Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Spain Last-Mile Delivery Market generated approximately USD ~ billion in revenue, supported by rapid growth in digital commerce and increasing parcel shipment volumes across national logistics networks. Data from Spain’s National Statistics Institute indicates that online retail transactions exceeded USD ~ billion, significantly strengthening demand for delivery services connecting fulfillment centers with consumers. Logistics providers expanded automated sorting hubs, electric delivery fleets, and digital route optimization platforms to manage high volumes of daily shipments efficiently across urban and suburban areas.

Major logistics activity is concentrated in metropolitan regions such as Madrid, Barcelona, Valencia, and Zaragoza, where dense population clusters and strong transportation infrastructure support efficient parcel distribution networks. Madrid functions as the largest logistics gateway due to its central geographic position and extensive fulfillment center capacity supporting nationwide deliveries. Barcelona benefits from strong port connectivity and international trade flows, while Valencia and Zaragoza host large logistics parks and distribution hubs that support e-commerce fulfillment operations and regional parcel transportation across Spain.

Market Segmentation

By Product Type

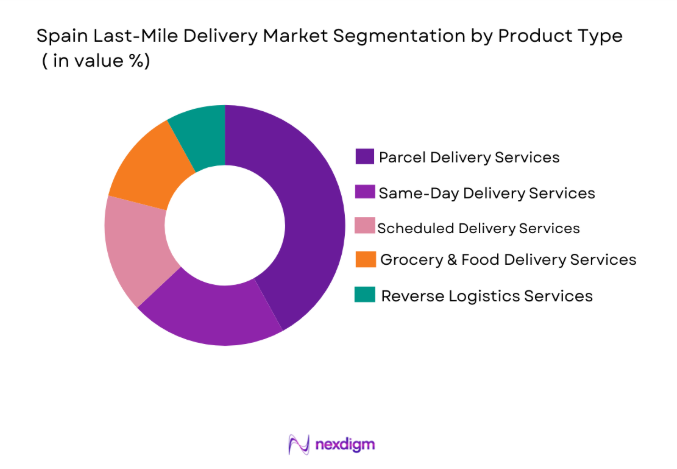

Spain Last-Mile Delivery Market is segmented by product type into parcel delivery services, same day delivery services, scheduled delivery services, grocery and food delivery services, and reverse logistics services. Recently, parcel delivery services has a dominant market share due to factors such as strong demand from online retail platforms, widespread logistics infrastructure, and the rapid growth of parcel shipments across metropolitan areas. E-commerce marketplaces generate extremely high parcel volumes requiring efficient transportation from fulfillment warehouses to residential consumers. Large logistics companies operate automated parcel sorting centers and extensive delivery fleets, allowing them to process millions of daily shipments. Retail companies increasingly rely on parcel delivery networks to support omnichannel distribution models connecting warehouses, retail stores, and final consumers. As consumer expectations for fast and reliable deliveries continue increasing, parcel delivery services remain the largest operational segment within the national logistics ecosystem.

By Platform Type

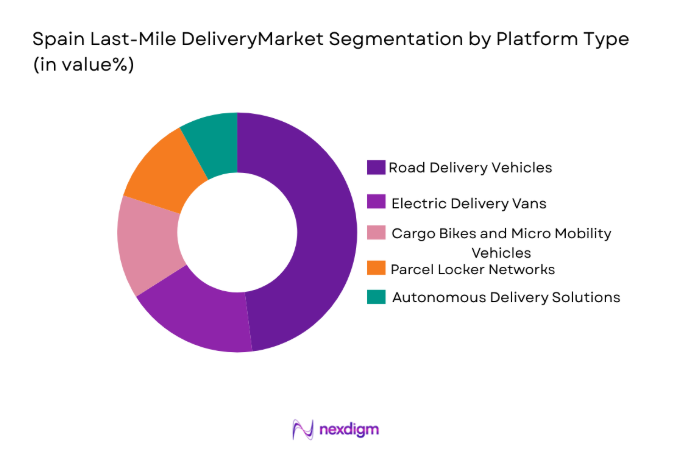

Spain Last-Mile Delivery Market is segmented by platform type into road delivery vehicles, electric delivery vans, cargo bikes and micro mobility vehicles, parcel locker networks, and autonomous delivery solutions. Recently, road delivery vehicles has a dominant market share due to factors such as established transportation infrastructure, large logistics fleets, and the flexibility required to deliver shipments across urban and suburban areas. Logistics operators maintain thousands of vans and trucks capable of transporting parcels between distribution centers and final delivery points. Major courier companies depend on road networks linking logistics parks with metropolitan consumer markets. Road delivery fleets allow operators to handle high shipment volumes efficiently while supporting both same day and scheduled delivery services. As urban logistics networks continue expanding, conventional road-based delivery vehicles remain the primary operational platform across the national distribution system.

Competitive Landscape

The Spain Last-Mile Delivery Market exhibits moderate consolidation with a combination of national postal operators, international logistics corporations, and specialized urban delivery platforms competing for market presence. Established courier companies maintain extensive distribution networks, automated sorting facilities, and large delivery fleets that enable nationwide parcel transportation. At the same time, technology-driven logistics startups focus on rapid delivery services and urban micro-fulfillment networks. Strategic partnerships with e-commerce retailers and investments in automated logistics technologies continue to influence competitive positioning across the market.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Fleet Size |

| Correos | 1716 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| SEUR | 1942 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| MRW | 1977 | Barcelona, Spain | ~ | ~ | ~ | ~ | ~ |

| DHL Parcel Spain | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| Amazon Logistics Spain | 2018 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

Spain Last-Mile Delivery Market Analysis

Growth Drivers

Expansion of E Commerce Fulfillment and Digital Retail Logistics Networks

The Spain Last-Mile Delivery Market experiences strong growth due to the rapid expansion of online retail platforms generating extremely high parcel shipment volumes across urban consumer markets. Digital commerce companies selling electronics, clothing, groceries, and household goods depend heavily on professional delivery networks capable of processing thousands of orders daily. Large fulfillment centers located near metropolitan regions distribute products to consumers through complex logistics networks. Automated sorting hubs and warehouse management technologies accelerate parcel handling efficiency. Retail companies increasingly adopt omnichannel distribution models where warehouses supply both physical stores and direct consumer deliveries. Logistics providers invest in route optimization software and automated dispatch systems that improve operational productivity. High smartphone penetration and digital payment adoption further increase participation in online retail purchases across Spain. Continuous growth in digital retail transactions therefore remains one of the strongest structural drivers supporting long term expansion of last-mile logistics services nationwide.

Urban Population Density and Consumer Demand for Rapid Delivery Services

Spain’s major metropolitan regions host large populations that generate extremely high demand for fast parcel delivery services supporting daily consumer purchases. Cities such as Madrid, Barcelona, and Valencia contain dense residential neighborhoods where millions of online orders are delivered directly to households. Consumers increasingly expect same day or next day delivery options when purchasing products through digital retail platforms. Logistics operators therefore deploy advanced delivery scheduling platforms that coordinate shipments across thousands of addresses daily. Urban micro fulfillment centers positioned close to residential districts help reduce delivery distances and transportation times. Courier companies also operate parcel lockers and neighborhood pickup points that increase convenience for urban consumers. Continuous growth of digital commerce activity across urban populations significantly increases the number of daily parcel shipments processed by logistics networks. Rising consumer expectations for faster delivery services therefore remains a major structural driver accelerating the expansion of last-mile logistics infrastructure.

Market Challenges

Urban Traffic Congestion and Delivery Route Inefficiencies

Urban congestion across major Spanish cities significantly complicates last-mile delivery operations because delivery vehicles must navigate crowded streets and limited parking availability during peak traffic periods. Courier drivers frequently experience delays while transporting parcels between distribution centers and residential neighborhoods. Municipal traffic restrictions and limited access zones further increase delivery complexity in dense urban districts. Logistics companies must therefore design advanced route optimization systems that minimize transportation delays. Delivery fleets often operate during extended hours to avoid daytime congestion. Increased delivery volumes from digital retail transactions further intensify traffic pressure across metropolitan areas. Courier companies must invest heavily in operational planning technologies that improve route efficiency and vehicle utilization. These operational constraints increase delivery costs and reduce fleet productivity across logistics networks. Urban congestion therefore represents a persistent logistical challenge affecting last-mile distribution efficiency throughout Spain’s largest cities.

Rising Operational Costs and Labor Shortages in Logistics Services

Logistics providers operating across Spain face increasing operational costs related to labor wages, fuel expenses, vehicle maintenance, and distribution facility operations. Delivery companies require thousands of drivers and logistics staff to manage nationwide parcel shipments. Competition for qualified logistics workers creates recruitment challenges for courier operators. Fuel price fluctuations significantly influence transportation costs associated with daily delivery operations. Companies must also invest in modern logistics technologies including automated sorting equipment and route optimization software. Environmental regulations encouraging the adoption of electric vehicles further increase capital expenditure requirements for logistics fleets. Distribution hubs require large warehouse facilities and advanced infrastructure capable of managing growing shipment volumes. As parcel shipments continue increasing nationwide, logistics companies must continuously expand operational capacity while managing rising cost pressures. These structural cost factors create significant operational challenges for delivery providers competing within Spain’s last-mile logistics ecosystem.

Opportunities

Adoption of Electric Delivery Vehicles and Sustainable Urban Logistics Solutions

The Spain Last-Mile Delivery Market presents strong opportunities through the transition toward environmentally sustainable urban logistics operations using electric delivery vehicles and low emission transport technologies. Government policies supporting carbon reduction encourage logistics companies to replace conventional diesel delivery vans with electric vehicle fleets. Electric vans reduce fuel costs while complying with emission regulations implemented across urban low emission zones. Logistics providers therefore invest in electric vehicle charging infrastructure and energy efficient distribution hubs. Cargo bikes and micro mobility delivery vehicles also support sustainable parcel transportation within dense city centers. E commerce companies increasingly prioritize environmentally responsible logistics partners capable of reducing carbon emissions. Municipal authorities support sustainable logistics initiatives through regulatory incentives and urban mobility programs. Continuous investment in green logistics technologies therefore opens significant growth opportunities for companies modernizing their delivery fleets and distribution infrastructure across Spain.

Expansion of Automated Parcel Lockers and Urban Micro Fulfillment Centers

Rapid deployment of parcel locker networks and urban micro fulfillment centers creates major opportunities for improving delivery efficiency across the Spain Last-Mile Delivery Market. Automated parcel lockers allow consumers to collect packages at convenient locations without requiring direct home delivery. Retailers and logistics companies install locker stations in residential complexes, transportation hubs, and retail centers. These systems reduce failed delivery attempts and improve parcel distribution efficiency. Urban micro fulfillment centers positioned close to residential districts shorten delivery distances and enable faster shipment dispatch. Logistics providers increasingly integrate automated warehouse technologies that accelerate order processing within these facilities. E commerce retailers benefit from reduced delivery times and improved customer satisfaction levels. As online retail purchases continue increasing across Spain, parcel locker networks and micro fulfillment infrastructure provide significant opportunities for optimizing last-mile logistics operations nationwide.

Future Outlook

The Spain Last-Mile Delivery Market is expected to experience strong expansion driven by continuous growth in digital commerce and urban logistics infrastructure development. Logistics companies are increasingly adopting automated warehouse technologies, artificial intelligence route optimization systems, and electric delivery fleets to improve operational efficiency. Government policies encouraging sustainable urban transportation will accelerate the transition toward low emission logistics networks. Increasing consumer expectations for faster deliveries will also encourage companies to expand micro fulfillment centers and automated parcel locker systems across major metropolitan regions.

Major Players

- Correos

- SEUR

- MRW

- DHL Parcel Spain

- UPS Spain

- FedEx Spain

- Amazon Logistics Spain

- GLS Spain

- Nacex

- Tipsa

- Paack

- Stuart

- Deliverea

- Ontime Logistics

- Sending Transporte y Logistica

Key Target Audience

- Logistics and transportation companies

- E-commerce retail companies

- Parcel delivery service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Supply chain technology providers

- Urban logistics infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Key operational variables including parcel shipment volumes, logistics infrastructure development, transportation fleet capacity, and digital retail activity were identified to evaluate demand patterns within the Spain Last-Mile Delivery Market. Data collection included logistics network capacity, urban distribution infrastructure, and technology adoption trends influencing delivery efficiency.

Step 2: Market Analysis and Construction

Comprehensive analysis of logistics providers, delivery networks, distribution centers, and e-commerce fulfillment infrastructure was conducted to construct the market structure. Historical operational data and industry performance indicators were examined to understand the relationship between retail transactions and parcel delivery demand.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics managers, distribution network operators, and supply chain specialists were consulted to validate market assumptions and operational trends. Expert insights were used to refine market dynamics, operational constraints, and technology adoption patterns influencing logistics performance.

Step 4: Research Synthesis and Final Output

All collected quantitative data and qualitative industry insights were consolidated into a comprehensive analytical framework to generate final market conclusions. Market drivers, operational challenges, technological developments, and strategic opportunities were synthesized to produce a structured industry report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E Commerce Fulfillment and Digital Retail Logistics Networks

Urban Population Density Driving High Parcel Delivery Demand

Adoption of Smart Logistics Technologies and Route Optimization Systems - Market Challenges

Urban Traffic Congestion and Delivery Route Inefficiencies

Rising Operational Costs and Labor Shortages in Logistics Services

Environmental Regulations Restricting Conventional Delivery Fleets - Market Opportunities

Adoption of Electric Delivery Vehicles and Sustainable Urban Logistics Solutions

Expansion of Automated Parcel Locker Networks

Development of Urban Micro Fulfillment Centers - Trends

Growth of Sustainable Green Delivery Fleets

Integration of Artificial Intelligence in Logistics Route Optimization - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

By System Type (In Value%)

Parcel Delivery Services

Same Day Delivery Services

Scheduled Time Slot Delivery Services

Food and Grocery Delivery Services

Reverse Logistics Pickup Services

By Platform Type (In Value%)

Road Delivery Vehicles

Electric Delivery Vans

Cargo Bikes and Micro Mobility Vehicles

Autonomous Delivery Robots

Drone Delivery Platforms

By Fitment Type (In Value%)

In House Logistics Networks

Third Party Logistics Integration

Marketplace Fulfillment Partnerships

Hybrid Delivery Networks

By End User Segment (In Value%)

E Commerce Retailers

Food and Grocery Platforms

Pharmaceutical and Healthcare Distributors

- Market Share Analysis

- Cross Comparison Parameters (Delivery Fleet Size, Geographic Coverage, Delivery Speed, Technology Integration, Sustainability Initiatives, Pricing Model, Service Portfolio)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Correos

SEUR

MRW

GLS Spain

DHL Parcel Spain

UPS Spain

FedEx Spain

Amazon Logistics Spain

Paack Logistics

Stuart Delivery

Nacex

Ontime Logistics

Tipsa

Sending Transporte y Logistica

Deliverea

- Retailers Increasing Dependence on Third Party Delivery Networks

- Food Delivery Platforms Expanding Rapid Urban Distribution Services

- Pharmaceutical Distributors Requiring Temperature Controlled Delivery Logistics

- Grocery Retail Chains Expanding Same Day Delivery Infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now