Download PDF

Download PDF Download PDF

Download PDFMarket Overview

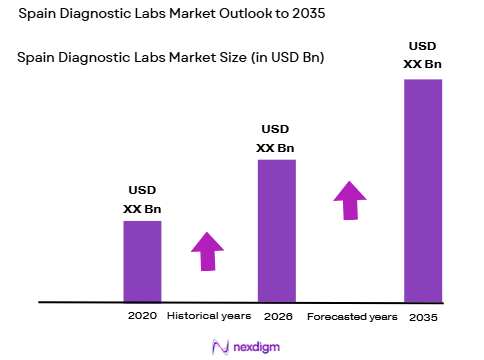

The Spain diagnostic labs market is valued at approximately USD ~ billion based on a recent historical assessment. The market is driven by increasing healthcare demand, the rise in chronic diseases, and advancements in diagnostic technologies. The need for accurate and early disease detection, coupled with the expansion of healthcare infrastructure and government initiatives, has fueled the growth of diagnostic labs in Spain. Additionally, private and public sector investments in diagnostic services are playing a pivotal role in market expansion.

The dominant cities in Spain’s diagnostic labs market are Madrid, Barcelona, and Valencia. Madrid, being the capital, is home to many large diagnostic laboratories, research institutions, and hospitals that provide a wide range of medical testing services. Barcelona follows with its strong presence in medical research and development, including diagnostic labs that cater to both national and international patients. Valencia also plays a vital role, with multiple diagnostic centers expanding their services and increasing their patient base due to a growing demand for specialized healthcare.

Market Segmentation

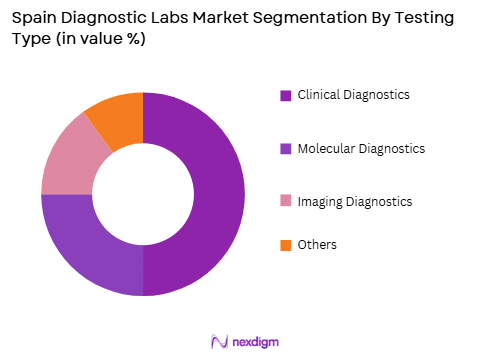

By Testing Type

The Spain diagnostic labs market is segmented by testing type into clinical diagnostics, molecular diagnostics, imaging diagnostics, and others. Recently, clinical diagnostics have dominated the market share due to their broad application in healthcare settings, ranging from routine blood tests to more complex diagnostics like pathology. The rise in chronic diseases, especially cardiovascular diseases, diabetes, and cancer, has driven the demand for clinical diagnostic services. Additionally, advancements in diagnostic technologies, such as automated blood analysis and point-of-care testing, have further fueled the growth of clinical diagnostics in Spain.

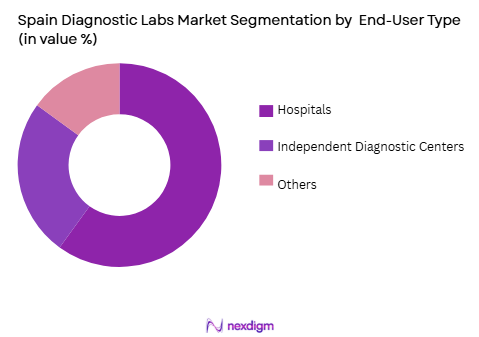

By End-User

The Spain diagnostic labs market is segmented by end-user into hospitals, independent diagnostic centers, and others. Recently, hospitals have dominated the market share due to their central role in providing diagnostic services across multiple specialties. Hospitals in Spain have integrated advanced diagnostic labs, such as imaging systems, molecular diagnostics, and pathology departments, into their routine operations to meet the increasing demand for disease detection. The increasing emphasis on early disease diagnosis, the rise in chronic disease incidences, and government investments in healthcare infrastructure further contribute to the dominance of hospitals in the diagnostic labs market.

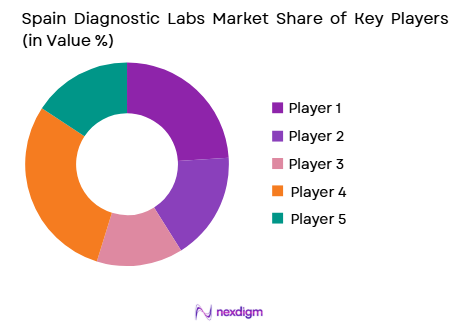

Competitive Landscape

The competitive landscape of Spain’s diagnostic labs market is characterized by a mix of local players and international companies. Large diagnostic lab chains are consolidating their market position through acquisitions and partnerships with healthcare providers. The focus is on providing a wide range of diagnostic services, improving test accuracy, and adopting cutting-edge technologies such as molecular diagnostics and AI-based imaging. Major players are competing to expand their market share by offering advanced, cost-effective testing solutions and improving accessibility in both urban and rural areas.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Grupo Quirónsalud | 1999 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| Labcorp | 1969 | Burlington, USA | ~ | ~ | ~ | ~ | ~ |

| B. Braun Melsungen | 1839 | Melsungen, Germany | ~ | ~ | ~ | ~ | ~ |

| Echevarne | 1985 | Barcelona, Spain | ~ | ~ | ~ | ~ | ~ |

| Synlab | 1966 | Barcelona, Spain | ~ | ~ | ~ | ~ | ~ |

Spain Diagnostic Labs Market Analysis

Growth Drivers

Increase in Chronic Diseases

One of the primary growth drivers for Spain’s diagnostic labs market is the increasing prevalence of chronic diseases such as cardiovascular diseases, diabetes, and cancer. These conditions require regular monitoring and early detection, which drives the demand for diagnostic testing services. As Spain’s population ages, the incidence of chronic diseases continues to rise, further escalating the need for efficient and accurate diagnostic services. The growing awareness among patients and healthcare providers about the importance of early diagnosis is propelling the adoption of diagnostic tests. This trend is expected to continue, contributing to sustained demand for diagnostic services across the country. Additionally, Spain’s healthcare system is increasingly focused on preventive care, and diagnostic labs play a critical role in this shift, ensuring that conditions are identified before they progress.

Government Healthcare Initiatives

Another key growth driver is the Spanish government’s support for healthcare initiatives, particularly those aimed at improving healthcare infrastructure and accessibility. Spain has made significant investments in expanding its healthcare facilities, including diagnostic labs, to meet the rising demand for medical services. Public-private partnerships have further facilitated the development of diagnostic centers and testing facilities, especially in underserved regions. The Spanish government has also been increasing funding for the adoption of digital health solutions, including diagnostic technology, to improve healthcare delivery. These initiatives have made diagnostic services more accessible to the population, driving growth in the diagnostic labs market. As healthcare policies continue to evolve, there will be ongoing support for diagnostic labs, boosting market expansion.

Market Challenges

Regulatory Compliance and Standardization

One of the key challenges in Spain’s diagnostic labs market is the need to comply with stringent regulatory standards and ensure the standardization of diagnostic procedures. Spain’s healthcare system follows strict regulations regarding the approval, certification, and operation of diagnostic labs to ensure patient safety and test accuracy. However, maintaining compliance with these standards can be time-consuming and costly for smaller diagnostic centers, limiting their ability to expand or modernize. Additionally, regulatory differences between Spain’s autonomous communities can create inconsistencies in the operation of diagnostic labs, leading to inefficiencies and challenges for both service providers and patients. The complexity of the regulatory landscape poses a significant barrier to the smooth functioning and expansion of the diagnostic labs market.

High Operational Costs

The high operational costs associated with running diagnostic labs is another challenge faced by the market. Diagnostic labs require significant investment in advanced equipment, technology, and highly trained personnel. The cost of acquiring and maintaining diagnostic tools, such as imaging systems, molecular diagnostic machines, and laboratory instruments, can be prohibitively high, especially for smaller facilities. Furthermore, diagnostic labs must invest in research and development to stay competitive and offer the latest diagnostic technologies. These high operational costs often lead to higher prices for diagnostic services, making it more difficult for patients in lower-income brackets to access essential tests. In addition, the reimbursement rates for diagnostic services may not always cover the full cost of the tests, putting pressure on diagnostic labs to operate efficiently while maintaining quality standards.

Opportunities

Integration of AI and Automation in Diagnostics

The integration of artificial intelligence (AI) and automation into diagnostic procedures presents a significant opportunity for Spain’s diagnostic labs market. AI-powered diagnostic tools, such as image recognition software, have the potential to greatly improve the accuracy and speed of diagnoses, especially in imaging diagnostics like radiology and pathology. Automation in diagnostic labs can also streamline processes, reduce human error, and increase operational efficiency. The growing interest in AI-driven diagnostic solutions, particularly for detecting diseases such as cancer, cardiovascular conditions, and neurological disorders, offers a unique opportunity for diagnostic labs to enhance their services. By adopting these technologies, diagnostic labs can provide faster results and improve patient outcomes, creating a competitive advantage in the market.

Growing Demand for Preventive Healthcare

The growing focus on preventive healthcare presents an opportunity for diagnostic labs to expand their services. Preventive care, including early disease detection through regular diagnostic tests, is becoming increasingly popular among the Spanish population. The shift toward preventive care is driven by rising health awareness, an aging population, and the increasing prevalence of lifestyle diseases. As patients seek to identify potential health risks early on, there is a growing demand for routine diagnostic tests, including blood tests, screenings, and imaging. Diagnostic labs that offer comprehensive preventive healthcare services, such as wellness check-ups and early-stage disease screenings, will be well-positioned to tap into this growing demand, driving market growth in the coming years.

Future Outlook

The future outlook for Spain’s diagnostic labs market is highly positive, with continued growth expected in the next five years. The demand for diagnostic testing services will be driven by the increasing prevalence of chronic diseases, the aging population, and the growing focus on preventive healthcare. Technological advancements, particularly in AI, automation, and molecular diagnostics, will further enhance the capabilities of diagnostic labs, improving patient outcomes and operational efficiency. The Spanish government’s ongoing support for healthcare infrastructure and its emphasis on digitizing the healthcare system will also contribute to the market’s expansion. As the market continues to evolve, diagnostic labs that embrace innovation and improve accessibility will be key players in Spain’s healthcare sector.

Major Players

- Grupo Quirónsalud

- Labcorp

- B. Braun Melsungen

- Echevarne

- Synlab

- Roche Diagnostics

- Siemens Healthineers

- Abbott Laboratories

- Thermo Fisher Scientific

- GE Healthcare

- BioMérieux

- Illumina

- Quest Diagnostics

- RIMSA

- Laboratorio Dr. Esteve

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Hospitals and clinics

- Pharmaceutical companies

- Medical device manufacturers

- Insurance providers

- Medical research organizations

Research Methodology

Step 1: Identification of Key Variables

Key variables such as market size, growth drivers, challenges, and technological trends are identified through primary and secondary research.

Step 2: Market Analysis and Construction

Comprehensive data is collected and analyzed using statistical models to build accurate market forecasts.

Step 3: Hypothesis Validation and Expert Consultation

Insights and assumptions are validated through consultations with industry experts to ensure the accuracy of the findings.

Step 4: Research Synthesis and Final Output

The final report synthesizes all data, providing a comprehensive analysis of Spain’s diagnostic labs market, including growth drivers, challenges, and opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increasing Incidences of Chronic Diseases

Technological Advancements in Diagnostic Equipment

Growing Healthcare Investments by Government - Market Challenges

High Operational and Maintenance Costs

Regulatory Compliance and Certification Challenges

Lack of Skilled Technicians - Market Opportunities

Expansion of Point-of-Care Diagnostics

Rise in Demand for Personalized Diagnostics

Technological Advancements in Genetic Testing - Trends

Integration of AI and Machine Learning in Diagnostics

Shift Towards Minimally Invasive Diagnostic Methods - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Labs

Pathology Labs

Genetic Testing Labs

Microbiology Labs

Immunoassay Labs - By Platform Type (In Value%)

Automated Diagnostic Platforms

Manual Diagnostic Platforms

Hybrid Diagnostic Platforms

Cloud-based Diagnostic Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Integrated Solutions - By End User Segment (In Value%)

Hospitals

Private Diagnostic Centers

Public Healthcare Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technological Integration, Market Penetration, Regulatory Compliance, Data Security, Service Availability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Laboratorios Clínicos Valdés

Laboratorio Dr. Bédard

Laboratorios Reig Jofré

Grupo Echevarne

Laboratorio Laba

Eurofins

Laboratorio Clínico López

Laboratorio Biolab

Centros de Diagnóstico Borrás

Laboratorios Ochoa

Laboratorios Aragó

Grupo Envera

Laboratorios de Salud

Laboratorio Antón

Laboratorio Sanitas

- Hospitals Increasing Diagnostic Services

- Private Diagnostic Centers Adopting Advanced Technologies

- Public Healthcare Expanding Diagnostic Access

- Research Institutions Fostering Innovation in Diagnostics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now