Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Spain digital health market is valued at approximately USD ~ billion based on a recent historical assessment. This growth is driven by the increasing adoption of digital technologies in healthcare, including electronic health records (EHR), telemedicine, and AI-powered diagnostic tools. Additionally, the Spanish government’s investment in digital health infrastructure and its push for e-health solutions across both public and private sectors have significantly contributed to the market’s expansion.

Madrid, Barcelona, and Valencia are the dominant cities in Spain’s digital health market due to their advanced healthcare infrastructure and high concentration of tech-enabled health services. Madrid leads in terms of healthcare innovation and is home to several major healthcare providers that are integrating digital technologies into their operations. Barcelona, with its growing healthtech startup ecosystem, also plays a significant role in driving digital health adoption. These cities benefit from strong technological capabilities and access to a broad base of healthcare professionals, making them ideal hubs for the growth of the digital health market.

Market Segmentation

By Technology Type

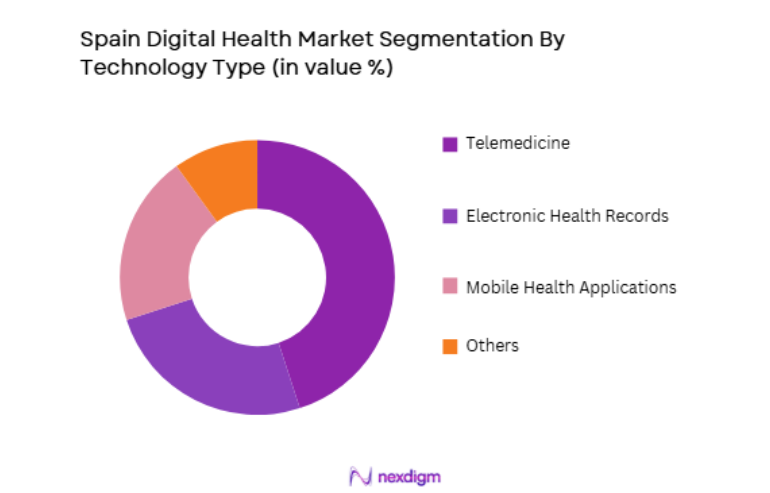

Spain’s digital health market is segmented by technology type into telemedicine, electronic health records (EHR), mobile health applications, and others. Recently, telemedicine has dominated the market share due to its increased adoption in response to the COVID-19 pandemic. The demand for remote healthcare services, particularly video consultations and virtual care, surged as the healthcare system adapted to social distancing measures. Telemedicine has proven to be an effective solution for providing healthcare services in rural areas and reducing the burden on in-person clinics. The growing need for accessible and affordable healthcare solutions has further driven the adoption of telemedicine, making it a dominant segment in Spain’s digital health market.

By End-User

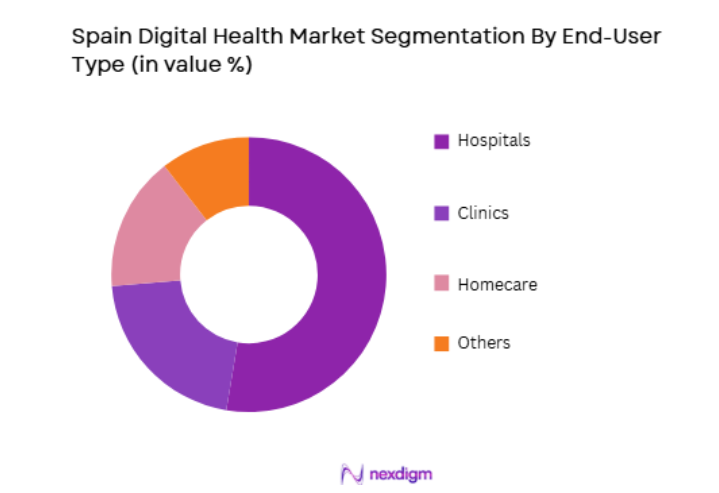

Spain’s digital health market is segmented by end-user into hospitals, clinics, homecare, and others. Recently, hospitals have dominated the market share due to their central role in delivering healthcare services and adopting digital health solutions. The integration of EHR systems, telemedicine platforms, and diagnostic tools in hospitals has helped improve patient care and streamline operations. Hospitals are increasingly using digital health technologies to reduce waiting times, improve treatment outcomes, and offer more personalized care. Additionally, public and private hospitals in Spain are rapidly embracing digital health to align with government health policies that encourage the use of e-health solutions, thereby contributing to the market’s growth.

Competitive Landscape

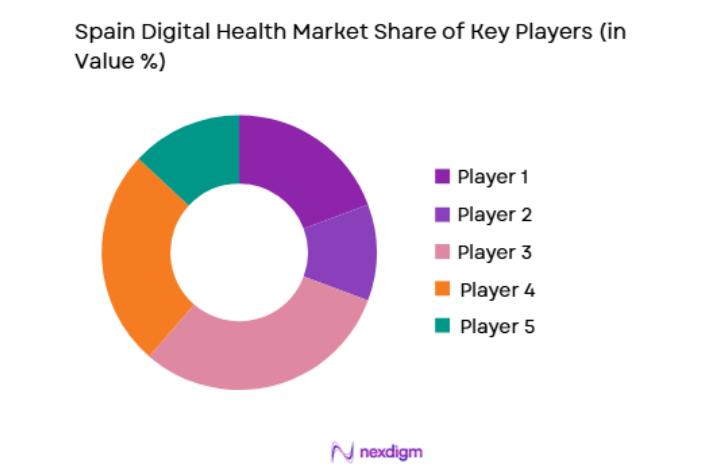

The competitive landscape of Spain’s digital health market is characterized by a mix of large multinational companies and local startups that are introducing innovative solutions. The market is consolidating, with several mergers and acquisitions taking place as larger players acquire smaller tech firms to expand their portfolios and geographic reach. Both public and private healthcare providers are adopting digital health technologies to improve efficiency and reduce costs. Major players are increasingly focusing on developing AI-powered healthcare solutions and expanding telemedicine services to meet the growing demand for digital health services.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Philips Healthcare | 1891 | Amsterdam, Netherlands | ~ | ~ | ~ | ~ | ~ |

| Cerner Corporation | 1979 | Kansas City, USA | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Dublin, Ireland | ~ | ~ | ~ | ~ | ~ |

| DKV Seguros | 1999 | Zaragoza, Spain | ~ | ~ | ~ | ~ | ~ |

| MIB Health | 2015 | Barcelona, Spain | ~ | ~ | ~ | ~ | ~ |

Spain Digital Health Market Analysis

Growth Drivers

Government Support for Digital Health

One of the key growth drivers for Spain’s digital health market is the strong government support for digital health initiatives. The Spanish government has prioritized the digitization of its healthcare system, launching several e-health programs that aim to improve patient care, reduce costs, and streamline healthcare delivery. Initiatives such as the National Health System (SNS) have paved the way for the widespread adoption of digital health technologies like electronic health records (EHR), telemedicine platforms, and mobile health applications. The Spanish government has also allocated funding to support digital health infrastructure, making it easier for healthcare providers to implement advanced technological solutions. This support has created a favorable environment for both local and international companies to develop and deploy digital health solutions in Spain, driving market growth.

Increasing Demand for Accessible Healthcare

The increasing demand for accessible healthcare is another major growth driver for Spain’s digital health market. Spain, like many other countries, is experiencing an aging population, which is leading to an increased demand for healthcare services. As the elderly population grows, there is a greater need for healthcare solutions that offer convenience and accessibility. Digital health technologies, particularly telemedicine, have become essential tools for providing healthcare services to patients who have limited access to healthcare facilities, especially in rural areas. Telemedicine platforms allow patients to consult with healthcare professionals remotely, reducing the need for in-person visits and making healthcare more accessible. Additionally, the COVID-19 pandemic accelerated the adoption of digital health technologies, as patients and healthcare providers alike turned to virtual care to avoid exposure to the virus. The continued demand for accessible healthcare solutions will drive further growth in Spain’s digital health market.

Market Challenges

Privacy and Data Security Concerns

One of the key challenges facing Spain’s digital health market is the issue of privacy and data security. With the increasing adoption of digital health solutions, large amounts of sensitive patient data are being stored and transmitted electronically. Ensuring the security of this data is a critical concern, as healthcare organizations must comply with strict data protection regulations such as the General Data Protection Regulation (GDPR). While Spain has made significant strides in implementing data privacy laws, the growing use of telemedicine, EHR, and mobile health applications increases the risk of data breaches and cyberattacks. Healthcare providers must invest in secure digital infrastructure to protect patient information from unauthorized access and maintain trust in digital health solutions. The complexity of managing data privacy and security risks presents a challenge for healthcare organizations and digital health providers in Spain.

High Initial Investment Costs

The high initial investment required for implementing digital health technologies is another challenge in Spain’s healthcare market. While digital health solutions offer long-term cost savings and efficiency improvements, the upfront costs for acquiring and integrating these technologies can be prohibitive for smaller healthcare providers, particularly in rural areas. Telemedicine platforms, EHR systems, and mobile health applications require substantial investment in technology infrastructure, training, and ongoing maintenance. Smaller clinics and independent healthcare providers may struggle to afford these initial investments, limiting their ability to adopt digital health solutions. Additionally, public healthcare institutions, which often operate under budget constraints, may find it difficult to secure the necessary funding to implement these technologies. Addressing this challenge will require financial support from the government or private sector, as well as cost-effective solutions that cater to smaller healthcare providers.

Opportunities

Expansion of Telemedicine Services

The expansion of telemedicine services presents a significant opportunity for Spain’s digital health market. Telemedicine has gained significant traction in Spain, especially during the COVID-19 pandemic, as patients and healthcare providers embraced remote consultations to reduce the risk of exposure to the virus. As the demand for telehealth services continues to rise, there are ample opportunities for digital health companies to expand their offerings, particularly in underserved and rural areas. Telemedicine platforms allow patients to access healthcare professionals without the need to travel, improving healthcare accessibility for patients with limited mobility or those living in remote areas. The Spanish government’s ongoing support for telemedicine, coupled with the growing acceptance of remote healthcare services, is expected to drive the continued expansion of telemedicine services in Spain, creating opportunities for companies in the digital health space.

Growth in Mobile Health Applications

The growth of mobile health applications is another promising opportunity for Spain’s digital health market. With the increasing penetration of smartphones and internet connectivity, mobile health apps have become a convenient way for patients to monitor their health, access medical information, and receive virtual consultations. These apps offer services such as fitness tracking, medication reminders, mental health support, and chronic disease management. The demand for mobile health apps is expected to rise as more patients seek personalized healthcare solutions that are accessible anytime and anywhere. Additionally, mobile health apps are increasingly being integrated with telemedicine platforms and EHR systems, enhancing the overall patient experience and improving healthcare outcomes. The growing interest in mobile health solutions presents a significant opportunity for digital health companies to expand their market presence and offer innovative solutions.

Future Outlook

The future outlook for Spain’s digital health market is highly positive, with continued growth expected over the next five years. Government support for digital health initiatives, the expansion of telemedicine services, and the increasing demand for mobile health applications will drive market expansion. Technological advancements, such as AI-driven diagnostics and telemedicine platforms, will continue to enhance the quality and accessibility of healthcare services in Spain. Additionally, the integration of digital health solutions into public and private healthcare systems will further facilitate the adoption of these technologies, creating new growth opportunities for market players. With a strong focus on improving healthcare delivery and patient outcomes, Spain is poised to remain a leader in the digital health market in Europe.

Major Players

- Philips Healthcare

- Cerner Corporation

- Medtronic

- Siemens Healthineers

- GE Healthcare

- DKV Seguros

- Sanitas

- Fresenius Medical Care

- Baxter International

- Roche Diagnostics

- MIB Health

- Ferring Pharmaceuticals

- iSalud

- Vithas

- Teladoc Health

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Hospitals and clinics

- Pharmaceutical companies

- Medical device manufacturers

- Insurance providers

- Medical research organizations

Research Methodology

Step 1: Identification of Key Variables

Key variables such as market size, growth drivers, and technological trends are identified through both primary and secondary research methods.

Step 2: Market Analysis and Construction

Comprehensive market data is collected, analyzed, and synthesized using statistical models to construct accurate market forecasts.

Step 3: Hypothesis Validation and Expert Consultation

Insights and assumptions are validated through consultations with industry experts to ensure the accuracy of the findings.

Step 4: Research Synthesis and Final Output

The final report synthesizes all collected data, providing a detailed analysis of Spain’s digital health market, including growth drivers, challenges, and opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Investments in Healthcare Digitalization

Technological Advancements in Mobile Health

Growing Healthcare Infrastructure - Market Challenges

Data Security and Privacy Concerns

Regulatory Compliance Barriers

Limited Access to Digital Health Services in Rural Areas - Market Opportunities

Growth in Telemedicine Adoption

Increasing Demand for Wearable Health Devices

Expanding Remote Monitoring Solutions - Trends

Integration of AI in Healthcare

Shift Towards Preventive Healthcare with Digital Tools - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Telemedicine Solutions

EHR and EMR Systems

Health Information Systems

Wearable Health Devices

Remote Patient Monitoring Systems - By Platform Type (In Value%)

Cloud-Based Platforms

On-Premise Solutions

Mobile Platforms

Web Platforms - By Fitment Type (In Value%)

Integrated Solutions

Cloud Solutions

Modular Solutions

Standalone Solutions - By End User Segment (In Value%)

Hospitals

Clinics

Government Healthcare Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technological Integration, Market Penetration, Regulatory Compliance, Service Quality, Cost Efficiency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Teladoc Health

Amwell

Cerner Corporation

Philips Healthcare

Medtronic

GE Healthcare

IBM Watson Health

Allscripts

Accenture

HealthTap

Doctor On Demand

Siemens Healthineers

Doctor Anywhere

Maple

Lifecare

- Hospitals Expanding Digital Health Services

- Clinics Adopting Telemedicine Solutions

- Government Bodies Promoting Healthcare IT Adoption

- Increasing Healthcare Needs in Rural Areas

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now