Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Thailand Advanced Materials market reached approximately USD ~ driven by strong demand from automotive manufacturing, electronics production, aerospace components, and construction industries. Advanced materials including high performance polymers, carbon composites, specialty metals, and nanomaterials increasingly support high precision manufacturing and lightweight product design. Government supported industrial innovation programs and strong electronics manufacturing clusters encourage the integration of advanced materials across industrial supply chains, accelerating material science adoption throughout Thailand’s manufacturing ecosystem.

Advanced materials consumption across Thailand is concentrated within major industrial and manufacturing hubs including Bangkok, Chonburi, and Rayong due to their extensive electronics and automotive production infrastructure. These regions host large industrial estates and export manufacturing zones where advanced materials are widely used in semiconductor packaging, automotive lightweight components, and precision engineering applications. Industrial clusters within the Eastern Economic Corridor also attract multinational technology manufacturers that integrate high performance materials within advanced manufacturing processes, strengthening Thailand’s role within global electronics and automotive supply chains.

Market Segmentation

By Material Type

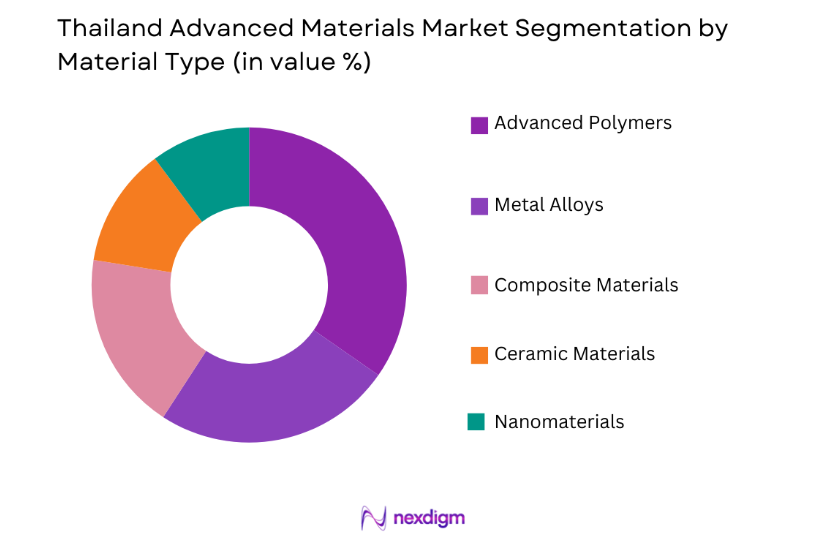

Thailand Advanced Materials market is segmented by material type into advanced polymers, metal alloys, ceramic materials, composite materials, and nanomaterials. Recently, advanced polymers have a dominant market share due to factors such as demand patterns, infrastructure availability, and strong adoption within electronics manufacturing and automotive production industries. Advanced polymers provide lightweight durability, corrosion resistance, and high thermal stability which makes them suitable for electronic components, automotive parts, and packaging applications. Thailand’s strong electronics manufacturing ecosystem requires large volumes of engineering plastics and polymer composites used in semiconductor packaging and electrical insulation materials. Automotive manufacturers also integrate advanced polymers to reduce vehicle weight and improve fuel efficiency. Continuous expansion of consumer electronics production facilities further strengthens the demand for advanced polymer materials across Thailand’s industrial manufacturing ecosystem.

By End Use Industry

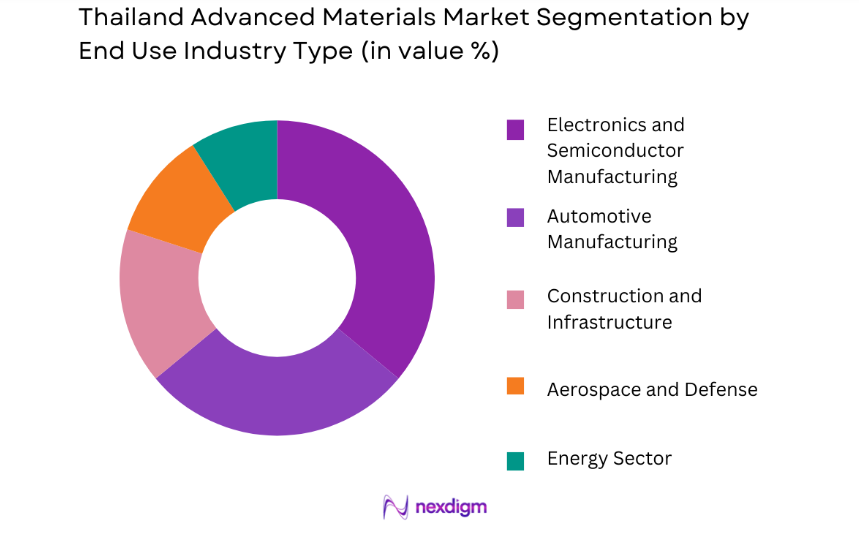

Thailand Advanced Materials market is segmented by end use industry into automotive manufacturing, electronics and semiconductor manufacturing, construction and infrastructure, aerospace and defense, and energy sector. Recently, electronics and semiconductor manufacturing has a dominant market share due to factors such as industrial infrastructure expansion, export manufacturing demand, and strong presence of multinational electronics manufacturers. Thailand operates as a major electronics production hub within Southeast Asia where advanced materials support semiconductor packaging, circuit board manufacturing, and electronic component assembly. High performance materials such as conductive polymers, specialty ceramics, and nanomaterials are widely used in electronic devices and integrated circuit production processes. Continuous expansion of electronics manufacturing clusters across Thailand strengthens the demand for advanced materials supporting precision manufacturing and electronic component reliability.

Competitive Landscape

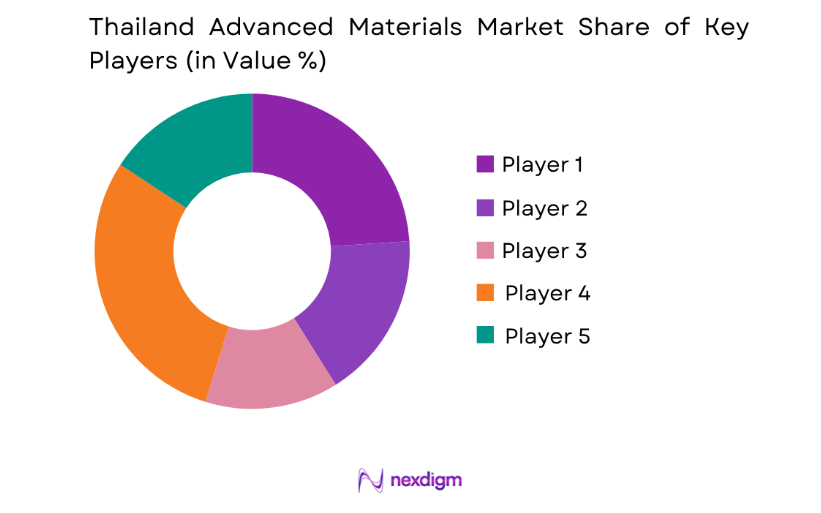

The Thailand Advanced Materials market is characterized by the presence of multinational chemical manufacturers and specialized materials producers supplying advanced polymers, specialty metals, and high performance composites to electronics and automotive industries. Global materials companies collaborate with local manufacturers to develop specialized materials used in semiconductor packaging, automotive lightweight structures, and industrial engineering applications. Market competition is influenced by technological innovation, production capacity, and strong integration with Thailand’s export manufacturing supply chains.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Materials Specialization |

| BASF SE | 1865 | Germany | ~ | ~ | ~ | ~ | ~ |

| Dow Inc | 1897 | USA | ~ | ~ | ~ | ~ | ~ |

| Toray Industries | 1926 | Japan | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Chemical Group | 1933 | Japan | ~ | ~ | ~ | ~ | ~ |

| Covestro AG | 2015 | Germany | ~ | ~ | ~ | ~ | ~ |

Thailand Advanced Materials Market Analysis

Growth Drivers

Expansion of Electronics Manufacturing and Semiconductor Packaging Industry

Thailand’s rapidly expanding electronics manufacturing ecosystem significantly increases demand for advanced materials used in semiconductor packaging, circuit board manufacturing, and electronic component assembly operations. Electronics manufacturing facilities require high purity polymers, advanced ceramic substrates, and specialized conductive materials capable of supporting precision manufacturing environments. Semiconductor packaging processes rely heavily on advanced materials capable of providing thermal stability, electrical insulation, and mechanical durability within compact electronic devices. Thailand hosts numerous multinational electronics companies operating production facilities that manufacture integrated circuits, printed circuit boards, and consumer electronic devices for global export markets. These production facilities require continuous supply of advanced materials that support microelectronics fabrication processes and ensure long term product reliability. Advanced materials therefore play a critical role in supporting Thailand’s electronics manufacturing competitiveness within global technology supply chains. As electronics production continues expanding across industrial clusters within the Eastern Economic Corridor, demand for advanced materials used in semiconductor packaging and electronic device manufacturing continues increasing significantly across the industrial materials ecosystem.

Automotive Lightweighting and Electric Vehicle Manufacturing Materials Demand

Thailand’s position as one of Southeast Asia’s largest automotive manufacturing hubs significantly strengthens demand for advanced materials used in vehicle production and lightweight engineering applications. Automotive manufacturers increasingly integrate lightweight materials including carbon composites, aluminum alloys, and advanced polymers in order to improve vehicle efficiency and structural performance. These materials help reduce vehicle weight while maintaining mechanical strength and safety standards required for modern transportation systems. Electric vehicle manufacturing further accelerates demand for advanced materials used in battery components, thermal management systems, and lightweight structural components. Advanced materials such as high performance polymers and specialty alloys support battery enclosure structures, insulation systems, and electronic control modules within electric vehicles. Automotive manufacturers operating across Thailand’s industrial zones therefore require continuous supply of specialized materials capable of supporting advanced vehicle design and manufacturing innovation. As electric mobility adoption expands across regional automotive markets, Thailand’s automotive industry will increasingly depend on advanced materials supporting next generation vehicle manufacturing technologies.

Market Challenges

Limited Domestic Production Capacity for Specialized Advanced Materials

Thailand’s advanced materials market faces challenges due to limited domestic manufacturing capacity for certain specialized materials including high purity semiconductor materials, advanced nanomaterials, and aerospace grade composites. Many of these materials require sophisticated production technologies and highly specialized chemical processing capabilities that remain concentrated within developed industrial economies. Thai manufacturers therefore depend significantly on imported advanced materials to support high precision manufacturing operations across electronics and automotive sectors. Import dependency exposes the supply chain to fluctuations in international trade conditions, logistics disruptions, and raw material price volatility. Limited domestic research infrastructure for certain advanced materials technologies also restricts local production capabilities. Although Thailand possesses strong manufacturing capabilities, development of specialized materials production requires significant long term investment in research laboratories, chemical engineering expertise, and advanced processing facilities. Without expanding domestic materials innovation capacity, Thailand may continue relying heavily on international suppliers for critical advanced materials used in high technology manufacturing sectors.

High Research and Development Costs for Advanced Material Innovation

Developing advanced materials requires extensive research and development investment involving complex chemical engineering processes, laboratory experimentation, and materials testing programs. Advanced materials such as nanomaterials, high temperature ceramics, and aerospace grade composites require years of scientific research before commercial production becomes feasible. Companies operating within Thailand’s materials sector often face financial challenges when investing in long term research programs without immediate commercial returns. Establishing research laboratories equipped with advanced analytical instruments also requires substantial capital expenditure. Skilled materials scientists and chemical engineers are required to design new materials with improved performance characteristics and industrial compatibility. Recruiting and training specialized research talent further increases operational costs for materials manufacturers. Smaller materials companies may therefore face difficulties competing with large multinational chemical companies possessing significant research resources. These high innovation costs can slow the development of new advanced materials technologies within Thailand’s industrial materials ecosystem.

Opportunities

Development of Advanced Materials Research Centers within Industrial Innovation Zones

Thailand’s government continues encouraging industrial innovation through research programs and technology development initiatives supporting advanced materials science. Establishing dedicated research centers for materials engineering within industrial technology parks creates new opportunities for collaboration between universities, chemical companies, and manufacturing industries. These research facilities enable scientists to develop advanced materials including nanostructured materials, specialty polymers, and high performance composites suitable for industrial manufacturing applications. Collaborative research programs accelerate material innovation and facilitate commercialization of newly developed materials technologies. Government supported innovation zones within Thailand’s industrial corridors provide financial incentives encouraging companies to invest in advanced materials research. These research programs strengthen Thailand’s capability to produce specialized materials required by electronics, automotive, and aerospace manufacturing sectors. Expanding materials research infrastructure therefore creates significant opportunities for local innovation and technology development within the advanced materials industry.

Growing Demand for Sustainable and Eco Friendly Advanced Materials

Industrial sectors across Thailand increasingly prioritize environmentally sustainable manufacturing practices that encourage the development of eco friendly advanced materials. Manufacturers seek materials capable of reducing carbon emissions, improving energy efficiency, and enabling recyclable product design. Bio based polymers, lightweight composite materials, and recyclable engineering plastics are gaining attention across automotive, electronics, and construction industries. Sustainable materials also support regulatory compliance as governments introduce environmental standards aimed at reducing industrial pollution. Companies that develop environmentally friendly advanced materials gain competitive advantages as manufacturers seek greener supply chain solutions. Research into biodegradable polymers, recyclable composite materials, and low emission production processes therefore represents a major growth opportunity for the advanced materials market. As sustainability initiatives expand across industrial sectors, demand for environmentally responsible advanced materials will continue increasing across Thailand’s manufacturing ecosystem.

Future Outlook

Thailand’s advanced materials market is expected to expand steadily as electronics manufacturing, automotive production, and industrial innovation continue strengthening across the country. Demand for high performance polymers, composite materials, and nanomaterials will increase as manufacturers adopt advanced production technologies. Government support for industrial innovation zones and technology development initiatives will further encourage research and commercialization of new materials. Growing demand for lightweight, sustainable, and high performance materials will support long term growth of the advanced materials ecosystem.

Major Players

- BASF SE

- Dow Inc

- Toray Industries

- Mitsubishi Chemical Group

- Covestro AG

- SABIC

- Solvay SA

- DuPont

- LG Chem

- Arkema SA

- Sumitomo Chemical

- Asahi Kasei Corporation

- Teijin Limited

- Lanxess AG

- Evonik Industries

Key Target Audience

- Electronics Manufacturing Companies

- Automotive Manufacturing Companies

- Aerospace Component Manufacturers

- Construction Material Manufacturers

- Energy Equipment Manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key industry sectors including electronics manufacturing, automotive production, aerospace engineering, and construction infrastructure were analyzed to identify demand drivers influencing advanced materials adoption across Thailand’s industrial economy.

Step 2: Market Analysis and Construction

Industry data regarding advanced materials consumption patterns, manufacturing infrastructure, and technology adoption trends were evaluated to construct the market framework and understand the structural dynamics influencing materials demand.

Step 3: Hypothesis Validation and Expert Consultation

Consultations with materials scientists, industrial manufacturers, and supply chain experts helped validate assumptions regarding advanced materials usage across electronics, automotive, and industrial engineering sectors.

Step 4: Research Synthesis and Final Output

All research insights were consolidated to generate the final analytical framework outlining market structure, competitive landscape, technological trends, and long term growth opportunities within the Thailand Advanced Materials market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of Automotive and Electric Vehicle Manufacturing in Thailand

Increasing Semiconductor and Electronics Manufacturing Activities

Growing Demand for High Performance Materials in Renewable Energy Infrastructure - Market Challenges

High Production Costs Associated with Advanced Material Processing

Limited Domestic Production of Specialized Raw Materials

Dependence on Imported Advanced Material Processing Technologies - Market Opportunities

Expansion of Electric Vehicle Supply Chains Requiring Lightweight Materials

Growing Demand for Nanomaterials in Electronics and Semiconductor Manufacturing

Development of Advanced Composite Materials for Aerospace and Aviation Industries - Trends

Increasing Integration of Nanotechnology in High Performance Industrial Materials

Growing Adoption of Advanced Composites in Automotive Lightweight Engineering - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Advanced Composite Materials

High Performance Polymers

Advanced Ceramics

Nanomaterials

Metal Matrix Composites - By Platform Type (In Value%)

Automotive and Electric Vehicle Platforms

Electronics and Semiconductor Platforms

Aerospace and Aviation Platforms

Energy and Power Infrastructure Platforms - By Fitment Type (In Value%)

Structural Components

Thermal Management Systems

Electronic and Semiconductor Components

Industrial Equipment Components - By End User Segment (In Value%)

Automotive and Transportation Industry

Electronics and Semiconductor Industry

Energy and Industrial Manufacturing

- Market Share Analysis

- Cross Comparison Parameters (Material Technology Portfolio, Manufacturing Capability, Application Industry Coverage, Supply Chain Integration, Pricing Structure, Innovation Capability, Regional Distribution Network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Toray Industries

Hexcel Corporation

Solvay SA

Teijin Limited

SGL Carbon SE

3M Company

DuPont de Nemours

Dow Inc

BASF SE

Saint Gobain

Huntsman Corporation

Mitsubishi Chemical Group

Evonik Industries

Arkema SA

SCG Chemicals

- Automotive Manufacturers Utilizing Lightweight Materials to Improve Vehicle Efficiency

- Electronics Producers Deploying Nanomaterials for Semiconductor and Device Manufacturing

- Energy Companies Utilizing Advanced Materials in Renewable Power Infrastructure

- Industrial Equipment Manufacturers Using High Performance Materials for Durability

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now