Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Spain home finance market is experiencing growth, driven by factors such as an expanding middle class, low interest rates, and the increasing adoption of digital mortgage solutions. In recent assessments, the market size is valued in the billions of USD, with mortgage lending playing a crucial role in the growth of the sector. This growth is bolstered by the rise in property ownership rates and ongoing government housing initiatives aimed at boosting the market’s development.

Spain’s dominant cities, such as Madrid and Barcelona, continue to be the main drivers of the home finance market. Their central locations, growing infrastructure, and robust economic activity create strong demand for housing and mortgages. The strong presence of financial institutions and digital platforms in these urban areas fuels the market’s expansion, while ongoing urbanization and migration trends contribute to increased demand for home loans across the country.

Market Segmentation

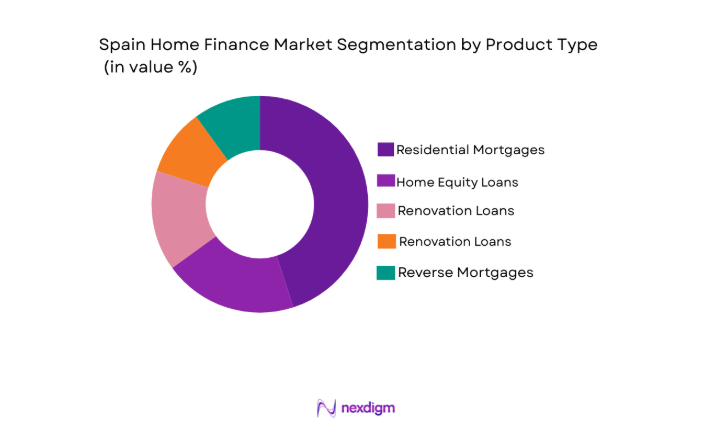

By Product Type

The Spain home finance market is segmented by product type into residential mortgages, home equity loans, renovation loans, refinancing products, and reverse mortgages. Recently, residential mortgages dominate the market share due to the increasing demand for homeownership across various income levels, supported by favorable government schemes and lower interest rates. The continuous expansion of urban areas and rising disposable incomes further contribute to the high uptake of residential mortgages, solidifying its position as the dominant sub-segment.

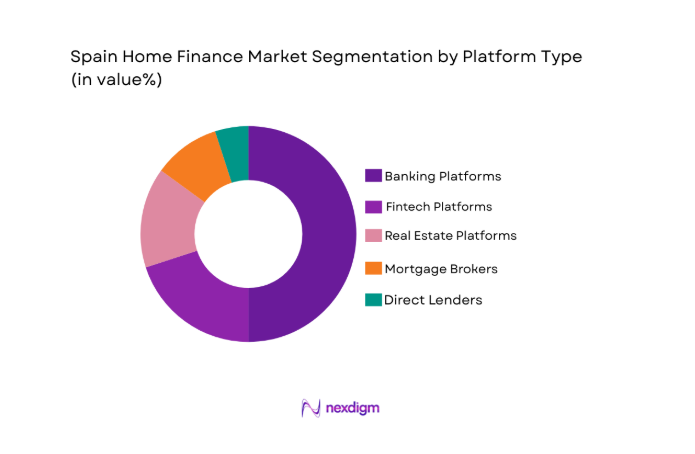

By Platform Type

The Spain home finance market is segmented by platform type into banking platforms, fintech platforms, real estate platforms, mortgage brokers, and direct lenders. Recently, banking platforms have dominated the market due to their established presence, customer trust, and extensive branch networks. These platforms are able to offer a variety of mortgage solutions, integrate new technologies, and attract both traditional customers and digitally-savvy borrowers, positioning them as the leading platform type in the market.

Competitive Landscape

The competitive landscape of the Spain home finance market is marked by a mix of traditional banking institutions, emerging fintech platforms, and digital lenders. The market is consolidating as major banks continue to acquire smaller players to expand their digital services and reach. Larger financial institutions dominate the market, with fintech firms gaining ground by offering specialized and more efficient services. This competitive environment is fostering innovation, improving service delivery, and expanding accessibility to home financing products.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Banco Santander | 1857 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| BBVA | 1857 | Bilbao, Spain | ~ | ~ | ~ | ~ | ~ |

| CaixaBank | 1904 | Barcelona, Spain | ~ | ~ | ~ | ~ | ~ |

| Bankinter | 1965 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| ING Direct | 1997 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

Spain Home Finance Market Analysis

Growth Drivers

Increasing Homeownership Demand

The growing demand for homeownership in Spain has significantly driven the home finance market. This surge is mainly due to a steady increase in disposable income, favorable interest rates, and government-backed initiatives aimed at helping first-time buyers. As urbanization continues, more people are looking to invest in property, boosting demand for mortgages and home loans. Additionally, the expansion of digital platforms has made accessing financing easier and faster, making homeownership more attainable for a broader population. The increasing middle-class population further supports this demand, as more individuals and families seek permanent housing solutions. Economic stability and improved consumer confidence contribute to this positive trend, further driving the mortgage market.

Government Housing Programs

Government-backed housing programs and subsidies have been a significant growth driver for the Spanish home finance market. These initiatives aim to make homeownership more accessible, particularly for first-time buyers and low-income households. By providing lower interest rates, tax incentives, and direct subsidies, the government has been able to stimulate demand in the home finance sector. In addition to these financial incentives, urban development projects in various regions, especially in major cities, have increased the supply of homes, making mortgages a key financing option. As these programs continue to evolve and expand, they are expected to further drive the growth of the home finance market in Spain.

Market Challenges

Economic Uncertainty and Political Instability

Economic uncertainty and political instability have posed challenges for Spain’s home finance market. Fluctuations in the national economy, combined with changes in government policies, can create a volatile environment for borrowers and lenders alike. Potential increases in interest rates and shifts in housing market regulations can lead to reluctance among homebuyers and lenders. For example, uncertainty around housing regulations or potential changes in tax laws can create hesitations for both consumers and investors. As such, the market’s growth could be dampened by these unpredictable external factors, which impact the overall consumer confidence and decision-making process.

High Levels of Household Debt

Another challenge for the Spain home finance market is the rising level of household debt. Overleveraging and the associated risks of default have created concerns within the financial sector. As the cost of living increases and wages remain stagnant for many, consumers may struggle to meet their financial obligations, including mortgage repayments. The growing reliance on credit and loans in general has made Spanish households vulnerable to financial instability. Lenders, in turn, face increased risk of non-repayment, leading to stricter lending criteria and higher interest rates. As a result, the market’s expansion could be hindered if consumers face difficulty in securing and repaying loans.

Opportunities

Rise in Digital Mortgage Solutions

The increasing adoption of digital mortgage platforms represents a key opportunity for the Spain home finance market. With the growth of fintech and mobile banking, more consumers are turning to online solutions for securing home loans and mortgages. These platforms offer greater convenience, faster approval processes, and lower costs compared to traditional methods. Fintech companies, in particular, are tapping into a younger, tech-savvy demographic, reshaping the mortgage landscape in Spain. With a growing preference for digital-first experiences, there is significant potential for the market to expand, as more consumers seek seamless, online mortgage solutions. The use of artificial intelligence and data analytics also allows lenders to better understand borrower profiles, improving the overall customer experience and fostering further growth in the sector.

Increasing Demand for Green Mortgages

As sustainability becomes a larger focus in the global financial market, the demand for green mortgages in Spain is growing. Green mortgages, which offer favorable terms for environmentally friendly homes, are expected to increase in popularity as both consumers and governments place greater emphasis on sustainability. These products not only support environmentally conscious borrowers but also benefit from regulatory incentives and tax breaks. As green building practices become more mainstream, lenders are increasingly offering specialized mortgage products that encourage energy-efficient home purchases or renovations. This growing demand for eco-friendly mortgages presents a valuable opportunity for lenders to differentiate themselves in the market, while simultaneously contributing to Spain’s sustainability goals.

Future Outlook

The future outlook for the Spain home finance market appears positive, with continued growth expected in digital mortgage solutions, driven by technological advancements and consumer preference for online platforms. The regulatory landscape is also evolving, with ongoing support for homeownership initiatives and green mortgages. As the market expands, new players, especially fintech firms, are expected to further disrupt traditional banking models. Overall, demand for home loans is set to grow as economic stability, urbanization, and favorable housing policies continue to support the sector.

Major Players

- Banco Santander

- BBVA

- CaixaBank

- Bankinter

- ING Direct

- UCI

- Deutsche Bank

- Sabadell

- Openbank

- Bankia

- ABN AMRO

- Kutxabank

- Liberbank

- Banc Sabadell

- ING Group

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Financial institutions

- Mortgage lenders

- Real estate developers

- Housing authorities

- Digital platform developers

- Consumers and homebuyers

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying key market variables such as demand patterns, customer preferences, and technological advancements that influence the home finance market. This helps in setting a clear scope for the research.

Step 2: Market Analysis and Construction

This step involves analyzing historical data, current market trends, and future forecasts, to build a comprehensive market model. Data from secondary and primary sources are used to ensure accuracy.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations are conducted to validate the hypotheses formed during market analysis. Industry professionals and market leaders provide insights that refine the findings and confirm market assumptions.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing all the research findings and preparing the output in a structured report. This is followed by a thorough review and final adjustments to ensure the accuracy of the market insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Property Ownership Rates

Government Subsidies and Housing Programs

Rising Middle-Class Affordability

Urbanization and Migration Trends

Expansion of Digital Mortgage Solutions - Market Challenges

Regulatory Compliance and Risk Management

High Interest Rates on Loans

Tightening of Lending Criteria

Fluctuations in Property Prices

Economic Uncertainty and Political Instability - Market Opportunities

Emerging Demand for Green Mortgages

Growth in Digital Mortgage Platforms

Increasing Demand for Short-Term Financing - Trends

Adoption of Digital Loan Origination Platforms

Growth in Home Equity Loan Products

Rise of AI and Automation in Loan Processing

Integration of ESG Criteria in Mortgage Lending

Shift Toward Paperless and Mobile Solutions - Government Regulations & Defense Policy

Data Protection and Privacy Laws

New Mortgage Regulation Guidelines

Housing Finance Policies and Government Aid - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Residential Mortgages

Home Equity Loans

Renovation Loans

Refinancing Products

Reverse Mortgages - By Platform Type (In Value%)

Banking Platforms

Fintech Platforms

Real Estate Platforms

Mortgage Brokers

Direct Lenders - By Fitment Type (In Value%)

Online Solutions

In-Branch Solutions

Hybrid Solutions

Automated Systems

Mobile App-Based Solutions - By End User Segment (In Value%)

First-Time Homebuyers

Homeowners Looking to Refinance

Real Estate Investors

Mortgage Advisors

Financial Institutions - By Procurement Channel (In Value%)

Direct Sales

Online Marketplaces

Referral Networks

Brokered Loans

Partnerships with Real Estate Agents

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Interest Rate, Loan Tenure, Loan-to-Value Ratio, Processing Time, Digital Onboarding Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Banco Santander

BBVA

CaixaBank

Bankinter

Sabadell

ING Direct

Openbank

Eurobank

UCI

Kreditea

Deutsche Bank

Abanca

Kutxabank

Unicaja Banco

Cajamar

- First-time homebuyers increasingly turn to digital solutions

- Homeowners pursue refinancing due to fluctuating rates

- Real estate investors leverage diverse financing products

- Financial institutions focus on expanding mortgage portfolios

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now