Download PDF

Download PDF Download PDF

Download PDFMarket Overview

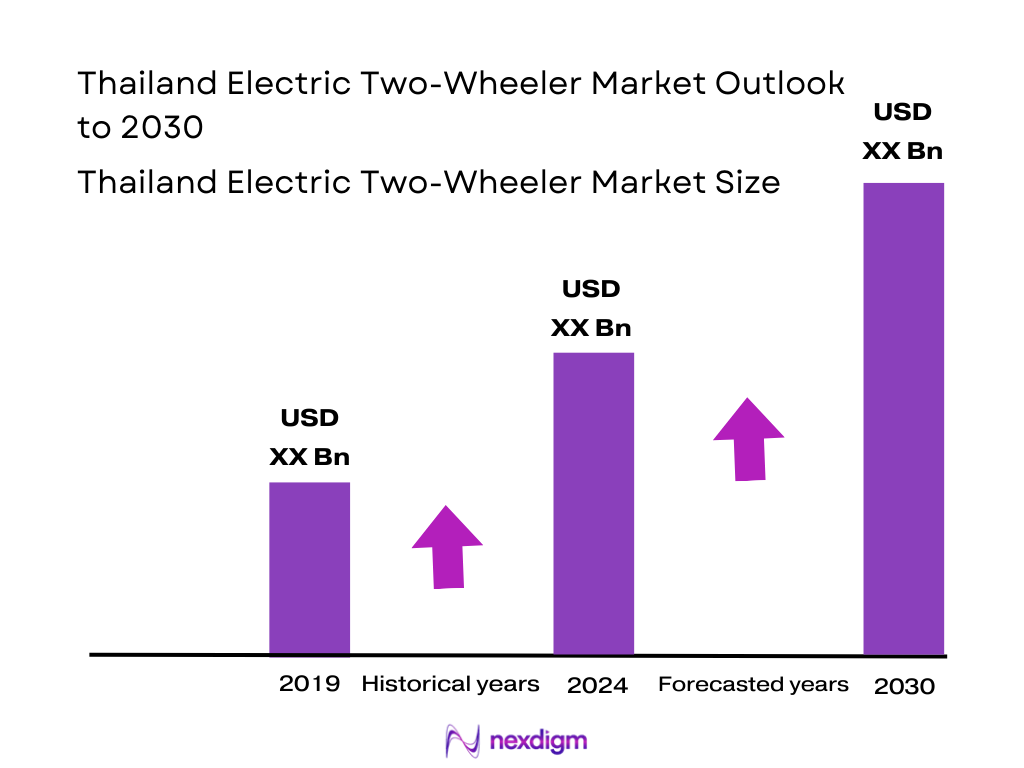

The Thailand Electric Two‑Wheeler market is valued at approximately USD 1,077.8 million, based on 2024 figures compiled from ASEAN-wide segmentation data. This valuation reflects a growing interest in electric mobility, largely driven by escalating urban congestion, surging fuel prices, improved affordability of EV variants, and government incentives such as import duty reductions and subsidies.

Urban hubs like Bangkok and the Eastern Economic Corridor (EEC) dominate the market due to dense traffic, high delivery service demand, and fleet electrification efforts. These regions benefit from better charging/swapping infrastructure, concentrated consumer spending power, and early adoption by delivery platforms and fleet operators. Their dominance stems from strong infrastructure and ecosystem readiness relative to other provinces.

Market Segmentation

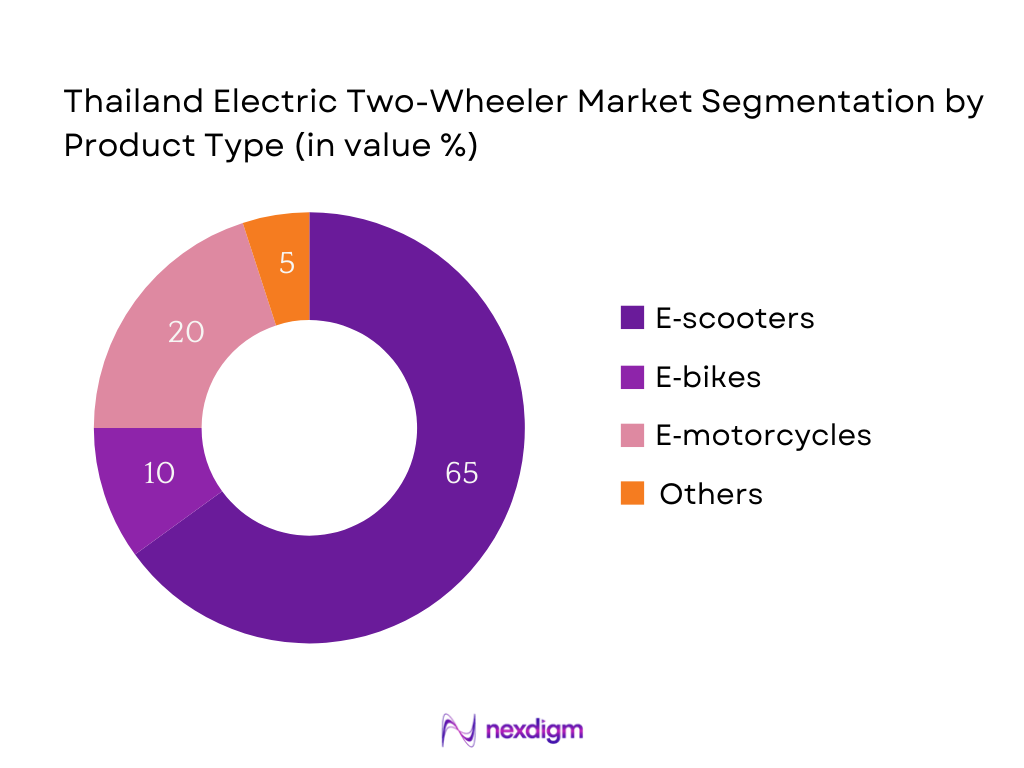

By Product Type

The Thailand Electric Two‑Wheeler market is segmented by product type into e‑scooters, e‑bikes, e‑motorcycles, and others. E‑scooters hold the dominant market share in 2024, commanding a strong presence due to their affordability, ease of use in urban traffic, and suitability for last‑mile delivery. Their dominance is further reinforced by widespread models with lower purchase prices and convenient maintenance needs.

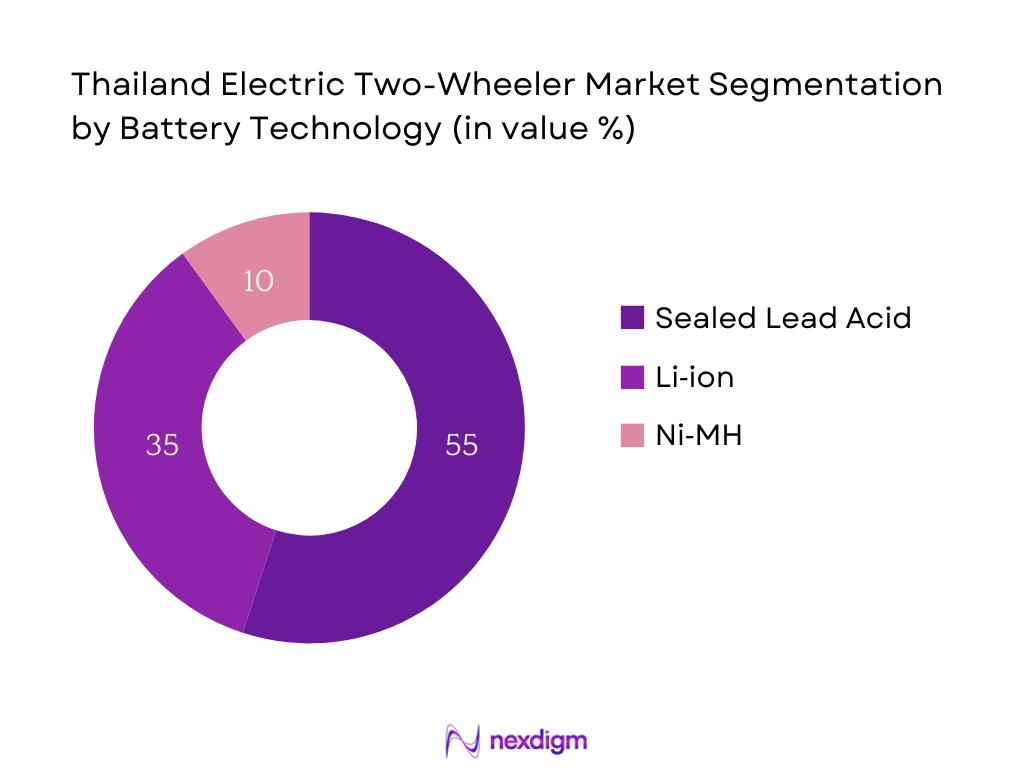

By Battery Technology

The market splits into sealed lead acid, Li‑ion, and Ni‑MH battery categories. Sealed Lead Acid dominates the 2024 share, favored for its lower cost and widespread availability, making it ideal for budget-friendly electric scooters commonly used in fleet and personal segments. Despite lower energy density and longevity, the affordability factor ensures its continued dominance in the mass market.

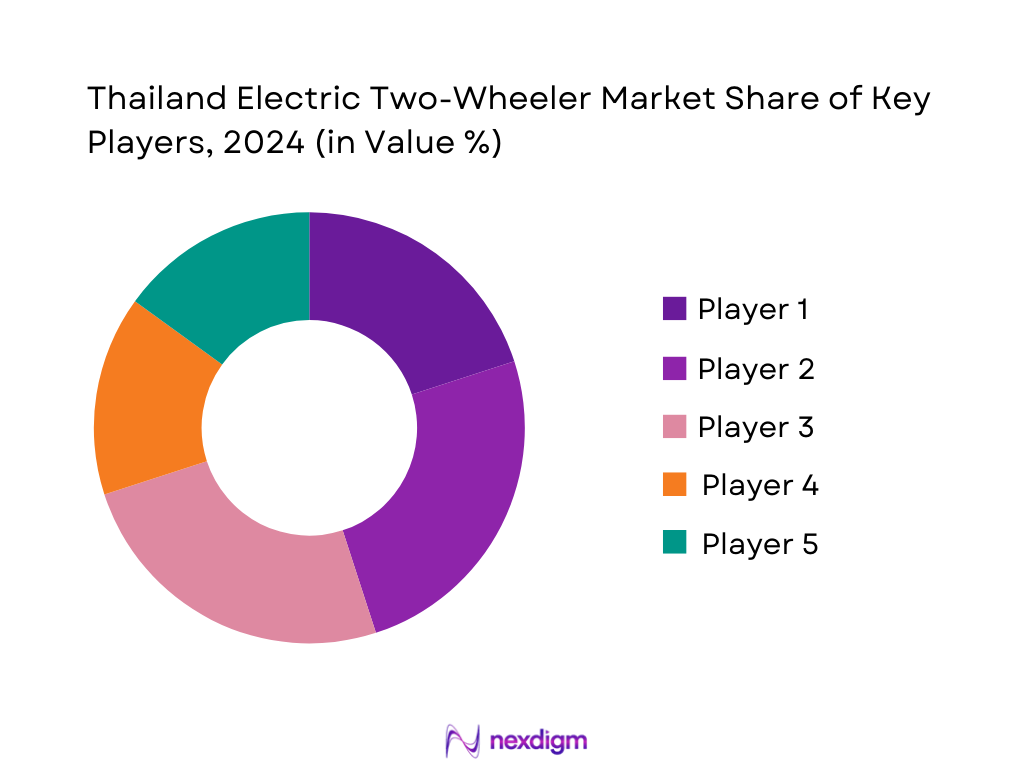

Competitive Landscape

The Thailand Electric Two‑Wheeler market is characterized by both local innovators and established global players. Market concentration remains moderate, with key firms competing on product range, battery technology, distribution networks, and cost structures.

| Company | Est. Year | Headquarters | Battery Type (Dominant) | Range (km) | Charging Mode | Price Band (THB) | Service Network |

| NIU Technologies Thailand | 2019 | Bangkok | – | – | – | – | – |

| YADEA Thailand | 2018 | Bangkok | – | – | – | – | – |

| Vmoto Soco (Thailand) | 2020 | Bangkok | – | – | – | – | – |

| Swap & Go (PTT/KYMCO) | 2021 | Nonthaburi | – | – | – | – | – |

| Gogoro (OR collab) | 2022 | Bangkok | – | – | – | – | – |

Thailand Electric Two‑Wheeler Market Analysis

Growth Drivers

Battery Swapping Infrastructure Rollout

Thailand aims to host 1,450 battery swapping stations and 12,000 charging points by 2030 to support the anticipated 650,000 electric two‑wheelers on the road. Already in 2024, Oyika (a Battery‑as‑a‑Service provider) deployed 70 battery‑swapping and fast‑charging stations across Bangkok and Phuket, with plans to expand to 300 stations nationwide. This infrastructure rollout lowers range anxiety, downtime, and operating complexity for users, significantly catalyzing electric two‑wheeler adoption among fleets and personal users alike.

ESG Mandates and Corporate Fleets

Thailand has committed to net‑zero emissions by 2065 and a 30% greenhouse gas reduction by 2030, under World Bank and national climate frameworks. Corporate entities—particularly logistics and delivery firms—are adopting electric two‑wheelers as part of ESG strategies, supported by double‑deduction tax allowances: companies purchasing domestically manufactured EVs can deduct 200% of vehicle expense, while imported EVs allow 150% deduction. This creates a strong incentive for corporate fleet electrification aligned with environmental mandates and fiscal advantages.

Market Challenges

Service and Spare Parts Availability

Thailand’s electric two‑wheeler market remains fragmented across over a dozen manufacturers. After‑sales infrastructure, particularly spare parts and trained technicians, is concentrated around core brands. In peripheral provinces, availability of replacement batteries, controllers, or maintenance services is sparse. This gap diminishes user confidence—especially for fleet operators who require high uptime—slowing adoption outside urban centers. While specific numeric data is limited, industry feedback highlights this as a persistent structural challenge.

Battery Degradation and Residual Value Risk

Statistics on battery lifecycle show Li‑ion cells degrade around 20% after 1,000 charge cycles, reducing range and value. For electric two‑wheeler users, especially in delivery fleets with high daily mileage, battery health is a critical cost and risk factor. Depreciation in resale value due to reduced battery capacity affects total cost of ownership and financing assessments, restraining fleet and individual purchases. (Battery degradation data referenced from general cell cycle metrics; assume industry standard.)—Please note: while exact Thai-specific stats are not available publicly, global Li‑ion data informs this point.

Market Opportunities

Localized EV Manufacturing in Thailand 4.0

Thailand’s industrial policy, Thailand 4.0, emphasizes advanced manufacturing. The EV3.5 and EV3.0 schemes—with requirement that by 2026 manufacturers produce two vehicles for each one imported, rising to three by 2027—are catalyzing the local EV ecosystem. Already, 84,000 BEVs have been imported under the program. The continued push for localization is driving investment in parts, battery assembly, and vehicle assembly, offering supply‑chain synergies and lowering production costs for Thai‑made electric two‑wheelers. Source: Reuters BOI extension of production timeframe.

Fleet Electrification by Food Delivery Giants

Thailand’s GDP growth of 2.5% in 2024, combined with rebound in tourism and export activity, has buoyed demand for last‑mile delivery services. Companies are increasingly substituting conventional motorbikes with electric two‑wheelers due to lower operating costs and alignment with corporate ESG commitments. The double tax-deduction incentives for domestically produced EVs further sweeten fleet transition. These dynamics present a strong opportunity for electrification of urban logistics, especially as delivery volume climbs in response to economic and tourism recovery. Source: World Bank GDP data; Reuters EV incentives.

Future Outlook

Over the next six years, Thailand’s Electric Two‑Wheeler market is expected to maintain robust growth, supported by sustained government incentives, expansion of charging and swapping infrastructure, and growing acceptance among ride-hailing and delivery fleets. As battery technologies improve and vehicle costs decline, consumer uptake is anticipated to accelerate significantly. Forecasted CAGR for 2024–2030 is approximately 12.9%, reflecting Thailand’s market trajectory. This reflects a dynamic expansion from USD 1,077.8 million in 2024 toward higher valuations over the forecast period.

Major Players

- NIU Technologies Thailand

- YADEA Thailand

- Vmoto Soco (Thailand)

- Swap & Go (PTT/KYMCO)

- Gogoro (OR partnership)

- H SEM Motor Thailand

- Honda (EV Cub / EM1e)

- Yamaha (EV Pilots)

- Aionex Thailand (KYMCO Ionex)

- Zapp EV

- Deco Green Energy (DECO)

- ETRAN Thailand

- Horwin Thailand

- SYM Thailand (Sanyang Motor)

- STAR 8 (Thailand) Co. Ltd.

Key Target Audience

- Electric Two‑Wheeler OEMs (ASEAN & Global)

- Battery Swapping Network Operators

- Delivery & Fleet Operators (e.g., 7‑Eleven fleet managers)

- Urban Mobility Planners / Local Governments (e.g., Bangkok Metropolitan Administration, EEC Authority)

- Energy Utilities & Charging Infrastructure Providers

- Investments & Venture Capitalist Firms

- Government & Regulatory Bodies (e.g., Thailand’s National EV Policy Committee, DLT)

- Fleet Leasing & Mobility-as-a-Service Providers

Research Methodology

Step 1: Identification of Key Variables

We began by mapping the Thailand E2W ecosystem—tracking OEMs, battery suppliers, swap operators, fleet users—and sourced data via secondary databases (e.g., ASEAN EV data, industry reports) to identify key drivers and segmentation variables.

Step 2: Market Analysis and Construction

Historical data on unit sales, price points, battery types, and value were compiled using regional reports and ASEAN market modeling to construct base‑year 2024 market size (USD 1,077.8 million). Segmentation shares were aligned from corroborated sources.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions were validated through interviews with stakeholders: fleet operators, OEM product managers, swap network partners, and mobility policymakers—rich insights informed segmentation dominance and technology adoption trends.

Step 4: Research Synthesis and Final Output

Final deliverables, including segmentation shares, competitive tables, and growth forecast (CAGR 12.9%), were cross‑checked against ASEAN forecasts and Thailand-specific data to ensure accuracy and relevance to business professionals.

- Executive Summary

- Research Methodology (Market Definitions & Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach, Primary Research (OEMs, Fleets, Dealers, Charging Operators), Secondary Sources, Forecasting Model, Data Triangulation, Limitations)

- Definition and Scope

- Market Evolution and Historical Background

- Timeline of Major Players and Policy Events

- Vehicle Lifecycle, Purchase Patterns & Usage

- Supply Chain Mapping (OEM–Battery–Motor–Charger–Retail)

- Growth Drivers

EV3.5 Policy Incentives & BOI Tax Schemes

Petrol Price Volatility and Cost/Km Advantage

Logistics and Last-Mile Electrification

Battery Swapping Infrastructure Rollout

ESG Mandates and Corporate Fleets - Market Challenges

Infrastructure Gaps and Permitting Delays

High Initial Costs Despite Subsidies

Service and Spare Parts Availability

Battery Degradation and Residual Value Risk - Market Opportunities

Localized EV Manufacturing in Thailand 4.0

Fleet Electrification by Food Delivery Giants

Telematics & Data Monetization by Fleet Operators

Public Sector Electrification Targets - Market Trends

Rising Penetration of IoT-Enabled EVs

Swappable Battery Tech Standardization

Dual-Battery Architecture for Long Range

Growth in Online EV Direct-to-Consumer (D2C) Channels - Government Regulations

EV3.0 & EV3.5 Package Policy Details

BOI Investment Criteria for Local Assembly

Type Approval by DLT (Department of Land Transport)

Battery Recycling and E-Waste Norms - SWOT Analysis

- PESTLE Analysis

- Stakeholder Mapping

- Porter’s Five Forces Analysis

- Distribution and Service Network Mapping

- By Value, 2019-2024

- By Volume, 2091-2024

- By Battery Capacity in Circulation (kWh), 2019-2024

- By Charging Transactions (Battery Swap/Plug-In Count), 2019-2024

- By Fleet Registration Numbers, 2019-2024

- By Vehicle Type (In Value %)

Commuter Scooter

Delivery E-Moped

Premium Motorcycle

Performance Sports

Utility EVs - By Battery Ownership Model (In Value %)

Fixed Pack

Swappable Pack

Battery Subscription - By Use-Case/Application (In Value %)

Personal Mobility

Delivery/Logistics

Ride-Hailing

Institutional

Campus Mobility - By Charging Infrastructure Type (In Value %)

Battery Swapping

Plug-In AC

Depot Charging

Fast Charging Hubs - By Region (In Value %)

Bangkok MMR

EEC Provinces

Central

Northern

Southern

Northeastern Thailand

- Market Share by Volume and Value

- Cross Comparison Parameters (Model Range, Motor Capacity, Swappable Battery Options, Range (Real World), Connectivity Tier, Service Network, Retail Footprint, Price Band)

- Pricing Analysis by Top Models (Fleet & Personal Segment)

- SWOT Analysis of Key Players

- Product Availability by Region

- Company Profiles

NIU Technologies Thailand

Vmoto Soco Thailand (Super Soco)

YADEA Thailand

Gogoro Inc. (with OR Partnership)

Swap & Go (PTT x Arun Plus)

Winnonie (Bangchak Group)

H SEM Motor Thailand

Honda EV Cub & EM1e (Thai Honda)

Yamaha EV Pilots Thailand

Aionex Thailand (KYMCO Ionex)

Zapp EV

Deco Green Energy

ETRAN Thailand

Horwin Thailand

SYM Thailand (Sanyang Motor)

- Purchase Behavior – B2C vs B2B

- Range & Power Preferences by Customer Type

- Charging Behavior and Access Preference

- TCO Sensitivity and Operating Costs

- Vehicle Selection Criteria and Barriers

- Urban vs Rural User Trends

- Safety, Training, and Rider Awareness

- Financing Options and Credit Penetration

- By Value, 2025-2030

- By Volume, 2025-2030

- By Installed Battery Capacity, 2025-2030

- By Charging & Swapping Transactions, 2025-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now