Download PDF

Download PDF Download PDF

Download PDFMarket Overview

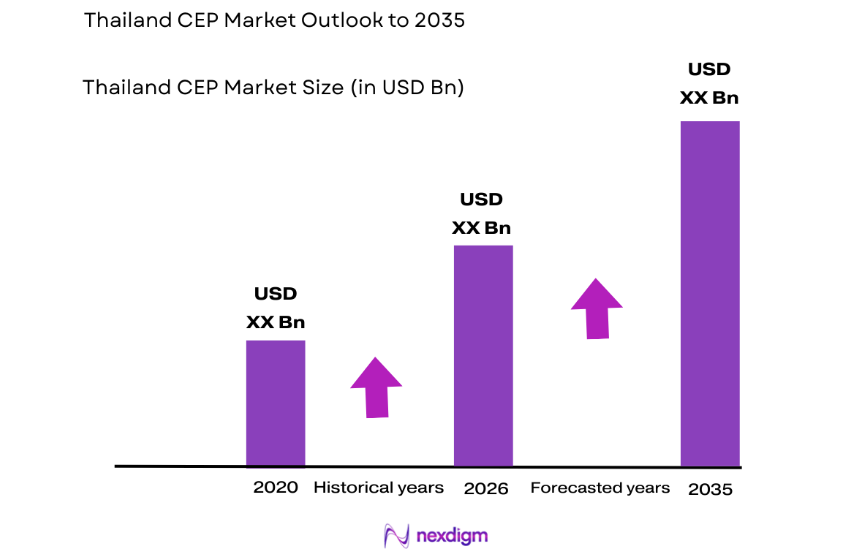

Based on a recent historical assessment, the Thailand Courier, Express, and Parcel market is valued at approximately USD ~ billion according to data published by Thailand Post, the Ministry of Digital Economy and Society, and Statista logistics datasets. The market is strongly driven by expanding e-commerce platforms, rising digital retail transactions, and increased domestic parcel shipments generated by online marketplaces and social commerce merchants. Logistics providers continue investing in automated sorting centers, nationwide delivery fleets, and digital tracking technologies to handle growing parcel volumes.

Bangkok remains the dominant logistics hub due to its concentration of fulfillment centers, e-commerce merchants, and national distribution infrastructure supported by major transport corridors and airports. Secondary logistics activity is expanding across provinces including Chonburi, Nonthaburi, Samut Prakan, and Chiang Mai where industrial estates, urban population clusters, and regional trade corridors generate high parcel shipment demand. Strategic infrastructure such as Laem Chabang Port, Suvarnabhumi Airport cargo facilities, and integrated highway networks further strengthens parcel distribution connectivity across Thailand.

Market Segmentation

By Service Type

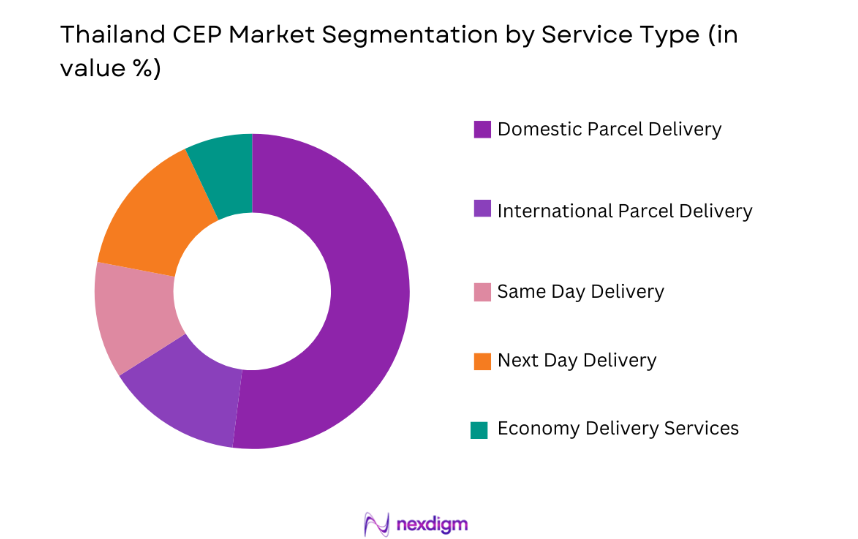

Thailand CEP market is segmented by service type into Domestic Parcel Delivery, International Parcel Delivery, Same Day Delivery, Next Day Delivery, and Economy Delivery Services. Recently, Domestic Parcel Delivery has a dominant market share due to factors such as expanding local e-commerce shipments, social commerce transactions, and rising small parcel distribution between urban consumers and provincial areas. Thailand’s rapidly expanding online retail ecosystem requires extensive domestic parcel movement across metropolitan and regional markets. Logistics providers have therefore developed nationwide delivery networks supported by sorting centers, last-mile motorcycle fleets, and digital parcel tracking platforms. These domestic networks allow logistics operators to handle large daily parcel volumes generated by e-commerce platforms, retail merchants, and direct consumer shipments.

By End User

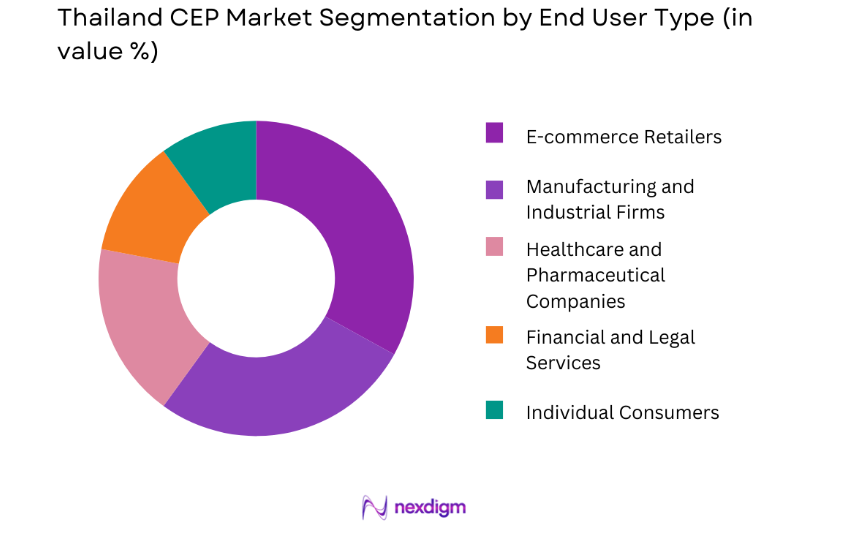

Thailand CEP market is segmented by end user into E-commerce Retailers, Manufacturing and Industrial Firms, Healthcare and Pharmaceutical Companies, Financial and Legal Services, and Individual Consumers. Recently, E-commerce Retailers have a dominant market share due to factors such as strong online retail adoption, high order volumes generated by digital marketplaces, and continuous growth of mobile commerce transactions. Online marketplaces such as Lazada, Shopee, and regional social commerce platforms generate substantial daily shipment volumes requiring reliable parcel distribution networks. Retail merchants rely heavily on courier operators for order fulfillment, last-mile delivery, and reverse logistics operations. Logistics providers therefore prioritize e-commerce fulfillment services including parcel sorting automation, warehouse integration, and real-time shipment tracking systems.

Competitive Landscape

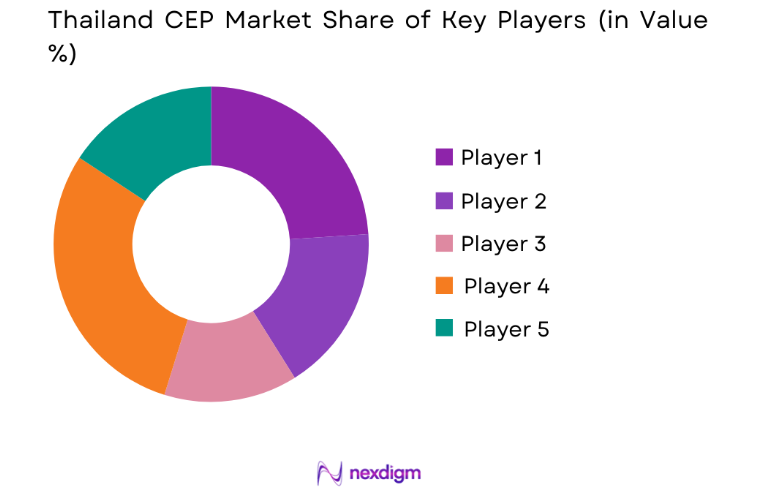

The Thailand CEP market demonstrates moderate consolidation with a mixture of national postal operators, international logistics corporations, and rapidly growing private courier companies competing for parcel distribution contracts. Major logistics providers expand delivery networks through investments in automated sorting centers, fulfillment infrastructure, and advanced parcel tracking technologies. Strategic partnerships with e-commerce platforms further strengthen parcel volumes handled by leading operators. Competition is driven by delivery speed, service coverage, pricing efficiency, and technological integration supporting high parcel throughput.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Network Size |

| Thailand Post | 1883 | Bangkok, Thailand | ~ | ~ | ~ | ~ | ~ |

| Kerry Express Thailand | 2006 | Bangkok, Thailand | ~ | ~ | ~ | ~ | ~ |

| DHL Express Thailand | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| Flash Express | 2017 | Bangkok, Thailand | ~ | ~ | ~ | ~ | ~ |

| FedEx Thailand | 1971 | Memphis, USA | ~ | ~ | ~ | ~ | ~ |

Thailand CEP Market Analysis

Growth Drivers

Expansion of E-commerce Platforms and Social Commerce Logistics Demand

The rapid growth of digital marketplaces and social commerce platforms across Thailand has significantly increased parcel shipment volumes handled by courier, express, and parcel operators nationwide. Online marketplaces facilitate daily transactions for electronics, fashion goods, household products, and groceries, which require efficient delivery infrastructure capable of reaching urban and rural consumers. Increasing smartphone penetration and mobile payment adoption allow consumers to purchase goods through digital platforms more frequently, generating continuous parcel demand across logistics networks. Social commerce merchants selling products through live streaming and messaging applications also rely heavily on courier networks for nationwide product distribution. Logistics providers respond by investing in automated parcel sorting centers, warehouse fulfillment infrastructure, and last mile delivery fleets designed to manage high shipment volumes efficiently. Digital parcel tracking platforms and route optimization software further improve delivery transparency and operational efficiency. Partnerships between courier companies and e-commerce platforms enable integrated order management systems that streamline fulfillment processes. As digital retail participation continues expanding across Thailand’s consumer economy, parcel logistics networks remain critical infrastructure supporting nationwide e-commerce growth.

Rapid Urbanization and Nationwide Logistics Infrastructure Development

Thailand’s expanding urban population and ongoing logistics infrastructure development significantly support the growth of courier, express, and parcel services across metropolitan and regional markets. Urban centers generate high parcel density because residential clusters, retail activity, and business transactions occur within concentrated geographic areas that allow efficient delivery operations. Major infrastructure investments including highway expansions, airport cargo facilities, and logistics parks improve national transportation connectivity and reduce parcel transit times between regions. Industrial zones located near Bangkok and eastern economic corridor provinces generate substantial shipment volumes requiring reliable courier networks connecting manufacturers, suppliers, and customers. Logistics providers establish regional distribution hubs and automated sorting facilities positioned strategically near transportation corridors to accelerate parcel movement across provinces. Government initiatives aimed at strengthening digital infrastructure and trade logistics further enhance parcel distribution capabilities nationwide. The development of regional fulfillment centers also enables faster delivery services to consumers located outside major metropolitan areas. These infrastructure improvements collectively support growing parcel shipment volumes across Thailand’s expanding logistics ecosystem.

Market Challenges

High Operational Costs and Last Mile Delivery Complexity

Logistics companies operating within the Thailand CEP market face significant operational cost pressures associated with last mile delivery operations, transportation fuel expenses, and labor intensive distribution networks. Delivering parcels to dense urban areas and geographically dispersed rural regions requires extensive transportation fleets, delivery personnel, and sorting infrastructure capable of handling large shipment volumes daily. Rising fuel prices increase the cost of maintaining nationwide delivery fleets including vans, trucks, and motorcycle couriers commonly used in urban distribution networks. Labor costs associated with recruiting and managing thousands of delivery riders further increase operational expenditures for logistics providers. Traffic congestion within Bangkok and surrounding metropolitan areas also creates logistical inefficiencies that extend delivery times and reduce route productivity. Courier companies must therefore invest heavily in route optimization software, parcel tracking technologies, and automated sorting facilities to maintain service reliability while controlling operational expenses. These investments require significant capital expenditure that smaller logistics operators may struggle to finance. As parcel shipment volumes continue expanding nationwide, logistics providers must carefully balance operational efficiency with cost management strategies to maintain sustainable profitability.

Infrastructure Limitations in Secondary and Rural Delivery Regions

Parcel logistics operations across Thailand encounter infrastructure challenges when delivering shipments to secondary provinces and rural regions where transportation networks and logistics facilities remain less developed. Many rural communities are located far from major logistics hubs, requiring longer delivery routes that increase fuel consumption and operational time for courier companies. Limited availability of regional sorting centers and parcel distribution facilities further complicates efficient shipment processing outside major metropolitan areas. Delivery companies often rely on decentralized delivery networks or subcontracted distribution partners to reach remote customers, which may reduce service consistency and operational control. Road infrastructure quality in certain rural districts can also affect transportation efficiency and vehicle maintenance costs for logistics operators. Seasonal weather conditions including heavy rainfall and flooding occasionally disrupt transportation routes and delay parcel deliveries to affected regions. Logistics companies must therefore invest in expanded distribution infrastructure and regional logistics hubs capable of improving service reliability across remote locations. These operational constraints remain important challenges influencing the overall efficiency of nationwide parcel distribution networks.

Opportunities

Expansion of Cross Border E Commerce and Regional Parcel Trade

Thailand’s strategic geographic location within Southeast Asia creates significant opportunities for cross border e commerce logistics and international parcel delivery services connecting regional consumer markets. Online retail platforms increasingly facilitate international transactions between merchants located in Thailand, China, Singapore, and other regional economies, generating growing demand for cross border parcel shipments. Logistics companies are developing international courier services capable of supporting customs clearance, international freight forwarding, and last mile delivery integration across multiple countries. Improved regional trade agreements and digital commerce frameworks also simplify cross border retail transactions between Southeast Asian markets. International logistics companies are investing in regional fulfillment hubs and automated parcel processing facilities that allow efficient handling of international shipments entering and leaving Thailand. Airports such as Suvarnabhumi and Don Mueang serve as major international cargo gateways supporting parcel exports and imports generated by online retail transactions. As cross border e commerce continues expanding across Southeast Asia, Thailand’s CEP industry is positioned to benefit from growing international parcel logistics demand.

Adoption of Logistics Automation and Smart Delivery Technologies

The integration of advanced logistics automation technologies presents significant growth opportunities for courier, express, and parcel companies seeking to improve delivery efficiency and service quality across Thailand. Automated parcel sorting systems allow logistics operators to process high shipment volumes rapidly while reducing manual labor requirements and operational errors. Artificial intelligence powered route optimization platforms enable delivery companies to determine efficient transportation routes that reduce fuel consumption and delivery time. Smart parcel lockers installed within residential complexes, transportation hubs, and retail centers provide alternative delivery points that improve customer convenience and reduce failed delivery attempts. Robotics and warehouse automation technologies also support faster order fulfillment processes for e commerce merchants using integrated logistics networks. Real time shipment tracking platforms allow customers to monitor parcel movement across logistics networks, improving transparency and service reliability. Logistics providers adopting these technologies can significantly improve operational productivity while reducing long term distribution costs. These digital innovations are expected to transform parcel logistics operations as technology adoption accelerates across the industry.

Future Outlook

Thailand’s CEP market is expected to expand steadily as digital commerce adoption continues increasing across urban and provincial regions. Logistics companies are investing heavily in automation technologies, fulfillment centers, and nationwide distribution infrastructure to support rising parcel volumes generated by online retail activity. Government initiatives aimed at strengthening digital trade infrastructure and logistics connectivity further support industry expansion. Technological innovations including route optimization systems, automated warehouses, and smart delivery lockers are expected to enhance operational efficiency and service reliability across Thailand’s parcel delivery ecosystem.

Major Players

- Thailand Post

- Kerry Express Thailand

- Flash Express

- DHL Express Thailand

- FedEx Thailand

- SCG Logistics

- Ninja Van Thailand

- J&T Express Thailand

- Best Express Thailand

- Aramex Thailand

- UPS Thailand

- Lalamove Thailand

- Deliveree Logistics

- CJ Logistics Thailand

- Yusen Logistics Thailand

Key Target Audience

- E commerce retailers and digital marketplace operator

- Logistics and courier service providers

- Manufacturing and industrial exporters

- Retail distribution and fulfillment companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Supply chain technology solution providers

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the Thailand CEP market including parcel shipment volume, e-commerce adoption, logistics infrastructure, and courier service demand were identified through secondary data sources and logistics industry reports.

Step 2: Market Analysis and Construction

The market structure was constructed using trade data, parcel shipment statistics, government logistics infrastructure reports, and company financial disclosures to estimate overall market size and segmentation patterns.

Step 3: Hypothesis Validation and Expert Consultation

Industry insights were validated through consultation with logistics professionals, supply chain analysts, and transportation infrastructure specialists to ensure reliability and consistency of market assumptions.

Step 4: Research Synthesis and Final Output

All research findings were synthesized into a structured market framework combining quantitative shipment data and qualitative industry analysis to produce the final Thailand CEP market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of E-commerce and Online Retail Networks

Government Investment in Logistics Infrastructure

Adoption of Real-Time Tracking and Automation Technologies - Market Challenges

High Capital Expenditure for Automation and Fleet Management

Fragmented Logistics Providers Across Regions

Regulatory Compliance for Cross-Border Deliveries - Market Opportunities

Expansion of Cold Chain and Temperature-Sensitive Delivery Solutions

Integration of AI and Predictive Analytics in Delivery Networks

Partnerships Between Logistics Providers and E-commerce Platforms - Trends

Use of Autonomous and Electric Delivery Vehicles

Implementation of Smart Locker and Micro-Distribution Networks - Government Regulations

Data Protection and Privacy Regulations

Transport Licensing and Compliance

Supportive Public-Private Logistics Initiatives - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Sorting and Handling Systems

Automated Guided Vehicles

Conveyor and Material Handling Systems

Cold Chain Management Systems

Tracking and Monitoring Systems - By Platform Type (In Value%)

Land Transportation Platforms

Air Freight Platforms

Maritime Freight Platforms

Integrated Multimodal Platforms - By Fitment Type (In Value%)

On-premise CEP Solutions

Cloud-based CEP Solutions

Hybrid CEP Solutions

Modular CEP Solutions - By End User Segment (In Value%)

E-commerce Retailers

Logistics Service Providers

Food and Beverage Companies

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Technology Adoption, Automation Level, Geographic Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

JNE Express Thailand

TIKI Thailand

POS Thailand

SiCepat Ekspres Thailand

J&T Express Thailand

Lion Parcel Thailand

Ninja Xpress Thailand

Anteraja Thailand

SAP Express Thailand

Wahana Prestasi Logistik Thailand

Sicepat Ekspres Thailand

Lalamove Thailand

GrabExpress Thailand

FedEx Thailand

DHL Express Thailand

- E-commerce Retailers Expanding Same-Day and Express Delivery Services

- Food and Beverage Companies Requiring Cold Chain Distribution

- Logistics Providers Outsourcing Last-Mile Operations

- Retailers Leveraging Technology for Route Optimization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now