Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Thailand AI infrastructure market demonstrates expanding investment in high performance computing, cloud data centers, and AI-optimized semiconductor capacity, supported by national digital economy initiatives and regional hyperscale expansion. Based on a recent historical assessment, Thailand’s data center and AI infrastructure related capital expenditure exceeded USD ~ billion, with strong contributions from hyperscale cloud deployments and government-supported digital infrastructure programs reported by Thailand Board of Investment and industry infrastructure disclosures. Demand is primarily driven by enterprise AI adoption, cloud localization requirements, and regional digital platform growth.

Bangkok dominates AI infrastructure deployment due to concentration of hyperscale facilities, connectivity hubs, and enterprise headquarters, while Eastern Economic Corridor zones attract new capacity through industrial digitization incentives and power availability advantages. Regional cloud operators from Singapore, China, and the United States expand infrastructure presence in Thailand to serve mainland Southeast Asia demand, benefiting from strategic location, subsea cable connectivity expansion, and government data localization support encouraging domestic AI compute infrastructure scaling.

Market Segmentation

By Product Type

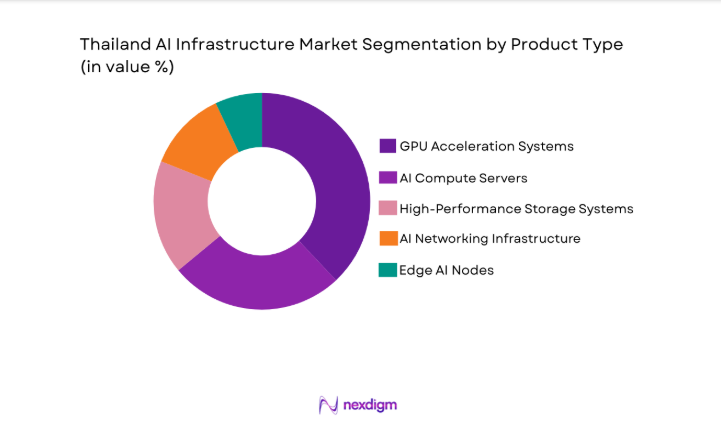

Thailand AI Infrastructure market is segmented by product type into GPU Acceleration Systems, AI Compute Servers, High-Performance Storage Systems, AI Networking Infrastructure, and Edge AI Nodes. Recently, GPU Acceleration Systems has a dominant market share due to factors such as enterprise AI training workloads, hyperscale cloud GPU cluster deployments, deep learning adoption in finance and manufacturing, and demand for high-performance parallel computing environments. Major cloud operators and telecom firms prioritize GPU-dense architecture for generative AI, computer vision, and predictive analytics use cases, while government AI initiatives support advanced computing infrastructure investments. Availability of vendor ecosystems and software optimization frameworks also reinforces GPU-centric infrastructure preference across enterprise and cloud deployments.

By Platform Type

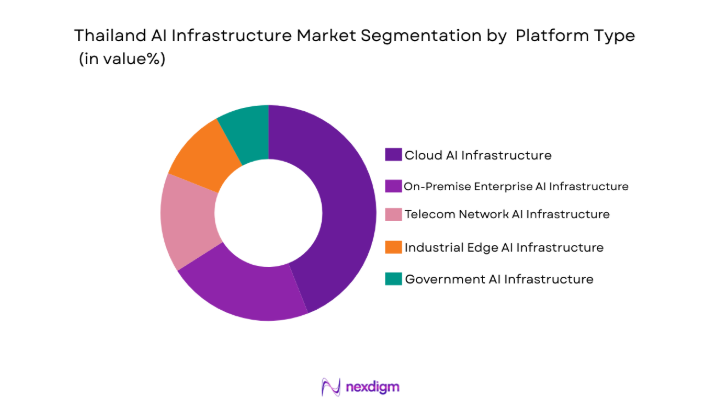

Thailand AI Infrastructure market is segmented by platform type into Cloud AI Infrastructure, On-Premise Enterprise AI Infrastructure, Telecom Network AI Infrastructure, Industrial Edge AI Infrastructure, and Government AI Infrastructure. Recently, Cloud AI Infrastructure has a dominant market share due to factors such as rapid enterprise migration toward AI-as-a-service platforms, hyperscale GPU cluster deployments, scalable compute accessibility, and reduced capital expenditure requirements for organizations adopting artificial intelligence capabilities. Cloud providers continue expanding regional AI availability zones and managed AI stacks, while enterprises prioritize flexible consumption models and integrated AI development environments, reinforcing cloud-centric infrastructure adoption across industries.

Competitive Landscape

Thailand AI infrastructure market shows moderate consolidation with global semiconductor and cloud vendors partnering local telecom and data center operators to expand AI compute capacity. International hyperscale providers dominate GPU clusters and AI cloud platforms, while regional data center firms enable colocation and enterprise AI hosting. Hardware vendors supply accelerators, servers, and networking systems through channel partnerships. Market competition increasingly centers on performance density, energy efficiency, AI stack integration, and regional availability zones.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AI Accelerator Portfolio |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Huawei | 1987 | China | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| HPE | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

| Supermicro | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

Thailand AI Infrastructure Market Analysis

Growth Drivers

National digital economy and AI policy investment acceleration

Thailand’s coordinated digital economy strategy and AI development roadmap are catalyzing sustained investment in compute infrastructure, data centers, and AI-optimized hardware across public and private sectors, creating structural demand expansion for domestic AI infrastructure deployment at scale. Government investment incentives administered through Thailand Board of Investment programs reduce capital expenditure burdens for hyperscale operators and semiconductor infrastructure investors while encouraging localization of cloud services and AI workloads within national borders. Expansion of smart city programs, digital public services, and AI-enabled governance platforms requires sovereign compute capacity, increasing procurement of GPU clusters, AI servers, and secure data facilities. Public sector demand further stimulates telecom operators and utilities to modernize fiber networks and power infrastructure supporting high-density AI compute environments. National research and innovation initiatives in healthcare AI, agriculture analytics, and manufacturing automation require local high performance computing clusters and AI training infrastructure. Policy emphasis on data sovereignty and cybersecurity strengthens requirements for domestic data storage and processing, accelerating hyperscale region establishment in Thailand rather than reliance on offshore capacity. Government co-investment in digital infrastructure zones such as the Eastern Economic Corridor provides land, energy access, and regulatory facilitation supporting rapid facility deployment. Combined policy measures create predictable demand visibility for infrastructure vendors and operators, encouraging long-term capacity expansion aligned with national AI adoption objectives.

Enterprise AI adoption and regional cloud localization demand

Rapid adoption of artificial intelligence across Thai enterprises in finance, retail, manufacturing, logistics, and telecommunications is creating escalating requirements for scalable compute infrastructure capable of supporting model training, inference, and analytics workloads within national latency and compliance constraints. Multinational corporations operating in Thailand increasingly require localized AI cloud regions to meet data residency policies and performance expectations, driving hyperscale providers to expand GPU-enabled infrastructure domestically. Growth of digital commerce platforms, fintech services, and real-time analytics applications generates continuous demand for high-performance storage and networking integrated with AI servers and accelerators. Manufacturing sector digitization initiatives within industrial zones require edge AI processing and centralized training clusters, expanding hybrid infrastructure deployment. Telecom operators deploying 5G and network automation platforms adopt AI infrastructure to optimize traffic management and predictive maintenance, further increasing enterprise demand. Regional businesses serving mainland Southeast Asia use Thailand as an operational hub, strengthening cross-border cloud and AI service requirements hosted locally. Increasing availability of AI software ecosystems and managed services reduces adoption barriers for enterprises, translating application demand into infrastructure investment. Strong growth of startup ecosystems in AI applications also stimulates consumption of cloud GPU resources and shared compute facilities, reinforcing sustained infrastructure expansion.

Market Challenges

Power capacity constraints and energy cost volatility for high density AI compute

Thailand’s electricity infrastructure faces increasing strain from rapid growth in energy-intensive data centers and GPU clusters, where high power density racks significantly exceed traditional facility consumption patterns and require grid upgrades and dedicated substations. AI infrastructure operators encounter challenges securing reliable long-term power contracts at stable tariffs due to fluctuating energy costs and competing industrial demand across manufacturing and urban sectors. Cooling requirements for AI compute further increase energy intensity, amplifying operational expenditure pressures and sustainability concerns among investors and regulators. Renewable energy integration remains uneven across regions, limiting options for low-carbon AI infrastructure deployment necessary to meet environmental commitments of hyperscale providers. Grid connection timelines and permitting processes can delay facility commissioning, affecting capacity rollout schedules and market responsiveness. Land availability with adequate power and connectivity in prime urban areas such as Bangkok remains constrained, raising development costs and limiting scalability. Energy security considerations also influence infrastructure siting decisions, complicating expansion planning across multiple regions. These power and cost constraints collectively restrict rapid scaling of AI infrastructure despite strong demand signals.

Dependence on imported advanced semiconductors and AI hardware supply chains

Thailand’s AI infrastructure ecosystem relies heavily on imported GPUs, AI accelerators, advanced networking components, and specialized semiconductor systems sourced from global manufacturers, exposing the market to geopolitical supply disruptions and pricing volatility. Export controls and technology access restrictions affecting advanced AI chips can delay procurement cycles for hyperscale operators and enterprises planning large-scale deployments. Limited domestic semiconductor fabrication capability constrains local value chain participation in AI hardware manufacturing, reducing supply resilience and increasing import dependence. Logistics disruptions and component shortages extend lead times for critical infrastructure equipment, affecting deployment schedules and capacity availability. Currency fluctuations against major supplier currencies elevate capital expenditure unpredictability for infrastructure investors and operators. Maintenance and replacement cycles also depend on imported parts and technical expertise, increasing lifecycle costs and operational risk exposure. Domestic skill gaps in high-performance computing hardware engineering and AI infrastructure integration further compound dependence on foreign vendors and specialists. These supply chain vulnerabilities create structural uncertainty in infrastructure expansion planning and cost management.

Opportunities

Thailand as a regional AI compute hub for mainland Southeast Asia

Thailand’s geographic position, connectivity expansion, and growing hyperscale presence create an opportunity to evolve into a regional AI compute hub serving neighboring markets such as Cambodia, Laos, Myanmar, and Vietnam, which have emerging AI demand but limited domestic infrastructure. Cross-border digital service provision from Thai data centers can capture regional enterprise and government workloads seeking proximity and regulatory stability. Expansion of subsea cable landing stations and terrestrial fiber corridors enhances Thailand’s attractiveness for regional cloud and AI traffic aggregation. Multinational cloud providers can leverage Thailand facilities to distribute AI services across mainland Southeast Asia with optimized latency and compliance alignment. Regional enterprises operating supply chains across these countries benefit from centralized AI analytics hosted in Thailand, increasing infrastructure utilization. Government promotion of digital trade and cross-border data frameworks can further enable Thailand-hosted AI services to scale regionally. Co-location and managed AI infrastructure offerings targeting neighboring markets present new revenue streams for Thai operators. This positioning supports sustained infrastructure investment and capacity growth beyond domestic demand constraints.

Development of green AI data centers and sustainable compute infrastructure

Rising environmental expectations from global cloud providers and investors create opportunity for Thailand to differentiate through renewable-powered AI data centers and energy-efficient compute infrastructure aligned with sustainability standards. Integration of solar, wind, and energy storage systems with AI facilities can reduce operational emissions and attract hyperscale tenants seeking low-carbon hosting environments. Government incentives for green infrastructure and carbon reduction technologies can accelerate adoption of advanced cooling, liquid immersion systems, and energy optimization platforms tailored to AI workloads. Industrial zones with renewable energy availability can become preferred sites for next-generation AI campuses. Sustainable infrastructure branding enhances Thailand’s competitiveness against regional data center hubs while meeting corporate ESG requirements. Development of local expertise in energy-efficient AI facility design and operation can build domestic capability and innovation ecosystems. Green financing instruments and climate-aligned investment funds provide capital access for sustainable AI infrastructure projects. This transition toward environmentally optimized AI infrastructure creates long-term market differentiation and investment attraction.

Future Outlook

Thailand AI infrastructure market is expected to expand steadily over the next five years supported by hyperscale cloud region deployment, enterprise AI adoption, and national digital infrastructure investment programs. Continued data localization policies and smart city initiatives will sustain domestic compute demand. Technological shifts toward higher density GPUs, edge AI nodes, and energy-efficient cooling will shape infrastructure evolution. Regulatory facilitation and renewable energy integration are likely to influence site development and capacity expansion.

Major Players

- Amazon Web Services

- Microsoft

- ST Telemedia Global DataCentres

- NTT Global Data Centers

- Equinix • Huawei Cloud

- Alibaba Cloud

- Tencent Cloud

- True IDC

- Chindata Group

- GDS Holdings

- AIS

- CAT Telecom

- SupernapThailand

Key Target Audience

- Cloud service providers

- Telecommunications operators

- Data center developers

- Semiconductor and AI hardware vendors

- Large enterprises

- Investments and venture capitalist firms

- Government and regulatory bodies

- Smart city infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Key variables include AI compute capacity, hyperscale deployment activity, enterprise AI adoption levels, power infrastructure availability, semiconductor supply dependencies, and policy incentives influencing infrastructure investment across Thailand.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using data center investment disclosures, infrastructure deployment announcements, government digital economy programs, and enterprise AI adoption indicators across sectors requiring high performance computing resources.

Step 3: Hypothesis Validation and Expert Consultation

Infrastructure operators, cloud architects, telecom engineers, and regional digital infrastructure analysts were consulted to validate capacity trends, deployment economics, technology evolution, and demand drivers shaping Thailand AI infrastructure expansion.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized to produce market structure, segmentation shares, competitive positioning, and strategic outlook reflecting Thailand’s AI infrastructure ecosystem and regional role.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National AI strategy and digital economy investment programs

Expansion of hyperscale and colocation data centers - Market Challenges

High capital intensity and power infrastructure constraints

Limited domestic semiconductor ecosystem

Skills gap in AI infrastructure deployment and optimization - Market Opportunities

Regional AI hub positioning in Southeast Asia

Edge AI deployment across smart city and telecom networks

Public sector sovereign AI cloud initiatives - Trends

Shift toward GPU dense clusters and liquid cooling

Hybrid cloud AI infrastructure adoption

AI infrastructure localization and data sovereignty focus - Government Regulations & Defense Policy

Thailand Personal Data Protection Act data localization requirements

Board of Investment incentives for data center and AI investments

National AI strategy and digital infrastructure roadmap - Swot Analysis

Strong regional connectivity and digital policy support

Dependence on imported advanced hardware components

Growing enterprise AI adoption across regulated industries - Porters 5 forces

High supplier power due to concentrated GPU vendors

Moderate entry barriers from capital and expertise needs

Increasing buyer power among hyperscalers and telecoms

- By Market Value 2020-2025

- By Installed Units 2020-2025

- By Average System Price 2020-2025

- By System Complexity Tier 2020-2025

- By System Type (In Value%)

AI Compute Servers

GPU Accelerators

AI Networking Infrastructure

Edge AI Appliances

AI Storage Systems - By Platform Type (In Value%)

Cloud Data Centers

Enterprise On-premise AI Clusters

Telecom Edge Facilities

Hyperscale Facilities

Research and Academic Supercomputing Centers - By Fitment Type (In Value%)

Rack-integrated Systems

Blade AI Infrastructure

Modular AI Pods

Standalone Accelerator Units

Hyperconverged AI Systems - By End User Segment (In Value%)

Cloud Service Providers

Telecommunications Operators

Financial Services Institutions

Government and Public Sector

Healthcare and Life Sciences Organizations - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrators

Cloud Marketplace Procurement

Government Technology Contracts

Value-added Distributors

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Compute Density, Energy Efficiency, Deployment Scalability, AI Framework Compatibility, Service Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

AMD

Intel

Supermicro

Hewlett Packard Enterprise

Dell Technologies

Lenovo

Huawei

Inspur

Quanta Cloud Technology

Foxconn Industrial Internet

Wiwynn

Advantech

NEC

Fujitsu

- Cloud providers scaling GPU clusters for AI services

- Telecom operators integrating edge AI into 5G networks

- Financial institutions deploying AI risk and analytics platforms

- Government agencies building sovereign AI compute capacity

- Forecast Market Value 2026-2035

- Forecast Installed Units 2026-2035

- Price Forecast by System Tier 2026-2035

- Future Demand by Platform 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now