Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Spain Green Hydrogen Market has experienced substantial growth, driven by the country’s commitment to decarbonizing its energy sector. With a market size valued at approximately USD ~ billion, Spain’s strategic focus on green hydrogen aligns with its broader renewable energy goals, which include reducing emissions and increasing the share of renewable energy in hydrogen production. Spain’s favorable renewable energy resources, particularly solar and wind, contribute to the country’s competitive advantage in producing green hydrogen. In response to the EU Green Deal, Spain has committed significant investments to develop the hydrogen infrastructure, estimated at over $8 billion by 2030, ensuring robust growth in the sector. This financial commitment, along with government policies that incentivize clean energy adoption, has accelerated the development of green hydrogen as a key element of Spain’s energy transition plan.

The dominant regions within Spain driving the green hydrogen market include Andalusia, Castilla-La Mancha, and Aragón. These areas benefit from abundant renewable energy resources and supportive local governments committed to hydrogen projects. The proximity to major European markets and Spain’s favorable regulatory environment make it an attractive destination for green hydrogen production. Spain’s role in the EU’s hydrogen roadmap and the increased emphasis on hydrogen for energy security, decarbonization, and industrial use further solidify the country’s position as a European leader in the green hydrogen market. As a result, Spain is well-positioned to leverage both domestic and international markets for green hydrogen, driving its continued growth and influence in the sector.

Market Segmentation

By Product Type

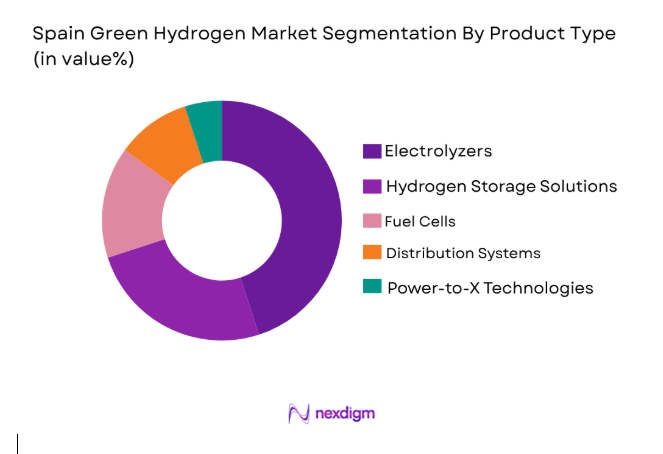

The Spain Green Hydrogen market is segmented by product type into electrolyzers, hydrogen storage solutions, fuel cells, distribution systems, and power-to-X technologies. Among these, the electrolyzer segment is the dominant market share leader due to its essential role in hydrogen production. This dominance can be attributed to the increased demand for efficient and scalable hydrogen production systems. As the production cost of electrolyzers continues to decrease and their efficiency improves, they are expected to remain the key driver of growth within the green hydrogen market. Technological advancements in electrolysis are contributing to cost competitiveness, making electrolyzers more accessible for large-scale commercial and industrial applications.

By Platform Type

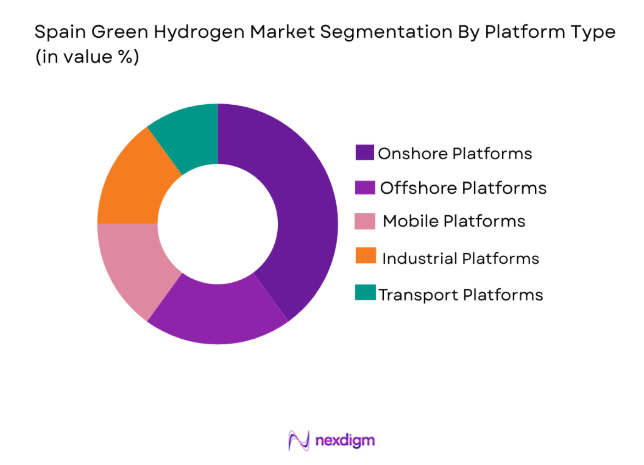

The Spain Green Hydrogen market is also segmented by platform type, which includes onshore platforms, offshore platforms, mobile platforms, industrial platforms, and transport platforms. The onshore platform segment currently dominates the market due to the extensive availability of renewable energy sources on land, such as solar and wind power. These platforms are the most cost-effective for large-scale hydrogen production due to proximity to energy sources and infrastructure. Additionally, the growing number of onshore renewable energy projects and government incentives have reinforced the demand for onshore hydrogen platforms, solidifying their leadership in the market.

Competitive Landscape

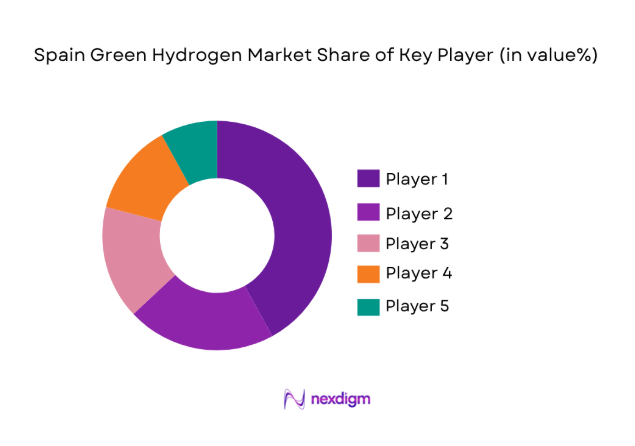

The competitive landscape of the Spain Green Hydrogen Market shows significant consolidation, with a mix of established energy companies, innovative startups, and research institutions. The influence of major players is expanding as they focus on building long-term strategies to integrate green hydrogen into their existing infrastructure and supply chains. The market is highly competitive, driven by government support, technological advancements, and the increasing need for decarbonization solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Strategic Partnerships |

| Iberdrola | 1992 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| Acciona | 2000 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| Enagas | 2002 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| Cepsa | 1939 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| Siemens Energy | 2008 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

Spain Green Hydrogen Market Analysis

Growth Drivers

Government Policy Support

Spain’s government has firmly committed to the decarbonization of its energy sector, with significant investments directed towards developing green hydrogen solutions. A key component of Spain’s national hydrogen roadmap is its focus on decarbonizing the transport, industrial, and power sectors through the increased use of green hydrogen. These policies align with the broader European Union Green Deal, which sets ambitious targets for carbon neutrality. As part of this commitment, Spain is dedicating a substantial portion of its renewable energy investments to hydrogen infrastructure, thus accelerating the country’s transition to clean energy. By promoting renewable hydrogen production, Spain aims to boost its energy security and reduce dependency on imported fossil fuels, which further strengthens its position in the green hydrogen market. With additional incentives and tax benefits offered to private companies, the market is attracting significant private sector investments aimed at scaling up hydrogen production. Spain’s continued alignment with EU policies further ensures sustained growth in the sector, opening new opportunities for innovation and long-term investments in green hydrogen technology. As the country becomes a global leader in green hydrogen, this government-led push promises to drive substantial growth, creating more opportunities for domestic and international players involved in the hydrogen value chain.

Technological Advancements

Significant advancements in electrolysis technology are accelerating the growth of Spain’s green hydrogen market. The development of more efficient electrolyzers, along with reduced costs, has made green hydrogen production more competitive against other renewable energy sources. Electrolysis, which is the process of using electricity to split water into hydrogen and oxygen, is now becoming more efficient, making it a cost-effective method of producing hydrogen. Research and development efforts are also driving improvements in hydrogen storage and fuel cell technologies, making them more efficient and easier to integrate with the national power grid. Spain, known for its innovation in renewable energy, is well-positioned to lead Europe in the green hydrogen market. Technological breakthroughs have lowered production costs, allowing Spain to scale up green hydrogen initiatives at a faster rate than previously expected. This technological momentum not only boosts the green hydrogen sector in Spain but also enhances its competitiveness within the European market. As electrolyzers become increasingly efficient and affordable, Spain can expand its capacity to produce green hydrogen at large scales, positioning itself as one of the most competitive markets in Europe. Furthermore, innovation in storage and fuel cell technologies supports green hydrogen’s integration into existing energy systems, reducing reliance on conventional fossil fuels.

Market Challenges

High Infrastructure Costs

The transition to green hydrogen faces substantial financial challenges, especially in the development of infrastructure. The integration of large-scale hydrogen production, transportation, and storage into Spain’s energy mix requires substantial investment in both public and private sectors. Hydrogen production plants, pipelines, refueling stations, and storage systems represent a massive cost to implement and maintain. The construction of hydrogen infrastructure, such as hydrogen refueling stations and pipelines across the country, requires capital that exceeds what is available through existing funding mechanisms. Although Spain’s government has committed billions to support hydrogen projects, including tax credits and other financial incentives, the costs involved in building a fully integrated hydrogen economy remain high. These substantial financial requirements are a major barrier, as they slow the market’s overall growth rate and hinder the widespread adoption of hydrogen technologies across Spain. The need for additional investments to build this infrastructure further complicates the development of green hydrogen, preventing faster scaling and delaying the widespread rollout of hydrogen-based solutions. Without significant private sector participation and public-private collaborations, the high infrastructure costs are expected to remain one of the key challenges to Spain’s green hydrogen ambitions.

Energy Efficiency Concerns

Despite the significant advancements in electrolyzer technology, one of the key challenges to green hydrogen adoption in Spain is the energy efficiency of the hydrogen production process. Electrolysis is still an energy-intensive process that requires a considerable amount of renewable energy, particularly from sources like wind and solar, to convert water into hydrogen. While renewable energy is abundant in Spain, the current conversion efficiency of electrolyzers remains relatively low, often operating at only 70-75% efficiency. This inefficiency means that more energy must be consumed to produce the same amount of hydrogen, making it less cost-competitive than other renewable solutions. For green hydrogen to become a widely accepted energy source, improvements in electrolyzer efficiency are crucial to reducing overall production costs and improving the viability of hydrogen-powered systems. Moreover, the inefficiency in energy conversion limits the scalability of green hydrogen, especially for large industrial applications. If these efficiency concerns are not addressed, Spain could struggle to meet its production targets for green hydrogen, and the adoption rate may be slower than anticipated. For green hydrogen to remain a competitive and sustainable energy solution, it is critical that Spain continues to invest in improving the energy efficiency of electrolysis technologies.

Opportunities

Private Sector Collaborations

One of the most promising opportunities for Spain’s green hydrogen market lies in increased collaboration with the private sector. Strategic partnerships between energy companies, technology firms, and research institutions will accelerate innovation and drive the development of cost-effective hydrogen production and storage technologies. With venture capital firms increasingly interested in funding renewable energy initiatives, private sector involvement is essential to scaling green hydrogen projects in Spain. Collaborations with international firms will also provide Spain with access to advanced hydrogen technologies and enable the country to expand its green hydrogen exports, particularly to other European nations that are actively pursuing decarbonization goals. These collaborations could lead to the development of new hydrogen production technologies, storage solutions, and distribution networks that can reduce the costs and inefficiencies of the hydrogen supply chain. Spain’s government incentives, such as tax breaks and subsidies for private companies, will further enhance these collaborations, making them a key driver of growth in the green hydrogen market. As private sector investment continues to grow, Spain’s green hydrogen market is expected to benefit significantly, with a more diversified supply chain and lower production costs.

Expansion of Hydrogen in Transportation

The transportation sector represents a significant growth opportunity for Spain’s green hydrogen market. As the European Union works to meet its ambitious climate goals, Spain has the potential to become a leader in hydrogen-powered transportation, including buses, trucks, and trains. Spain’s government has already taken steps to encourage this transition by providing incentives for the purchase of hydrogen-powered vehicles and establishing hydrogen refueling infrastructure in major cities. Furthermore, Spain is positioning itself as a hub for hydrogen-powered transport, with several ongoing pilot projects demonstrating the viability of hydrogen fuel cell vehicles (FCVs) for public transportation and freight. The development of hydrogen refueling stations and transportation infrastructure is expected to expand rapidly in the coming years, making hydrogen-powered vehicles more accessible. This presents a unique opportunity for Spain to capitalize on the growing demand for zero-emission transportation solutions. As hydrogen vehicles become more common, demand for green hydrogen will rise significantly, benefiting both the transport and energy sectors. By focusing on the development of hydrogen-powered transportation systems, Spain can help reduce transportation sector emissions and position itself as a global leader in hydrogen mobility.

Future Outlook

The Spain Green Hydrogen Market is expected to experience significant growth over the next five years, driven by continued policy support and technological advancements. With the EU’s stringent decarbonization targets, Spain is positioning itself as a major player in green hydrogen production and export. Investment in hydrogen infrastructure, along with the integration of hydrogen into industrial processes, will drive demand. Technological developments in electrolysis efficiency and storage solutions will further reduce costs, making green hydrogen more accessible to various sectors, including transportation and energy.

Major Players

- Iberdrola

- Acciona

- Enagas

- Cepsa

- Siemens Energy

- Haldor Topsoe

- McPhy Energy

- Nel ASA

- Plug Power

- Air Products

- Shell

- RWE

- Sacyr

- Ferrovial

- Hydrostor

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Energy utilities

- Industrial companies

- OEMs in transport

- Hydrogen technology providers

- Renewable energy developers

Research Methodology

Step 1: Identification of Key Variables

Identify key variables impacting the green hydrogen market, including policy, technology, and demand factors.

Step 2: Market Analysis and Construction

Analyze historical data, current trends, and market dynamics to estimate market size and forecast growth.

Step 3: Hypothesis Validation and Expert Consultation

Consult with industry experts, stakeholders, and market participants to validate assumptions and refine projections.

Step 4: Research Synthesis and Final Output

Compile findings into a comprehensive report that includes market size, trends, competitive landscape, and forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Policy Support

Technological Advancements in Electrolysis

Rise in Demand for Decarbonization Solutions - Market Challenges

High Initial Capital Investment

Energy Efficiency of Green Hydrogen Production

Storage and Transportation Infrastructure Challenges - Market Opportunities

Partnerships with Private Sector for R&D

Investment in Export Markets

Integration of Green Hydrogen in Industrial Processes - Trends

Increase in Hydrogen Refueling Stations

Deployment of Hydrogen-Powered Vehicles - Government Regulations

Hydrogen Production Standards

Carbon Emissions Regulations

Energy Transition Policies - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Electrolyzers

Hydrogen Storage Solutions

Fuel Cells

Distribution and Transport Systems

Power-to-X Technologies - By Platform Type (In Value%)

Onshore Platforms

Offshore Platforms

Mobile Platforms

Industrial Platforms

Transport Platforms - By Fitment Type (In Value%)

On-site Systems

Centralized Systems

Portable Systems

Hybrid Systems - By End User Segment (In Value%)

Industrial Applications

Energy Sector

Transportation Sector

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, End User Segment, Procurement Channel, Fitment Type, Technology, Regulatory Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Iberdrola

Acciona

Enagas

Ferrovial

Naturgy

Sacyr

Cepsa

Siemens Energy

Nel ASA

Plug Power

McPhy Energy

Air Products

Shell

RWE

Haldor Topsoe

- Adoption in Heavy Industries

- Integration into Public Transport

- Shift Toward Renewable Energy Sources

- Incentive Programs for Industrial Users

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now