Download PDF

Download PDFMarket Overview

Spain edge computing market is valued at approximately USD ~ billion based on a recent historical assessment, driven by nationwide 5G rollout, industrial IoT deployment, and growing enterprise demand for low latency computing. Telecom operators and cloud providers are expanding distributed data infrastructure to support real time analytics, AI inference, and connected devices. Public digitalization programs and manufacturing automation investments are accelerating adoption of localized processing architecture across sectors requiring secure and deterministic data handling.

Madrid and Barcelona dominate Spain edge computing market due to dense telecom infrastructure, hyperscale connectivity nodes, and concentration of technology enterprises and data centers. These cities host major carrier neutral facilities, innovation hubs, and smart mobility deployments that require edge processing. Industrial regions such as Basque Country and Catalonia also contribute through advanced manufacturing and logistics digitization initiatives, supported by regional digital transformation funding and strong presence of telecom operators and system integrators enabling localized computing ecosystems.

Market Segmentation

By Product Type

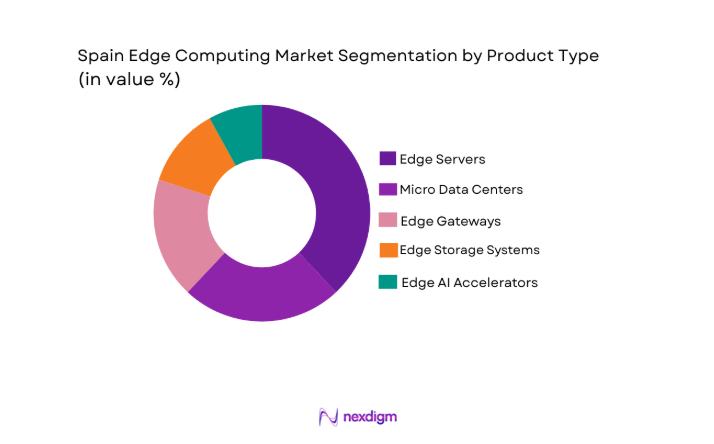

Spain edge computing market is segmented by product type into edge servers, micro data centers, edge gateways, edge storage systems, and edge AI accelerators. Recently, edge servers has a dominant market share due to factors such as enterprise compute demand, telecom deployment scale, infrastructure availability, and preference for scalable localized processing platforms. Telecom operators and enterprises prioritize edge servers because they integrate virtualization, AI inference capability, and multi workload processing within compact footprints, enabling rapid deployment across 5G sites, industrial facilities, and urban infrastructure nodes while maintaining interoperability with centralized cloud environments.

By Platform Type

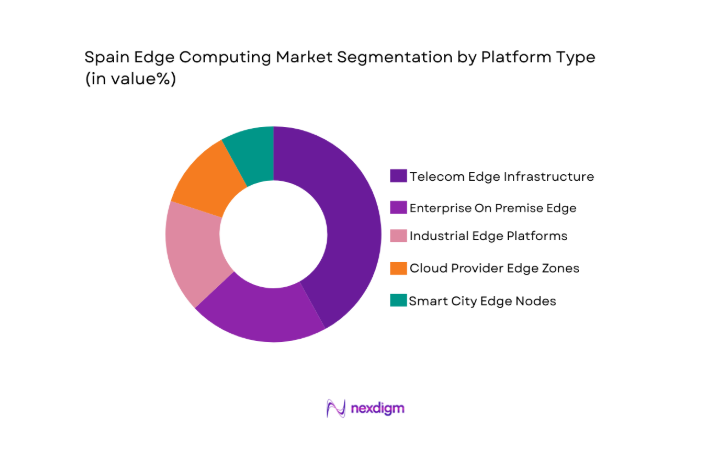

Spain edge computing market is segmented by platform type into telecom edge infrastructure, enterprise on premise edge, industrial edge platforms, cloud provider edge zones, and smart city edge nodes. Recently, telecom edge infrastructure has a dominant market share due to factors such as nationwide 5G network expansion, carrier investment capacity, infrastructure ownership, and demand for low latency services. Telecom operators control distributed network locations, fiber backhaul, and tower assets, enabling rapid deployment of multi access edge computing nodes that support consumer applications, enterprise connectivity services, and content delivery workloads at scale across metropolitan and regional coverage zones.

Competitive Landscape

Spain edge computing market shows moderate consolidation led by telecom operators, global IT infrastructure vendors, and domestic digital engineering firms. Major carriers leverage network ownership to deploy multi access edge platforms, while global hardware providers supply compute systems and software stacks. Domestic integrators and industrial technology firms enable sector specific deployments across manufacturing, utilities, and transport. Partnerships between cloud providers and telecom operators are strengthening ecosystem integration and accelerating commercialization of distributed computing services.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Model |

| Telefonica | 1924 | Madrid Spain | ~ | ~ | ~ | ~ | ~ |

| Vodafone Spain | 2001 | Madrid Spain | ~ | ~ | ~ | ~ | ~ |

| Orange Spain | 2006 | Madrid Spain | ~ | ~ | ~ | ~ | ~ |

| Indra Sistemas | 1993 | Madrid Spain | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 2015 | Texas USA | ~ | ~ | ~ | ~ | ~ |

Spain Edge Computing Market Analysis

Growth Drivers

Nationwide 5G Infrastructure Expansion and Multi Access Edge Computing Integration

Spain edge computing market growth is strongly driven by rapid nationwide deployment of fifth generation mobile networks combined with integration of multi access edge computing architecture into telecom infrastructure, enabling ultra low latency processing and localized service delivery across urban and industrial environments. Telecom operators are densifying base station networks and embedding compute nodes within radio access sites to support emerging applications such as autonomous mobility, immersive media, and real time analytics that require deterministic network performance and proximity processing. Government digital connectivity initiatives and spectrum allocation policies are encouraging carrier investment in distributed infrastructure, accelerating commercialization of edge enabled services for enterprises and public sector entities. Industrial sectors including manufacturing, logistics, and energy are adopting private 5G networks connected to edge computing platforms to enable machine automation, robotics coordination, and predictive maintenance systems that depend on real time data processing and minimal latency communication. Hyperscale cloud providers are partnering with telecom operators to extend cloud services to edge locations, allowing enterprises to deploy applications closer to users while maintaining hybrid cloud integration and orchestration consistency. Content delivery, gaming, and video streaming providers are leveraging telecom edge nodes to optimize user experience and reduce network congestion, further increasing demand for localized compute infrastructure. Smart city programs across major Spanish municipalities are integrating edge computing into traffic management, surveillance, and environmental monitoring systems, expanding distributed processing footprints across public infrastructure. As network coverage expands to suburban and regional areas, telecom edge platforms are becoming foundational digital infrastructure supporting new services ecosystems across Spain.

Industrial Digitalization and Real Time Data Processing Requirements Across Manufacturing and Utilities

Spain edge computing market is also expanding due to accelerating industrial digitalization initiatives that require real time data processing, localized analytics, and secure operational technology integration within manufacturing plants, energy facilities, and logistics operations. Advanced manufacturing clusters in regions such as Catalonia and Basque Country are deploying edge platforms to support robotics coordination, machine vision inspection, and digital twin simulation, enabling production optimization and predictive maintenance without dependence on centralized cloud latency. Utilities and energy companies are integrating edge computing into smart grid infrastructure and renewable energy management systems to process sensor data locally and ensure operational resilience across distributed generation assets. Transportation and logistics operators are implementing edge based fleet monitoring, route optimization, and autonomous vehicle coordination systems that depend on continuous low latency computation near operational environments. Industrial cybersecurity frameworks are increasingly relying on localized processing to detect anomalies and secure operational networks, driving demand for on site edge compute nodes with specialized analytics capabilities. Enterprises prioritize edge deployments to maintain data sovereignty and regulatory compliance, particularly for sensitive industrial and infrastructure data that cannot be transmitted to centralized cloud environments. Integration of artificial intelligence inference accelerators within edge hardware is enabling automated decision making at the operational layer, reducing downtime and enhancing productivity across industrial processes. Spain’s national Industry 4.0 strategies and regional digital transformation funding are incentivizing deployment of localized computing infrastructure, reinforcing edge computing adoption across industrial sectors.

Market Challenges

High Capital Expenditure and Operational Complexity of Distributed Edge Infrastructure Deployment

Spain edge computing market faces significant barriers due to high capital investment requirements associated with deploying distributed computing nodes across telecom sites, industrial facilities, and urban infrastructure environments, combined with operational complexity of managing geographically dispersed hardware and software systems. Edge deployments require ruggedized equipment, power and cooling integration, secure connectivity, and physical site preparation, increasing upfront costs compared to centralized data center infrastructure. Telecom operators and enterprises must integrate edge platforms with existing network and IT architectures, often involving complex orchestration, virtualization, and security frameworks that demand specialized expertise and increase implementation timelines. Maintenance and lifecycle management of distributed nodes across remote or outdoor locations introduces operational challenges including hardware failure risk, environmental exposure, and limited on site technical support availability. Economies of scale are difficult to achieve during early deployment phases due to fragmented demand across sectors and regions, slowing return on investment realization for infrastructure providers. Interoperability issues between vendor hardware, network equipment, and cloud software platforms create integration risks and vendor lock in concerns for adopters. Skilled workforce shortages in edge computing architecture, network virtualization, and industrial integration further constrain deployment capacity across Spain. Enterprises often struggle to justify investment without clear monetization models or application demand visibility, limiting adoption beyond pilot stages. These financial and operational barriers continue to moderate pace of edge computing expansion despite strong technological drivers.

Data Governance, Security, and Interoperability Constraints in Multi Vendor Edge Ecosystems

Spain edge computing market also encounters challenges related to data governance complexity, cybersecurity risks, and interoperability limitations across heterogeneous multi vendor edge ecosystems spanning telecom networks, enterprise systems, and industrial operational technology environments. Distributed processing architectures expand attack surfaces and introduce new cybersecurity vulnerabilities, requiring robust encryption, authentication, and monitoring frameworks that increase deployment complexity and cost. Regulatory compliance obligations related to data protection and critical infrastructure security necessitate localized data handling policies and stringent access controls, complicating cross platform integration and cloud connectivity. Enterprises deploying edge solutions must manage data ownership, sovereignty, and lifecycle governance across multiple locations and stakeholders, creating operational and legal complexities. Lack of standardized edge computing architectures and open interoperability frameworks results in fragmented solutions that hinder scalability and ecosystem collaboration across vendors and service providers. Integration of legacy industrial systems with modern edge platforms requires custom engineering and protocol translation, increasing implementation risk and limiting adoption speed in traditional sectors. Telecom and cloud provider partnerships involve coordination of network, compute, and service layers, often complicated by differing technology stacks and commercial models. End users may hesitate to deploy mission critical workloads on edge infrastructure without proven reliability and security assurances. These governance and interoperability constraints remain key structural barriers affecting Spain edge computing market maturity.

Opportunities

Integration of Edge Artificial Intelligence and Autonomous Systems Across Industrial and Urban Infrastructure

Spain edge computing market presents substantial opportunity through integration of artificial intelligence processing capabilities within distributed edge infrastructure to support autonomous systems, real time analytics, and intelligent automation across industrial facilities and urban environments. Embedding AI accelerators in edge servers enables local inference for machine vision, anomaly detection, and predictive maintenance applications without reliance on centralized cloud connectivity, improving responsiveness and operational resilience. Smart transportation systems including connected traffic management and autonomous mobility coordination require localized data processing to enable rapid decision making and safety assurance. Industrial robotics and automated production lines benefit from edge AI platforms capable of real time object recognition and adaptive control within factory environments. Energy and utility networks can deploy edge intelligence to manage distributed renewable generation and grid stability through localized analytics. Public safety and surveillance systems across municipalities are increasingly adopting AI enabled edge processing for video analytics and situational awareness. Telecom operators and infrastructure providers can monetize edge AI services for enterprise customers seeking intelligent automation capabilities. As AI hardware efficiency improves and software frameworks mature, Spain edge computing deployments incorporating AI inference are expected to expand rapidly across sectors.

Expansion of Edge Cloud Service Models Through Telecom and Hyperscale Partnerships

Spain edge computing market opportunity is further strengthened by emerging service models combining telecom network edge infrastructure with hyperscale cloud platforms to deliver distributed cloud capabilities closer to end users and enterprises. Telecom operators possess geographically distributed network sites and connectivity assets, while cloud providers offer scalable computing platforms and developer ecosystems, enabling collaborative edge cloud architectures that extend cloud services to local environments. Enterprises can deploy latency sensitive applications such as augmented reality, industrial automation, and real time analytics on telecom edge nodes while maintaining integration with centralized cloud management and data storage. Content delivery networks, gaming platforms, and immersive media providers require localized processing to enhance user experience, creating new revenue streams for edge cloud providers. Government and public sector digital services including smart city infrastructure and emergency response systems benefit from resilient localized cloud capabilities hosted within national telecom networks. Hybrid cloud strategies across enterprises increasingly demand edge integration to support distributed operations and data sovereignty compliance. Telecom hyperscale alliances can accelerate commercialization by providing standardized platforms and marketplaces for edge applications. As these partnerships mature, Spain edge computing ecosystem is expected to evolve toward scalable edge cloud service markets.

Future Outlook

Spain edge computing market is expected to expand steadily over the next five years driven by continued 5G densification, industrial digitalization, and smart infrastructure deployment. Edge artificial intelligence integration and telecom cloud convergence will accelerate distributed computing adoption across enterprises and public sector. Regulatory support for digital infrastructure and data sovereignty will reinforce localized processing architectures. Demand for low latency applications across mobility, manufacturing, and utilities will sustain infrastructure investment. Ecosystem partnerships between telecom operators, cloud providers, and integrators will shape competitive dynamics.

Major Players

- Telefonica

- Vodafone Spain

- Orange Spain

- Indra Sistemas

- GMV

- Amper

- Fujitsu Spain

- Hewlett Packard Enterprise

- Dell Technologies

- Cisco Systems

- Nokia • Ericsson

- Schneider Electric

- Siemens

- Equinix

Key Target Audience

- Telecom operators

- Cloud service providers

- Industrial automation companies

- Smart city authorities

- Energy and utilities companies

- Transportation and logistics firms

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Core variables including infrastructure deployment scale, telecom network density, industrial adoption levels, and enterprise digitalization indicators were defined. Data sources included telecom statistics, infrastructure investments, and technology adoption metrics. Market boundaries and segmentation structures were established.

Step 2: Market Analysis and Construction

Supply and demand side data were integrated to construct market size and segmentation models. Company revenues, infrastructure deployments, and technology adoption indicators were triangulated. Regional and sectoral distribution patterns were analyzed.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultation with industry experts, telecom engineers, and enterprise IT stakeholders. Technology adoption drivers and barriers were reviewed. Assumptions were refined based on expert insights and secondary validation.

Step 4: Research Synthesis and Final Output

Validated data and analysis were synthesized into structured market insights and forecasts. Competitive landscape and segmentation were finalized. Findings were reviewed for consistency, accuracy, and analytical coherence before publication.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

5G network densification and low latency service demand

Industrial automation and real time analytics adoption

Smart city and connected infrastructure programs - Market Challenges

High deployment and maintenance costs at distributed sites

Interoperability issues across multi vendor edge ecosystems

Data sovereignty and regulatory compliance complexity - Market Opportunities

Expansion of edge enabled AI inference services

Growth of private 5G and industrial edge convergence

Edge cloud partnerships with hyperscale providers - Trends

Rise of telecom operator edge cloud platforms

Integration of AI accelerators in edge hardware

Adoption of modular micro data center architectures

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025 .

- By System Type (In Value%)

Edge Servers

Micro Data Centers

Edge Gateways

Edge Storage Systems

Edge AI Accelerators - By Platform Type (In Value%)

Telecom Edge Infrastructure

Enterprise OnPremise Edge

Industrial Edge Platforms

Cloud Provider Edge Zones

Smart City Edge Nodes - By Fitment Type (In Value%)

Standalone Edge Deployments

Integrated EdgeCloud Systems

Ruggedized Edge Installations

Modular Edge Units

Embedded Edge Systems - By EndUser Segment (In Value%)

Telecom Operators

Manufacturing Enterprises

Transportation and Logistics Providers

Energy and Utilities Companies

Public Sector and Smart Cities - By Procurement Channel (In Value%)

Direct OEM Procurement

Telecom Vendor Contracts

System Integrator Partnerships

Cloud Marketplace Procurement

Government and Public Tenders

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Deployment Model, Latency Capability, Compute Density, AI Acceleration Support, Industry Solutions Portfolio, Geographic Presence, Integration Capability, Pricing Model, Service Support)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Telefonica

Vodafone Spain

Orange Spain

Indra Sistemas

GMV

Amper

Fujitsu Spain

Hewlett Packard Enterprise

Dell Technologies

Cisco Systems

Nokia

Ericsson

Schneider Electric

Siemens

Equinix

- Telecom operators expanding multi access edge computing footprints

- Manufacturers deploying edge for predictive maintenance and robotics

- Transport and logistics firms using edge for fleet and traffic analytics

- Public sector adopting edge for surveillance and smart infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now