Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Spain telemedicine market is valued at approximately USD ~ billion based on a recent historical assessment. The market is driven by factors such as the increasing demand for accessible healthcare, especially in rural areas, the adoption of digital health technologies, and the rising focus on reducing healthcare costs. Additionally, the Spanish government’s support for digital health solutions and the growing adoption of telemedicine during the COVID-19 pandemic have further propelled the market’s expansion.

Cities such as Madrid, Barcelona, and Valencia are the dominant players in Spain’s telemedicine market, benefiting from advanced healthcare infrastructure and high adoption rates of digital health technologies. Madrid, as the capital, has the highest concentration of hospitals and clinics implementing telemedicine services. Barcelona, with its focus on health tech startups and innovation, is also a significant hub for telemedicine. Valencia follows closely with regional investments aimed at improving healthcare access through digital solutions, making these cities key contributors to Spain’s telemedicine market.

Market Segmentation

By Service Type

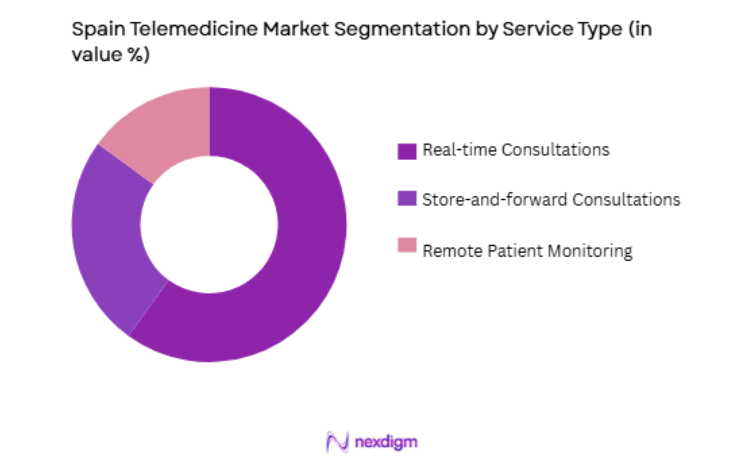

Spain’s telemedicine market is segmented by service type into real-time consultations, store-and-forward consultations, and remote patient monitoring. Recently, real-time consultations have dominated the market share due to the increasing demand for virtual healthcare services. Real-time consultations, such as video calls between patients and healthcare professionals, have become widely accepted due to the convenience they offer. The growing acceptance of telemedicine by both healthcare providers and patients, combined with the flexibility of real-time consultations, has led to a surge in their adoption. These consultations are especially beneficial in rural areas where access to healthcare services is limited. Additionally, the COVID-19 pandemic accelerated the adoption of these services, which continue to thrive in Spain’s digital health landscape.

By End-User

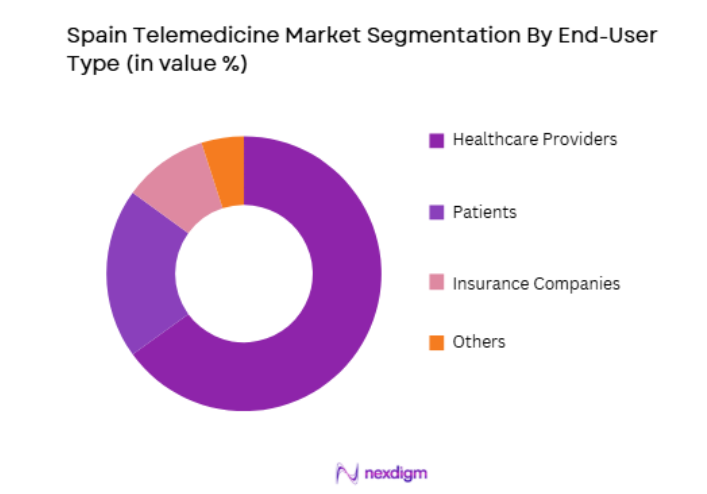

Spain’s telemedicine market is segmented by end-user into healthcare providers, patients, insurance companies, and others. Recently, healthcare providers have dominated the market share due to their increasing adoption of telemedicine platforms for patient consultations, diagnosis, and follow-up care. Hospitals, private clinics, and general practitioners are integrating telemedicine solutions into their daily operations to reduce patient wait times, increase access to care, and optimize their workflow. Spain’s well-established public healthcare system, combined with the growing demand for telemedicine in private healthcare settings, has further contributed to the dominance of healthcare providers in the telemedicine market. As more healthcare providers invest in telemedicine infrastructure, this segment will continue to expand in the coming years.

Competitive Landscape

The competitive landscape of Spain’s telemedicine market is characterized by a combination of established healthcare providers and technology companies offering telemedicine solutions. Large multinational companies are entering the market through strategic partnerships with healthcare institutions to expand their service offerings. Furthermore, Spain has seen an increase in local startups that are developing innovative telemedicine platforms to meet the specific needs of Spanish patients and healthcare providers. The market is becoming more competitive, with companies focusing on providing user-friendly, cost-effective telemedicine solutions, as well as expanding their presence in underserved regions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Teladoc Health | 2002 | New York, USA | ~ | ~ | ~ | ~ | ~ |

| DKV Seguros | 1999 | Zaragoza, Spain | ~ | ~ | ~ | ~ | ~ |

| Sanitas | 1954 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| Docplanner | 2012 | Barcelona, Spain | ~ | ~ | ~ | ~ | ~ |

| Vithas | 1993 | Valencia, Spain | ~ | ~ | ~ | ~ | ~ |

Spain Telemedicine Market Analysis

Growth Drivers

Government Support for Telemedicine

Government support for telemedicine is a significant growth driver in Spain’s telemedicine market. The Spanish government has been actively promoting digital health solutions, including telemedicine, through policies such as the Digital Health Strategy. These initiatives aim to modernize Spain’s healthcare system by integrating telemedicine into both public and private healthcare settings. The government has introduced several funding programs to encourage healthcare providers to adopt telemedicine platforms, making it more accessible to rural areas with limited healthcare access. Additionally, Spain’s National Health System (SNS) has been working to integrate telemedicine into its routine services, improving efficiency and accessibility for patients. The government’s commitment to digital health solutions is expected to continue supporting the growth of the telemedicine market, particularly as more healthcare institutions incorporate these technologies into their services.

Rising Demand for Convenient Healthcare Solutions

The rising demand for convenient healthcare solutions is another key growth driver for Spain’s telemedicine market. With the increasing pressure on healthcare systems to provide accessible care, telemedicine offers a solution to meet the growing demand for healthcare services. Telemedicine allows patients to receive consultations from healthcare professionals without the need to travel, saving both time and money. This convenience is particularly important for patients living in rural areas, where access to healthcare providers is limited. Additionally, telemedicine has gained significant traction during the COVID-19 pandemic, with patients and healthcare providers turning to virtual consultations to maintain continuity of care while minimizing exposure to the virus. As patients and healthcare providers continue to recognize the benefits of telemedicine, the demand for these services is expected to grow, further driving market expansion.

Market Challenges

Regulatory and Legal Barriers

One of the significant challenges facing Spain’s telemedicine market is navigating the regulatory and legal barriers associated with telehealth services. While Spain has made strides in integrating telemedicine into its healthcare system, the regulatory framework remains complex and varies by region. Healthcare providers must ensure that they comply with privacy and data protection regulations, such as the General Data Protection Regulation (GDPR), when offering telemedicine services. Furthermore, telemedicine platforms must meet certain standards to be approved by regulatory bodies, which can result in delays in the deployment of new technologies. The lack of a standardized regulatory framework for telemedicine services across Spain can also lead to confusion for healthcare providers and patients alike, hindering the widespread adoption of telemedicine. Overcoming these regulatory challenges will be essential for the continued growth of Spain’s telemedicine market.

Technology Integration and Adoption Challenges

Another challenge for the growth of Spain’s telemedicine market is the technology integration and adoption challenges faced by healthcare providers. While telemedicine technologies are increasingly available, many healthcare providers, particularly smaller clinics and private practices, may struggle with integrating telemedicine platforms into their existing systems. These institutions may lack the necessary infrastructure, such as high-speed internet connections or the technical expertise required to operate telemedicine platforms effectively. Furthermore, healthcare professionals may be hesitant to adopt telemedicine services due to concerns over the effectiveness of remote consultations or unfamiliarity with the technology. Addressing these challenges will require ongoing investments in infrastructure, training, and support to ensure that healthcare providers can seamlessly integrate telemedicine into their services.

Opportunities

Expansion of Telemedicine Services to Rural Areas

The expansion of telemedicine services to rural and underserved areas presents a significant opportunity for Spain’s telemedicine market. Rural areas in Spain often face challenges in accessing healthcare due to a lack of medical professionals and healthcare facilities. Telemedicine offers an effective solution to these issues, allowing patients to consult with healthcare providers remotely. The Spanish government has recognized the need to expand healthcare services in rural regions and has been promoting telemedicine as a way to address healthcare access disparities. With the growing demand for healthcare services in rural areas and the government’s support for digital health initiatives, there is a significant opportunity for telemedicine providers to expand their services to these regions, improving access to care and driving market growth.

Integration with Other Digital Health Technologies

The integration of telemedicine with other digital health technologies presents another opportunity for Spain’s telemedicine market. As digital health continues to evolve, there is a growing trend toward integrating telemedicine platforms with electronic health records (EHR), remote patient monitoring systems, and AI-driven diagnostic tools. These integrations enable healthcare providers to offer more comprehensive and personalized care, improving patient outcomes and operational efficiency. For example, telemedicine consultations can be seamlessly integrated with EHR systems to provide healthcare professionals with real-time access to patient medical histories. The integration of remote monitoring systems with telemedicine platforms can also allow for continuous care, particularly for patients with chronic conditions. As the healthcare industry embraces these digital health solutions, there will be growing opportunities for telemedicine providers to expand their offerings and improve the quality of care.

Future Outlook

The future outlook for Spain’s telemedicine market is promising, with steady growth expected in the coming years. The increasing demand for accessible healthcare, combined with government support for digital health solutions, will continue to drive the adoption of telemedicine across Spain. The integration of telemedicine with other digital health technologies, such as EHR systems and remote patient monitoring, will further enhance the market’s growth. Additionally, as Spain’s healthcare system continues to evolve and adapt to the changing needs of its population, telemedicine will play an increasingly important role in providing high-quality, accessible care. With the ongoing push for healthcare digitalization, Spain’s telemedicine market is poised for sustained expansion.

Major Players

- Teladoc Health

- DKV Seguros

- Sanitas

- Docplanner

- Vithas

- Médicos Sin Fronteras

- Doctoralia

- Babylon Health

- Doctor on Demand

- MyDoc

- Mediquo

- Mobile Doctors

- Aetna International

- Bupa Global

- SaludOnNet

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Hospitals and clinics

- Pharmaceutical companies

- Medical device manufacturers

- Insurance providers

- Medical research organizations

Research Methodology

Step 1: Identification of Key Variables

Key variables such as market size, growth drivers, technological trends, and challenges are identified through both primary and secondary research methods.

Step 2: Market Analysis and Construction

Comprehensive data is gathered, analyzed, and synthesized using statistical models to build a detailed market forecast.

Step 3: Hypothesis Validation and Expert Consultation

Insights are validated through consultations with industry experts to ensure the reliability of the findings.

Step 4: Research Synthesis and Final Output

The final report synthesizes all collected data, providing a comprehensive analysis of Spain’s telemedicine market, including growth drivers, challenges, and opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Support for Telemedicine Initiatives

Rising Demand for Remote Healthcare Services

Technological Advancements in Telehealth - Market Challenges

High Initial Investment in Infrastructure

Data Security and Privacy Issues

Lack of Telemedicine Regulations - Market Opportunities

Expanding Telemedicine for Mental Health

Telemedicine Adoption in Rural Areas

Growing Use of AI and Machine Learning in Telehealth - Trends

Increase in Adoption of Virtual Healthcare Services

Integration of Wearables in Telemedicine - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Telemedicine Platforms

Remote Patient Monitoring Systems

Teleconsultation Services

Telehealth Devices

Healthcare Analytics Solutions - By Platform Type (In Value%)

Cloud-based Platforms

Mobile Platforms

Web-based Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Integrated Solutions - By End User Segment (In Value%)

Hospitals

Clinics

Healthcare Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technological Integration, Patient Experience, Market Reach, Data Security, Compliance with Healthcare Regulations)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Teladoc Health

Amwell

Doximity

Cerner Corporation

GE Healthcare

Philips Healthcare

Medtronic

HealthTap

Doctor On Demand

Lifecare

SnapMD

Vivify Health

Doctor Anywhere

Maple

Lifecare

- Hospitals Increasing Telemedicine Services

- Clinics Expanding Teleconsultation Offerings

- Healthcare Providers Adopting Virtual Health Models

- Patients Increasingly Seeking Remote Consultations

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now