Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Thailand’s cold chain logistics market is valued at approximately USD ~ billion based on a recent historical assessment, driven by increasing demand for temperature-sensitive storage and transportation services across food, pharmaceutical, and biotechnology sectors. Government initiatives to improve cold storage infrastructure, expansion of refrigerated transport networks, and growth of modern retail and e commerce sectors further accelerate market adoption. Investments in technology-enabled monitoring systems, automated warehouses, and refrigerated fleet expansions enhance operational efficiency and service reliability, supporting the growing logistics needs of perishable and sensitive products across the country.

Major cold chain operations are concentrated in Bangkok, Chonburi, and Samut Prakan due to their proximity to industrial zones, ports, and airports facilitating domestic and international distribution. Bangkok serves as the primary logistics hub with access to urban and regional refrigerated networks, supporting both wholesale and retail distribution. Chonburi’s Eastern Seaboard industrial corridor strengthens export-oriented cold chain operations, particularly for seafood and processed foods. Samut Prakan hosts major cold storage facilities serving industrial and pharmaceutical clients. These cities attract leading cold chain providers due to operational efficiency, connectivity, and concentration of temperature-sensitive manufacturing and distribution activities.

Market Segmentation

By Service Type

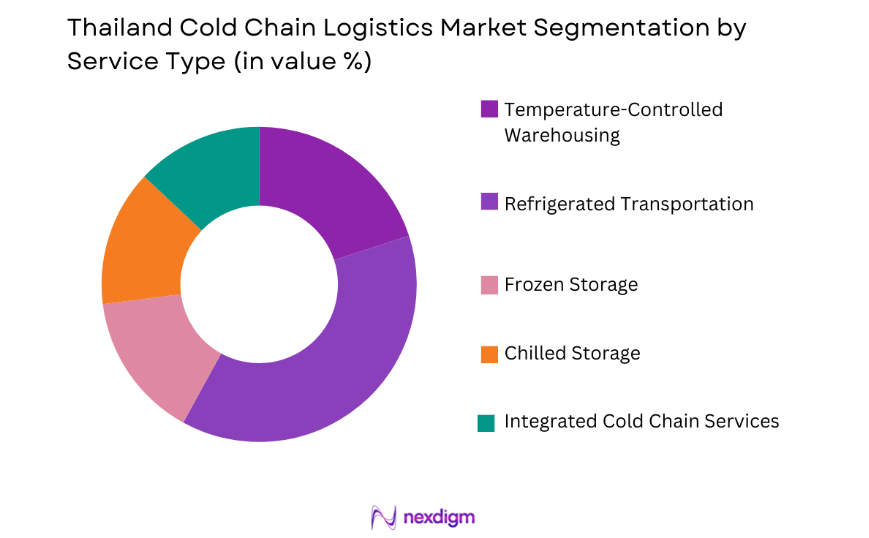

Thailand Cold Chain Logistics Market is segmented by product type into temperature-controlled warehousing, refrigerated transportation, frozen storage, chilled storage, and integrated cold chain services. Recently, refrigerated transportation has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Efficient transportation of perishable goods including seafood, dairy, and pharmaceuticals is critical to maintain product quality and regulatory compliance. Providers invest in refrigerated trucks, vans, and air cargo solutions equipped with real-time temperature monitoring. Rapid growth of retail, e commerce, and export sectors increases reliance on reliable refrigerated transportation. Integration with warehouses and distribution networks ensures timely deliveries across metropolitan and regional areas. Investments in GPS tracking and IoT-enabled vehicles further strengthen operational efficiency and service reliability, making refrigerated transportation the primary service segment.

By End User Industry

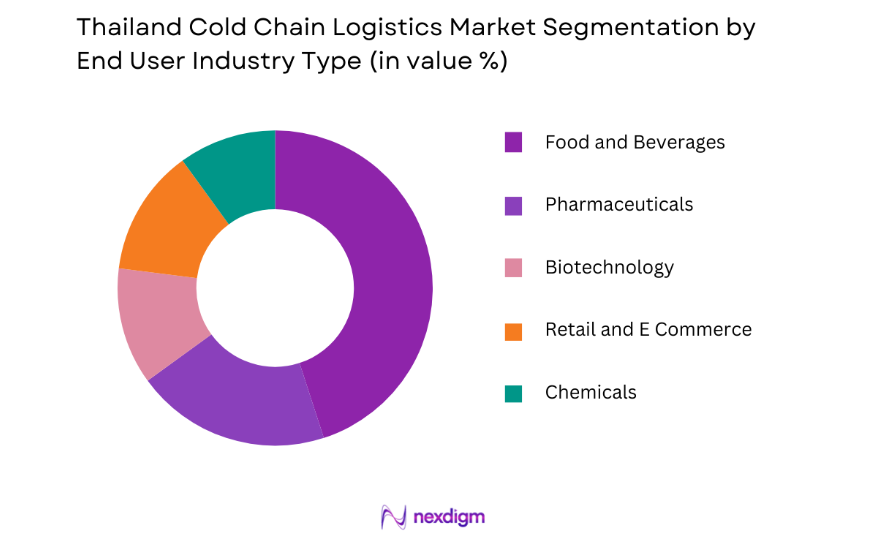

Thailand Cold Chain Logistics Market is segmented by product type into food and beverages, pharmaceuticals, biotechnology, retail and e commerce, and chemicals. Recently, food and beverages has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Thailand’s large agricultural and seafood export sectors require cold chain solutions to preserve freshness and quality during transport. Rapid growth of modern retail chains, online grocery platforms, and convenience store networks generates high demand for refrigerated storage and distribution. Providers implement automated cold storage systems and advanced temperature monitoring to meet stringent product handling requirements. Efficient distribution from production sites to urban centers and export destinations strengthens the adoption of cold chain services. Food safety regulations and international export standards further reinforce market reliance on reliable cold logistics providers.

Competitive Landscape

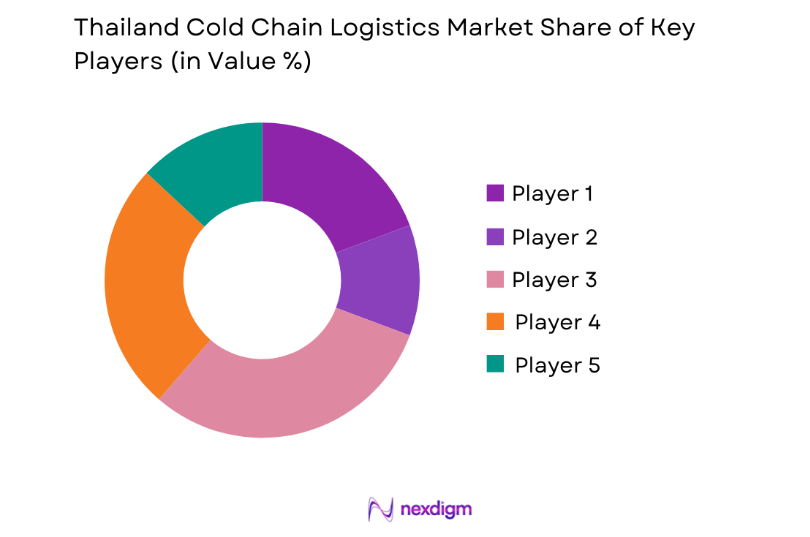

The Thailand cold chain logistics market is moderately consolidated with multinational and domestic operators offering temperature-controlled warehousing, transportation, and integrated logistics services. Key players compete through advanced technology adoption, infrastructure investments, and specialized industry partnerships. Strategic alliances with pharmaceutical companies, food exporters, and retail chains enhance operational scale and regional reach. Investments in IoT monitoring, automated warehouses, and refrigerated fleet expansion strengthen competitive advantage across temperature-sensitive logistics operations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Refrigerated Fleet Size |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Germany | ~ | ~ | ~ | ~ | ~ |

| CEVA Logistics | 2007 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Agility Logistics | 1979 | Kuwait | ~ | ~ | ~ | ~ | ~ |

Thailand Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Food and Seafood Export Logistics Networks

Thailand Cold Chain Logistics Market growth is strongly driven by the expansion of food and seafood export logistics networks, which require temperature-controlled warehousing and refrigerated transportation solutions. The country’s seafood and agricultural sectors produce high-volume perishable goods that must maintain strict temperature standards for international shipments. Cold chain providers invest in refrigerated trucks, containers, and monitoring systems to ensure product quality during domestic and international transport. Export-oriented industrial estates and port connectivity enhance operational efficiency. Automation in storage and sorting increases throughput capacity. Food safety regulations demand adherence to strict quality control, further driving investment in cold chain technology. Integration of real-time tracking, GPS monitoring, and IoT-enabled refrigeration ensures compliance with global standards. Strategic partnerships between cold chain providers and exporters reduce logistical complexity and improve delivery reliability. Urban distribution hubs support fast movement to retail and wholesale markets. Investments in cold storage facilities near production zones facilitate efficient inventory management and shipment readiness. Advanced temperature monitoring reduces spoilage and product loss, enhancing profitability. Consumer expectations for freshness increase demand for rapid, reliable delivery. Seasonal production peaks require scalable cold logistics solutions. Export volume growth drives fleet expansion and operational scaling. Cross-border trade agreements increase international shipment flows. Technology adoption improves route planning, storage optimization, and workflow efficiency. Operational resilience and service reliability strengthen competitive positioning. Cold chain investments sustain Thailand’s export competitiveness and market expansion.

Rising Pharmaceutical and Biotechnology Logistics Demand

Thailand Cold Chain Logistics Market is further driven by increasing demand for temperature-sensitive pharmaceutical and biotechnology logistics services. Pharmaceutical manufacturers and biotech firms require strict cold storage and refrigerated transportation to maintain product efficacy, particularly for vaccines, biologics, and clinical trial materials. Regulatory compliance mandates precise temperature monitoring, documented handling procedures, and validated storage facilities. Providers implement automated cold storage units, IoT-enabled monitoring systems, and real-time alerts to maintain quality standards. Urban and regional distribution networks facilitate timely delivery to hospitals, pharmacies, and research centers. Expansion of healthcare infrastructure and medical supply chains supports higher volume logistics requirements. Partnerships with hospitals and pharmaceutical distributors enhance operational reach and service reliability. Investments in specialized refrigerated vehicles and packaging solutions ensure product integrity. Technology-enabled inventory management systems enable predictive demand planning. Seasonal fluctuations in vaccine distribution create temporary capacity demand that 3PL providers must accommodate. Staff training in cold chain handling reduces human error and maintains compliance. Integration with digital supply chain platforms improves transparency and traceability. Cross-border pharmaceutical exports generate additional logistics volumes. Real-time tracking and monitoring improve operational efficiency. Strategic location of cold storage hubs near industrial zones and transport networks ensures timely access. Regulatory updates encourage continuous technology adoption. Increasing healthcare product complexity requires specialized cold chain expertise. Collaborative solutions between providers and pharmaceutical firms drive market growth. Innovation in cold chain packaging and transport reduces spoilage and enhances competitiveness.

Market Challenges

High Energy Costs and Refrigeration Infrastructure Maintenance

Thailand Cold Chain Logistics Market faces challenges from high energy costs associated with operating temperature-controlled storage and refrigerated transport fleets. Electricity-intensive cold storage facilities and fuel for refrigerated vehicles increase operational expenditure. Maintenance of refrigeration units, monitoring systems, and backup power systems further escalates costs. Providers must invest in energy-efficient technologies to reduce utility expenses. Aging infrastructure requires continuous upgrades to maintain compliance and service reliability. Operational downtime due to equipment failure impacts delivery schedules. Urban congestion affects vehicle efficiency and increases fuel consumption. Investments in sustainable energy sources and solar-assisted cooling mitigate some costs. Staff training is required to operate refrigeration and monitoring equipment efficiently. Peak demand periods increase energy consumption, straining operational budgets. Expansion of warehouse capacity must consider energy efficiency and cooling reliability. High energy costs limit margins for temperature-sensitive logistics services. Providers must optimize storage layouts, fleet deployment, and route planning to minimize energy use. Regulatory compliance for pharmaceuticals and food safety adds operational complexity. Capital-intensive infrastructure upgrades are required to sustain service quality. Energy management systems help monitor consumption and improve efficiency. Cost pressure may limit service expansion into secondary cities. Balancing operational cost and service quality is critical to competitiveness. Energy expenditure affects pricing strategies and long-term profitability. Efficient maintenance programs enhance reliability and extend equipment life.

Limited Skilled Workforce in Cold Chain Operations

Thailand Cold Chain Logistics Market is challenged by a limited pool of skilled personnel trained in temperature-sensitive handling, monitoring, and regulatory compliance. Refrigeration system operation, packaging protocols, and cold storage management require specialized knowledge to maintain product integrity. Shortages in trained drivers, warehouse staff, and logistics coordinators affect operational efficiency and service reliability. Continuous training programs are necessary to ensure staff competence in handling perishable goods, pharmaceuticals, and biotechnology products. Recruitment and retention of skilled workforce are challenging due to high demand across urban and regional hubs. Labor turnover increases operational disruptions and training costs. Compliance with international quality standards demands ongoing workforce certification and proficiency. Automation reduces some labor dependency, but human oversight remains essential for quality assurance. Workforce constraints limit the ability of providers to scale operations rapidly. Seasonal peaks in food and pharmaceutical demand require temporary skilled staffing. Cross-training in multiple cold chain functions enhances operational flexibility. Staff shortages impact throughput, response time, and service reliability. Collaboration with vocational programs and industry training initiatives can mitigate shortages. Workforce planning and capacity allocation are critical to maintaining service standards. Skilled personnel ensure accurate temperature monitoring, documentation, and regulatory compliance. Operational excellence depends on integrating technology with a competent workforce. Staff retention strategies reduce turnover costs and maintain consistent service delivery. High-quality workforce training supports expansion into new geographic regions. Skilled personnel contribute to operational efficiency, customer satisfaction, and regulatory adherence.

Opportunities

Expansion of Cold Storage Infrastructure for Export-Oriented Food and Seafood Supply Chains

Thailand Cold Chain Logistics Market has significant growth opportunities from expanding cold storage infrastructure supporting food and seafood exports. Export-oriented fisheries, agriculture, and processed food industries require reliable temperature-controlled warehousing and distribution networks. Investment in modern cold storage facilities near production zones and ports improves operational efficiency and reduces spoilage. Providers implement automated storage systems, temperature monitoring, and integrated logistics software to maintain product quality. Government initiatives promoting food export competitiveness incentivize private sector investment. Urban distribution hubs facilitate domestic and regional delivery, supporting both B2B and B2C operations. Strategic partnerships with exporters and retailers increase service adoption. Infrastructure expansion enables scalability to accommodate seasonal and peak production volumes. Integration with refrigerated transport fleets ensures end-to-end cold chain integrity. Technology-enabled monitoring enhances traceability and regulatory compliance. Cold storage capacity expansion attracts investment in energy-efficient refrigeration and sustainable operations. Enhanced infrastructure reduces transit times and improves customer satisfaction. Industrial estate planning supports optimal facility placement. Regional hubs improve distribution to secondary cities. Expansion strengthens Thailand’s position in global food and seafood trade. Co-located logistics parks enable cost-sharing and operational synergies. Advanced infrastructure supports integration with e commerce and retail cold chain networks. Supply chain transparency and reliability drive customer trust and adoption. Growth of export-oriented industries directly fuels cold chain logistics market expansion.

Integration of Technology and Digital Monitoring in Cold Chain Operations

Thailand Cold Chain Logistics Market benefits from opportunities arising from the integration of technology and digital monitoring systems. IoT-enabled sensors, real-time temperature monitoring, and automated reporting enhance operational efficiency, reduce product spoilage, and ensure regulatory compliance. Cloud-based platforms allow centralized control over warehouse conditions, fleet monitoring, and shipment tracking. Predictive analytics support capacity planning, route optimization, and proactive maintenance of refrigeration equipment. Integration with enterprise resource planning systems ensures seamless coordination between storage, transportation, and distribution functions. Automation in sorting, loading, and unloading increases throughput and operational accuracy. Mobile applications provide customers with shipment visibility and notifications, enhancing satisfaction. Technology adoption reduces labor dependency and operational errors. Data analytics improve decision-making and performance monitoring across networks. Digital integration facilitates compliance with international quality and safety standards. Real-time alerts prevent temperature excursions and product loss. Investment in AI and machine learning enables predictive maintenance and workflow optimization. Integration with e commerce and retail platforms streamlines last-mile cold deliveries. Technology-driven monitoring enhances traceability, reporting, and accountability. Fleet management systems optimize refrigerated vehicle utilization. Digital platforms support expansion into new geographic markets. Continuous technology upgrades maintain service reliability and competitiveness. Adoption of innovative solutions enhances Thailand Cold Chain Logistics Market efficiency, scalability, and customer confidence.

Future Outlook

Thailand Cold Chain Logistics Market is expected to grow steadily over the next five years, driven by increasing demand from food, pharmaceutical, and biotechnology sectors. Investments in modern cold storage facilities, automated warehouses, and refrigerated transport fleets will enhance service efficiency. Adoption of digital monitoring, IoT, and AI driven logistics platforms will improve traceability, reduce spoilage, and support regulatory compliance. Expansion of regional distribution hubs and export-oriented logistics infrastructure will strengthen market penetration and operational scalability. Government support and regulatory frameworks will facilitate sustainable growth across the industry.

Major Players

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- CEVA Logistics

- Agility Logistics

- Kerry Logistics

- Yusen Logistics

- Nippon Express

- Toll Group

- CJ Logistics

- Sinotrans Logistics

- DHL Global Forwarding

- Kühne + Nagel Thailand

- Linfox Thailand

- SATS Cold Chain

Key Target Audience

- Food and beverage manufacturers

- Pharmaceutical and biotechnology companies

- Retail and e commerce distributors

- Logistics and cold chain service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Seafood export companies

Research Methodology

Step 1: Identification of Key Variables

Key variables include temperature-sensitive product volumes, refrigerated transport networks, warehouse capacities, export/import volumes, technology adoption, and regulatory compliance requirements affecting the Thailand Cold Chain Logistics Market.

Step 2: Market Analysis and Construction

Market analysis includes evaluating cold storage capacities, refrigerated fleet size, technology integration, shipment volumes, and end-user demand patterns across food, pharmaceutical, and e commerce sectors to construct segmentation and market structure.

Step 3: Hypothesis Validation and Expert Consultation

Research hypotheses are validated through consultations with cold chain operators, logistics managers, industry analysts, and government trade authorities to ensure accuracy of operational, regulatory, and market trend assumptions.

Step 4: Research Synthesis and Final Output

Collected data, expert insights, and secondary sources are synthesized into a structured report providing comprehensive analysis of Thailand Cold Chain Logistics Market size, segmentation, competitive landscape, growth drivers, challenges, and opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising Demand for Perishable and Pharmaceutical Product Distribution

Expansion of E-commerce Grocery and Food Delivery Services

Investment in Temperature-Controlled Infrastructure and Technology - Market Challenges

High Capital Expenditure for Cold Chain Equipment and Warehouses

Fragmented Logistics Providers Across Regions

Regulatory Compliance for Food Safety and Pharmaceutical Transport - Market Opportunities

Adoption of IoT-Enabled Cold Chain Monitoring Solutions

Expansion of Last-Mile Refrigerated Delivery Services

Partnerships Between Logistics Providers and E-commerce Platforms - Trends

Use of Automated Refrigerated Vehicles

Integration of Real-Time Temperature Monitoring Systems - Government Regulations

Food Safety and Cold Chain Compliance Standards

Pharmaceutical Transport Regulations

Incentives for Infrastructure Development - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Trucks and Vehicles

Cold Storage Warehouses

Temperature Monitoring Systems

Refrigerated Containers

Automated Handling Equipment - By Platform Type (In Value%)

Land Transportation Platforms

Air Freight Platforms

Maritime Shipping Platforms

Integrated Multimodal Platforms - By Fitment Type (In Value%)

On-premise Cold Chain Solutions

Cloud-based Cold Chain Solutions

Hybrid Cold Chain Solutions

Modular Refrigeration Solutions - By End User Segment (In Value%)

Pharmaceutical and Healthcare Companies

Food and Beverage Manufacturers

E-commerce Grocery Platforms

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Technology Integration, Automation Level, Geographic Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

CJ Logistics Thailand

Lotte Global Logistics Thailand

Hanjin Transportation Thailand

Hyundai Glovis Thailand

Dongwon Logistics Thailand

Korea Cold Storage Thailand

Hyosung Logistics Thailand

CJ Freshway Logistics Thailand

Orion Logistics Thailand

LF Logistics Thailand

Kerry Logistics Thailand

Maersk Logistics Thailand

DB Schenker Thailand

DHL Supply Chain Thailand

Kuehne + Nagel Thailand

- Increasing Demand from Pharmaceutical Companies for Temperature-Controlled Logistics

- Food and Beverage Companies Expanding Refrigerated Distribution

- E-commerce Platforms Outsourcing Cold Chain Deliveries

- Grocery Retailers Requiring Rapid and Reliable Cold Storage Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now