Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Spain Solar PV market is valued in billions ~ USD, driven by factors such as government incentives, increased consumer demand for sustainable energy, and the growing trend of solar adoption in both residential and commercial sectors. Technological advancements in solar panels and efficiency improvements have further accelerated growth. Regulatory frameworks, such as net metering and feed-in tariffs, have also provided a stable foundation, enhancing the market’s robustness and investment opportunities. These factors have collectively contributed to the rapid growth of the solar sector.

Spain continues to dominate the Southern European solar PV landscape, with regions such as Andalusia and Castilla-La Mancha being key areas for solar projects. The dominance is due to high solar radiation levels, large expanses of land suitable for ground-mounted installations, and significant government support in terms of funding and incentives. Urban areas, particularly Madrid and Barcelona, have also seen rapid growth in rooftop solar installations, driven by both public and private sector investments.

Market Segmentation

By Product Type

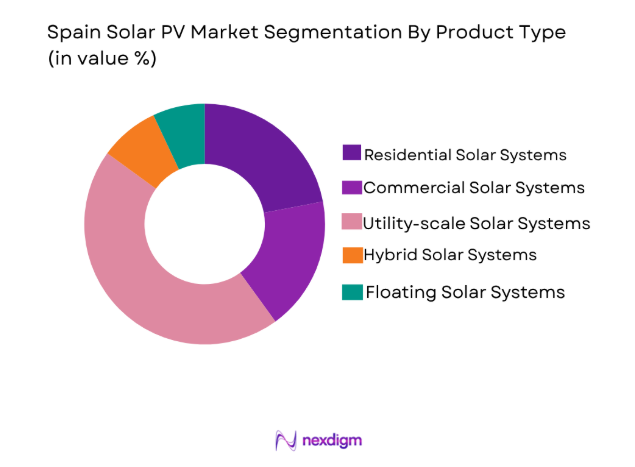

The Spain Solar PV market is segmented by product type into residential solar systems, commercial solar systems, utility-scale solar systems, hybrid solar systems, and floating solar systems. Recently, utility-scale solar systems have shown a dominant market share due to factors such as government policy support, increased renewable energy goals, and cost competitiveness compared to other energy sources. Large-scale projects benefit from economies of scale, improved technology, and robust financial incentives, making them attractive to both developers and investors.

By Platform Type

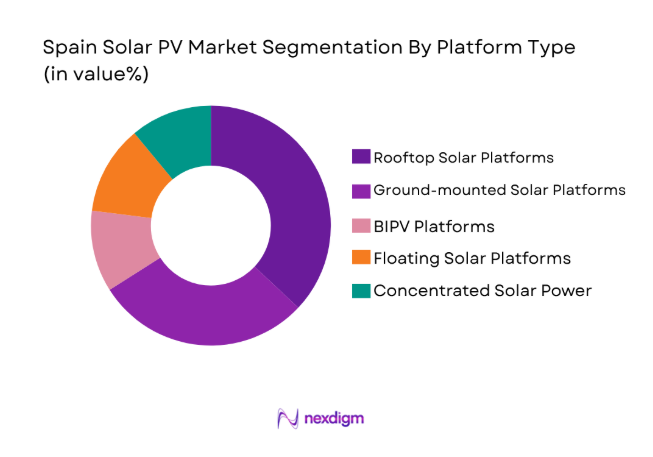

The Spain Solar PV market is also segmented by platform type, which includes rooftop solar platforms, ground-mounted solar platforms, BIPV (Building Integrated Photovoltaic) platforms, floating solar platforms, and concentrated solar power platforms. The rooftop solar platforms sub-segment has a dominant market share due to the growing trend of self-consumption and rising electricity prices. Additionally, there are many government initiatives encouraging rooftop solar installations, which further increases their adoption. Rooftop systems have become an easy and viable option for both residential and commercial sectors looking for decentralized energy solutions.

Competitive Landscape

The Spain Solar PV market has witnessed a mix of international and domestic players who play a crucial role in shaping the competitive landscape. There has been considerable consolidation, with major companies expanding their footprint through acquisitions and partnerships. Leading companies are investing in technological innovations to improve efficiency and reduce costs, further enhancing their market positioning. As Spain continues to promote clean energy, the influence of major players is likely to increase.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Key Market-specific Parameter |

| Iberdrola | 1992 | Spain | ~ | ~ | ~ | ~ | ~ |

| Acciona | 1997 | Spain | ~ | ~ | ~ | ~ | ~ |

| Siemens Gamesa | 1976 | Spain | ~ | ~ | ~ | ~ | ~ |

| First Solar | 1999 | USA | ~ | ~ | ~ | ~ | ~ |

| Enel Green Power | 2008 | Italy | ~ | ~ | ~ | ~ | ~ |

Spain Solar PV Market Analysis

Growth Drivers

Government Incentives and Policies

Government incentives and policies are critical to driving the growth of the Spain Solar PV market. The Spanish government has implemented several favorable policies, including tax benefits, feed-in tariffs, and subsidies, aimed at encouraging the adoption of renewable energy solutions. These policies have effectively lowered the capital expenditure required for solar power installations, making solar energy more accessible to both residential and commercial consumers. Additionally, Spain’s long-term energy targets for renewable energy, as part of its commitment to the European Union’s sustainability goals, have further strengthened the market’s growth potential. These targets encourage investments in solar power, both from domestic players and international investors. Moreover, the government has worked on simplifying permitting processes and offering financial incentives to developers, making it easier and more cost-effective to implement solar energy solutions. This continuous support from the government ensures a favorable environment for both existing and new players in the market, fueling continued expansion. Furthermore, the alignment of Spain’s renewable energy goals with broader EU directives ensures that the country will maintain its commitment to solar energy, providing stability to the market.

Technological Advancements in Solar PV

Technological advancements in solar PV are a major growth driver in the Spanish market. Recent innovations in solar panel efficiency, energy storage solutions, and system integration have made solar PV a more viable and cost-competitive energy source compared to traditional fossil fuels. For instance, bifacial solar panels that capture sunlight on both sides have enhanced energy yields, allowing more power to be generated from a smaller installation area. Additionally, energy storage systems have gained significant traction, enabling the storage of excess energy generated during the day for use at night or during cloudy days. This integration of energy storage has helped resolve the intermittency issue, which has been one of the key barriers to wider adoption of solar energy. As these technologies become more affordable and efficient, they significantly reduce the overall cost of solar PV ownership, making it more accessible for residential, commercial, and industrial consumers. The continued improvements in solar panel efficiency and storage solutions make the Spain Solar PV market increasingly attractive to both end-users and investors, offering a promising future for renewable energy expansion.

Market Challenges

High Initial Capital Costs

One of the significant challenges facing the Spain Solar PV market is the high initial capital cost associated with installing solar systems. While the cost of solar panels has dropped significantly in recent years, the installation, maintenance, and integration of energy storage systems still require substantial upfront investments. This is a particular challenge for residential users and small businesses that may not have the financial resources to cover these costs. Though government subsidies and tax credits do alleviate some of the initial financial burden, they do not fully address the high capital requirements. Additionally, financing options for small and medium-sized enterprises (SMEs) are limited, making it difficult for these businesses to invest in solar energy despite its long-term benefits. The payback period for these solar systems can also be lengthy, which diminishes the financial appeal for certain consumers. Although solar energy provides substantial savings in the long run, the high upfront costs continue to be a major deterrent for a segment of the market, particularly in a price-sensitive environment.

Regulatory and Policy Uncertainties

Regulatory and policy uncertainties present another key challenge to the Spain Solar PV market. While the Spanish government has introduced several favorable renewable energy policies, including subsidies, incentives, and feed-in tariffs, the potential for policy changes remains a significant risk. Shifts in government leadership or changes to EU regulations can lead to modifications or even reductions in support for renewable energy projects, creating an unstable investment climate. The lack of policy consistency, especially regarding subsidies and tax incentives, leaves developers and investors uncertain about the long-term prospects of their investments. This uncertainty could cause delays in the planning and execution of solar projects, and may discourage potential investors from committing to large-scale projects. Furthermore, variations in local regulations and permitting requirements across different regions of Spain add an additional layer of complexity for developers. Without a stable regulatory framework, market participants may hesitate to invest in the solar sector, limiting growth opportunities.

Opportunities

Expansion of Hybrid Solar Systems

Hybrid solar systems, which combine solar PV with other energy sources such as wind or battery storage, represent a major growth opportunity for the Spain Solar PV market. These hybrid systems offer higher energy reliability and efficiency, overcoming the intermittency issues typically associated with solar energy. The integration of battery storage systems allows consumers to store excess energy generated during the day for use during nighttime or cloudy periods, providing a continuous power supply. This makes hybrid systems ideal for both off-grid solutions and those seeking to supplement their grid connection with renewable energy. Furthermore, Spain’s government has expressed strong support for renewable energy integration into the national grid, creating a favorable environment for hybrid solar solutions. As technological advancements continue to drive down the costs of hybrid systems and energy storage solutions, these systems are expected to become a dominant part of the Spanish solar landscape. The growing demand for energy independence, particularly in rural and remote areas, will likely accelerate the adoption of hybrid solar systems. These systems are positioned to play a central role in achieving Spain’s renewable energy targets, offering substantial growth potential for both developers and investors in the coming years.

Emerging Demand for Floating Solar Solutions

Floating solar solutions are rapidly gaining popularity in Spain, especially in areas where land availability for ground-mounted solar projects is limited. These systems are installed on bodies of water, such as lakes and reservoirs, offering a unique solution to the land scarcity issue that has affected traditional solar installations. Floating solar systems also benefit from the natural cooling effect of water, which improves their efficiency and energy output. As Spain continues to explore innovative ways to expand its renewable energy capacity, floating solar presents a promising opportunity for market growth. With large expanses of water bodies in coastal regions and inland reservoirs, floating solar systems have the potential to scale up rapidly, especially in areas where land-based solar projects are not feasible. The ability to deploy floating solar systems on water bodies without occupying valuable land space makes them an ideal solution for regions looking to meet their renewable energy goals. Furthermore, technological advancements and lower installation costs will likely make floating solar increasingly attractive, fostering greater adoption of this innovative energy solution. The growing interest in floating solar solutions offers significant opportunities for market expansion in Spain.

Future Outlook

The Spain Solar PV market is expected to see continued growth in the coming years, driven by increasing government support, technological advancements, and expanding commercial and residential adoption. Regulatory frameworks are likely to evolve to facilitate the further integration of solar energy into the national grid, with a greater focus on energy storage solutions and hybrid systems. As the costs of solar panels and battery storage continue to fall, the market is anticipated to become more accessible to a wider range of consumers and businesses. This will enable Spain to remain a leader in Europe’s renewable energy transition.

Major Players

- Iberdrola

- Acciona

- Siemens Gamesa

- First Solar

- Enel Green Power

- SunPower

- Enphase Energy

- JinkoSolar

- Trina Solar

- Canadian Solar

- LONGi Solar

- Risen Energy

- JA Solar

- Q CELLS

- Solaria

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Utility companies

- Large commercial enterprises

- Residential energy consumers

- Energy technology developers

- Renewable energy project developers

Research Methodology

Step 1: Identification of Key Variables

Key variables impacting the Spain Solar PV market, including government policies, technological advancements, and market demand patterns, are identified and assessed.

Step 2: Market Analysis and Construction

A detailed analysis of the market is conducted to understand its dynamics, segmentation, and drivers, followed by market construction based on available data.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding market trends, growth drivers, and challenges are validated with insights from industry experts and key stakeholders in the solar energy field.

Step 4: Research Synthesis and Final Output

The data and insights gathered are synthesized to produce the final report, ensuring accuracy and actionable conclusions for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government incentives and subsidies for renewable energy

Technological advancements in solar PV technology

Growing demand for clean and sustainable energy - Market Challenges

High capital investment for large-scale installations

Intermittency of solar energy generation

Regulatory and policy uncertainties - Market Opportunities

Increasing adoption of hybrid solar systems

Expansion of solar PV in commercial and industrial sectors

Growing interest in off-grid solar solutions - Trends

Integration of energy storage systems with solar PV

Rise of innovative financing models for solar PV installations - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Residential Solar Systems

Commercial Solar Systems

Utility-scale Solar Systems

Hybrid Solar Systems

Floating Solar Systems - By Platform Type (In Value%)

Rooftop Solar Platforms

Ground-mounted Solar Platforms

BIPV (Building Integrated Photovoltaic) Platforms

Floating Solar Platforms

Concentrated Solar Power Platforms - By Fitment Type (In Value%)

On-grid Solar Systems

Off-grid Solar Systems

Hybrid Solar Systems

Modular Solar Systems - By End User Segment (In Value%)

Residential

Commercial

Industrial

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, End User Segment, Procurement Channel, System Complexity Tier, Fitment Type, Installed Units)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Iberdrola

Acciona

Siemens Gamesa

First Solar

Enel Green Power

SunPower

Enphase Energy

JinkoSolar

Trina Solar

Canadian Solar

LONGi Solar

Risen Energy

JA Solar

Q CELLS

Solaria

- Increase in demand from residential sectors

- Commercial sector adoption of large-scale solar PV

- Industrial sector looking for cost-effective energy solutions

- Government and policy-driven demand for solar solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now