Download PDF

Download PDF Download PDF

Download PDFMarket Overview

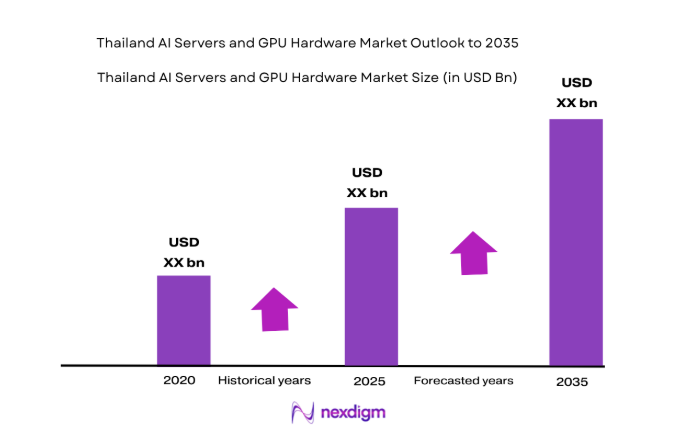

Thailand AI servers and GPU hardware market reflects accelerating capital expenditure on artificial intelligence infrastructure across enterprise and hyperscale deployments, with hardware imports and domestic system integration together exceeding USD ~ billion based on a recent historical assessment by Thailand Board of Investment and UN Comtrade technology hardware trade data. Growth is driven by expansion of AI cloud zones, national digital economy programs, and enterprise adoption of generative AI workloads that require high performance parallel computing architectures and advanced accelerator clusters.

Bangkok and Eastern Economic Corridor provinces dominate deployment due to concentration of hyperscale data centers, telecom landing stations, and government supported digital infrastructure clusters attracting global cloud and semiconductor ecosystem participants. Thailand serves as a regional AI infrastructure node linking ASEAN workloads, benefiting from submarine cable connectivity, competitive colocation costs, and policy incentives for high performance computing investments, making it a preferred location for regional GPU clusters and AI training facilities.

Market Segmentation

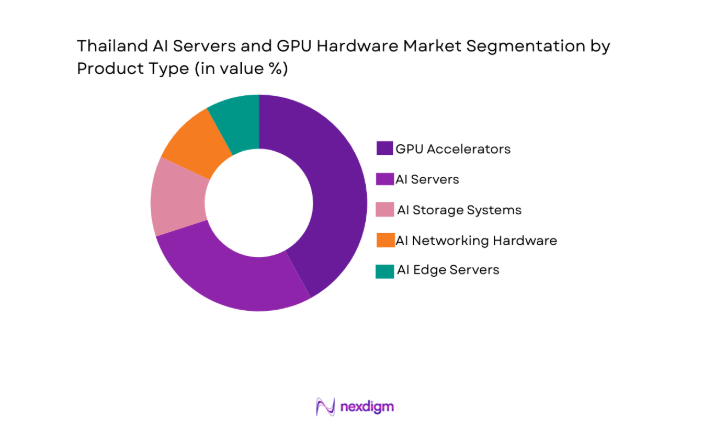

By Product Type

Thailand AI Servers and GPU Hardware market is segmented by product type into AI servers, GPU accelerators, AI storage systems, AI networking hardware, and AI edge servers. Recently, GPU accelerators has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

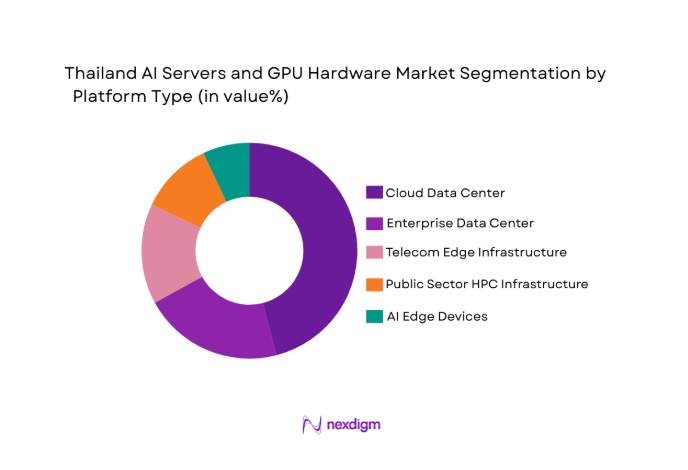

By Platform Type

Thailand AI Servers and GPU Hardware market is segmented by platform type into cloud data center, enterprise data center, telecom edge infrastructure, government and research HPC facilities, and AI edge devices. Recently, cloud data center has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

Competitive Landscape

Thailand AI servers and GPU hardware market shows moderate concentration with global accelerator manufacturers and OEM server vendors partnering with regional system integrators and cloud operators to deploy large scale AI clusters. Market structure is shaped by supply relationships with semiconductor leaders, while local distributors and integrators influence procurement and deployment across telecom and enterprise segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Accelerator Architecture |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| AMD | 1969 | USA | ~ | ~ | ~ | ~ | ~ |

| Intel | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Supermicro | 1993 | USA |

Thailand AI Servers and GPU Hardware Market Analysis

Growth Drivers

Expansion of Hyperscale AI Cloud Infrastructure in Southeast Asia

Thailand has emerged as a strategic artificial intelligence infrastructure hub within Southeast Asia due to rapid hyperscale data center expansion, sovereign cloud programs, and regional workload aggregation trends that are concentrating AI training and inference deployments in a limited number of digitally advanced locations. Global cloud providers are investing in GPU dense server clusters and AI supercomputing facilities to serve enterprise and platform customers across ASEAN markets from Thailand, benefiting from strong connectivity, stable power infrastructure, and investment incentives that reduce capital costs for large scale compute deployments. Telecom operators and colocation providers are also building AI ready data center campuses with high density power and liquid cooling capabilities, directly increasing demand for AI servers and accelerator hardware shipments. The emergence of generative artificial intelligence adoption among financial services, manufacturing, retail, and digital platform firms in Thailand is further accelerating enterprise procurement of GPU clusters either on premise or through domestic cloud zones, strengthening local hardware demand. Government backed national AI strategies and digital economy initiatives are supporting public sector supercomputing and research AI infrastructure investments that rely on advanced accelerator systems. Supply chain localization strategies by global server OEMs and semiconductor firms are improving availability and reducing procurement latency for AI hardware in Thailand, encouraging faster deployment cycles. Regional AI workload centralization is also driving multinational firms to establish Thai GPU clusters to serve multilingual Southeast Asian applications requiring proximity to users and data compliance alignment. The combination of hyperscale cloud expansion, enterprise AI adoption, and policy incentives is structurally increasing Thailand’s demand for AI servers and GPU hardware over the medium term.

Enterprise Adoption of Generative AI and High Performance Computing Workloads

Organizations across banking, telecommunications, healthcare, manufacturing, and digital commerce sectors in Thailand are integrating generative artificial intelligence, predictive analytics, and machine learning models into operational and customer facing systems, which is fundamentally increasing requirements for high performance computing infrastructure based on GPUs and AI optimized servers. Training large language models, computer vision systems, and recommendation engines requires massively parallel compute architectures that traditional CPU based servers cannot efficiently deliver, driving enterprises to procure GPU clusters either directly or via private cloud deployments. AI driven automation in manufacturing and logistics is expanding deployment of edge AI servers connected to central GPU training infrastructure, creating multi tier hardware demand across data center and edge layers. Thai enterprises are also building internal data science platforms and AI development environments that require on demand accelerator resources, increasing consumption of GPU hardware within corporate data centers. The rapid growth of AI enabled digital services and applications targeting regional Southeast Asian markets is pushing Thai technology firms and startups to invest in local training infrastructure to reduce latency and data transfer costs associated with offshore compute. Academic and research institutions collaborating with industry on AI innovation programs are expanding supercomputing capacity using GPU based clusters, reinforcing national demand. Availability of AI optimized software stacks and development frameworks is lowering adoption barriers and making GPU infrastructure more accessible to enterprises. As AI workloads transition from experimentation to production scale deployments across industries, sustained enterprise investment in GPU servers and accelerators is becoming a primary driver of Thailand’s AI hardware market expansion.

Market Challenges

Supply Constraints and High Cost of Advanced GPU Accelerators

The Thailand AI servers and GPU hardware market faces structural supply limitations driven by global shortages of advanced semiconductor nodes, concentrated manufacturing capacity, and prioritization of large hyperscale buyers in mature markets, which collectively restrict availability of cutting edge GPU accelerators for emerging AI infrastructure hubs. High performance GPUs used for training and inference are manufactured on leading edge process technologies with limited foundry capacity, resulting in long lead times and elevated procurement costs for Thai enterprises and data center operators seeking to deploy AI clusters. Import dependence on foreign semiconductor supply chains exposes Thailand to geopolitical trade restrictions and export control policies affecting availability of advanced accelerators, particularly those designed for large scale AI training workloads. Currency fluctuations and logistics costs further increase landed prices of AI hardware in Thailand, constraining affordability for mid tier enterprises and research institutions. Capital intensity of GPU dense server deployments also raises financing barriers for local cloud and colocation providers attempting to scale AI infrastructure competitively with global hyperscale firms. Cooling, power density, and facility upgrade costs associated with high performance GPU clusters add to total cost of ownership, limiting widespread adoption. Smaller enterprises often rely on shared or offshore AI compute due to cost constraints, reducing domestic hardware demand growth potential. These supply and cost pressures create market concentration around large buyers and slow broader diffusion of AI hardware across Thailand’s economy.

Infrastructure Readiness and Power Density Limitations for AI Data Centers

Deployment of large scale AI servers and GPU clusters requires data center environments capable of supporting extremely high power density, advanced cooling technologies, and resilient electrical infrastructure, which remains unevenly distributed across Thailand despite rapid digital infrastructure growth. Many existing enterprise data centers were designed for conventional IT loads and lack the electrical capacity and thermal management systems required for modern AI accelerators operating at high wattage levels, necessitating costly retrofits or migration to specialized facilities. Availability of liquid cooling infrastructure, high voltage substations, and redundant power supply in certain regions outside Bangkok and the Eastern Economic Corridor is limited, constraining geographic expansion of AI hardware deployments. Power reliability and sustainability requirements for hyperscale AI clusters also impose stringent infrastructure standards that only a subset of Thai facilities currently meet. Land, permitting, and grid connection timelines for new high density AI data centers can delay deployment of GPU infrastructure projects. Skilled workforce availability for operating and maintaining AI optimized data center environments is another constraint affecting infrastructure readiness. Environmental and energy efficiency regulations are increasing complexity of high power AI facility development. These infrastructure limitations slow scaling of AI server installations and concentrate deployments in a few advanced zones, creating regional imbalance in Thailand’s AI hardware market development.

Opportunities

Thailand as Regional AI Compute Hub for ASEAN Workloads

Thailand possesses geographic, economic, and connectivity advantages that position it to serve as a regional artificial intelligence compute hub for Southeast Asia, enabling large scale deployment of AI servers and GPU clusters serving cross border enterprise and platform workloads across multiple ASEAN countries. Submarine cable connectivity and central location allow low latency access to major regional markets, encouraging multinational cloud and technology firms to place AI training infrastructure in Thailand rather than duplicating clusters in each smaller market. Policy incentives for digital infrastructure investment and data center development further enhance attractiveness for regional AI compute facilities. As neighboring economies expand AI adoption but lack comparable infrastructure readiness, Thailand can aggregate demand and host shared GPU clusters serving regional applications such as multilingual language models, fintech analytics, and regional e commerce platforms. Cross border data frameworks and regional cloud architectures are reinforcing centralized compute models that favor Thailand based AI hardware deployments. Telecom operators and data center developers are already expanding capacity targeting regional AI workloads, creating opportunities for accelerator vendors and server OEMs. Academic and innovation partnerships across ASEAN can also leverage Thai supercomputing resources, strengthening regional positioning. Establishment of Thailand as an AI compute hub would structurally increase long term demand for AI servers and GPU hardware installations.

Government Supported National AI Supercomputing and Research Infrastructure Programs

National digital economy and artificial intelligence strategies in Thailand include development of public sector supercomputing facilities, AI innovation centers, and research infrastructure that rely heavily on GPU based high performance computing systems, creating sustained institutional demand for AI servers and accelerator hardware. Government agencies and universities are investing in AI clusters to support scientific research, language technologies, smart city systems, and industrial AI innovation programs, expanding non commercial demand for advanced compute infrastructure. Public procurement initiatives can stimulate local ecosystem development around AI hardware deployment, integration, and maintenance services. National AI platforms providing shared compute access to startups and enterprises further increase installed GPU capacity in Thailand. Partnerships between government research institutions and global technology firms can accelerate deployment of state of the art accelerator systems in national facilities. Development of sovereign AI capabilities and secure domestic training environments for sensitive data applications reinforces need for local GPU infrastructure. Education and workforce development programs centered on AI supercomputing resources also expand utilization of installed hardware. Continued public investment in AI research infrastructure represents a stable long term opportunity segment for AI server and GPU hardware vendors in Thailand.

Future Outlook

Thailand AI servers and GPU hardware market is expected to expand steadily over the next five years as hyperscale cloud expansion, enterprise generative AI adoption, and national digital infrastructure programs accelerate deployment of high performance computing clusters. Advances in accelerator architectures, liquid cooled AI servers, and energy efficient data center design will improve deployment economics and scalability. Government incentives for AI infrastructure and regional data center investments will support capacity growth. Demand from ASEAN workloads and domestic AI applications will sustain hardware procurement momentum.

Major Players

- NVIDIA

- AMD

- Intel

- Dell Technologies

- Supermicro

- Hewlett Packard Enterprise

- Lenovo

- Inspur

- ASUS

- Gigabyte

- Foxconn Industrial Internet

- Quanta Computer

- Wistron

- Advantech

- Huawei

Key Target Audience

- Hyperscale cloud providers

- Telecom operators

- Data center developers

- Semiconductor and accelerator vendors

- Enterprise IT infrastructure buyers

- Investments and venture capitalist firms

- Government and regulatory bodies

- AI platform providers

Research Methodology

Step 1: Identification of Key Variables

Key market variables including AI server shipments, GPU accelerator imports, hyperscale data center capacity, enterprise AI adoption intensity, and public sector HPC investments were identified from government trade data, digital economy programs, and technology infrastructure databases to establish market scope and boundaries.

Step 2: Market Analysis and Construction

Supply side vendor shipments, regional deployment trends, and demand side infrastructure investments were triangulated to construct Thailand AI servers and GPU hardware market structure and segmentation across product types and end users.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market estimates and technology adoption assumptions were validated through consultation with data center operators, system integrators, and AI infrastructure specialists active in Southeast Asian deployments.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into final market sizing, segmentation, competitive landscape, and forward-looking analysis ensuring consistency with regional AI infrastructure development patterns.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of hyperscale and colocation data centers in Thailand

Rising enterprise AI adoption across finance manufacturing and telecom

Government digital economy and AI infrastructure incentives - Market Challenges

High capital cost and import dependence of advanced GPUs

Power and cooling constraints in dense AI data centers

Limited local semiconductor and server manufacturing base - Market Opportunities

Regional AI cloud hub positioning within ASEAN

Edge AI infrastructure for smart city and 5G applications

Local assembly and integration ecosystem development - Trends

Shift toward liquid cooled and high density GPU servers

Growth of sovereign and enterprise private AI clouds

Adoption of heterogeneous accelerators beyond GPUs - Government Regulations & Defense Policy

Data localization and cybersecurity compliance for AI workloads

Investment incentives for digital and data center infrastructure

Import and certification requirements for IT hardware - Swot Analysis

Strong data center expansion and connectivity advantages

Dependence on foreign GPU and server technology supply

Emerging ASEAN AI infrastructure demand spillover - Porters 5 Forces

High supplier power from limited advanced GPU vendors

Moderate entry barriers due to capital and expertise needs

Rising buyer power from hyperscale cloud operators

- By Market Value 2020-2025

- By Installed Units 2020-2025

- By Average System Price 2020-2025

- By System Complexity Tier 2020-2025

- By System Type (In Value%)

AI Training Servers

AI Inference Servers

GPU Accelerated Compute Nodes

Edge AI Servers

High Density GPU Clusters - By Platform Type (In Value%)

Data Center AI Infrastructure

Cloud AI Platforms

Enterprise On Premise AI Systems

Telecom Edge AI Platforms

Research and HPC Platforms - By Fitment Type (In Value%)

Rack Mounted AI Servers

Blade AI Servers

Tower GPU Workstations

Modular AI Server Blocks

Integrated AI Appliances - By End User Segment (In Value%)

Cloud Service Providers

Telecom Operators

Financial Services Institutions

Government and Research Labs

Large Enterprises and Conglomerates - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrator Contracts

Distributor and Channel Partners

Cloud Marketplace Bundling

Government Tenders

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (GPU Density, Compute Performance per Rack, Power Efficiency, Cooling Technology, AI Framework Optimization)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

Advanced Micro Devices

Intel

Super Micro Computer

Dell Technologies

Hewlett Packard Enterprise

Lenovo

Inspur

ASUS

Gigabyte

Quanta Computer

Foxconn Industrial Internet

Wiwynn

Cisco Systems

Fujitsu

- Cloud providers driving large scale GPU cluster deployments

- Telecom operators investing in edge AI compute for 5G services

- Enterprises adopting on premise AI for data sensitive workloads

- Government and academia expanding national AI compute capacity

- Forecast Market Value 2026-2035

- Forecast Installed Units 2026-2035

- Price Forecast by System Tier 2026-2035

- Future Demand by Platform 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now