Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Spain healthcare infrastructure market is valued at approximately USD ~ billion based on a recent historical assessment. This market is primarily driven by the increasing demand for healthcare services due to an aging population, the rise in chronic diseases, and advances in medical technologies. The Spanish government’s focus on improving healthcare infrastructure, coupled with private sector investment, further propels the market’s growth, enhancing healthcare accessibility and the overall quality of services.

Dominant cities such as Madrid, Barcelona, and Valencia play a crucial role in the healthcare infrastructure market in Spain. These cities have a high concentration of healthcare facilities, including hospitals, clinics, and specialized treatment centers, that cater to a growing population. Madrid, as the capital, is home to the largest healthcare facilities and top medical research institutions, making it a key hub for healthcare services in Spain. Additionally, Barcelona and Valencia continue to develop their healthcare infrastructure, attracting both domestic and international patients seeking advanced treatments and high-quality care.

Market Segmentation

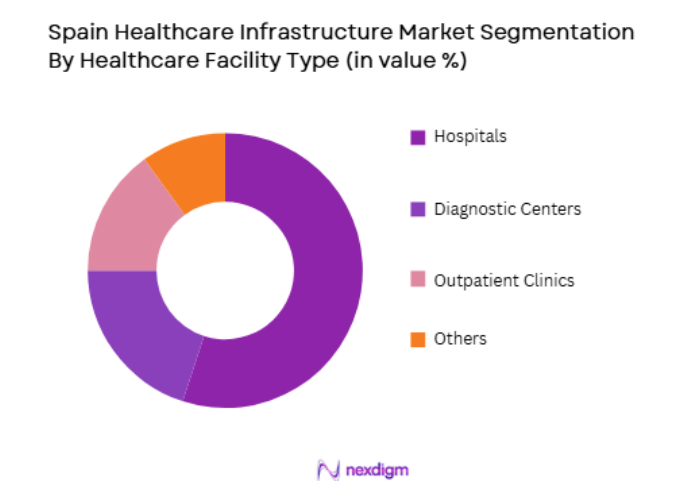

By Healthcare Facility Type

Spain’s healthcare infrastructure market is segmented by healthcare facility type into hospitals, diagnostic centers, outpatient clinics, and others. Recently, hospitals have dominated the market share due to their integral role in providing specialized treatments, emergency care, and critical healthcare services. Spain’s public healthcare system, along with the growing private healthcare sector, has contributed to the increasing demand for hospital services. These hospitals are adopting advanced technologies and expanding their services to meet the rising healthcare needs of the population. With a focus on specialized treatments such as cancer care, orthopedics, and cardiology, hospitals continue to drive growth in the Spanish healthcare infrastructure market.

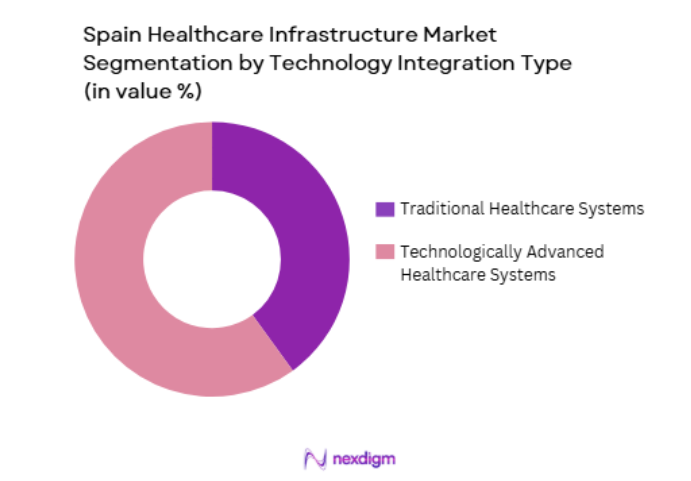

By Technology Integration

Spain’s healthcare infrastructure market is segmented by technology integration into traditional healthcare systems and technologically advanced healthcare systems. Recently, technologically advanced healthcare systems have dominated the market share due to the increasing adoption of digital health solutions such as electronic health records (EHR), telemedicine, and robotic-assisted surgeries. The integration of artificial intelligence (AI) and big data analytics has enhanced the efficiency and accuracy of healthcare services. As Spain continues to modernize its healthcare system, the demand for these advanced technological solutions is increasing, driving growth in this sub-segment of the market. Hospitals and clinics are leading the way in the adoption of these innovations, which are improving patient outcomes and operational efficiency.

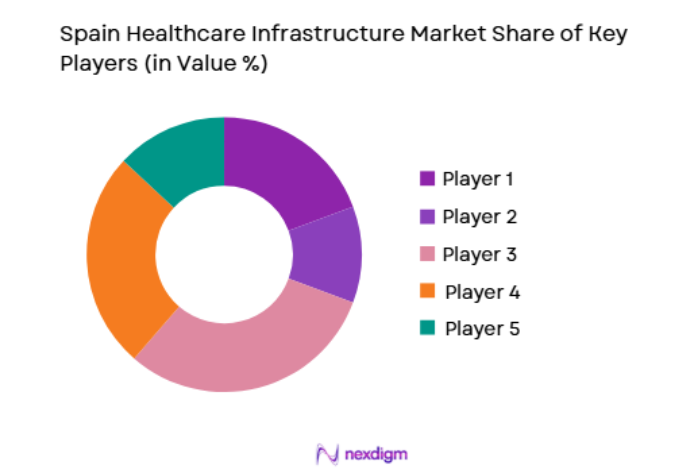

Competitive Landscape

The competitive landscape of Spain’s healthcare infrastructure market is characterized by a mix of public and private sector providers. The market is experiencing gradual consolidation, with larger hospital groups acquiring smaller clinics and diagnostic centers to expand their reach and service offerings. The influence of major players is growing, with large hospital networks and healthcare providers focusing on technological integration, efficiency improvements, and specialized services to meet the growing demand for high-quality healthcare. Private healthcare providers are also increasingly investing in advanced technologies such as telemedicine and AI to differentiate themselves in a competitive market.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Grupo Hospitalario Quirónsalud | 1999 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| Hospital Universitario La Paz | 1964 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| DKV Seguros | 1999 | Zaragoza, Spain | ~ | ~ | ~ | ~ | ~ |

| Sanitas | 1954 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| Fresenius Medical Care | 1996 | Bad Homburg, Germany | ~ | ~ | ~ | ~ | ~ |

Spain Healthcare Infrastructure Market Analysis

Growth Drivers

Government Investments in Healthcare

Government investments in healthcare infrastructure are a significant growth driver for Spain’s healthcare infrastructure market. Spain has committed to increasing public healthcare expenditure, focusing on improving hospital infrastructure, expanding healthcare facilities, and upgrading diagnostic centers. With a strong emphasis on enhancing healthcare services and accessibility, the government has been prioritizing the construction of new hospitals, modernization of existing healthcare facilities, and integration of digital health technologies. Furthermore, government-led initiatives such as the “Plan de Salud” aim to address regional disparities in healthcare access, which is expected to drive further demand for healthcare infrastructure. The public healthcare system, along with public-private partnerships, will continue to play a vital role in Spain’s healthcare infrastructure market, fostering growth in both urban and rural areas.

Technological Advancements in Healthcare

The adoption of technological advancements in healthcare is another major growth driver in Spain. As healthcare providers across the country continue to modernize their infrastructure, there has been a notable increase in the integration of digital health solutions. These include the widespread adoption of electronic health records (EHR), telemedicine services, robotic-assisted surgeries, and AI-driven diagnostics. The Spanish healthcare system is increasingly leveraging these technologies to enhance patient care, improve operational efficiency, and reduce healthcare costs. The growth of telemedicine, in particular, has accelerated due to the COVID-19 pandemic and is expected to continue expanding, especially in rural areas with limited access to healthcare facilities. As technological innovations continue to reshape the healthcare landscape, Spain’s healthcare infrastructure market is poised for sustained growth.

Market Challenges

Regulatory and Bureaucratic Challenges

One of the significant challenges facing Spain’s healthcare infrastructure market is navigating the complex regulatory and bureaucratic landscape. Spain has stringent regulations for the approval, certification, and operation of healthcare facilities, which can lead to delays in the development and expansion of new projects. Healthcare providers must adhere to various local, regional, and national regulations related to healthcare standards, safety, and patient care, which can be time-consuming and costly. Additionally, healthcare facilities must comply with evolving regulations regarding data privacy and security, particularly in relation to digital health technologies. While the Spanish government continues to streamline regulatory processes, the complexity of navigating these regulations remains a challenge for companies operating in the healthcare infrastructure market.

High Cost of Healthcare Infrastructure Development

The high cost of healthcare infrastructure development remains a significant challenge in Spain. Developing and maintaining state-of-the-art healthcare facilities, particularly in urban areas, requires significant investment in medical equipment, technology, and trained personnel. With Spain’s aging population and increasing demand for healthcare services, healthcare providers must continually invest in upgrading infrastructure to meet patient needs. However, the cost of construction, equipment, and technological adoption can be prohibitive, particularly for smaller healthcare providers and regional hospitals. Additionally, the economic uncertainty resulting from global challenges such as inflation and supply chain disruptions adds to the financial strain on healthcare infrastructure projects. To overcome this challenge, healthcare providers and the government must explore innovative financing options, such as public-private partnerships, to fund infrastructure development.

Opportunities

Medical Tourism

Spain’s growing reputation as a leading destination for medical tourism presents significant opportunities for the healthcare infrastructure market. The country offers high-quality healthcare services at competitive prices compared to other Western European nations, attracting patients from neighboring countries and beyond. Medical tourists are particularly drawn to Spain for elective procedures such as cosmetic surgeries, dental care, and fertility treatments. The Spanish healthcare system’s integration with tourism infrastructure also facilitates the growth of the medical tourism sector, with patients often combining treatments with leisure activities. To capitalize on this opportunity, Spain can expand its medical tourism services, enhance international marketing efforts, and continue to develop specialized treatment centers that cater to foreign patients.

Expansion of Healthcare Services in Rural Areas

The expansion of healthcare services in rural and underserved regions represents a key opportunity for Spain’s healthcare infrastructure market. While Spain’s major cities are home to world-class healthcare facilities, rural areas often face challenges in accessing specialized medical services. The government has recognized this disparity and has been working to expand healthcare services into these regions, including building new hospitals, diagnostic centers, and telemedicine networks. Investments in healthcare infrastructure in rural areas not only improve access to care but also create significant growth opportunities for both public and private healthcare providers. By addressing healthcare disparities, Spain can ensure that all citizens have access to high-quality medical services, driving further market expansion.

Future Outlook

The future outlook for Spain’s healthcare infrastructure market is positive, with continued growth expected over the next five years. The ongoing investments in healthcare facilities, the integration of advanced technologies, and the expansion of services into rural areas will drive market expansion. The growing demand for specialized medical services, combined with an aging population, will further increase the need for modern healthcare infrastructure. Technological advancements such as AI, telemedicine, and robotic surgery will continue to improve patient care and operational efficiency. With a strong focus on improving accessibility and patient outcomes, Spain’s healthcare infrastructure market is poised for sustained growth in the coming years.

Major Players

- GrupoHospitalarioQuirónsalud

- Hospital Universitario La Paz

- DKV Seguros

- Sanitas

- Fresenius Medical Care

- Hospital Clínic Barcelona

- Grupo Vithas

- Hospital General de Valencia

- Hospital Ramón y Cajal

- IDIS (Instituto para el Desarrollo e Integración de la Sanidad)

- HCA Healthcare España

- Grupo Quirónsalud

- Grupo Preving

- Ribera Salud

- Hospital de la Santa Creu i Sant Pau

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Hospitals and clinics

- Pharmaceutical companies

- Medical device manufacturers

- Insurance providers

- Medical research organizations

Research Methodology

Step 1: Identification of Key Variables

Key variables such as market size, growth drivers, segmentation factors, and key trends are identified through both primary and secondary research.

Step 2: Market Analysis and Construction

Comprehensive market data is gathered and analyzed using statistical models to build a detailed market forecast.

Step 3: Hypothesis Validation and Expert Consultation

Insights and assumptions are validated through consultations with industry experts to ensure the reliability of the findings.

Step 4: Research Synthesis and Final Output

The final report synthesizes all collected data, providing a comprehensive analysis of Spain’s healthcare infrastructure market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Investments in Healthcare Infrastructure

Technological Advancements in Healthcare Systems

Aging Population Driving Healthcare Demand - Market Challenges

High Operational Costs

Regulatory Barriers and Compliance Costs

Unequal Healthcare Access Across Regions - Market Opportunities

Adoption of Smart Healthcare Solutions

Government Initiatives for Rural Healthcare

Telemedicine Expansion - Trends

Integration of Artificial Intelligence in Healthcare

Shift Towards Value-based Care - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Hospital Infrastructure

Primary Care Facilities

Emergency Medical Services

Outpatient Care Centers

Specialized Healthcare Facilities - By Platform Type (In Value%)

Digital Health Platforms

Hospital Management Systems

Electronic Health Records (EHR) Platforms

Telemedicine Platforms

Integrated Healthcare Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions - By End User Segment (In Value%)

Public Healthcare Sector

Private Healthcare Sector

Healthcare Service Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technological Integration, Market Reach, Compliance with Healthcare Regulations, Service Quality, Infrastructure Scalability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Siemens Healthineers

GE Healthcare

Philips Healthcare

Medtronic

Roche Diagnostics

Schneider Electric

Cerner Corporation

Abbott Laboratories

Stryker Corporation

Becton Dickinson

Johnson & Johnson

Fujifilm Healthcare

Thermo Fisher Scientific

Zebra Technologies

Honeywell Life Sciences

- Public Healthcare Providers Adopting New Technologies

- Private Healthcare Expanding Infrastructure

- Government Role in Regulating Healthcare Systems

- Healthcare Service Providers Leveraging Digital Tools

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now