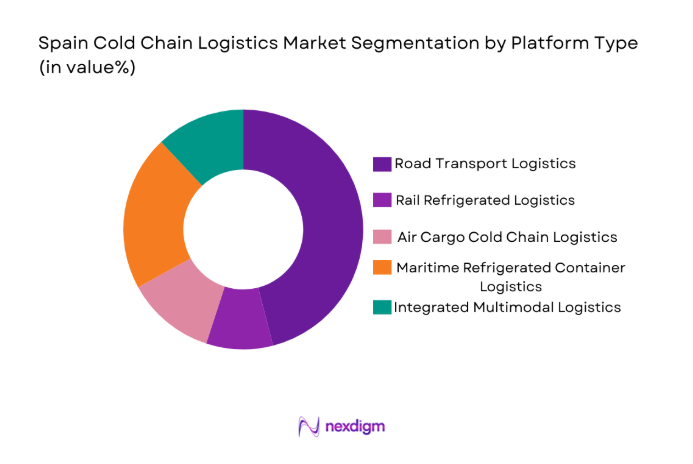

Spain Cold Chain Logistics market is segmented by platform type into road transport logistics, rail refrigerated logistics, air cargo cold chain logistics, maritime refrigerated container logistics, and integrated multimodal logistics networks. Recently, road transport logistics has a dominant market share due to factors such as Spain’s extensive highway infrastructure, flexibility of refrigerated trucking fleets, and strong domestic distribution demand for food and pharmaceutical products. Retail chains and food manufacturers rely heavily on road based refrigerated transportation for timely delivery of perishable goods between production sites, warehouses, and retail outlets. Road logistics also supports last mile distribution for supermarkets and pharmaceutical distributors, making it the most operationally efficient platform across Spain’s cold chain logistics ecosystem.

Competitive Landscape

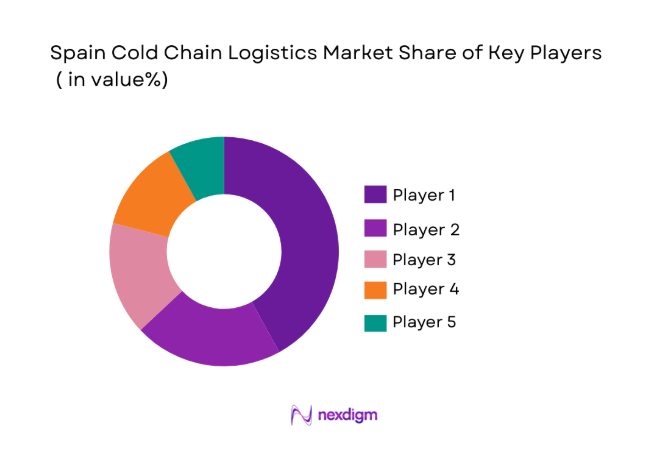

Spain cold chain logistics market is moderately consolidated with large international logistics providers operating alongside specialized regional refrigerated transport companies. Major players maintain extensive cold storage infrastructure, refrigerated truck fleets, and advanced temperature monitoring technologies that support pharmaceutical distribution and food supply chains. Global logistics corporations compete through integrated logistics solutions, while domestic operators focus on regional distribution efficiency and agricultural export logistics.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Refrigerated Fleet Size |

| Lineage Logistics | 2008 | United States | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| XPO Logistics | 1989 | United States | ~ | ~ | ~ | ~ | ~ |

| STEF Group | 1920 | France | ~ | ~ | ~ | ~ | ~ |

| Carreras Grupo Logístico | 1933 | Spain | ~ | ~ | ~ | ~ | ~ |

Spain Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Pharmaceutical Distribution and Biopharmaceutical Logistics Infrastructure

Spain’s pharmaceutical manufacturing sector and national healthcare distribution networks require highly reliable cold chain logistics systems capable of maintaining strict temperature ranges during storage and transportation of sensitive medical products. Biologic medicines, vaccines, insulin products, and specialty pharmaceuticals must remain within validated temperature conditions to preserve their therapeutic stability and regulatory compliance throughout distribution. Pharmaceutical manufacturers therefore depend heavily on specialized logistics providers that operate temperature controlled warehouses, refrigerated vehicles, and advanced monitoring technologies ensuring product integrity across supply chains. The expansion of pharmaceutical exports across European markets further strengthens demand for validated cold chain infrastructure connecting manufacturing facilities with international transportation corridors. Healthcare distributors increasingly implement digital temperature monitoring platforms and automated alert systems capable of detecting temperature fluctuations in real time. These technologies allow logistics providers to maintain regulatory compliance with pharmaceutical good distribution practice requirements enforced across the European Union. Growing healthcare consumption across Spain also increases shipment volumes for temperature sensitive medicines distributed through hospitals, pharmacies, and healthcare distributors nationwide. As pharmaceutical innovation expands with biologics and advanced therapies requiring strict temperature management, demand for specialized cold chain logistics services continues strengthening across the national logistics ecosystem.

Rising Consumption of Frozen and Temperature Controlled Food Products

Changing dietary patterns and expanding supermarket retail networks significantly increase the demand for temperature controlled logistics services across Spain’s food distribution system. Consumers increasingly purchase frozen vegetables, seafood, ready to cook meals, dairy products, and processed foods that require reliable refrigerated storage and transportation from production facilities to retail outlets. Food processing companies therefore depend heavily on refrigerated logistics networks capable of maintaining precise temperature ranges throughout the supply chain. Supermarket chains operate extensive distribution networks connecting centralized cold storage warehouses with thousands of retail stores located across metropolitan and regional markets. Growth of organized retail and online grocery delivery services further increases shipment volumes requiring high efficiency refrigerated transportation systems. Agricultural exporters also require cold chain infrastructure to preserve the quality of fruits, vegetables, and seafood shipped through Spain’s major port terminals to international markets. Logistics providers therefore invest in energy efficient refrigeration technologies and automated warehouse systems designed to improve storage capacity and operational efficiency. As consumer demand for fresh and frozen food continues expanding nationwide, cold chain logistics infrastructure becomes increasingly essential for supporting Spain’s food distribution networks.

Market Challenges

High Operational Costs of Energy Intensive Refrigeration Infrastructure

Cold chain logistics operations require continuous refrigeration across warehouses, transport vehicles, and packaging systems in order to maintain strict temperature conditions for perishable products. These refrigeration systems consume large volumes of electricity which significantly increases operating expenses for logistics providers managing large cold storage facilities and refrigerated vehicle fleets. Rising energy prices across Europe therefore directly impact the profitability of cold chain logistics operators. Warehouses storing frozen food products or pharmaceutical goods must operate powerful refrigeration units around the clock to prevent temperature fluctuations that could damage sensitive cargo. Refrigerated trucking fleets also require specialized cooling equipment that increases fuel consumption during long distance transport operations. Maintenance costs associated with refrigeration systems and temperature monitoring equipment further increase operational expenses for logistics companies. Compliance with food safety and pharmaceutical regulatory requirements also requires extensive monitoring infrastructure and documentation processes. Smaller logistics providers often struggle to invest in energy efficient refrigeration technologies due to high capital costs associated with upgrading warehouse infrastructure. As operational expenses increase across the industry, logistics providers must continuously invest in efficiency improvements in order to maintain competitiveness.

Complex Regulatory Compliance for Pharmaceutical and Food Safety Logistics

Cold chain logistics providers operating in Spain must comply with strict regulatory standards governing the storage and transportation of pharmaceutical products and food items. European Union regulations including pharmaceutical good distribution practice guidelines require validated temperature monitoring, documentation procedures, and quality control systems throughout the supply chain. Logistics companies must implement certified temperature monitoring equipment capable of recording environmental conditions during transportation and storage operations. Food distribution networks are also subject to strict food safety regulations requiring controlled storage conditions for frozen and chilled food products. Regulatory audits conducted by government agencies and pharmaceutical companies require logistics providers to maintain extensive operational records demonstrating compliance with temperature management standards. Meeting these regulatory requirements requires significant investment in digital monitoring technologies and employee training programs. Small and medium sized logistics companies may face operational challenges when attempting to comply with complex documentation and validation procedures required for pharmaceutical cold chain operations. Any failure in temperature management could result in product losses and regulatory penalties affecting logistics providers. Consequently regulatory complexity represents a significant operational challenge within the cold chain logistics industry.

Opportunities

Expansion of Online Grocery Delivery and Urban Food Logistics Networks

Rapid growth of online grocery platforms and digital retail food distribution systems creates strong demand for temperature controlled logistics services across Spain’s urban markets. Consumers increasingly purchase fresh produce, frozen foods, dairy products, and ready to eat meals through digital retail platforms requiring reliable refrigerated delivery infrastructure. Online grocery retailers rely heavily on cold chain logistics providers capable of transporting perishable goods from distribution centers to residential consumers while maintaining strict temperature control. Logistics companies therefore develop urban micro fulfillment centers equipped with temperature controlled storage zones supporting rapid delivery services. Advanced route optimization technologies allow refrigerated delivery fleets to complete high volumes of urban deliveries efficiently while preserving product quality. Supermarket chains also integrate e commerce operations with cold storage distribution facilities supporting omnichannel retail strategies. Investment in refrigerated last mile logistics vehicles and smart packaging technologies further strengthens cold chain delivery capabilities across metropolitan areas. As online grocery adoption continues expanding among urban consumers, demand for flexible cold chain distribution networks will increase significantly.

Investment in Sustainable and Energy Efficient Cold Storage Technologies

The transition toward sustainable logistics infrastructure creates significant opportunities for companies developing energy efficient refrigeration technologies and environmentally friendly cold storage facilities. Logistics providers increasingly invest in modern warehouse designs incorporating advanced insulation materials and automated temperature control systems that reduce electricity consumption. Solar powered refrigeration systems and energy efficient compressors allow cold storage operators to lower operating costs while reducing environmental impact. European environmental policies also encourage adoption of low emission refrigeration technologies across logistics infrastructure supporting long term sustainability objectives. Refrigerated vehicle fleets increasingly adopt electric and hybrid propulsion systems designed to reduce carbon emissions in urban transportation networks. These innovations create opportunities for logistics companies to modernize infrastructure while improving operational efficiency and environmental performance. Government incentives supporting sustainable logistics infrastructure further encourage investment in green cold storage technologies across Spain’s logistics sector. As sustainability requirements become more important across supply chains, companies adopting energy efficient cold chain technologies will gain strong competitive advantages.

Future Outlook

Spain cold chain logistics market is expected to experience steady expansion supported by growing pharmaceutical distribution networks, increasing frozen food consumption, and modernization of refrigerated logistics infrastructure. Technological advancements including automated cold storage warehouses, IoT based temperature monitoring systems, and digital logistics platforms will significantly improve supply chain efficiency. Government sustainability initiatives promoting energy efficient refrigeration systems are likely to influence infrastructure investments across the sector. Continued growth of e commerce grocery delivery and export oriented agricultural trade will further strengthen demand for temperature controlled transportation and storage services.

Major Players

- Lineage Logistics

- DHL Supply Chain

- XPO Logistics

- STEF Group

- Carreras Grupo Logístico

- GXO Logistics

- Kuehne + Nagel

- DB Schenker

- Norbert Dentressangle

- ID Logistics

- Primafrio

- Grupo Fuentes

- Logista

- Dachser

- Frialsa Frigorificos

Key Target Audience

- Food processing and frozen food manufacturing companies

- Pharmaceutical and biotechnology companies

- Supermarket and grocery retail chains

- Logistics and supply chain service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Cold storage infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Market analysis begins with identifying core variables including cold storage capacity, refrigerated fleet size, pharmaceutical logistics demand, food distribution infrastructure, and agricultural export logistics flows. These variables provide the foundational framework for evaluating the operational scale and economic importance of cold chain logistics across Spain.

Step 2: Market Analysis and Construction

Extensive secondary research from government publications, logistics associations, industry reports, and corporate financial disclosures is used to construct the overall market structure. Data sources include transport authorities, food distribution statistics, pharmaceutical supply chain data, and logistics infrastructure reports.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics operators, cold storage providers, and supply chain managers are consulted to validate operational insights and confirm market dynamics. Interviews and consultations help verify industry assumptions and provide deeper understanding of infrastructure capacity and logistics trends.

Step 4: Research Synthesis and Final Output

All collected information is synthesized into structured analytical models assessing market size, competitive landscape, and growth drivers. Quantitative data and qualitative insights are combined to produce a comprehensive analysis of the Spain Cold Chain Logistics market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Pharmaceutical and Biopharmaceutical Distribution Networks

Rising Consumption of Frozen and Processed Food Products

Growth of Export Oriented Agricultural and Seafood Supply Chains - Market Challenges

High Energy Consumption and Operational Costs of Refrigeration Infrastructure

Complex Regulatory Compliance for Pharmaceutical Temperature Control

Infrastructure Limitations in Long Distance Refrigerated Transport - Market Opportunities

Expansion of Pharmaceutical Cold Chain Distribution Infrastructure

Growth of Online Grocery and Fresh Food Delivery Networks

Investment in Energy Efficient Refrigeration Technologies - Trends

Adoption of IoT Enabled Temperature Monitoring Systems

Expansion of Automated Cold Storage Warehousing Facilities - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Transportation Services

Cold Storage Warehousing

Temperature Controlled Packaging Solutions

Pharmaceutical Cold Chain Logistics

Food and Beverage Cold Chain Distribution - By Platform Type (In Value%)

Road Based Refrigerated Transport

Rail Based Refrigerated Transport

Air Freight Cold Chain Logistics

Maritime Refrigerated Container Logistics

Integrated Multimodal Cold Chain Networks - By Fitment Type (In Value%)

Integrated Refrigeration Units

Portable Refrigerated Containers

Modular Cold Storage Systems

Mobile Temperature Monitoring Solutions - By End User Segment (In Value%)

Food and Beverage Manufacturers

Pharmaceutical and Biotechnology Companies

Retail and Supermarket Chains

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio, Refrigerated Fleet Capacity, Cold Storage Infrastructure, Temperature Monitoring Technology, Geographic Coverage, Industry Certifications, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain

Kuehne + Nagel

DB Schenker

XPO Logistics

Lineage Logistics

Frialsa Frigorificos

Grupo Fuentes

Stef Group

Dachser

GXO Logistics

Carreras Grupo Logistico

ID Logistics

Logista

Norbert Dentressangle Iberia

Primafrio

- Food Manufacturers Increasing Dependence on Temperature Controlled Distribution

- Pharmaceutical Companies Requiring Validated Cold Chain Transport Systems

- Retail Chains Expanding Refrigerated Food Supply Networks

- Exporters Utilizing Cold Chain Infrastructure for Perishable Agricultural Trade

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now