Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Spain Industrial Automation Market is expected to reach a significant size, with the market driven by continuous advancements in automation technology and increasing demand from industries such as manufacturing and automotive. Based on a recent historical assessment, the market size is estimated at USD ~ billion, showing consistent growth due to the widespread adoption of industrial robots, AI-driven solutions, and IoT integration. The push for greater efficiency and cost savings in industrial operations fuels this expansion.

Dominant regions in the Spanish industrial automation market include major urban centers like Madrid, Barcelona, and Valencia. These areas benefit from strong industrial infrastructure, government initiatives to modernize manufacturing processes, and proximity to key European markets. Barcelona’s emphasis on smart manufacturing, and Madrid’s leading role in automotive and machinery industries, further consolidates Spain’s position as a regional leader in industrial automation technology.

Market Segmentation

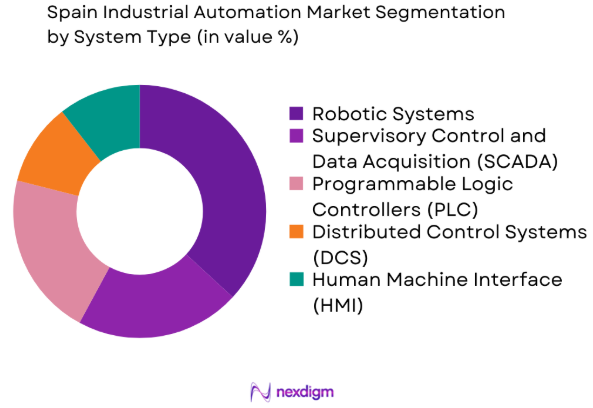

By System Type

The Spain Industrial Automation Market is segmented by system type into robotic systems, supervisory control and data acquisition (SCADA), programmable logic controllers (PLC), distributed control systems (DCS), and human-machine interface (HMI). Recently, robotic systems have taken the largest market share due to their widespread adoption in automotive and manufacturing sectors. The growing demand for efficiency, precision, and flexibility in production lines contributes to the dominance of robotic systems, particularly in automotive manufacturing, where robots play a critical role in assembly lines and component handling.

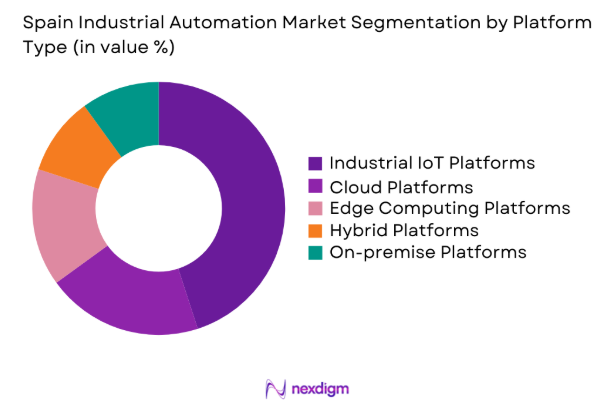

By Platform Type

The Spain Industrial Automation market is segmented by platform type into cloud platforms, edge computing platforms, on-premise platforms, hybrid platforms, and industrial IoT platforms. Industrial IoT platforms currently dominate the market due to their ability to connect diverse machinery and systems, enabling real-time monitoring and predictive maintenance. The increased push for data-driven decision-making and operational efficiency across industries, including manufacturing and logistics, has led to rapid adoption of IoT technologies for automation in Spain.

Competitive Landscape

The competitive landscape of the Spain Industrial Automation Market is highly dynamic, with a mix of established multinational companies and local players leading technological advancements. The consolidation of the industry is evident through strategic partnerships and mergers, aiming to enhance technological capabilities and expand market reach. Key players are increasingly focusing on the integration of AI, robotics, and IoT into their automation solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Parameter |

| Siemens AG | 1847 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

| Rockwell Automation | 1903 | Milwaukee, USA | ~ | ~ | ~ | ~ | ~ |

| ABB Ltd. | 1988 | Zurich, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Schneider Electric | 1836 | Rueil-Malmaison, France | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Electric | 1921 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

Spain Industrial Automation Market Analysis

Growth Drivers

Technological Advancements in Robotics

Advancements in robotics are driving substantial growth in the Spain Industrial Automation Market. The demand for robots is increasing due to the need for higher precision, greater productivity, and reduced human involvement in hazardous tasks. AI integration in robotic systems enhances their adaptability, improves decision-making, and cuts operational costs. Sectors like automotive and electronics are leading the adoption of robotics to streamline production lines and minimize waste. This technological progress is essential for automation, as industries aim to stay competitive in a globalized market. Additionally, ongoing investment in research and development to enhance robotic capabilities is accelerating growth. These innovations enable companies to provide smarter, more efficient solutions tailored to the unique needs of Spanish industries.

Market Demand for Smart Manufacturing

Smart manufacturing is a significant growth driver for the Spain Industrial Automation Market. By integrating IoT, AI, and big data analytics, manufacturers can monitor real-time data, predict maintenance needs, and optimize production. Cities like Barcelona and Madrid have emerged as hubs for smart manufacturing, focusing on reducing energy consumption, improving efficiency, and enhancing flexibility. Companies are investing in IoT-enabled sensors and devices to upgrade their facilities and automate workflows. This shift towards smart manufacturing is expected to boost demand for industrial automation systems, particularly in sectors like automotive, electronics, and heavy industries, further driving market growth as businesses adopt more efficient, data-driven production processes.

Market Challenges

High Initial Capital Investment

A significant challenge in the Spain Industrial Automation Market is the high upfront capital investment required for automation systems. While automation offers long-term savings and operational efficiency, the initial cost of installing automated machinery, robots, and advanced control systems can be a barrier for small and medium-sized enterprises (SMEs). These businesses often face challenges in securing the necessary funding for automation, as they prioritize short-term financial stability over long-term investments. The cost of upgrading existing infrastructure, training employees to operate new technologies, and ensuring compatibility with existing systems further increases the financial burden. Despite these challenges, the long-term benefits of automation, such as improved productivity and reduced labor costs, are gradually persuading companies to make the investment.

Integration Complexities

A key challenge in the Spain Industrial Automation Market is the difficulty in integrating new automation systems with existing legacy infrastructure. Many companies rely on outdated systems that are incompatible with modern technologies like AI, robotics, and IoT, which makes integration complex and resource-intensive. This requires significant time and effort to ensure compatibility between old and new systems. Additionally, the shortage of skilled workers proficient in both legacy and modern technologies exacerbates the issue. Companies must invest in workforce training to effectively manage these new systems. These integration challenges often result in delays, increased costs, and can discourage businesses from adopting automation.

Opportunities

Adoption of AI-driven Automation Solutions

One of the most promising opportunities for the Spain Industrial Automation Market is the increased adoption of AI-driven automation solutions. AI and machine learning algorithms enable systems to learn from historical data and optimize production processes in real time. These technologies can significantly reduce downtime, improve product quality, and enable predictive maintenance, which reduces the need for unscheduled maintenance and associated costs. Spain’s push toward Industry 4.0 and its focus on developing AI solutions for automation make this an attractive opportunity for companies to upgrade their operations. The growing need for automation in sectors such as automotive, manufacturing, and logistics will further drive demand for AI-based solutions that can optimize processes and enhance overall operational efficiency.

Expansion in Robotics for Small and Medium Enterprises (SMEs)

Small and medium-sized enterprises (SMEs) represent a significant untapped opportunity for the Spain Industrial Automation Market. While large corporations have been quick to adopt industrial automation, many SMEs still rely on traditional manual processes. However, advancements in robotics technology, such as collaborative robots (cobots), are making automation more accessible to SMEs. These robots are less expensive, easier to integrate, and do not require extensive changes to existing infrastructure. As SMEs in Spain look to modernize their operations, cobots present a cost-effective solution for automating repetitive tasks, improving worker safety, and enhancing productivity. This presents a significant growth opportunity for automation companies that can tailor solutions to the specific needs and budget constraints of SMEs.

Future Outlook

The future of the Spain Industrial Automation Market looks promising, with continued growth driven by technological advancements, government support, and increasing demand for smart manufacturing solutions. Over the next five years, the market is expected to see increased adoption of AI, robotics, and IoT technologies, which will further enhance production efficiency and reduce costs across industries. The Spanish government’s focus on digitalization and sustainable practices will create a favorable regulatory environment for automation technologies. As industries seek to stay competitive in a rapidly evolving global market, Spain will continue to be a key player in industrial automation.

Major Players

- Siemens AG

- Rockwell Automation

- ABB Ltd.

- Schneider Electric

- Mitsubishi Electric

- Honeywell International Inc.

- Yokogawa Electric Corporation

- Fanuc Corporation

- Emerson Electric Co.

- Bosch Rexroth AG

- KUKA AG

- Omron Corporation

- Beckhoff Automation

- Festo AG

- NACHI-FUJIKOSHI Corp.

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Industrial manufacturing companies

- Robotics and automation companies

- Engineering firms

- System integrators

- Automotive manufacturers

- Logistics and supply chain companies

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the key market drivers, challenges, and opportunities in the Spain Industrial Automation Market. The research includes a comprehensive review of the technological, economic, and regulatory factors that influence market dynamics.

Step 2: Market Analysis and Construction

Data collection is conducted through both primary and secondary sources to analyze current trends, market segments, and competitive positioning. This includes interviews with industry experts, market surveys, and company reports.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses developed from initial research are validated through consultations with industry experts and market participants to ensure accuracy and reliability in the findings.

Step 4: Research Synthesis and Final Output

The final research report synthesizes all collected data, providing actionable insights, forecasts, and recommendations for stakeholders in the Spain Industrial Automation Market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Demand for Automation in Manufacturing

Technological Advancements in Robotics and AI

Government Initiatives Supporting Industrial Modernization - Market Challenges

High Initial Capital Investment

Complex Integration with Existing Systems

Lack of Skilled Workforce in Automation Technologies - Market Opportunities

Expansion of AI and Machine Learning in Automation

Growth of Smart Manufacturing Initiatives

Increasing Demand for Customized Automation Solutions - Trends

Rise in Collaborative Robots (Cobots)

Adoption of Digital Twin Technology

Integration of IoT for Predictive Maintenance - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Robotic Systems

Supervisory Control and Data Acquisition (SCADA)

Programmable Logic Controllers (PLC)

Distributed Control Systems (DCS)

Human Machine Interface (HMI) - By Platform Type (In Value%)

- Cloud Platforms

Edge Computing Platforms

On-premise Platforms

Hybrid Platforms

Industrial IoT Platforms - By Fitment Type (In Value%)

Retrofitting Solutions

New Installations

System Upgrades

Custom Configurations

Modular Solutions - By End User Segment (In Value%)

Manufacturing Industry

Automotive Industry

Chemical and Petrochemical Industry

Food and Beverage Industry

Pharmaceutical Industry - By Procurement Channel (In Value%)

Direct Procurement

Third-party Distributors

Online Procurement

Government Tenders

Private Sector Procurement

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Automation Technology, Application Type, Service Type, Industry Vertical, Regional Presence)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Siemens AG

Rockwell Automation

ABB Ltd.

Schneider Electric

Mitsubishi Electric Corporation

Honeywell International Inc.

Yokogawa Electric Corporation

Fanuc Corporation

Emerson Electric Co.

Bosch Rexroth AG

KUKA AG

Omron Corporation

Beckhoff Automation

Festo AG

NACHI-FUJIKOSHI Corp.

- Manufacturing Industry’s Focus on Efficiency

- Automotive Sector’s Shift Towards Smart Factories

- Chemical Industry’s Adoption of Safety Automation

- Pharmaceutical Sector’s Increasing Demand for Precision

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now